Managing your mortgage closure requires understanding how your remaining funds are applied. An Escrow Balance Application Payoff Letter formally requests that your lender uses held escrow funds to reduce your final loan balance rather than issuing a refund check later. This process accelerates debt clearance and ensures financial accuracy during settlement. To simplify your request, below are some ready to use template.

Image cover: Applying Your Escrow Balance to Your Mortgage Payoff: Request Letter Templates and Guide

Letter Samples List

- Escrow Balance Application Payoff Letter

- Final Mortgage Payoff Demand Letter

- Escrow Overage Refund Authorization Letter

- Annual Escrow Account Analysis Letter

- Mortgage Satisfaction And Release Letter

- Escrow Shortage Notice And Collection Letter

- Mortgage Payoff Quote Request Letter

- Notice Of Escrow Account Closure Letter

- Escrow Holdback Agreement Letter

- Escrow Funds Disbursement Authorization Letter

- Notice Of Mortgage Servicing Transfer Letter

- Escrow Waiver Application Request Letter

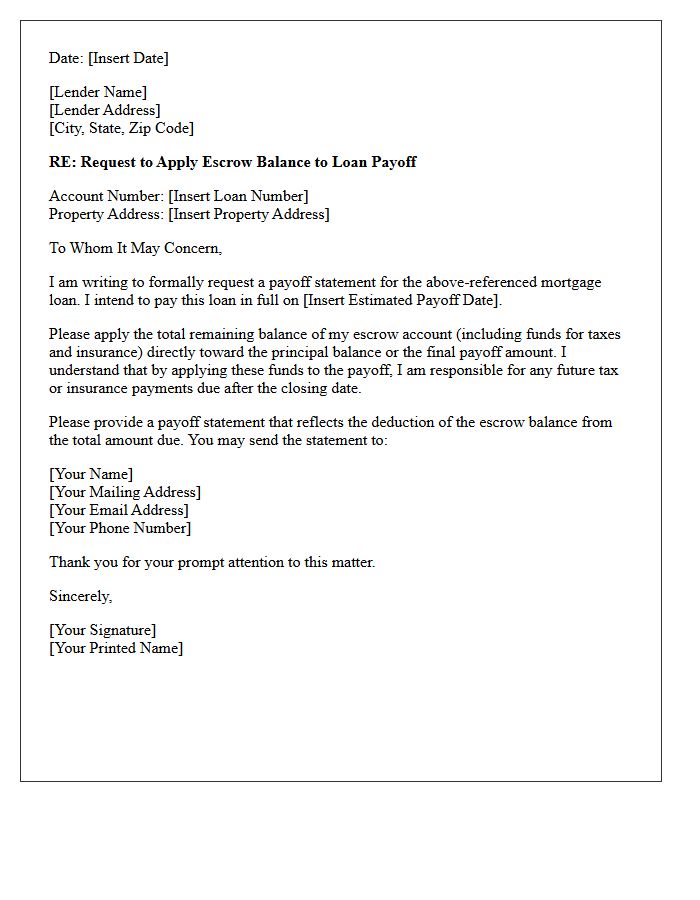

Escrow Balance Application Payoff Letter

An Escrow Balance Application Payoff Letter is a legal document confirming that your remaining escrow funds will be applied directly toward the final mortgage principal. Instead of receiving a separate refund check after closing, these funds reduce the total payoff amount required to satisfy the loan. Homeowners should verify the net payoff figure to ensure all tax and insurance reserves are accurately credited. This process simplifies the mortgage satisfaction by using existing equity to cover the remaining debt balance efficiently during the final settlement.

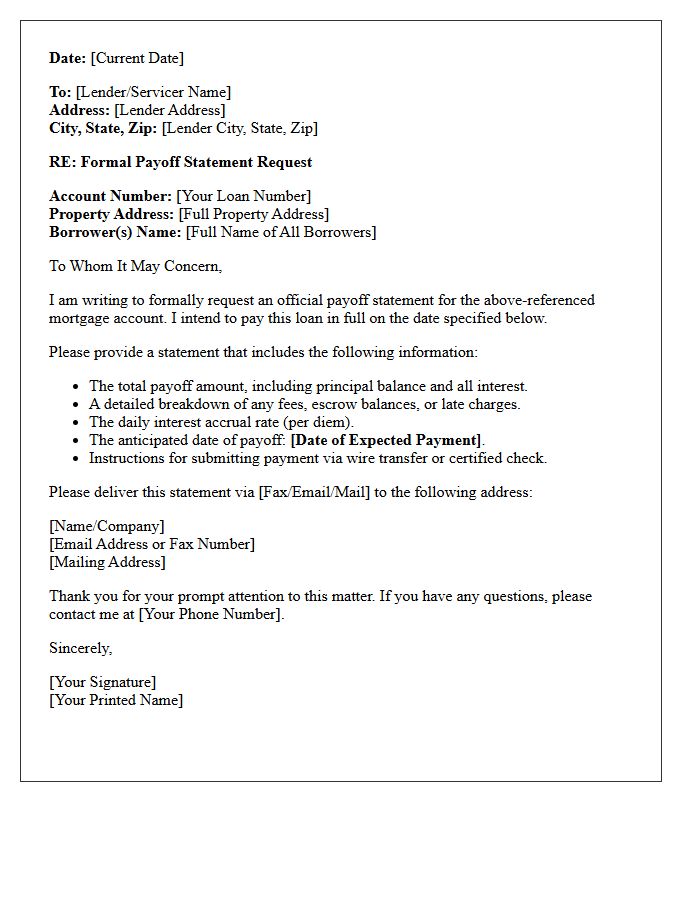

Final Mortgage Payoff Demand Letter

A Final Mortgage Payoff Demand Letter is a legal document issued by your lender providing the exact amount required to fully satisfy your loan balance. This statement includes the remaining principal, accrued interest, and administrative fees, valid until a specific expiration date. It is essential for ensuring your lien is released and your credit reflects the debt as paid. Borrowers must request this document before closing a home sale or refinancing to guarantee a zero balance and avoid unexpected charges or delays in the transfer of title.

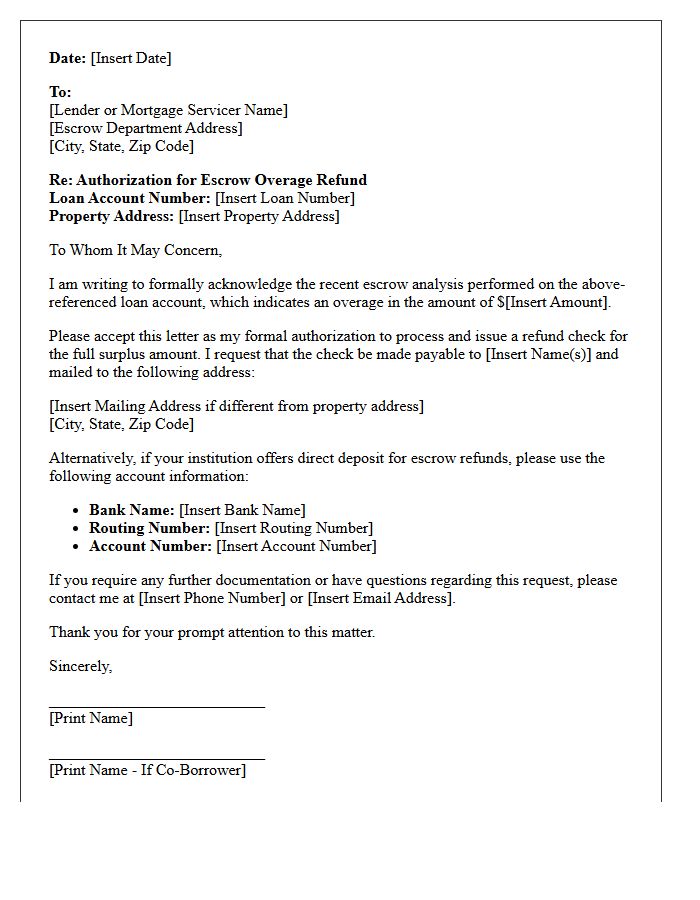

Escrow Overage Refund Authorization Letter

An Escrow Overage Refund Authorization Letter is a formal document used to request the release of surplus funds from a mortgage impound account. This occurs when property taxes or insurance premiums are lower than estimated, creating a financial surplus. Homeowners must submit this signed authorization to their loan servicer to confirm their current mailing address and preferred payment method. Providing accurate details ensures the surplus reimbursement is processed quickly, preventing delays in returning excess money back to the borrower after an annual escrow analysis.

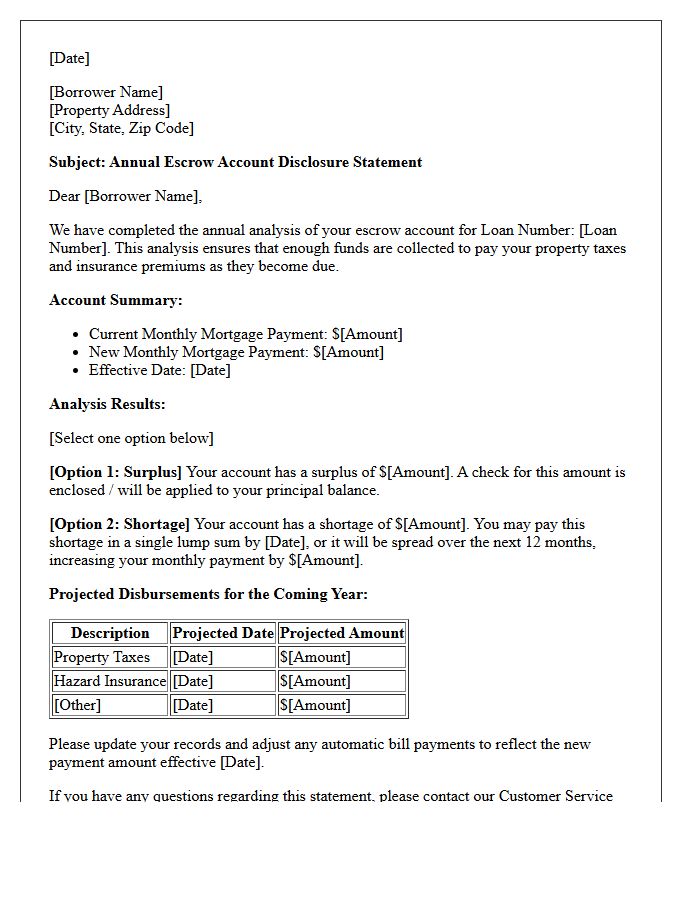

Annual Escrow Account Analysis Letter

An Annual Escrow Account Analysis is a mandatory statement reviewing your property taxes and insurance payments. It ensures your monthly mortgage payment accurately covers these fluctuating costs. If your tax or insurance rates increased, you may face an escrow shortage, requiring a higher payment or a one-time catch-up fee. Conversely, a decrease could result in an escrow overage refund. Carefully review this letter to understand upcoming changes to your total monthly obligation and to verify that your servicer is managing your funds correctly to prevent unexpected financial gaps.

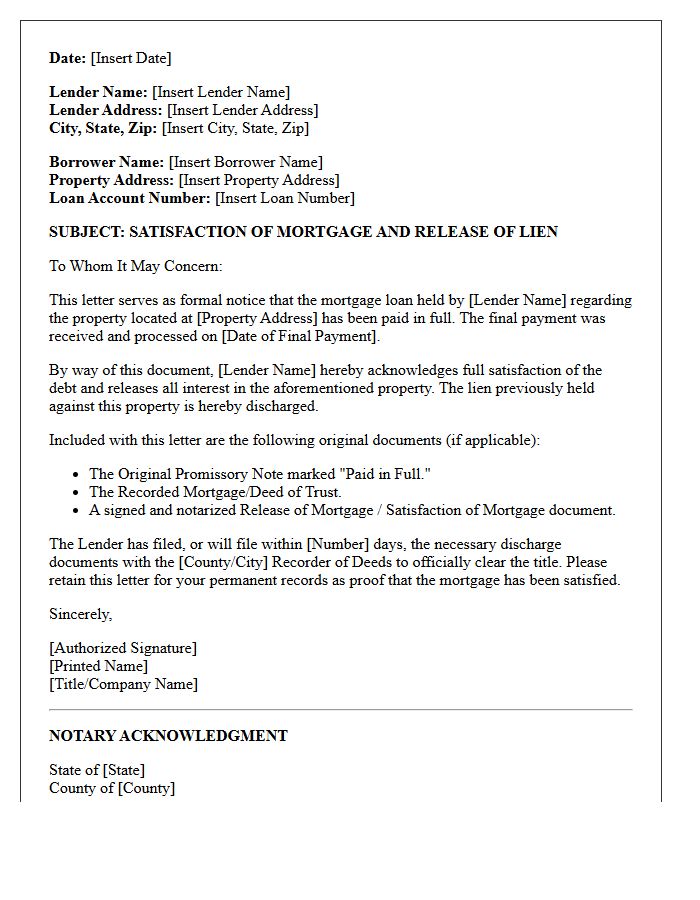

Mortgage Satisfaction And Release Letter

A Mortgage Satisfaction and Release Letter is a legal document confirming your loan is fully repaid. Once issued by the lender, it must be recorded with the local land registry to clear the title of the property. This process removes the lien, proving you hold full ownership without debt obligations. Homeowners should verify this filing to avoid title defects during future sales or refinancing. Always retain a copy of this official discharge as permanent proof that the mortgage contract is legally terminated and the lender no longer has a claim.

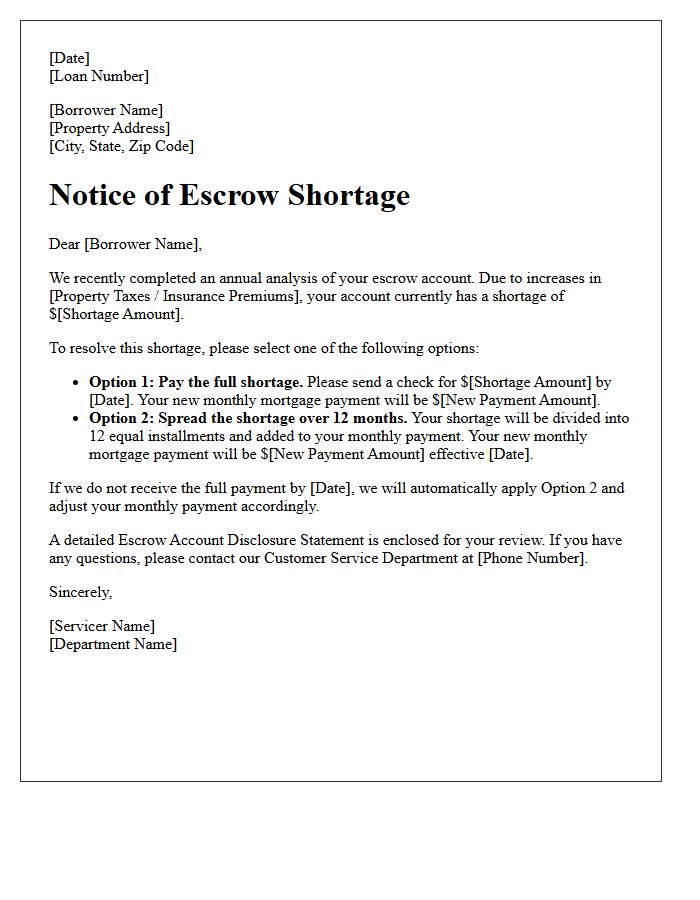

Escrow Shortage Notice And Collection Letter

An escrow shortage notice informs homeowners that their property tax or insurance payments increased, causing a deficit in their escrow account. Lenders issue a collection letter to recover these funds and adjust future monthly payments. To resolve this, you can usually pay the shortage amount in a single lump sum or spread the balance over the next twelve months. Promptly addressing this notice prevents significant spikes in your mortgage payment and ensures your required obligations remain fully funded throughout the year.

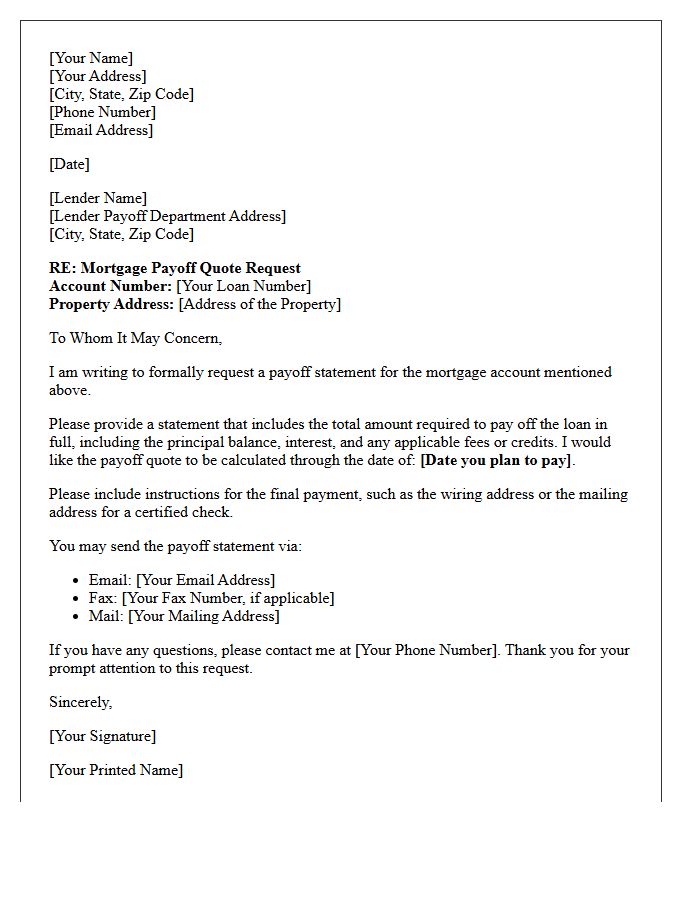

Mortgage Payoff Quote Request Letter

A Mortgage Payoff Quote Request Letter is a formal document sent to your lender to obtain the exact total balance required to settle your loan in full. This statement accounts for the remaining principal, daily interest accruals, and any applicable prepayment penalties or fees. To ensure accuracy, include your loan account number and a specific requested payoff date. Receiving this written quote is essential for homeowners planning to refinance or sell their property, as it provides a clear financial roadmap for closing the account and releasing the property lien.

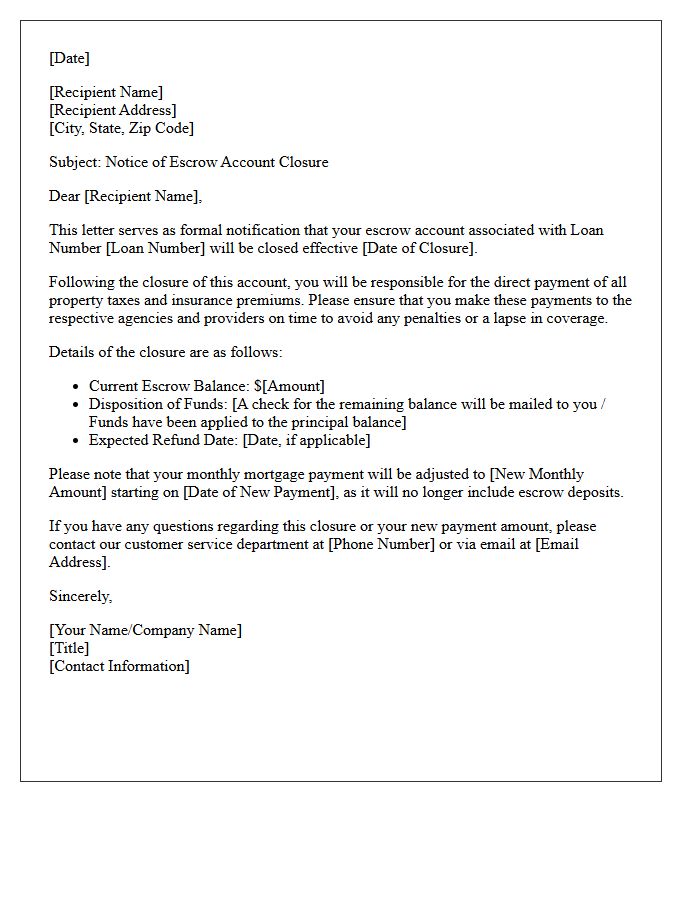

Notice Of Escrow Account Closure Letter

A Notice of Escrow Account Closure is a formal document informing homeowners that their mortgage servicer will no longer manage property tax and insurance payments. Once the account is closed, the borrower becomes personally responsible for paying these bills directly to the relevant authorities. It is crucial to monitor deadlines to avoid late fees or lien placements on the property. Ensure you have sufficient funds set aside, as you will no longer make monthly escrow deposits, shifting the full financial obligation to your direct oversight and manual payment schedule.

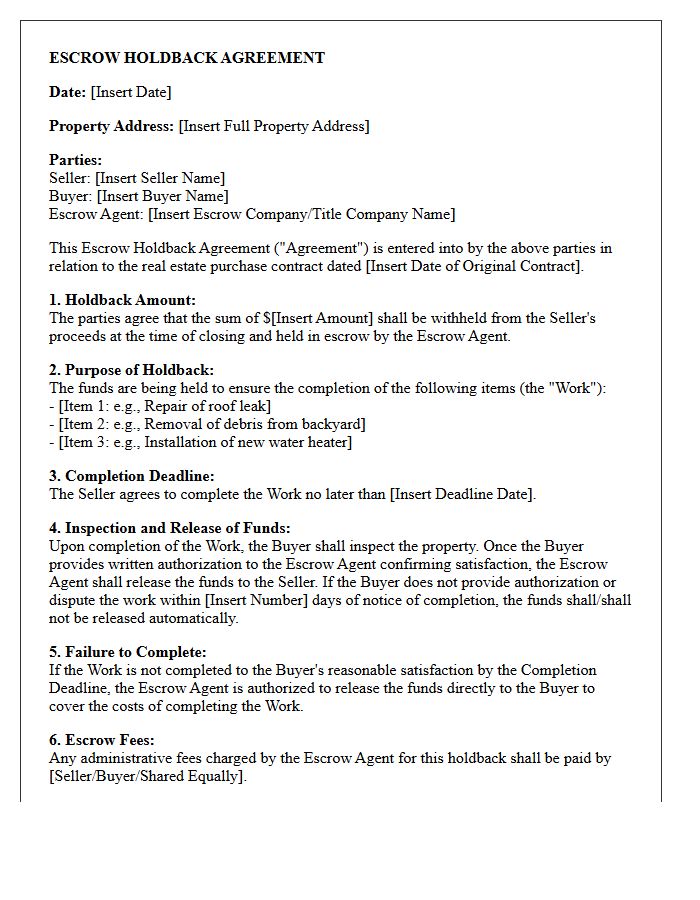

Escrow Holdback Agreement Letter

An Escrow Holdback Agreement Letter is a legal document used during real estate closings to delay the release of specific funds. It ensures that the seller completes required repairs or property improvements after the title has transferred. The withheld money is kept in a neutral account until the specified conditions are met and verified by an inspection. This agreement protects the buyer's interests by providing financial security against unfinished work, while allowing the transaction to proceed on schedule despite outstanding minor issues or seasonal maintenance delays.

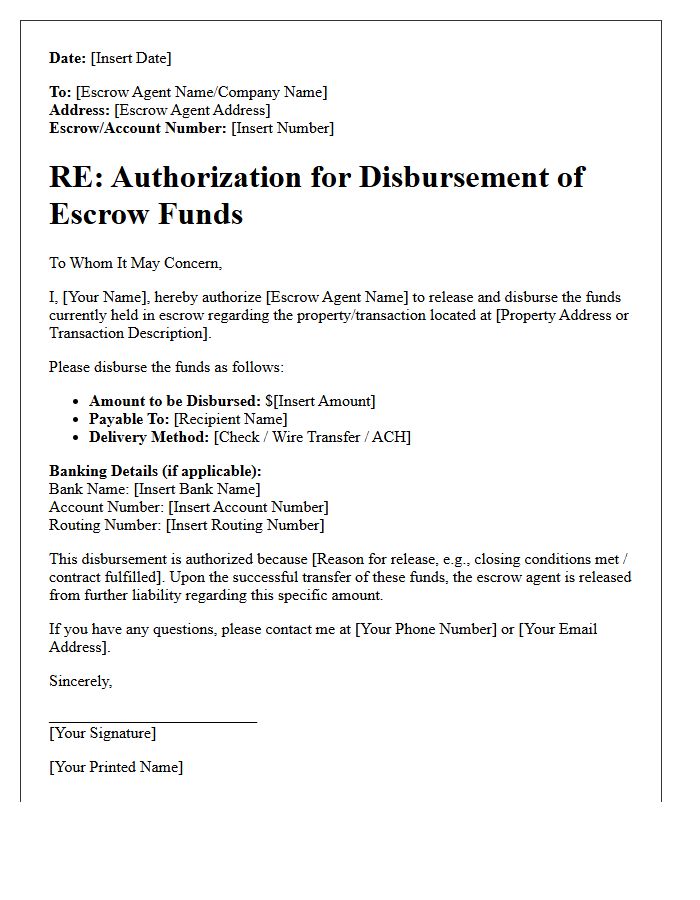

Escrow Funds Disbursement Authorization Letter

An Escrow Funds Disbursement Authorization Letter is a formal legal document that instructs an escrow agent to release specific funds to designated parties. It serves as written verification that all contractual contingencies have been satisfied. This letter must include the precise amount, the recipient's payment details, and the authorizing signatures of the involved parties. It ensures transparency and security, protecting both buyers and sellers by preventing the unauthorized transfer of money until the closing process is legally complete. Without this signed directive, the escrow holder cannot legally distribute the held assets.

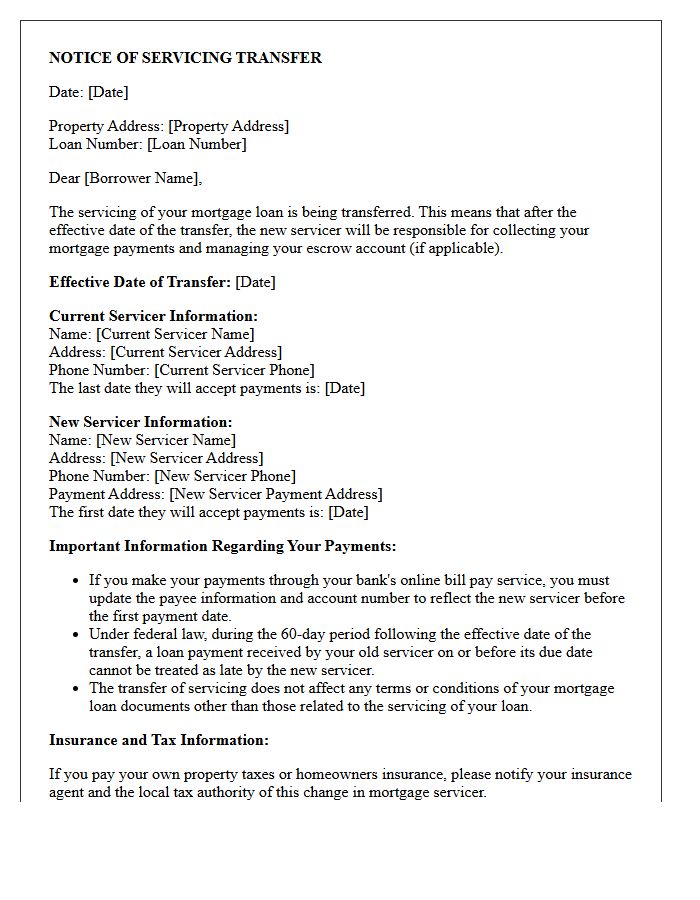

Notice Of Mortgage Servicing Transfer Letter

A Notice of Mortgage Servicing Transfer is a legal document informing you that a new company will manage your loan payments. By law, your current servicer must notify you 15 days before the change, and the new servicer must do so within 15 days after. This transition does not change your loan terms, interest rate, or balance. Always verify the new servicer's details to avoid payment scams and ensure your escrow accounts transfer correctly to prevent missed property tax or insurance payments during the transition period.

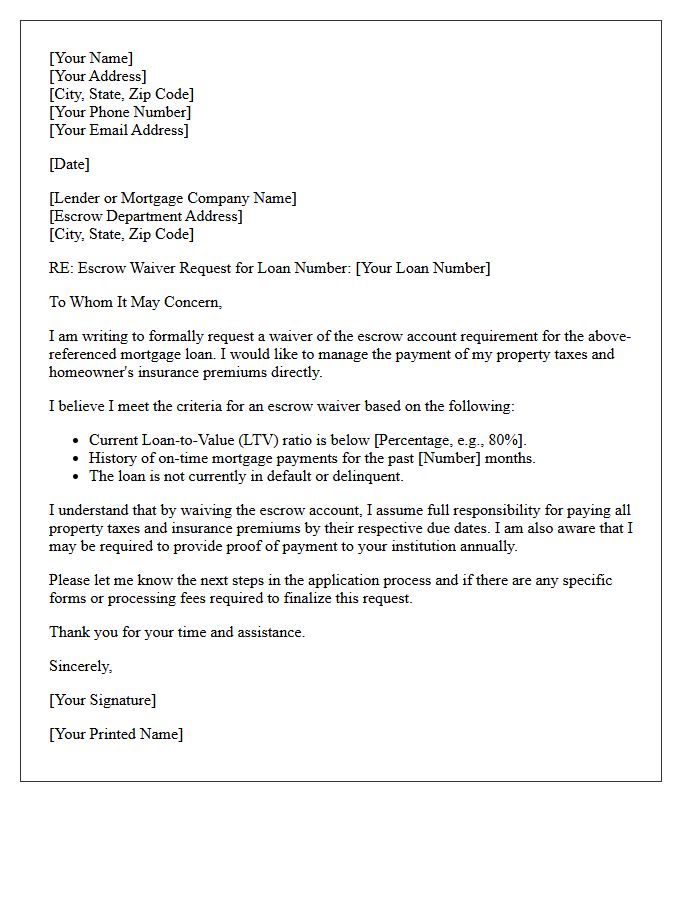

Escrow Waiver Application Request Letter

An Escrow Waiver Application Request Letter is a formal document sent to a mortgage lender to request the removal of an impound account. Homeowners use this to manage their own property taxes and homeowners insurance payments directly rather than through the servicer. To qualify, you typically need a specific loan-to-value (LTV) ratio, often 80% or less, and a history of on-time payments. Clearly state your loan number and intent to demonstrate financial responsibility. Successful approval provides greater control over your cash flow and potential interest earnings on withheld funds.

What is an escrow balance in a payoff letter?

An escrow balance in a payoff letter represents the remaining funds held by your lender for the payment of property taxes and homeowners insurance. When requesting a payoff statement, this balance is typically applied as a credit to reduce the total amount required to satisfy the mortgage debt.

How is the escrow credit applied to my final mortgage payoff?

Most lenders automatically deduct the existing escrow balance from the outstanding principal and interest to provide a "net payoff" figure. If the escrow is not applied directly to the payoff amount, the lender will instead issue a refund check for the balance within 20 to 30 days after the loan is closed.

Can I use my escrow balance to lower my final payoff amount?

Yes, you can request that the lender apply your current escrow funds toward the final payoff of your loan. This is common practice in "netting the escrow," which ensures you do not have to pay the full principal balance out of pocket only to wait for a refund check later.

Why does my payoff letter show a different amount than my monthly statement?

Your payoff letter includes the principal balance plus prorated interest, recording fees, and statement fees, minus any applied escrow credits. Your monthly statement only shows the current principal and does not account for the daily interest accrual or the final application of escrow funds.

What happens if there is a shortage in my escrow account at the time of payoff?

If your escrow account has a negative balance or a shortage, this amount will be added to your total payoff figure. To receive a clear title, you must cover the outstanding principal, interest, and any escrow deficiencies identified in the payoff letter.

Comments