Securing a renovation loan pre-approval letter is a critical first step in financing your home improvements. It proves your borrowing capacity to contractors and sellers, ensuring your project stays on budget and schedule. This official document validates your financial readiness and streamlines the lending process. To help you get started immediately, below are some ready to use template.

Image cover: Home Renovation Loan Pre-Approval Letter: Professional Templates and Examples

Letter Samples List

- Standard Renovation Loan Pre-Approval Letter

- Conditional Renovation Loan Pre-Approval Letter

- FHA 203(k) Renovation Loan Pre-Approval Letter

- Conventional HomeStyle Renovation Loan Pre-Approval Letter

- VA Renovation Loan Pre-Approval Letter

- Jumbo Renovation Loan Pre-Approval Letter

- Investment Property Renovation Loan Pre-Approval Letter

- Second Home Renovation Loan Pre-Approval Letter

- Contractor Contingent Renovation Loan Pre-Approval Letter

- Increased Renovation Loan Pre-Approval Letter

- Renovation Loan Pre-Approval Extension Letter

- Renovation Loan Pre-Approval Denial Letter

- Expired Renovation Loan Pre-Approval Letter

Standard Renovation Loan Pre-Approval Letter

A Standard Renovation Loan Pre-Approval Letter is a critical document confirming a lender's preliminary commitment to fund both your home purchase and renovation costs. It specifies a maximum loan amount based on your creditworthiness and the property's projected after-repair value. Having this letter strengthens your negotiating power with sellers, proving you possess the guaranteed financing necessary to complete extensive repairs. It is essential for streamlined budgeting, ensuring you only bid on properties where the combined acquisition and construction budget aligns with bank requirements.

Conditional Renovation Loan Pre-Approval Letter

A Conditional Renovation Loan Pre-Approval Letter is a critical document indicating a lender's preliminary commitment to fund both your home purchase and planned improvements. It outlines the specific financial requirements, such as credit scores and debt-to-income ratios, that must be verified. Unlike standard letters, it depends on the after-improved value of the property determined by an appraisal. Securing this letter proves to sellers that you have the financing capacity to manage a fixer-upper project, making your offer more competitive while establishing a clear renovation budget for contractors.

FHA 203(k) Renovation Loan Pre-Approval Letter

An FHA 203(k) pre-approval letter is a critical document verifying a borrower's eligibility to finance both the home purchase and renovation costs through a single mortgage. Unlike standard letters, it confirms the lender has vetted your creditworthiness specifically for rehabilitation projects. This letter demonstrates to sellers that you have the financial backing to handle distressed properties or necessary repairs. Securing this early is essential for budgeting, as it outlines your total borrowing capacity, ensuring you can cover the acquisition price plus all planned structural or cosmetic improvements.

Conventional HomeStyle Renovation Loan Pre-Approval Letter

A HomeStyle Renovation Loan Pre-Approval Letter proves you are qualified to finance both the home purchase and remodeling costs through a single conventional mortgage. Unlike standard letters, it verifies your eligibility for higher loan-to-value limits based on the as-completed value of the property. This document is essential for making competitive offers on fixer-uppers, as it assures sellers and contractors that you have secured funding for extensive structural or cosmetic home improvements. Obtaining this letter requires a thorough credit review and debt-to-income analysis by a Fannie Mae-approved lender.

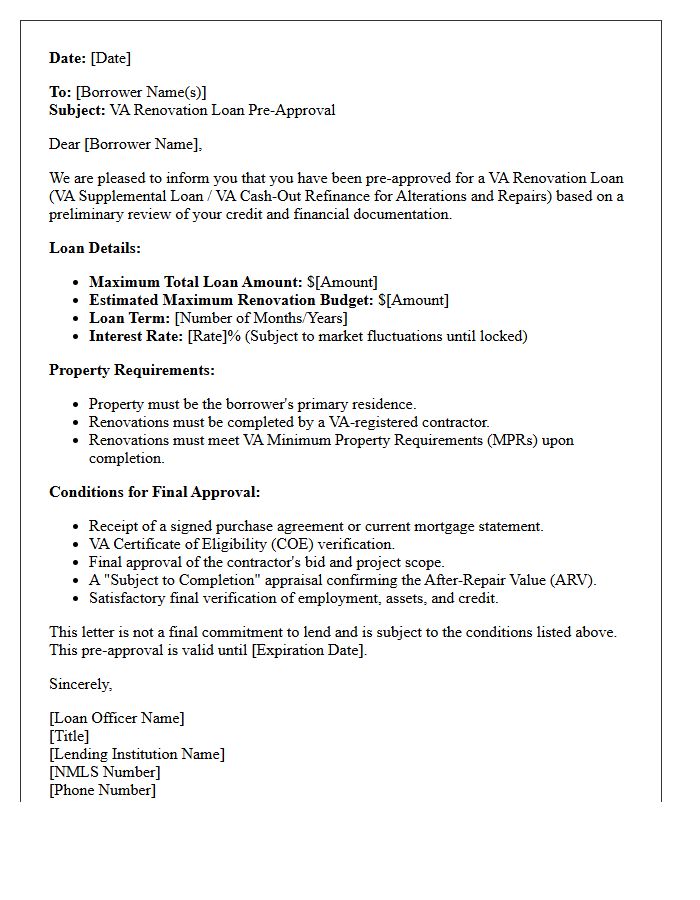

VA Renovation Loan Pre-Approval Letter

A VA Renovation Loan Pre-Approval Letter is a vital document confirming a Veteran's eligibility and borrowing capacity for both property purchase and home improvements. Unlike standard letters, it accounts for the after-improved value of the residence. This letter signals to sellers that the buyer is financially vetted for a complex government-backed renovation product. Obtaining this requires a specialized lender to review credit, income, and initial project feasibility. It is the essential first step in securing a one-time-close loan that combines mortgage and remodeling costs into a single monthly payment.

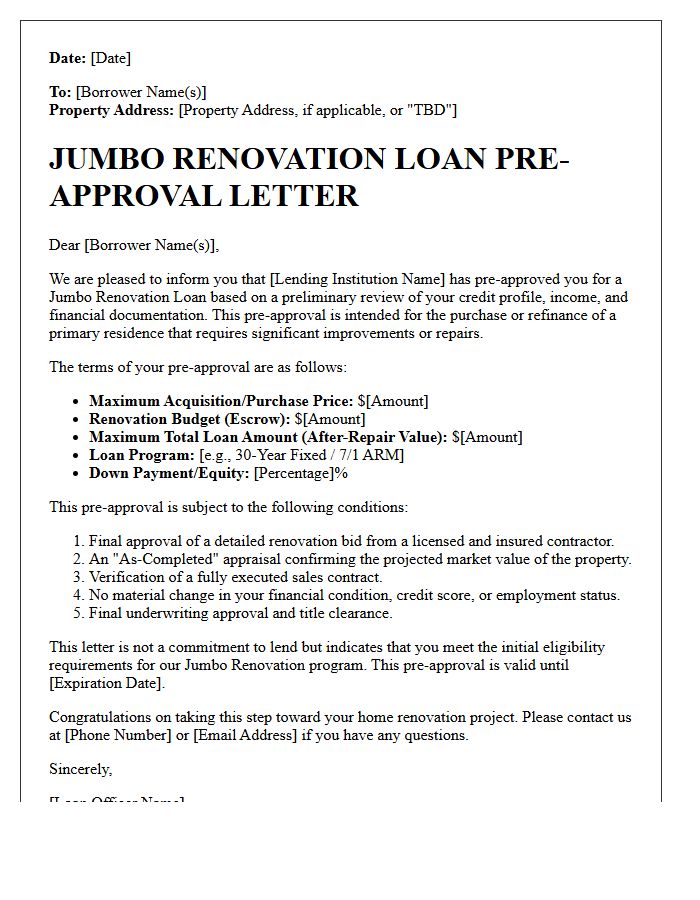

Jumbo Renovation Loan Pre-Approval Letter

A Jumbo Renovation Loan Pre-Approval Letter is a vital document for high-end homebuyers seeking to finance both a luxury property and its extensive remodeling costs through a single mortgage. Unlike standard loans, this letter confirms your eligibility for financing that exceeds conforming limits based on the home's after-repair value. To secure this approval, lenders require rigorous financial documentation and detailed construction bids. Having this letter strengthens your negotiating position, proving to sellers that you possess the verified capital necessary to complete a sophisticated large-scale renovation project effectively.

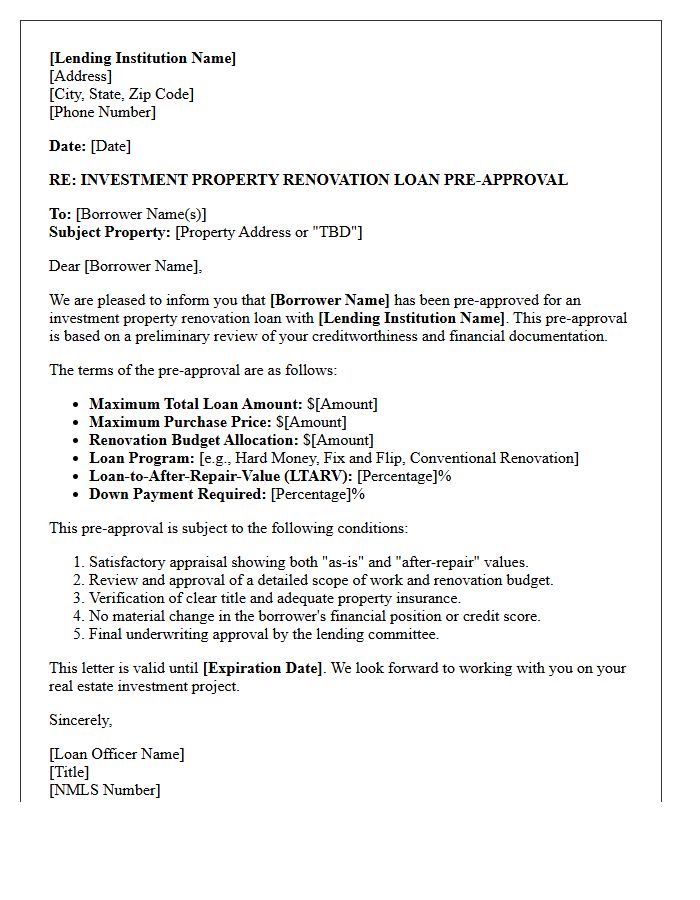

Investment Property Renovation Loan Pre-Approval Letter

An Investment Property Renovation Loan Pre-Approval Letter is a formal document from a lender verifying your financial capacity to fund both the purchase and construction costs. This credibility tool demonstrates to sellers that you are a qualified investor with access to specialized capital like hard money or fix-and-flip loans. It outlines your specific borrowing limit based on your creditworthiness and project experience. Having this letter is essential for making competitive offers in fast-moving markets, ensuring you can cover the after-repair value potential of a distressed asset.

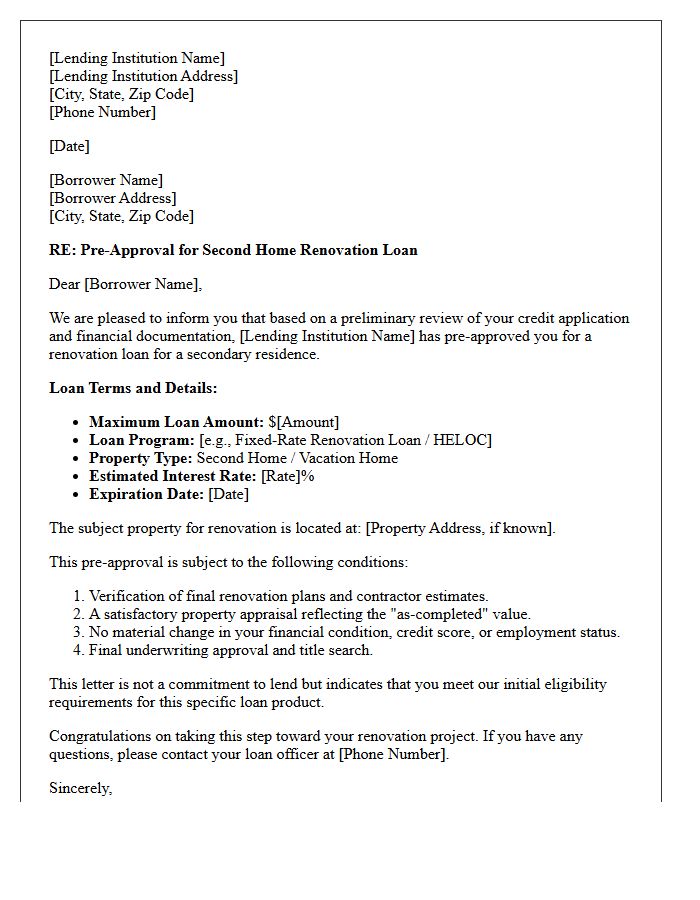

Second Home Renovation Loan Pre-Approval Letter

A Second Home Renovation Loan Pre-Approval Letter is a critical document proving your financial capability to lenders and contractors. It outlines the specific mortgage amount you qualify for based on your credit score, income, and existing debts. Getting pre-approved helps you establish a realistic budget for both the property purchase and the planned upgrades. This letter strengthens your negotiating position, demonstrating that you are a serious buyer ready to finance a secondary residence and its remodeling costs through specialized products like equity loans or construction financing.

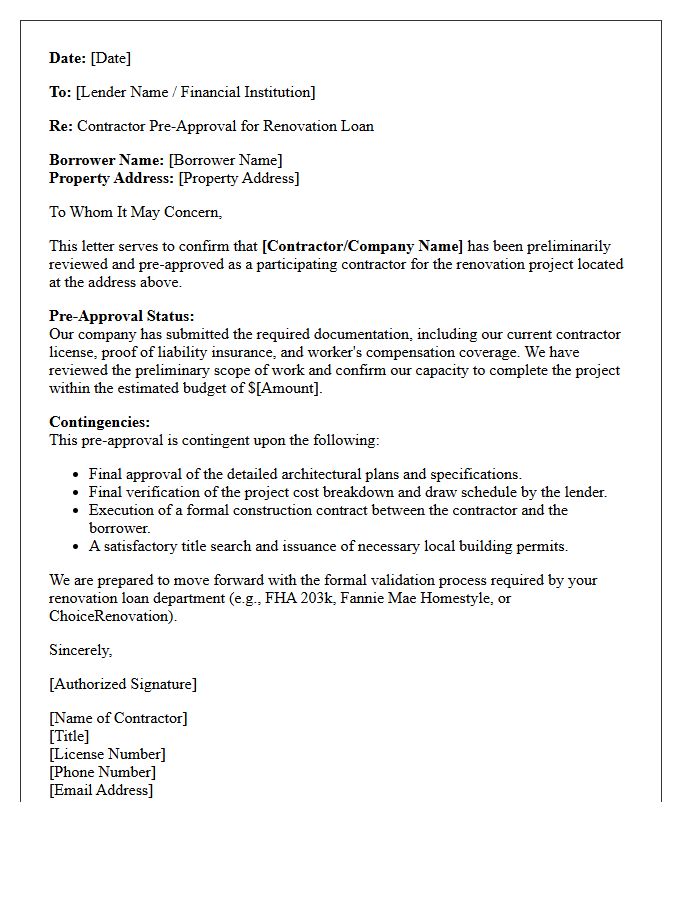

Contractor Contingent Renovation Loan Pre-Approval Letter

A Contractor Contingent Renovation Loan Pre-Approval Letter is a critical document indicating that a lender has verified your financial eligibility for a rehab mortgage. Unlike standard approvals, this commitment depends on an approved contractor's detailed scope of work and cost estimates. It confirms the lender supports both the purchase price and the projected after-repair value. For sellers, this letter provides assurance that the financing covers necessary improvements, making your offer competitive in the distressed property market while ensuring the renovation budget meets strict lending guidelines.

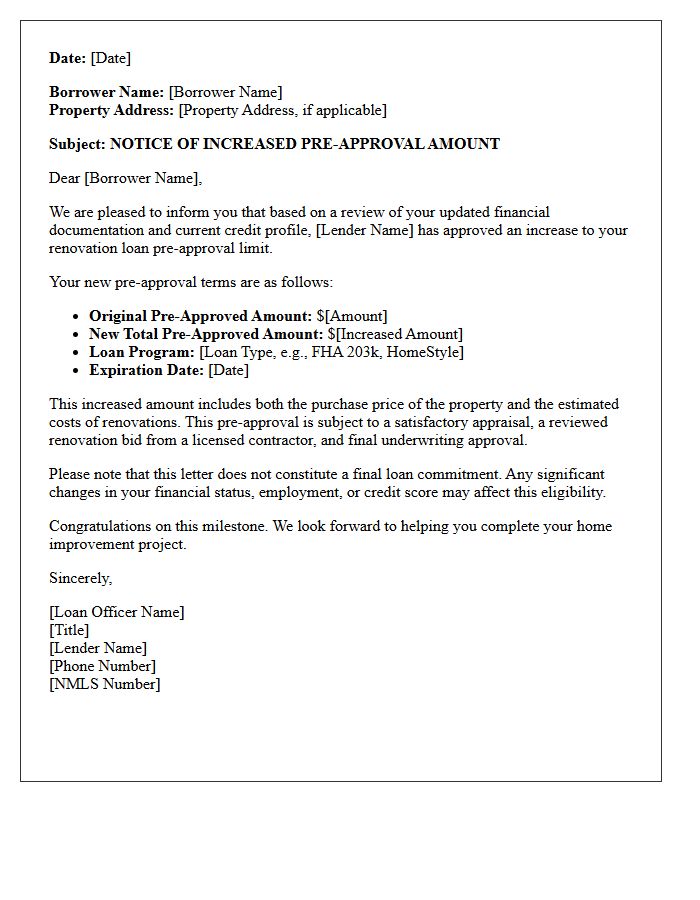

Increased Renovation Loan Pre-Approval Letter

An increased Renovation Loan Pre-Approval Letter serves as a verified financial guarantee, confirming you can borrow more than the standard property value. This document is essential because it accounts for both the purchase price and estimated renovation costs. Securing an updated letter ensures you remain competitive in the housing market while proving to sellers that your total budget covers extensive repairs. It effectively transforms your buying power by integrating future home improvements into a single, comprehensive mortgage commitment before you even start construction.

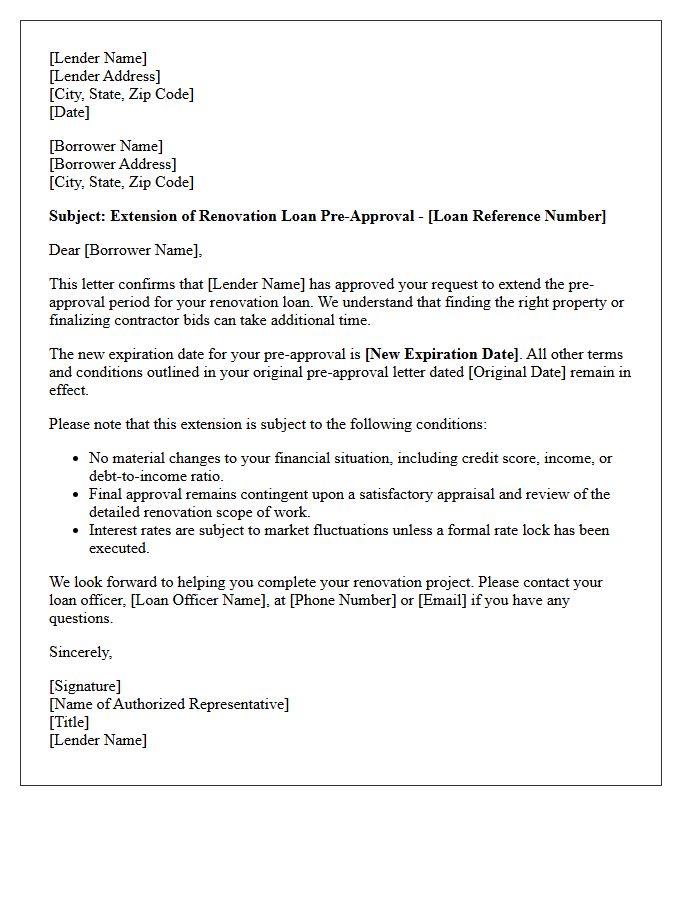

Renovation Loan Pre-Approval Extension Letter

A Renovation Loan Pre-Approval Extension Letter is a formal document issued by lenders to prolong the validity of your initial financing offer. It is crucial because renovation quotes and construction timelines often exceed the standard 60 to 90-day approval window. This extension ensures your borrowing capacity remains secure while you finalize contractor bids or architectural plans. Always verify if a credit refresh is required, as changes in your financial status can impact the terms. Securing this letter prevents your loan commitment from expiring during the lengthy planning phase.

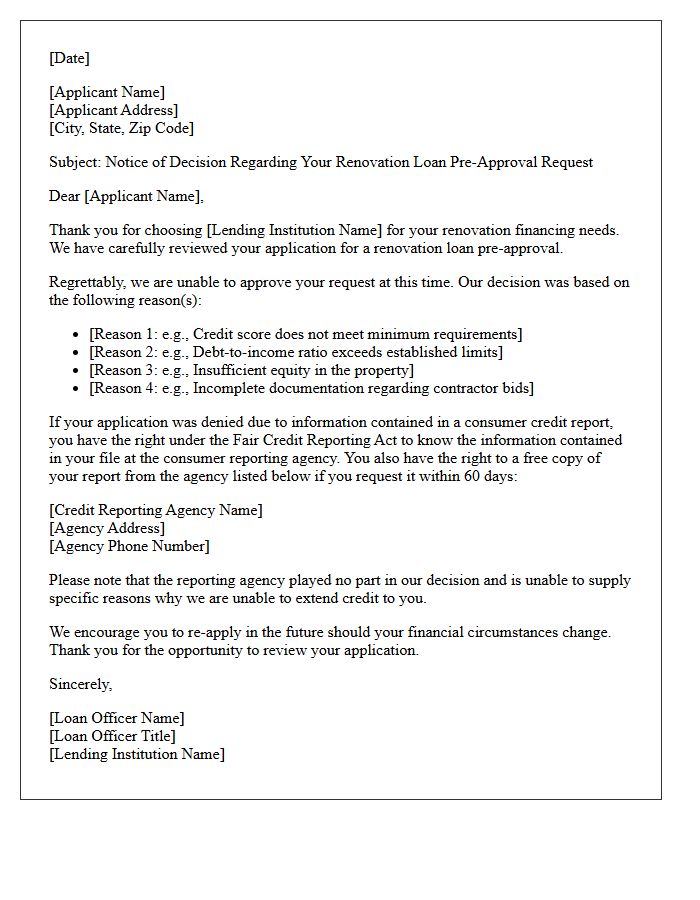

Renovation Loan Pre-Approval Denial Letter

Receiving a Renovation Loan Pre-Approval Denial Letter indicates that a lender cannot currently commit to financing your project. Common reasons for rejection include a low credit score, insufficient debt-to-income ratio, or issues with the property's projected after-repair value. It is essential to review the adverse action notice included in the letter to understand specific disqualifying factors. Addressing these financial gaps or refining your renovation budget can help you improve your eligibility for future applications and successfully secure the necessary funding for home improvements.

Expired Renovation Loan Pre-Approval Letter

An expired renovation loan pre-approval letter means your lender's initial commitment has lapsed, typically after 60 to 90 days. This document is invalid for making offers or securing contractors, as it no longer reflects current interest rates or your updated credit profile. To move forward, you must request a re-evaluation of your financial documents. Timely communication with your loan officer is essential to refresh your status, ensuring you remain a competitive buyer in the housing market and maintain your borrowing power for planned property improvements.

What is a renovation loan pre-approval letter?

A renovation loan pre-approval letter is an official document from a lender stating the specific amount you are qualified to borrow for both the home purchase and the intended property improvements. Unlike a standard pre-approval, it accounts for the future value of the home after renovations are completed.

How do I get a pre-approval letter for a renovation mortgage?

To obtain a renovation loan pre-approval, you must provide a lender with your financial documentation, including tax returns, pay stubs, and credit history. The lender will evaluate your debt-to-income ratio and credit score to determine your eligibility for programs like the Fannie Mae Homestyle or FHA 203(k) loans.

How long is a renovation loan pre-approval letter valid?

Typically, a renovation loan pre-approval letter is valid for 60 to 90 days. Because interest rates and your financial status can change, lenders require periodic updates to your documentation if your home search exceeds this timeframe.

Does a renovation loan pre-approval guarantee I will get the loan?

No, a pre-approval is not a final loan commitment. Final approval depends on a satisfactory appraisal of the property's "as-completed" value, a review of the contractor's credentials, and a detailed breakdown of the renovation costs and architectural plans.

Why is a renovation pre-approval letter important when making an offer?

A renovation pre-approval letter shows sellers that you are financially capable of financing both the purchase and the necessary repairs. It distinguishes your offer from standard buyers by proving you have already been vetted for the complexities of a construction-related mortgage product.

Comments