Securing a First-Time Homebuyer Pre-Qualification Letter is the essential first step in your real estate journey. This document estimates your borrowing power based on basic financial data, giving you the confidence to start house hunting and showing sellers you are a serious contender. Understanding this process streamlines your path to ownership. Below are some ready to use template.

Image cover: The First-Time Homebuyer's Guide to Mortgage Pre-Qualification Letter Samples and Templates

Letter Samples List

- First-Time Homebuyer Pre-Qualification Letter

- First-Time Homebuyer Pre-Approval Letter

- Initial Mortgage Application Acknowledgment Letter

- Missing Financial Documentation Request Letter

- Credit Score Disclosure and Action Letter

- Conditional Loan Approval Notification Letter

- Down Payment Assistance Eligibility Letter

- Interest Rate Lock Agreement Letter

- Pre-Qualification Status Update Letter

- First-Time Buyer Loan Commitment Letter

- Adverse Action and Pre-Qualification Denial Letter

- Clear to Close Authorization Letter

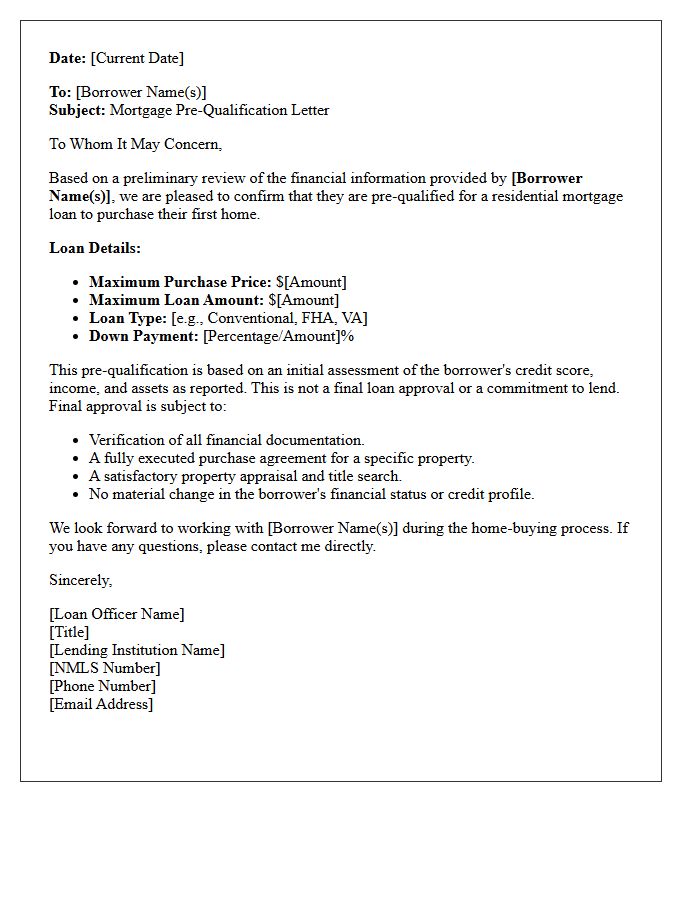

First-Time Homebuyer Pre-Qualification Letter

A Pre-Qualification Letter is an essential initial step for any first-time homebuyer. It provides an estimated loan amount based on self-reported financial data, such as income, debts, and assets. While not a guaranteed loan commitment, this document demonstrates to real estate agents and sellers that you are a serious prospect with the financial capacity to make an offer. Obtaining this letter helps you define a realistic budget and strengthens your purchasing power in a competitive housing market by showing you have engaged with a lender early in the process.

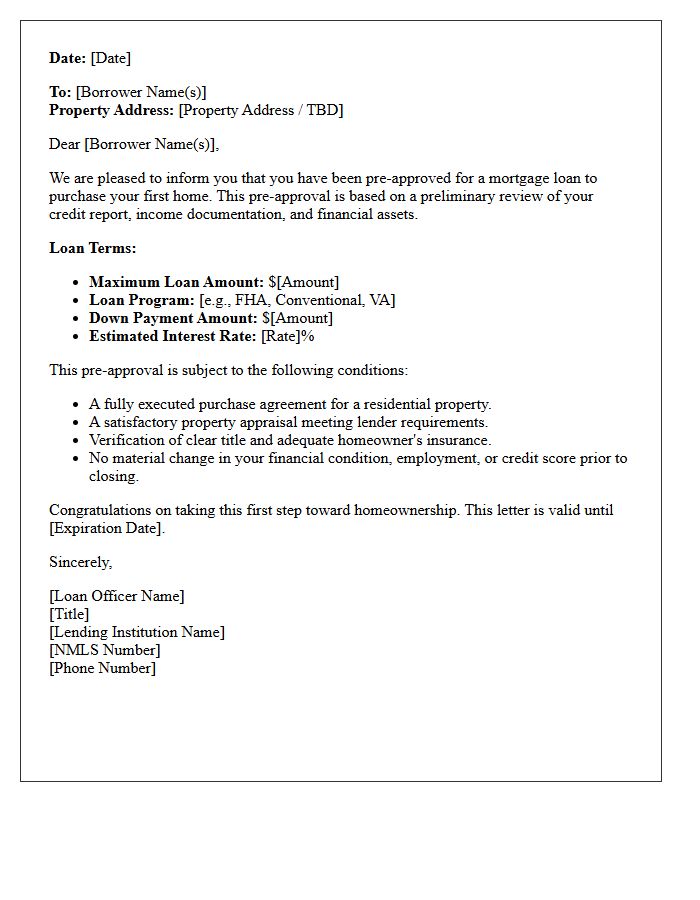

First-Time Homebuyer Pre-Approval Letter

A First-Time Homebuyer Pre-Approval Letter is a critical document from a lender verifying your borrowing capacity. It provides a competitive advantage by proving to sellers that you are a qualified buyer with secure financing. This letter outlines your maximum loan amount based on a thorough review of your credit, income, and assets. Obtaining this document is the essential first step in the real estate process, as most agents require it before showing properties or submitting an official offer in a competitive housing market.

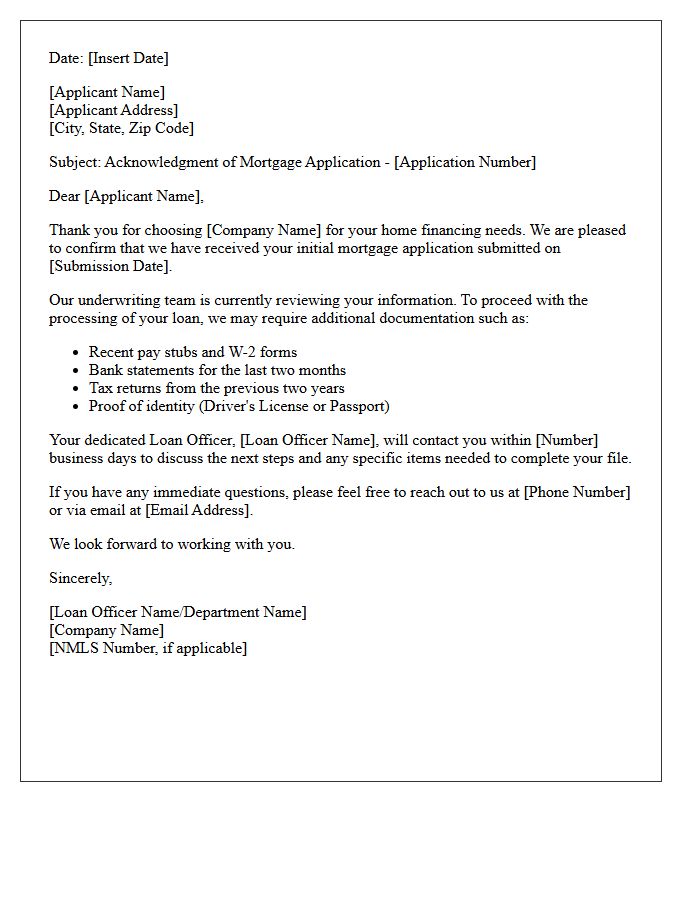

Initial Mortgage Application Acknowledgment Letter

The Initial Mortgage Application Acknowledgment Letter is a formal document sent by lenders to confirm receipt of your loan request. This essential communication marks the beginning of the underwriting process and outlines the next steps for approval. It typically includes a summary of the requested loan terms and a list of required documentation needed to verify your financial status. Reviewing this letter promptly ensures that all personal information is accurate, helping to prevent delays in securing your home financing and moving toward a successful closing.

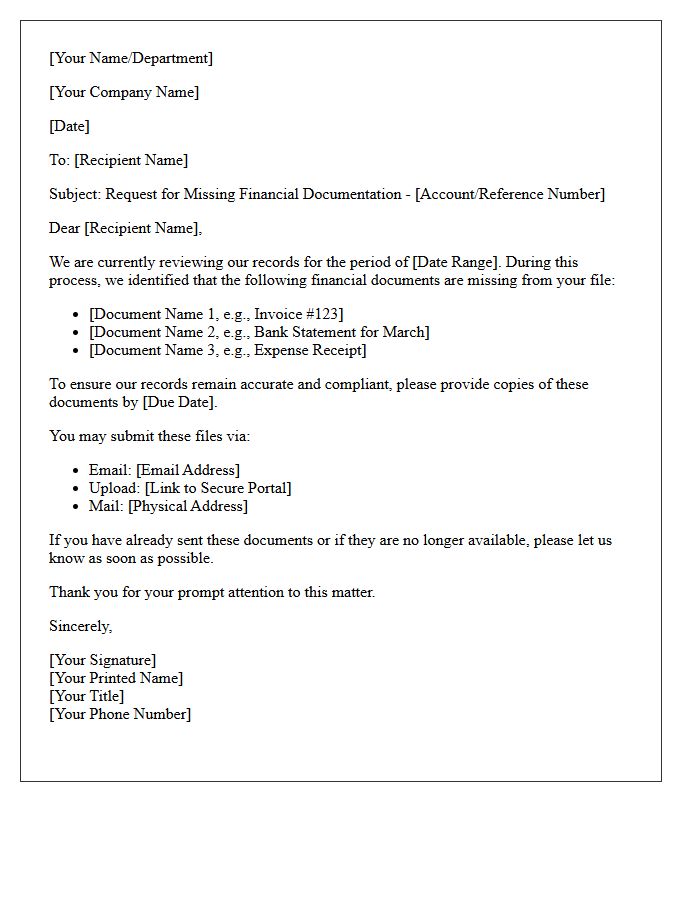

Missing Financial Documentation Request Letter

A Missing Financial Documentation Request Letter is a formal communication used to solicit specific, absent records necessary for audits, loan approvals, or tax compliance. It must clearly list the required evidence-such as bank statements, invoices, or tax forms-and specify a firm deadline for submission. Maintaining a professional tone ensures legal clarity and accountability. Providing precise details about the missing items helps prevent processing delays and ensures financial transparency between parties. Always include contact information to resolve potential discrepancies quickly and maintain accurate financial reporting standards.

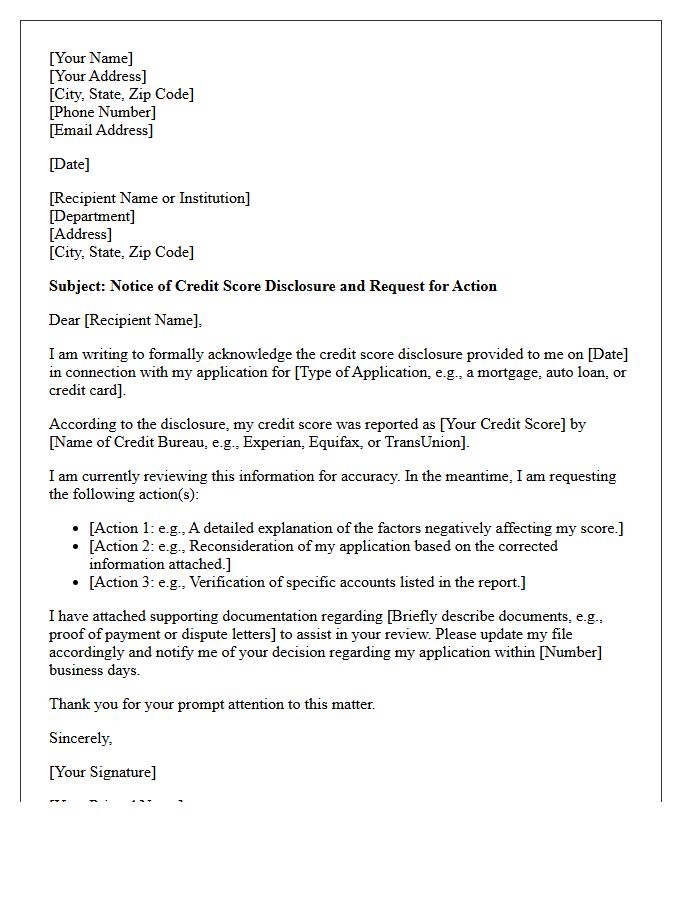

Credit Score Disclosure and Action Letter

A Credit Score Disclosure provides your current credit score, the range of possible scores, and the factors influencing your rating. When a lender denies your application or offers less favorable terms based on your report, they must issue an Adverse Action Letter. This document explains the specific reasons for the decision and identifies the credit bureau used. Reviewing these notices is essential for identifying errors, understanding your creditworthiness, and learning how to improve your financial standing for future loan approvals and lower interest rates.

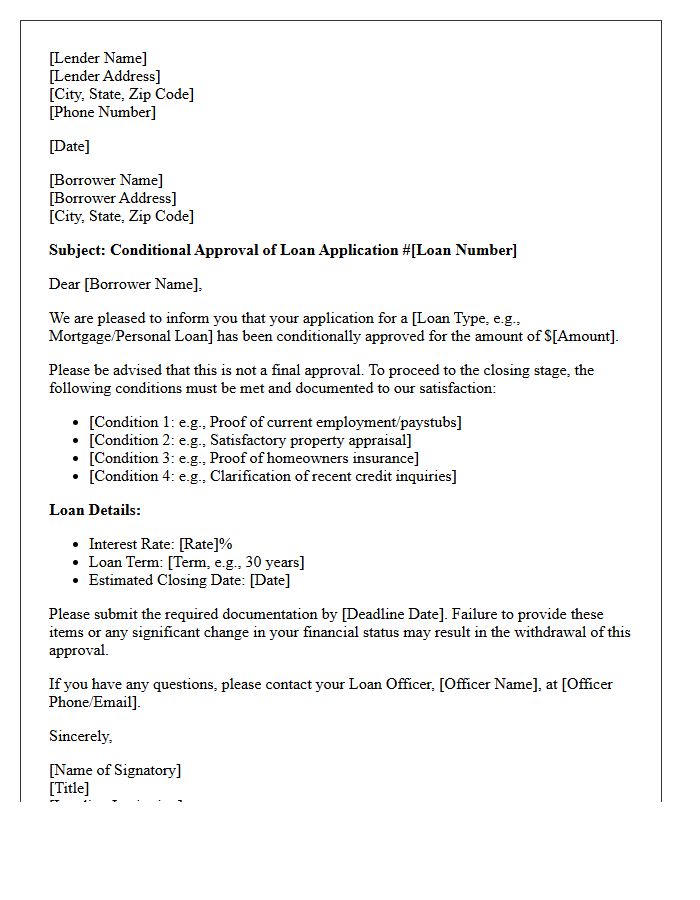

Conditional Loan Approval Notification Letter

A Conditional Loan Approval Notification Letter confirms that a lender is willing to fund your loan, provided you meet specific underwriting requirements. It is not a final guarantee but a formal commitment based on your initial application. To reach full approval, you must submit additional documentation, such as proof of income, tax returns, or a satisfactory property appraisal. Carefully review all listed contingencies and deadlines to ensure your financing remains secure. Failing to satisfy these conditions can result in a loan denial before the scheduled closing date.

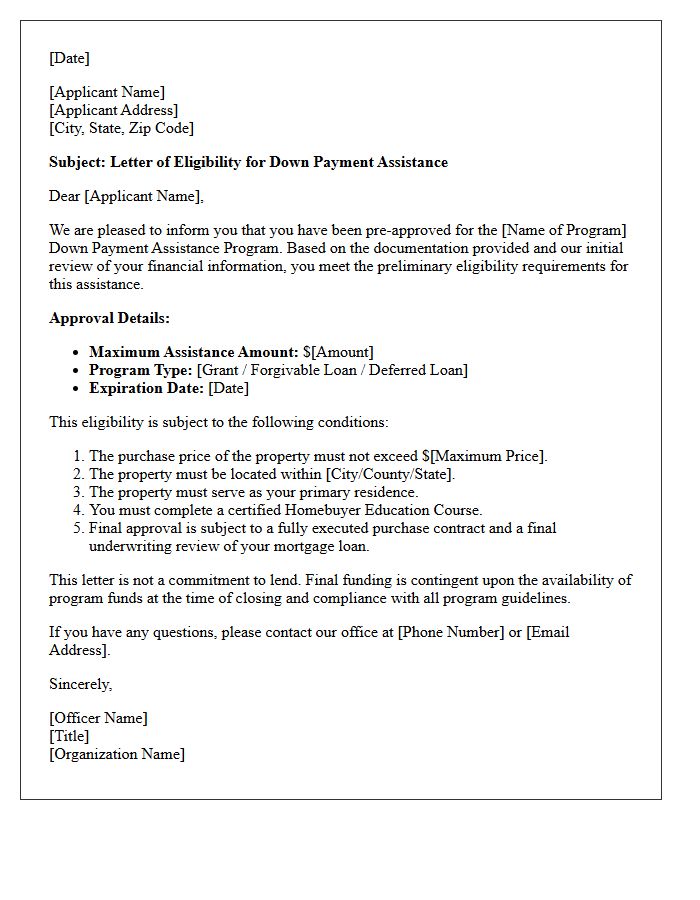

Down Payment Assistance Eligibility Letter

A Down Payment Assistance Eligibility Letter is a formal document issued by a housing agency or lender confirming you meet specific criteria for financial aid. This letter proves you qualify for grants or low-interest loans to cover upfront closing costs and home purchase deposits. To obtain one, you typically must complete homebuyer education and meet income or location requirements. Presenting this letter to sellers strengthens your offer by demonstrating verified funding approval, making it a critical tool for first-time buyers seeking to reduce their out-of-pocket expenses during the mortgage process.

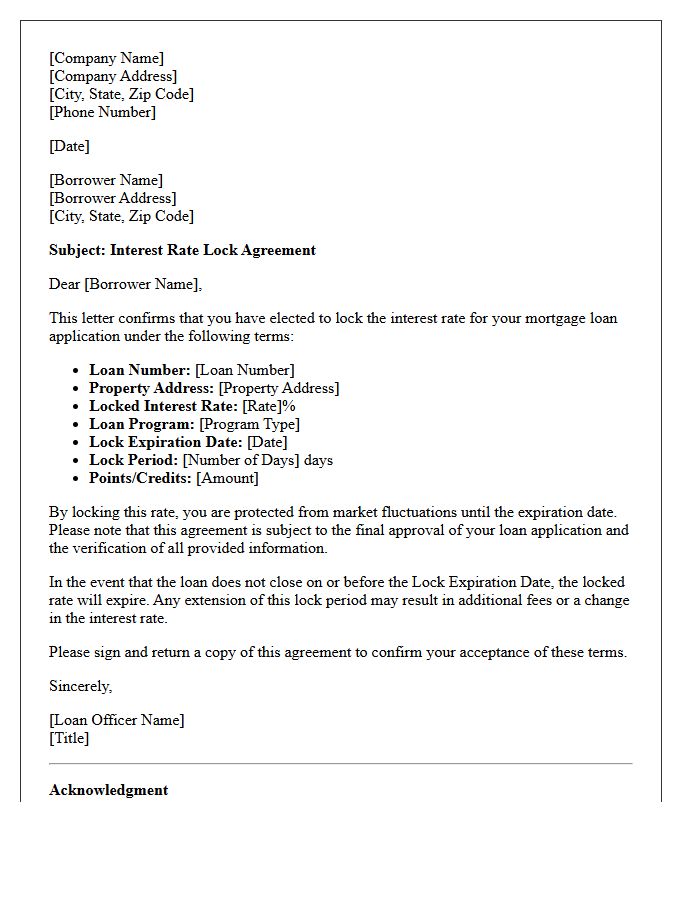

Interest Rate Lock Agreement Letter

An Interest Rate Lock Agreement is a formal commitment from a lender to freeze a specific interest rate and points for a set duration. This document protects borrowers from market fluctuations while their loan is being processed. It is essential to monitor the expiration date, as closing delays could lead to higher costs or the need for an extension fee. Review all terms carefully to understand if the agreement includes a float-down option, allowing you to benefit if market rates drop before your final closing date.

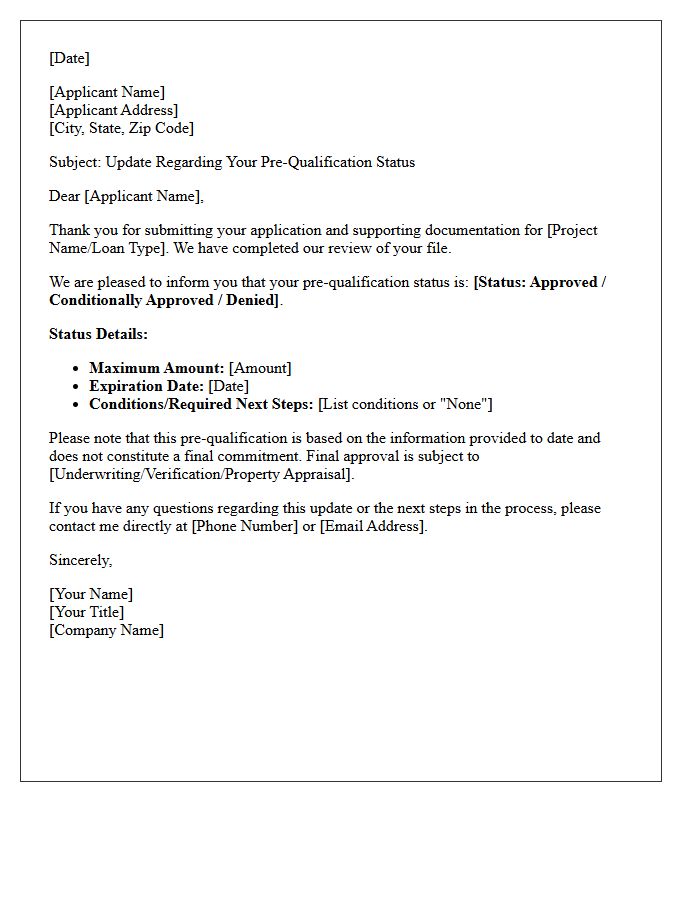

Pre-Qualification Status Update Letter

A Pre-Qualification Status Update Letter is a formal document issued by lenders to confirm a borrower's preliminary creditworthiness. It highlights the estimated loan amount the buyer can afford based on unverified financial data. This update reflects any changes in the applicant's financial situation or current market interest rates. For sellers, this letter serves as essential proof of financing potential, making an offer more competitive. It is a vital tool in the real estate process, though it remains subject to final underwriting approval and comprehensive documentation verification before closing.

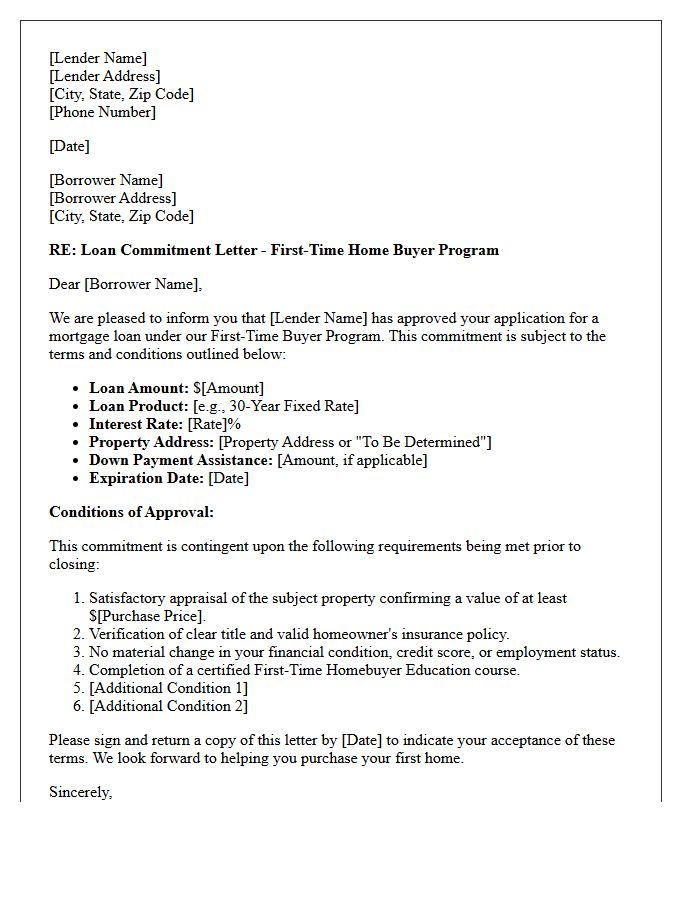

First-Time Buyer Loan Commitment Letter

A First-Time Buyer Loan Commitment Letter is a formal document issued by a lender after a rigorous underwriting process. Unlike a pre-approval, this letter signifies a conditional agreement to provide financing for a specific property. It is the most credible assurance for sellers that your mortgage is nearly finalized. To maintain this commitment, buyers must avoid financial changes, such as new debt or job switches, before closing. This document is a critical milestone that demonstrates your financial readiness and strengthens your position during the final stages of a real estate transaction.

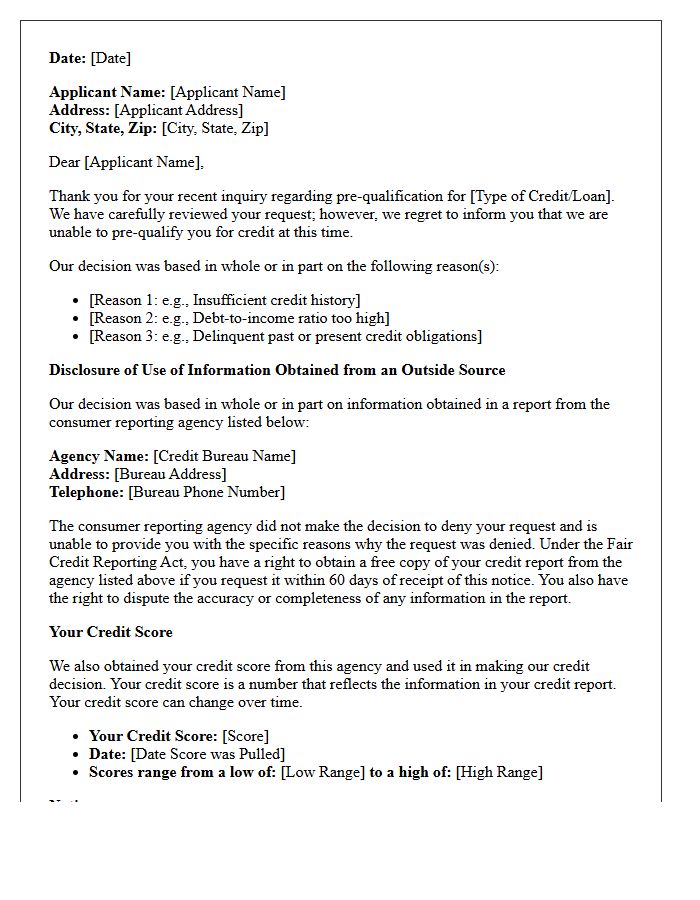

Adverse Action and Pre-Qualification Denial Letter

An Adverse Action Notice is a legally required document sent when a consumer is denied credit based on their credit report. Unlike a simple pre-qualification denial, which may occur during initial screening, an adverse action letter must detail the specific reasons for rejection and identify the credit bureau used. Understanding these notices is essential for transparency and allows applicants to dispute inaccuracies in their financial records. Always review these documents to improve your credit standing and ensure compliance with the Fair Credit Reporting Act (FCRA).

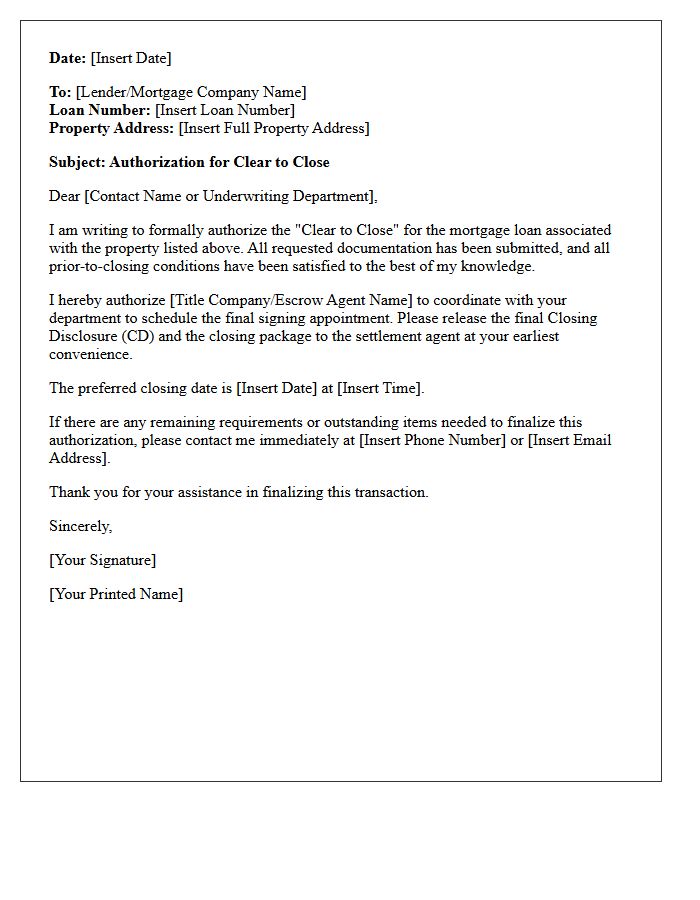

Clear to Close Authorization Letter

A Clear to Close Authorization Letter is a formal notification from a mortgage lender indicating that all loan conditions have been met. This document signifies the final approval stage of the financing process, confirming the borrower is authorized to sign the closing paperwork. It ensures that the underwriting review is complete, the appraisal is accepted, and funds are ready for disbursement. Receiving this authorization is the most critical milestone before the legal transfer of property ownership, allowing parties to finalize the real estate settlement and schedule the official signing date.

What is a pre-qualification letter for a first-time homebuyer?

A pre-qualification letter is an initial assessment from a mortgage lender that estimates how much a first-time homebuyer can afford to borrow based on self-reported financial data, such as income, debts, and assets.

How do I get a pre-qualification letter as a first-time buyer?

To obtain a pre-qualification letter, you must provide a lender with your basic financial information, including your annual income, total monthly debt obligations, and your estimated credit score for a preliminary review.

How long is a mortgage pre-qualification letter valid?

Most mortgage pre-qualification letters are valid for 60 to 90 days. If your home search takes longer, you may need to provide updated financial information to the lender to receive a renewed letter.

Does getting a pre-qualification letter affect my credit score?

Generally, a pre-qualification does not affect your credit score because lenders typically perform a "soft pull" or rely on self-reported data, unlike a pre-approval which requires a "hard pull" of your credit report.

Why do real estate agents require a pre-qualification letter?

Real estate agents require a pre-qualification letter to ensure first-time buyers are serious and financially capable of purchasing a home, and many sellers will not accept an offer without one attached.

Comments