A Condominium Purchase Pre-Qualification Letter is a vital document from your lender estimating your borrowing power specifically for a condo unit. It demonstrates your financial readiness to sellers by verifying your creditworthiness and down payment capability. Securing this letter is the first step toward a successful real estate transaction. To help you start, below are some ready to use template.

Image cover: Proven Templates and Samples for Your Condominium Pre-Qualification Letter

Letter Samples List

- Standard Condominium Purchase Pre-Qualification Letter

- Conventional Mortgage Condominium Pre-Qualification Letter

- FHA Approved Condominium Purchase Pre-Qualification Letter

- VA Approved Condominium Purchase Pre-Qualification Letter

- High-Rise Condominium Purchase Pre-Qualification Letter

- Non-Warrantable Condominium Pre-Qualification Letter

- Luxury Condominium Purchase Pre-Qualification Letter

- First-Time Buyer Condominium Pre-Qualification Letter

- Investment Property Condominium Pre-Qualification Letter

- Jumbo Loan Condominium Purchase Pre-Qualification Letter

- Second Home Condominium Purchase Pre-Qualification Letter

- Adjustable-Rate Mortgage Condominium Pre-Qualification Letter

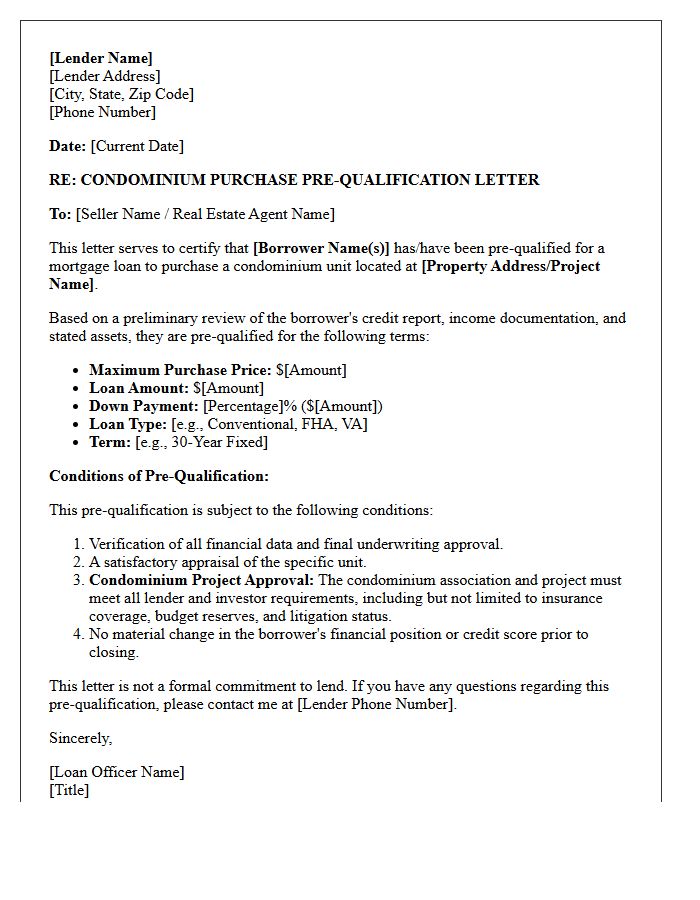

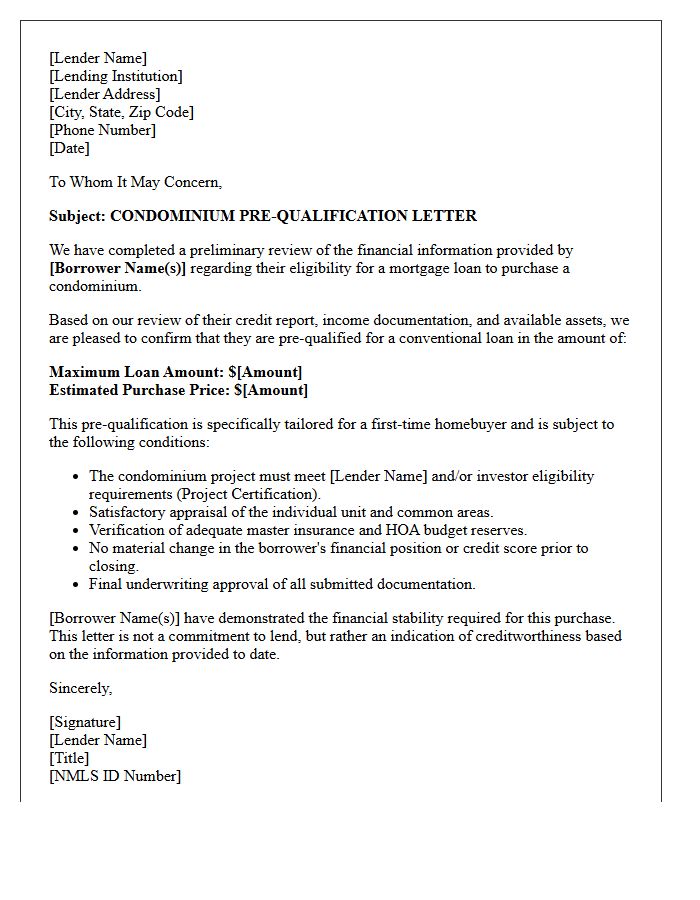

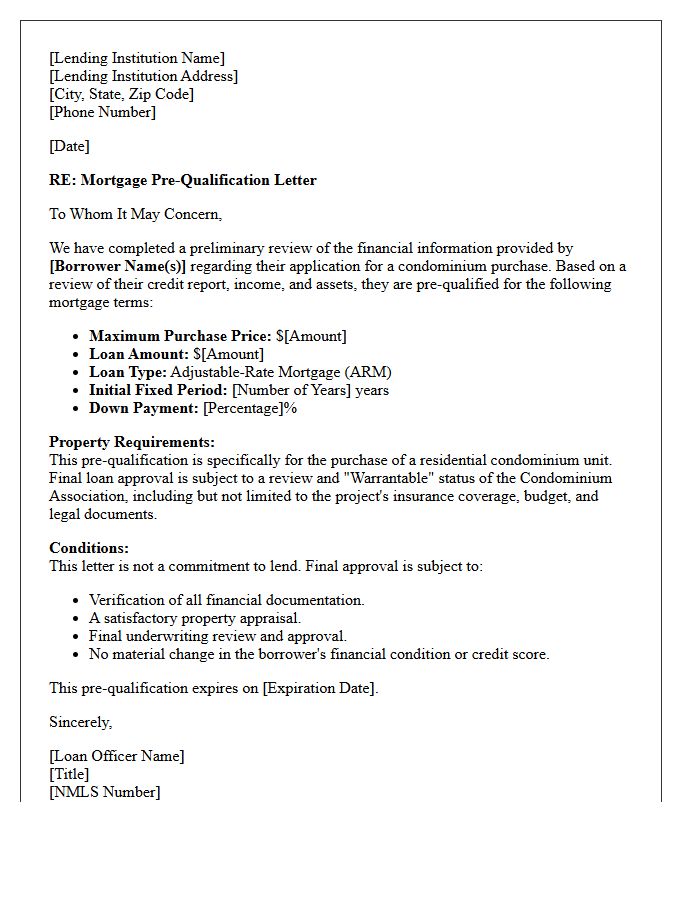

Standard Condominium Purchase Pre-Qualification Letter

A standard condominium purchase pre-qualification letter is a document from a lender indicating a buyer's estimated borrowing capacity. Crucially, for condos, this letter often hinges on project eligibility. Beyond your personal credit score and income, the lender must verify that the homeowners association meets specific financial and insurance standards. Having this letter demonstrates to sellers that you are a serious, qualified buyer who has undergone preliminary financial screening, though it remains subject to a full underwriting review of both your finances and the specific building's health.

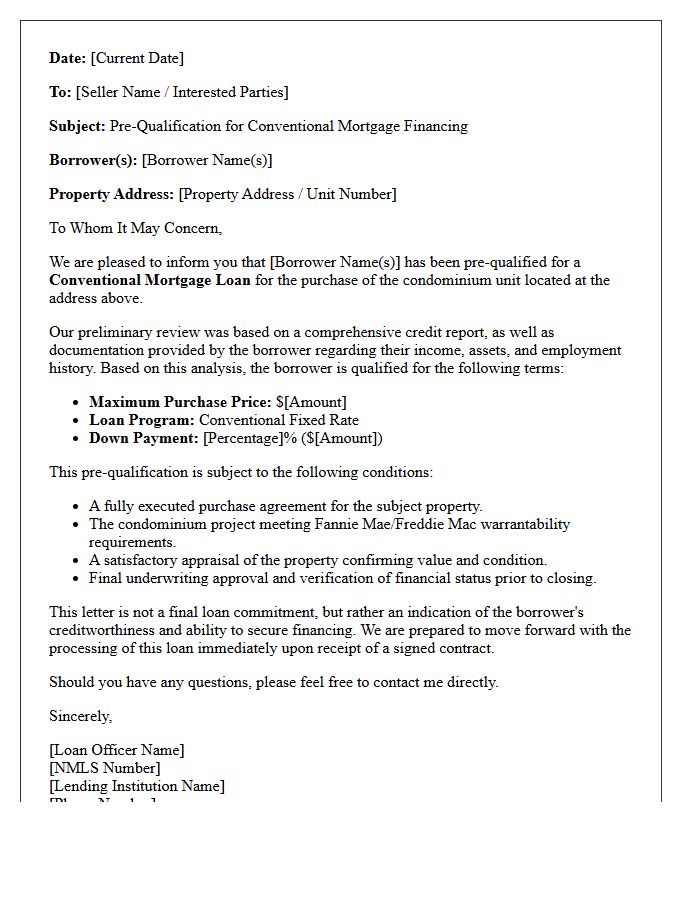

Conventional Mortgage Condominium Pre-Qualification Letter

A conventional mortgage condominium pre-qualification letter confirms a lender's preliminary approval based on your credit and income. Unlike standard homes, condo financing requires a project review to ensure the homeowners association meets Fannie Mae or Freddie Mac standards. This letter demonstrates your borrowing power to sellers, but final approval depends on the building's insurance, litigation status, and budget health. Obtaining this document early is essential for competitive bidding in the real estate market.

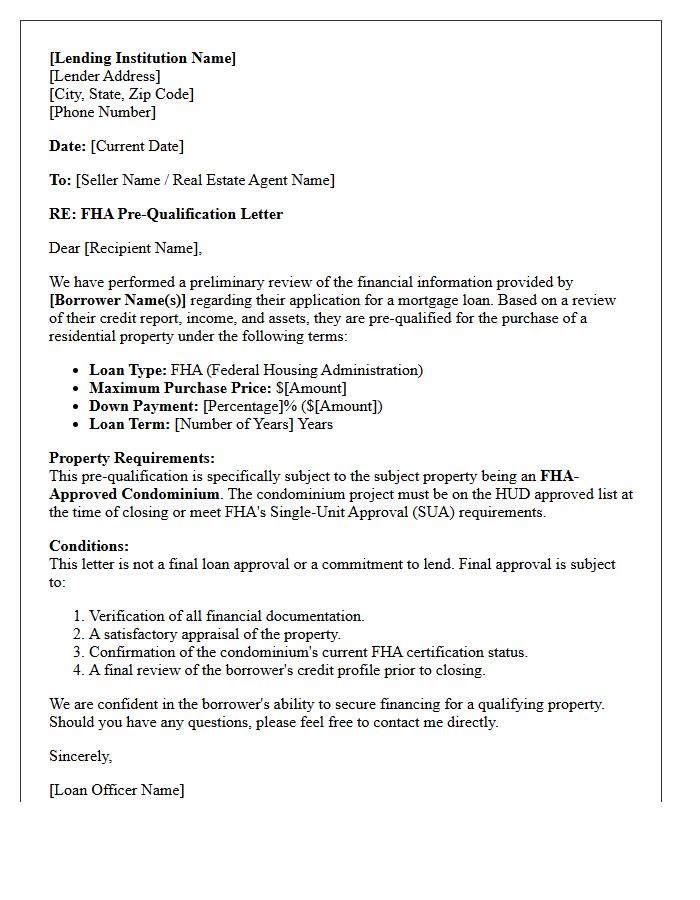

FHA Approved Condominium Purchase Pre-Qualification Letter

An FHA Approved Condominium Purchase Pre-Qualification Letter confirms a buyer's eligibility for financing based on credit and income. However, for the loan to close, the specific condo project must be on the HUD approval list. This letter is a vital initial step, but final funding depends on both the borrower's financial standing and the homeowners association meeting strict federal safety, financial, and insurance standards. Always verify the current FHA certification status of the development before submitting a formal offer to ensure a smooth mortgage process.

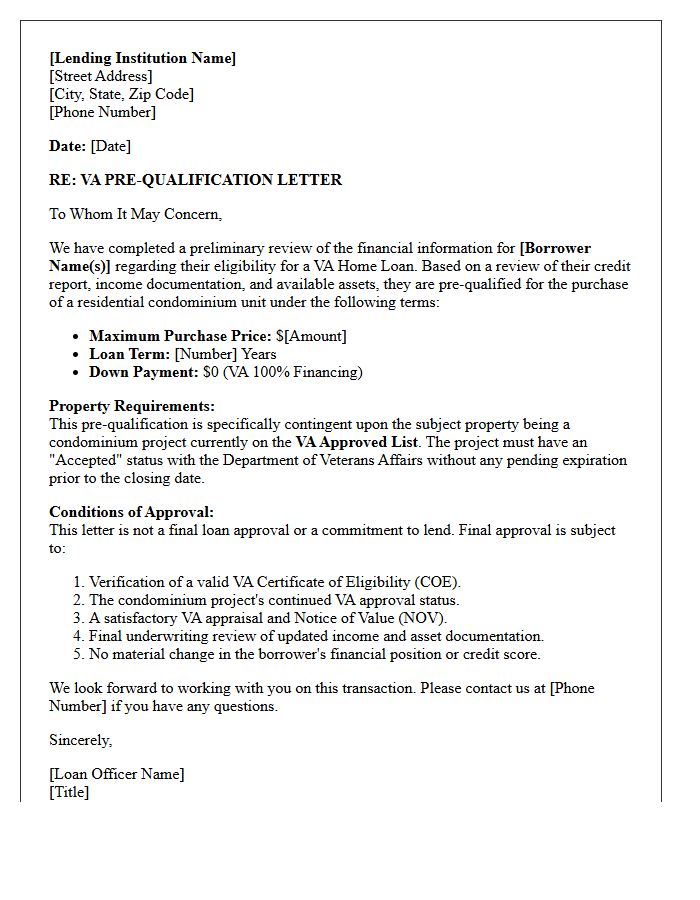

VA Approved Condominium Purchase Pre-Qualification Letter

A VA approved condominium purchase pre-qualification letter is a critical document verifying a Veteran's eligibility to finance a home within a specific project. Before issuing this letter, lenders must confirm the development is on the VA formal approval list to ensure the property meets federal guidelines. This pre-qualification process evaluates the Veteran's creditworthiness and the condo's legal standing simultaneously. Securing this letter early streamlines the offer process, proving to sellers that the buyer has the government-backed financing necessary to close on a verified, eligible unit.

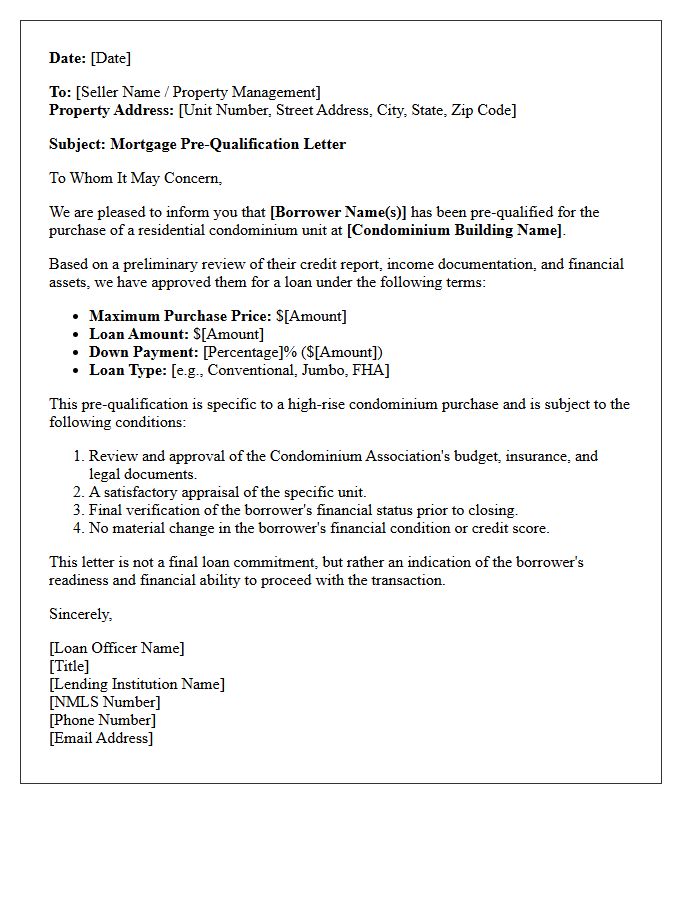

High-Rise Condominium Purchase Pre-Qualification Letter

A high-rise condominium purchase pre-qualification letter is a critical document from a lender estimating your borrowing power. It serves as preliminary approval, signaling to sellers that you are a serious buyer. For vertical living, ensure your lender evaluates both your finances and building eligibility, as high-rise associations must meet specific insurance and reserve requirements. Obtaining this letter early streamlines the offer process and strengthens your competitive advantage in fast-paced real estate markets.

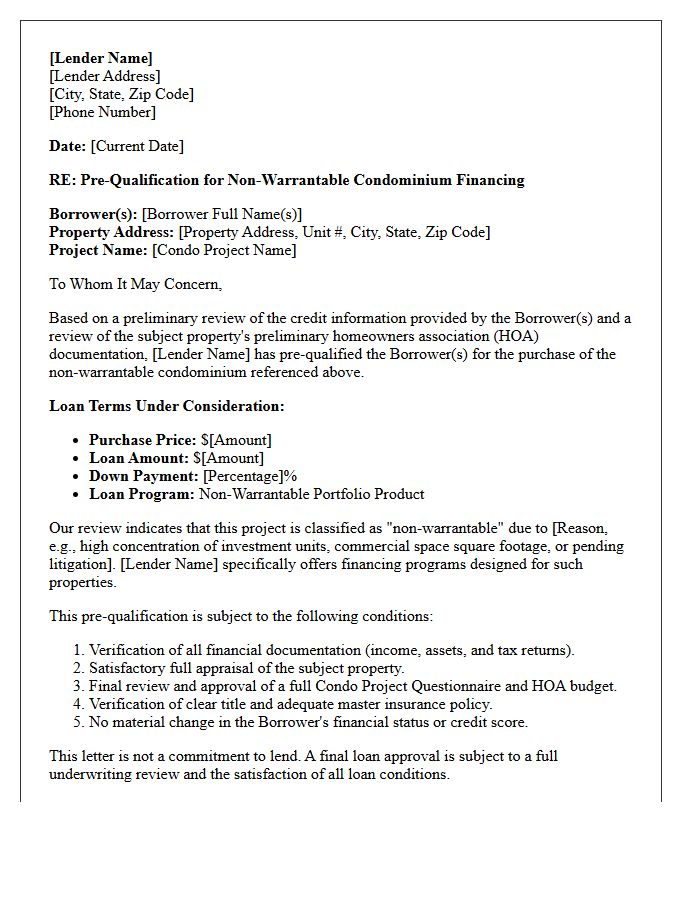

Non-Warrantable Condominium Pre-Qualification Letter

A Non-Warrantable Condominium Pre-Qualification Letter is a specialized document confirming a borrower's eligibility for financing on units that do not meet standard Fannie Mae or Freddie Mac guidelines. These properties often feature high investment concentration, pending litigation, or incomplete construction. Obtaining this letter early is essential because these loans require portfolio lenders or private investors rather than conventional sources. It proves the buyer has the financial strength and the specific loan product necessary to navigate the complex underwriting requirements associated with non-conforming condo projects.

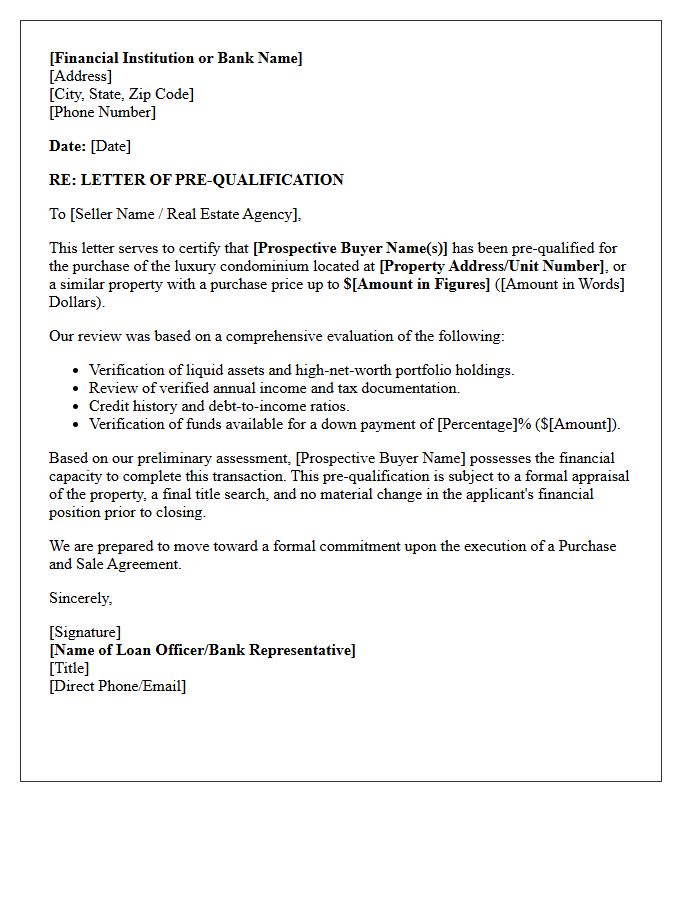

Luxury Condominium Purchase Pre-Qualification Letter

A luxury condominium purchase pre-qualification letter is an essential document proving a buyer's financial credibility to sellers. It outlines your estimated borrowing capacity based on basic income and credit data. In the high-end market, this letter acts as a competitive advantage, ensuring agents prioritize your offer during negotiations. However, because luxury buildings often have strict reserve requirements and litigation checks, obtaining this verified status early simplifies the complex approval process. It serves as a preliminary green light, signaling you are a serious, qualified candidate for a premium real estate investment.

First-Time Buyer Condominium Pre-Qualification Letter

A pre-qualification letter is an essential initial step for first-time buyers seeking a condominium. It provides an estimate of your borrowing power based on self-reported financial data, such as income and debt. This document signals to sellers that you are a serious contender. However, for condos, lenders also evaluate the homeowners association (HOA) health and building warrants. While not a formal loan approval, obtaining this letter helps you establish a realistic budget and strengthens your negotiating position in a competitive real estate market.

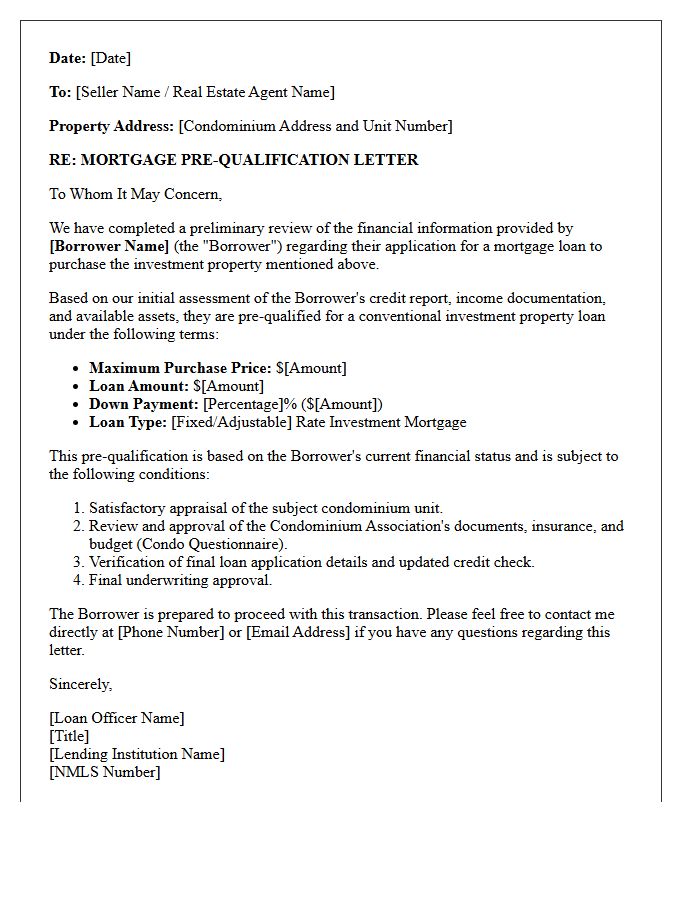

Investment Property Condominium Pre-Qualification Letter

An investment property condominium pre-qualification letter is a crucial document proving a buyer's financial capability to lenders and sellers. Unlike standard residential loans, this letter assesses both the borrower's creditworthiness and the specific homeowners association (HOA) stability. It confirms a preliminary loan approval based on income, assets, and debt ratios. Securing this document is the first step in competitive real estate markets, ensuring the condo project meets warrantable criteria while demonstrating to developers that the investor is a qualified and serious candidate for financing.

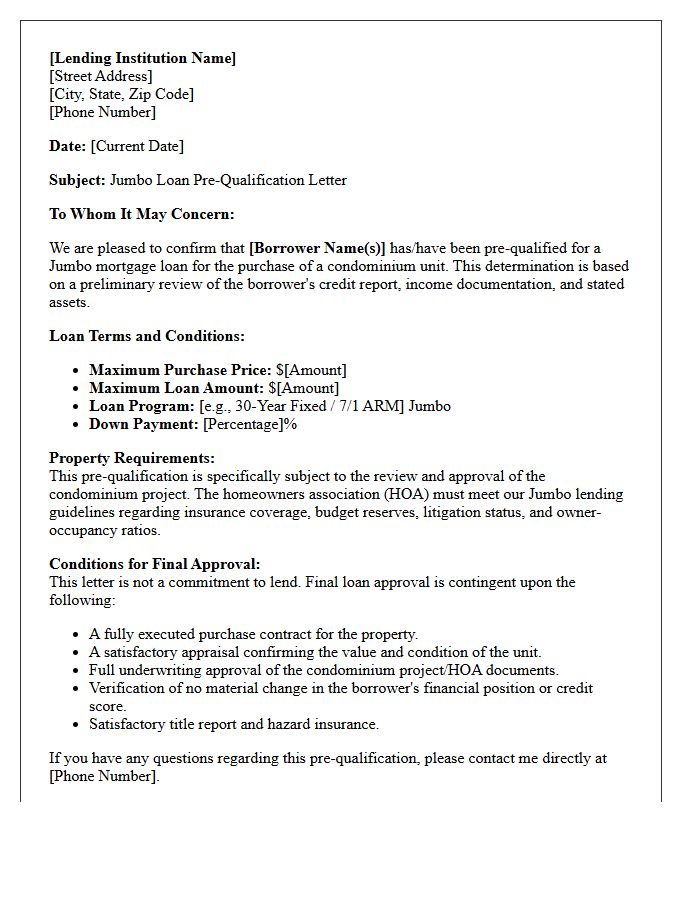

Jumbo Loan Condominium Purchase Pre-Qualification Letter

A Jumbo Loan Pre-Qualification Letter is essential for financing luxury units exceeding conforming limits. Lenders scrutinize the homeowners association's financial stability, insurance coverage, and litigation status before approving the building. To secure this letter, you must provide proof of substantial assets and a low debt-to-income ratio. Because high-value condominium purchases involve stricter underwriting, obtaining a property-specific pre-qualification ensures you meet the complex reserve requirements and occupancy ratios necessary to finalize your mortgage application successfully in a competitive real estate market.

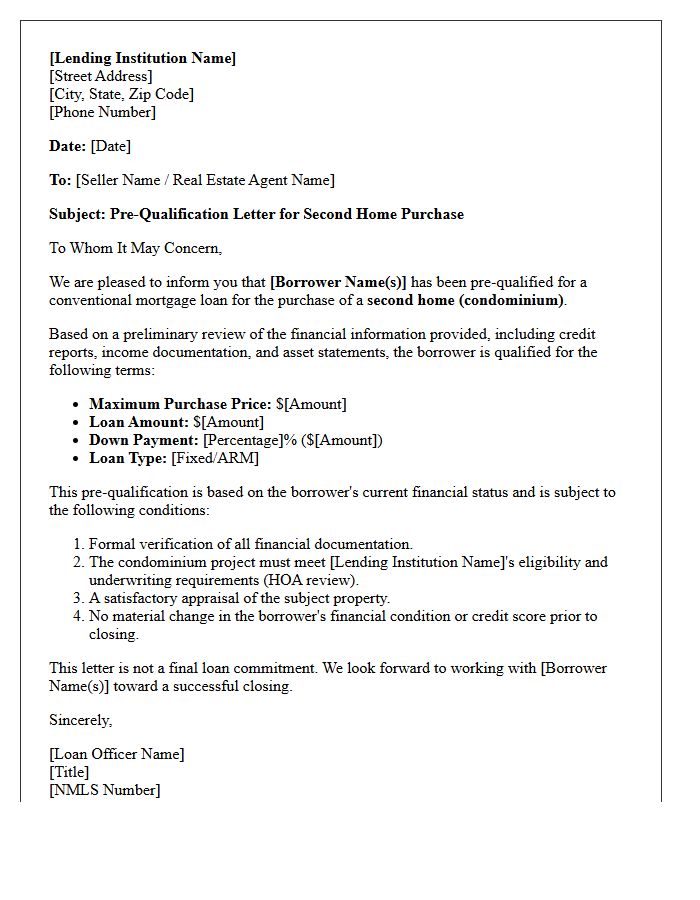

Second Home Condominium Purchase Pre-Qualification Letter

A Pre-Qualification Letter for a second home condominium is a vital document confirming your financial eligibility to lenders. Unlike primary residences, vacation homes often require higher credit scores and larger down payments. This letter proves you can manage dual mortgage obligations while meeting specific condo association requirements. Obtaining this early demonstrates your purchasing power to sellers in competitive markets, ensuring you meet strict investment property guidelines. It serves as the preliminary foundation for securing a conventional loan or specialized jumbo financing for your seasonal retreat.

Adjustable-Rate Mortgage Condominium Pre-Qualification Letter

An Adjustable-Rate Mortgage Condominium Pre-Qualification Letter proves a buyer's eligibility for financing a condo unit with a fluctuating interest rate. Lenders evaluate both the borrower's creditworthiness and the homeowners association's financial health before issuing this document. Since ARM rates change after an initial fixed period, the letter confirms the buyer can manage potential payment increases. This document is essential for making competitive offers, as it demonstrates to sellers that the buyer meets specific condo-specific lending criteria and debt-to-income requirements for a complex property type.

What is a pre-qualification letter for a condominium purchase?

A condominium pre-qualification letter is a document from a lender indicating that a potential buyer is likely to be approved for a mortgage on a condo unit based on a preliminary review of their credit score, income, and debt-to-income ratio.

How does a condo pre-qualification differ from a standard home pre-qualification?

While standard pre-qualification focuses solely on the borrower, a condo pre-qualification also accounts for building-specific requirements, such as HOA financial health, owner-occupancy ratios, and warrantability status which are unique to condominium lending.

What documents are required to obtain a condo pre-qualification letter?

To receive a pre-qualification letter, you typically need to provide basic financial information including recent pay stubs, W-2 forms, bank statements, and authorization for a credit report pull to verify your borrowing capacity.

Does a pre-qualification letter guarantee I will get the mortgage for the condo?

No, a pre-qualification letter is not a binding commitment; final loan approval is subject to a full underwriting process, verification of all financial data, and a successful evaluation of the specific condominium association's legal and financial documents.

Why do sellers require a pre-qualification letter before accepting a condo offer?

Sellers and condo boards require a pre-qualification letter to ensure the buyer has the financial means to complete the transaction, reducing the risk of the deal falling through due to financing issues during the escrow period.

Comments