A Verification of Hazard Insurance Letter is an essential document requested by mortgage lenders to confirm that a property has adequate protection against physical damage. This formal notice ensures the homeowner maintains continuous coverage, safeguarding both the owner's and the lender's financial interests. Understanding how to draft this request accurately prevents compliance issues. To simplify the process, below are some ready to use template.

Image cover: Official Guide to Hazard Insurance Verification Letters: Samples and Templates

Letter Samples List

- Verification Of Hazard Insurance Letter

- Request For Hazard Insurance Verification Letter

- Proof Of Hazard Insurance Coverage Letter

- Hazard Insurance Policy Renewal Letter

- Notice Of Expired Hazard Insurance Letter

- Lender Placed Hazard Insurance Notification Letter

- Insufficient Hazard Insurance Coverage Letter

- Hazard Insurance Declaration Page Request Letter

- Mortgagee Clause Update For Hazard Insurance Letter

- Proof Of Continuous Hazard Insurance Letter

- Force Placed Hazard Insurance Warning Letter

- Hazard Insurance Policy Cancellation Notice Letter

- Hazard Insurance Claim Check Endorsement Letter

- Missing Hazard Insurance Policy Information Letter

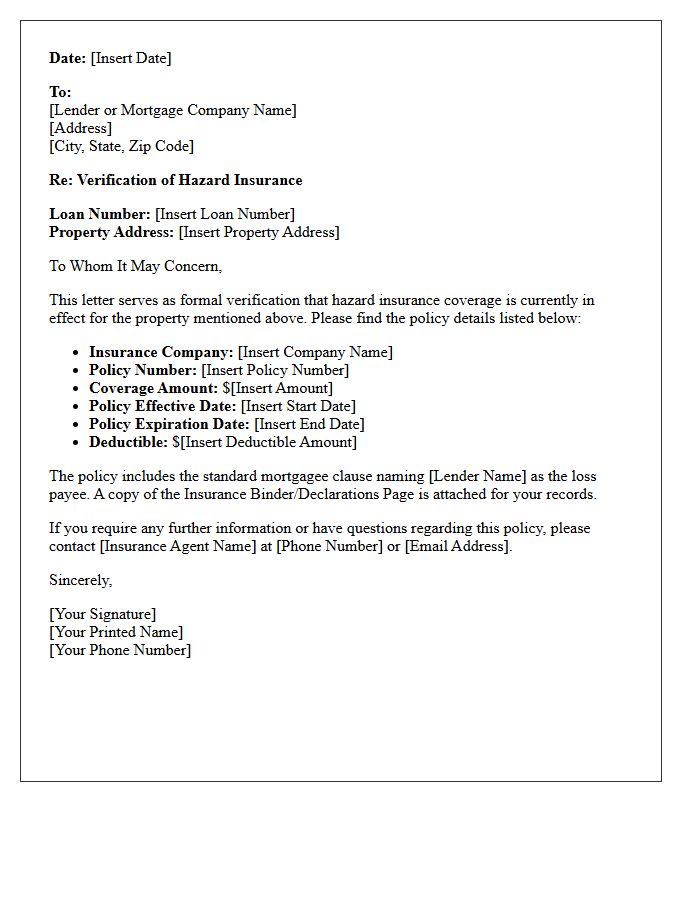

Verification Of Hazard Insurance Letter

A Verification of Hazard Insurance letter is a document sent by mortgage lenders to confirm that a property is adequately protected against risks like fire or storms. Lenders require this proof of coverage to safeguard their financial interest in the asset. If you receive this request, you must provide your current policy details promptly to avoid force-placed insurance, which is often more expensive and offers less protection. Ensuring your insurer includes the correct mortgagee clause is essential for successful verification and maintaining your loan compliance.

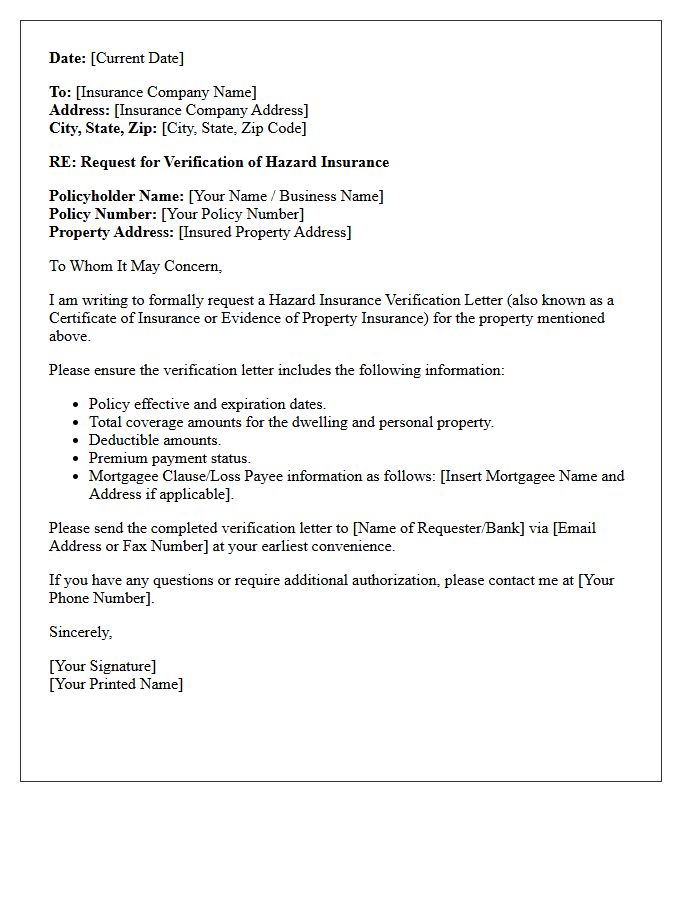

Request For Hazard Insurance Verification Letter

A Request for Hazard Insurance Verification Letter is a formal document used to confirm that a property has adequate protection against physical damage. Lenders require this proof of coverage to protect their financial interest in the collateral. The letter verifies essential details, including the policy number, coverage limits, and effective dates. Ensuring your insurance provider issues this document promptly is crucial for mortgage approval or maintaining compliance with loan servicing requirements. It serves as official validation that the asset is safeguarded against risks like fire, storms, or other natural disasters.

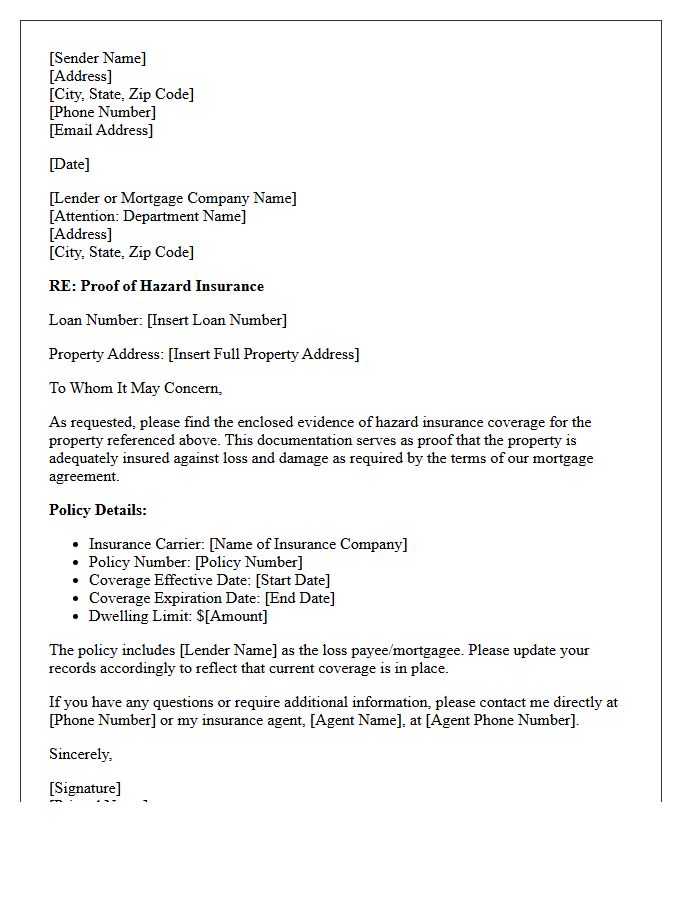

Proof Of Hazard Insurance Coverage Letter

A Proof of Hazard Insurance Coverage Letter is an official document verifying that a property is protected against physical damage like fire, storms, or theft. Lenders require this insurance binder to protect their financial interest in the collateral. Key details include the policy number, coverage limits, and the mortgagee clause, which lists the lender as a loss payee. Ensuring your coverage limits meet or exceed the loan balance is essential for maintaining compliance with your mortgage agreement and avoiding force-placed insurance, which is often more expensive.

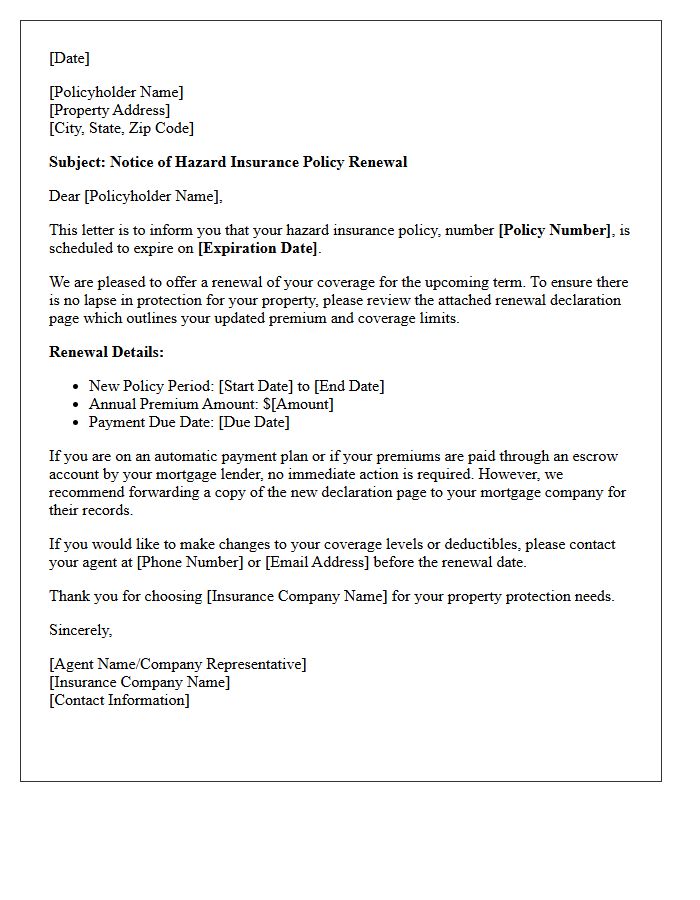

Hazard Insurance Policy Renewal Letter

A hazard insurance policy renewal letter is a crucial document notifying homeowners of upcoming coverage extensions. It outlines updated premium costs, coverage limits, and any changes in terms for protection against physical damage. It is essential to review this letter to ensure your property remains adequately insured against risks like fire or storms. Failure to respond or pay by the deadline can lead to a coverage lapse, potentially violating mortgage agreements. Always compare the new rates to maintain cost-effective protection for your home investment.

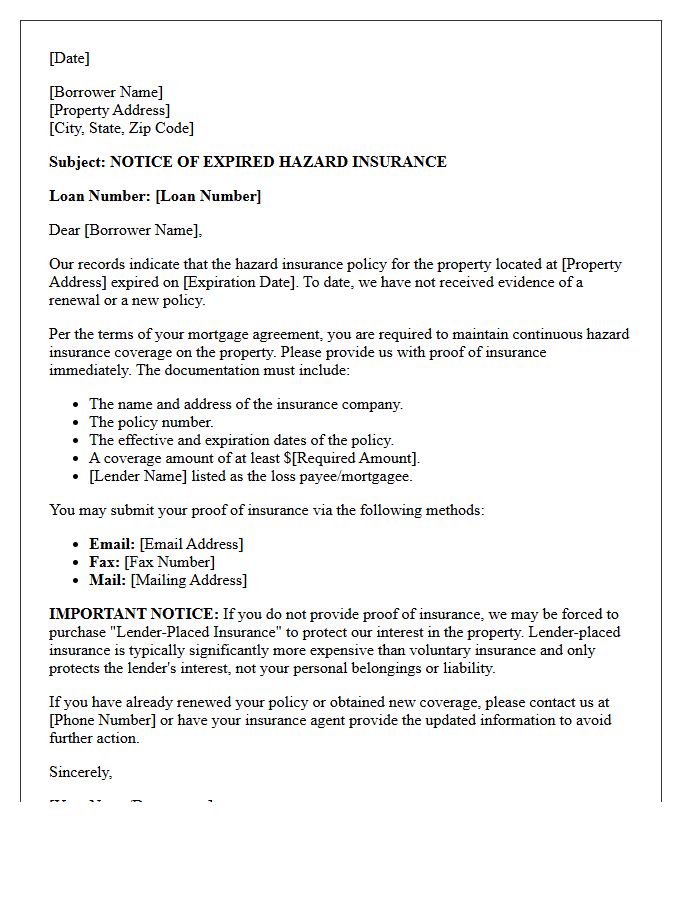

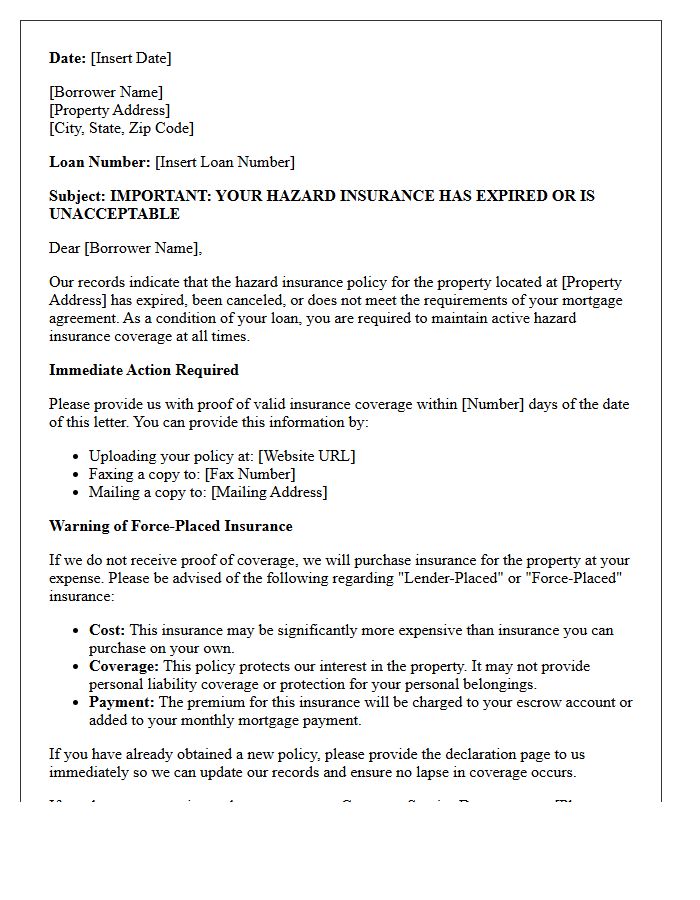

Notice Of Expired Hazard Insurance Letter

A Notice of Expired Hazard Insurance Letter is a formal alert from your mortgage lender stating that your property coverage has lapsed. It is crucial to act immediately because lenders require continuous protection to secure their investment. If you do not provide proof of a new policy, the lender will implement force-placed insurance. This substitute coverage is typically much more expensive and offers limited protection for your personal belongings. To resolve this, contact your insurance agent and forward the updated declarations page to your lender's compliance department promptly.

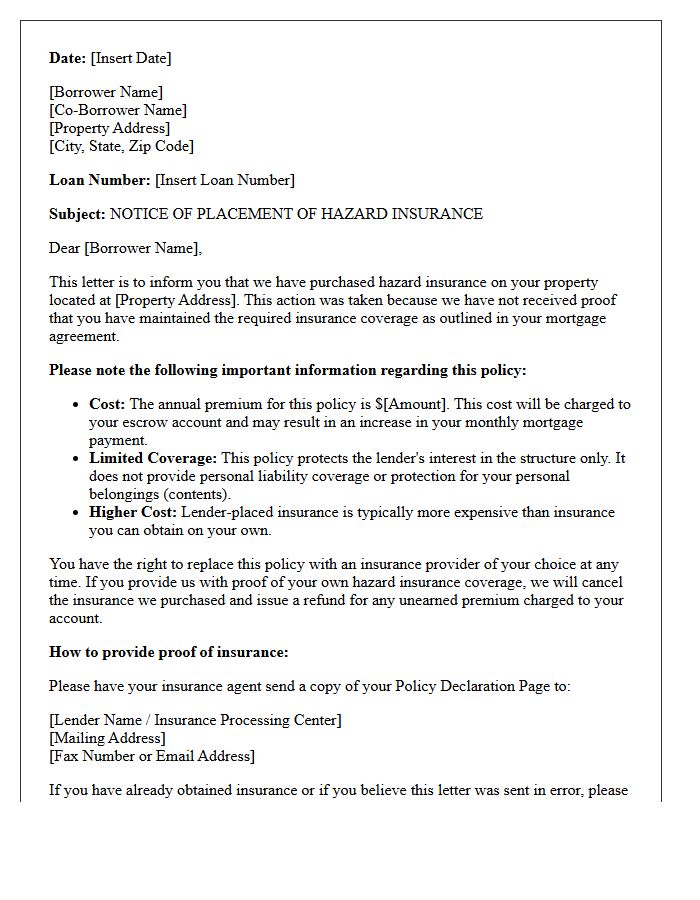

Lender Placed Hazard Insurance Notification Letter

A Lender Placed Hazard Insurance Notification Letter is a formal notice sent when your mortgage servicer detects a lapse in your homeowners coverage. If you fail to provide proof of voluntary insurance, the lender will purchase a policy to protect their financial interest in the property. These forced-placed policies are typically significantly more expensive and offer less protection for personal belongings. To avoid these high costs, you must immediately submit your current declarations page to the lender to prove continuous coverage and cancel any temporary forced-placed charges.

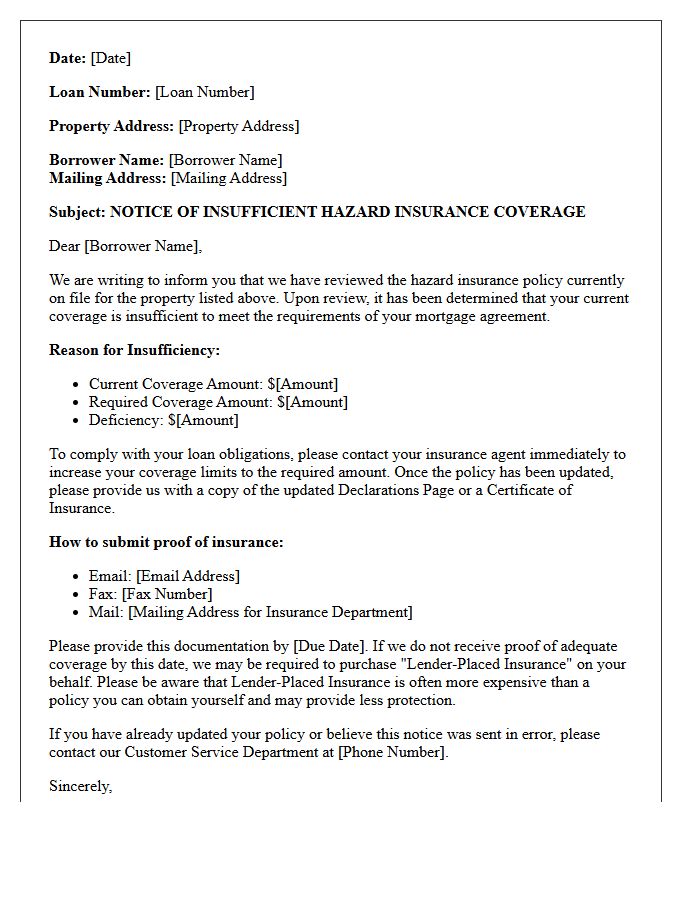

Insufficient Hazard Insurance Coverage Letter

An Insufficient Hazard Insurance Coverage Letter is a formal notice from your mortgage lender indicating that your current policy does not meet their specific financial protection requirements. This typically occurs when your coverage limit is lower than the remaining loan balance or the property's replacement cost. To resolve this, you must promptly increase your policy limits to avoid force-placed insurance, which is often more expensive and provides less coverage. Ensure your updated declarations page is submitted to your servicer immediately to maintain compliance and protect your investment.

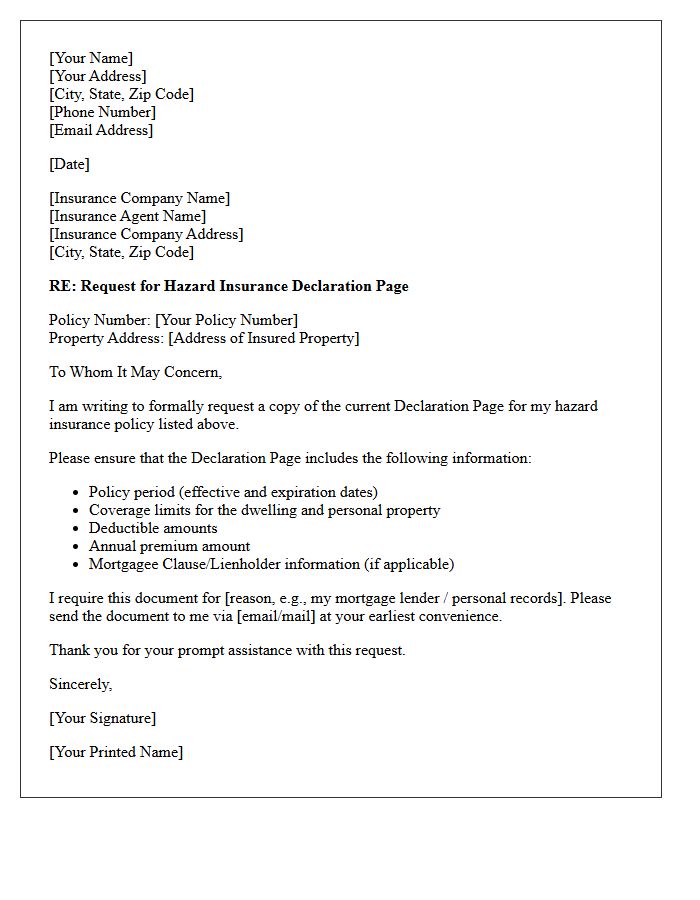

Hazard Insurance Declaration Page Request Letter

A Hazard Insurance Declaration Page Request Letter is a formal document sent to an insurer to obtain proof of coverage. It serves as a summary of your policy, detailing coverage limits, effective dates, and deductibles. Mortgage lenders frequently require this document to ensure the property is protected against physical risks like fire or storms. When drafting your request, include your policy number and property address to ensure a prompt response. This official record is essential for verifying insurance compliance during loan processing or annual escrow reviews.

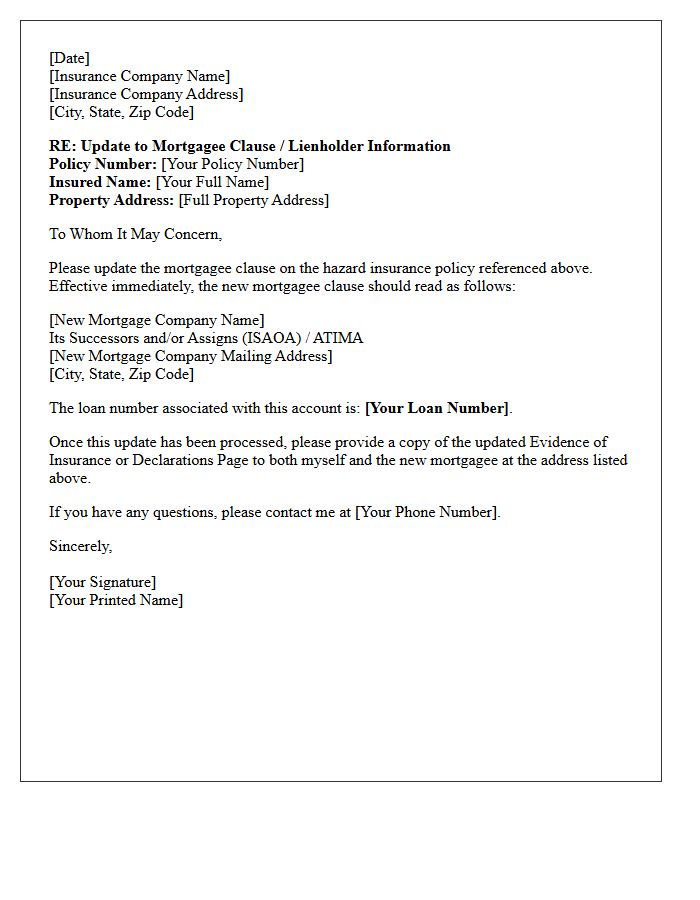

Mortgagee Clause Update For Hazard Insurance Letter

A mortgagee clause update for hazard insurance ensures your lender is correctly listed on your policy. This hazard insurance letter informs the insurer of changes to the lender's name, address, or loan number. Keeping this information current is vital to prevent coverage gaps and ensure escrow payments are disbursed correctly. If the mortgagee clause is outdated, the lender may force-place expensive insurance on your property. Always verify the ISAOA/ATIMA phrasing to guarantee your lender's financial interest remains legally protected during ownership or servicing transfers.

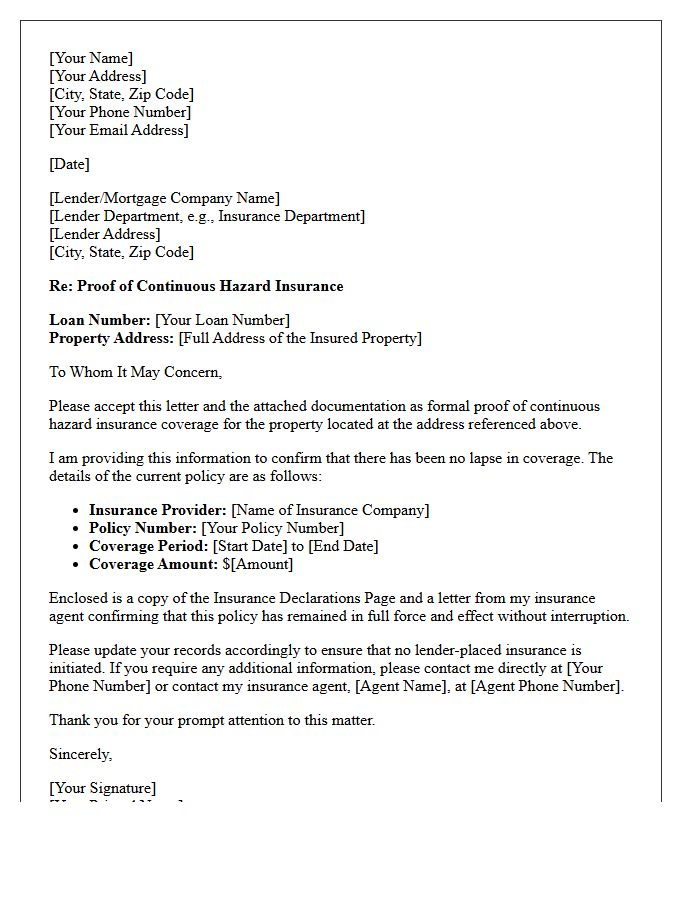

Proof Of Continuous Hazard Insurance Letter

A Proof of Continuous Hazard Insurance Letter is a formal document verifying that a property has maintained uninterrupted insurance coverage over a specific period. Lenders require this to ensure the asset was never unprotected against risks like fire or storms. This letter serves as a compliance guarantee, confirming there were no lapses in the policy that could jeopardize the loan agreement. It is essential during refinancing or property sales to demonstrate responsible risk management and protect the financial interests of both the homeowner and the mortgage holder.

Force Placed Hazard Insurance Warning Letter

A force-placed hazard insurance warning letter is a critical notice from your mortgage lender. It informs you that your current property coverage has lapsed or is insufficient. If you do not provide proof of insurance within 45 days, the lender will purchase a force-placed policy to protect their financial interest. These policies are typically much more expensive than private plans and offer limited protection, often excluding personal belongings. To avoid high costs and potential escrow shortages, immediately contact your insurance agent to verify active coverage and forward the documentation to your lender.

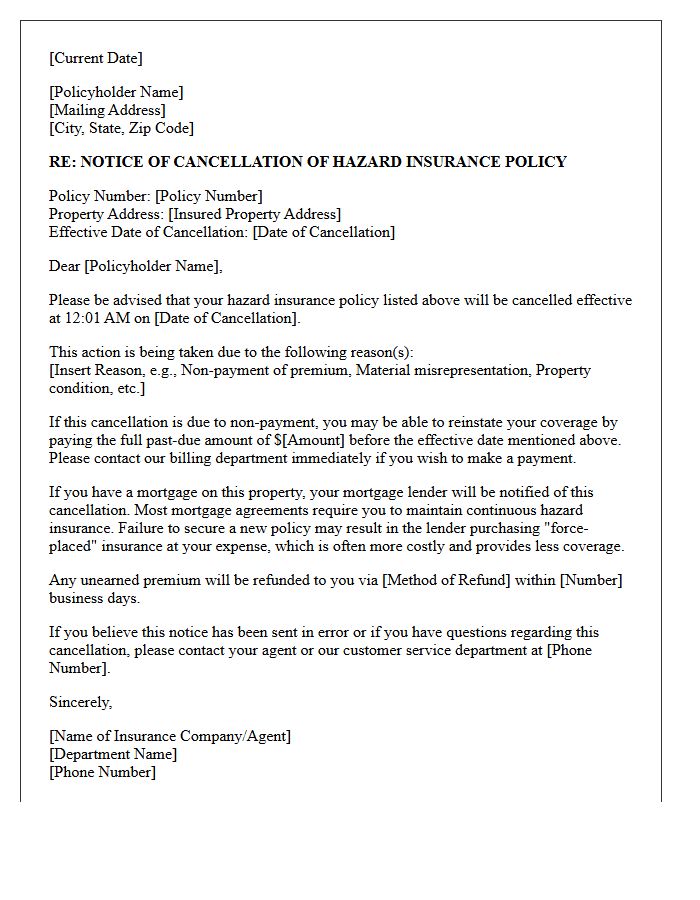

Hazard Insurance Policy Cancellation Notice Letter

A Hazard Insurance Policy Cancellation Notice Letter is a formal document notifying a homeowner that their property coverage is being terminated. This notice is critical because it highlights a potential lapse in coverage, leaving the home vulnerable to risks like fire or storms. Common reasons for cancellation include non-payment, increased property risk, or structural issues. Upon receipt, you must act quickly to resolve the underlying issue or secure a new policy to satisfy mortgage requirements and avoid a forced-place insurance policy from your lender.

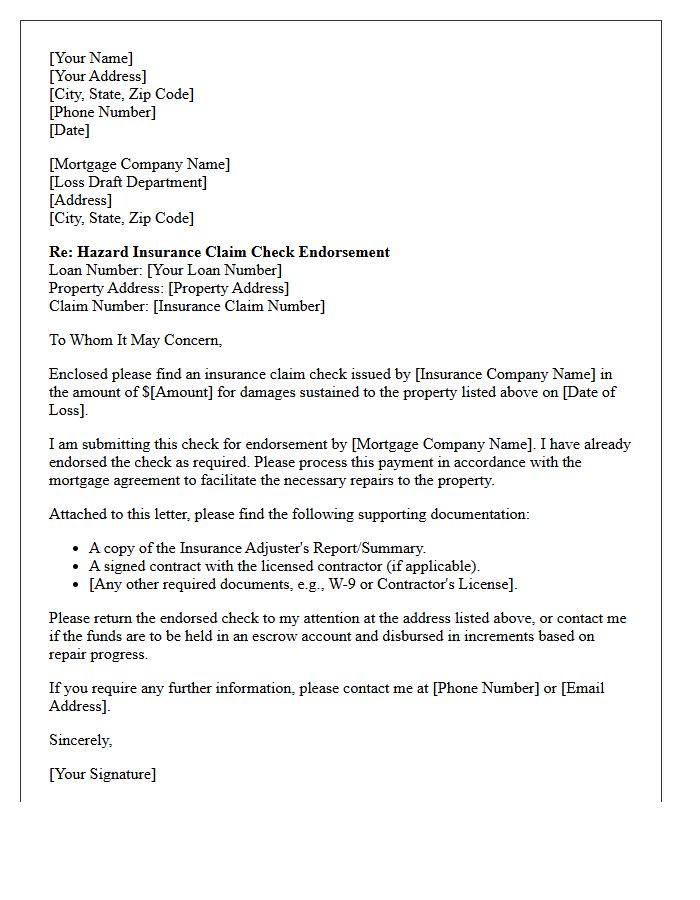

Hazard Insurance Claim Check Endorsement Letter

A Hazard Insurance Claim Check Endorsement Letter is a formal request sent to your mortgage lender to authorize the release of insurance funds. When a property is damaged, insurers typically issue checks payable to both the homeowner and the lienholder. To access the money for repairs, you must provide documentation like contractor bids and inspection reports. The lender endorses the check to ensure the collateral value of the home is restored. Understanding this process is essential for timely home restoration and maintaining your financial agreement with the bank.

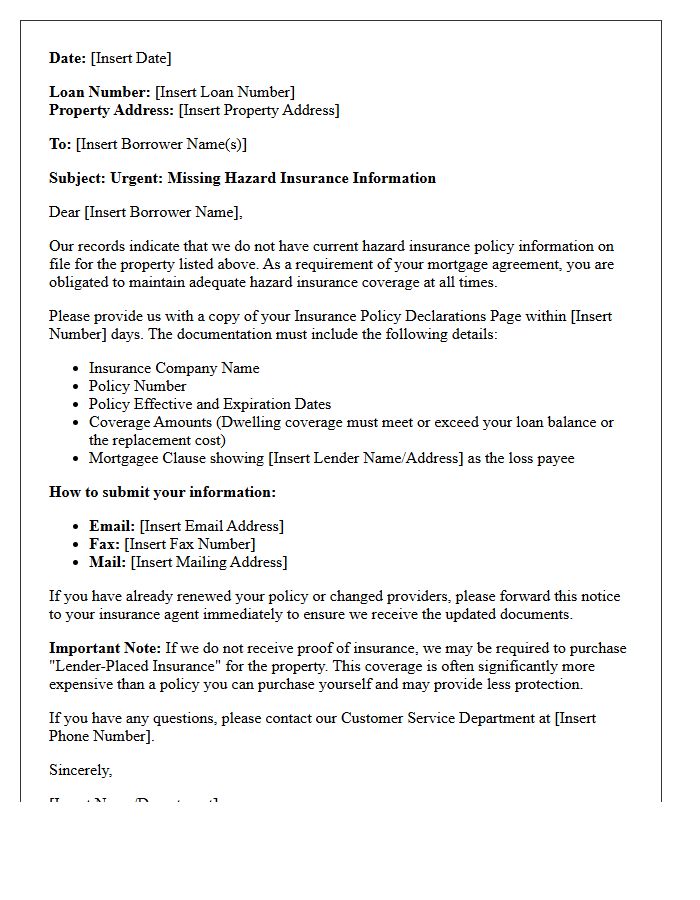

Missing Hazard Insurance Policy Information Letter

A Missing Hazard Insurance Policy Information Letter is a formal notice from a mortgage lender indicating they lack proof of your homeowners insurance. It is critical to respond promptly to avoid force-placed insurance, which is often more expensive and provides less coverage than a private policy. This letter typically requests your current policy declarations page, including the coverage amounts and effective dates. Providing this documentation ensures your loan compliance and protects your property investment from uninsured risks while preventing unnecessary increases in your monthly escrow payments.

What is a Verification of Hazard Insurance letter?

A Verification of Hazard Insurance letter is an official document issued by an insurance provider to confirm that a property has active coverage against physical damages. Lenders require this letter to ensure their financial interest in the property is protected against risks like fire, storms, and theft.

Why did I receive a request for verification of hazard insurance?

Lenders request this verification when they need updated proof of coverage for a mortgage, during a loan application, or if your previous policy information has expired or changed. It confirms that your policy meets the minimum coverage requirements set by your mortgage servicer.

What information must be included in a hazard insurance verification letter?

The letter must typically include the policyholder's name, the insured property address, the policy number, effective and expiration dates, the total coverage amount (dwelling limit), and a loss payee clause naming the lender as a primary stakeholder.

How do I submit my insurance verification to my mortgage lender?

You can provide verification by contacting your insurance agent and requesting they send a "Certificate of Insurance" or a "Declarations Page" directly to your lender's insurance department via their specified portal, email, or fax number found on your notice.

What happens if I fail to provide proof of hazard insurance?

If you do not provide valid verification, your lender may implement "force-placed insurance." This is a temporary policy the lender purchases on your behalf to protect the asset; it is typically more expensive than standard private insurance and offers less protection for the homeowner.

Comments