A Merger and Acquisition Financial Advisory Letter formalizes the partnership between a corporation and its investment bank. It outlines critical terms, including valuation services, strategic negotiation support, and the professional fee structure. This engagement letter ensures alignment during complex corporate transactions to maximize shareholder value. To help you draft your own agreement, below are some ready to use template.

Image cover: Professional Templates for Merger and Acquisition Financial Advisory Engagement Letters

Letter Samples List

- Merger and Acquisition Financial Advisory Engagement Letter

- Banking Institution Confidentiality and Non-Disclosure Letter

- Financial Advisory Services Pitch Letter

- Banking Merger Expression of Interest Letter

- Non-Binding Letter of Intent for Bank Acquisition

- Indicative Financial Offer Letter

- Binding Acquisition Proposal Letter

- Financial Advisory Fee and Remuneration Letter

- Bank Merger Target Exclusivity Letter

- Financial Due Diligence Reliance Letter

- Transaction Fairness Opinion Letter

- Financial Sponsor Comfort Letter

- Advisory Services Termination Letter

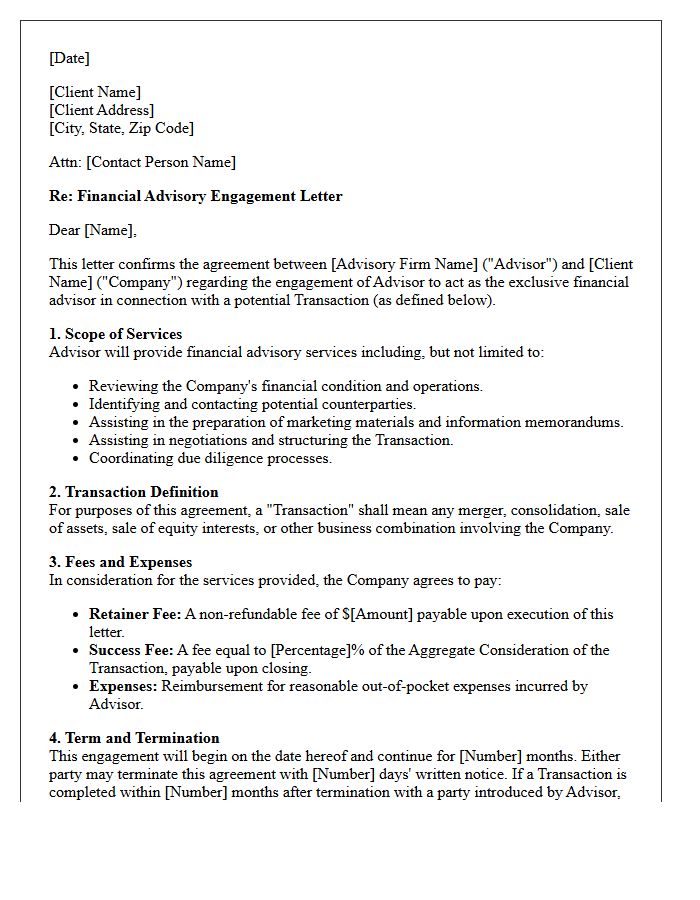

Merger and Acquisition Financial Advisory Engagement Letter

A Merger and Acquisition Financial Advisory Engagement Letter is a legally binding contract that defines the scope of services provided by an investment bank. It establishes the fee structure, typically including a monthly retainer and a performance-based success fee. Key provisions outline exclusivity periods, indemnification clauses, and the specific duration of the partnership. Understanding the tail provision is critical, as it ensures advisors receive compensation if a transaction occurs shortly after the contract ends. This document ensures strategic alignment and protects both parties during complex corporate transactions.

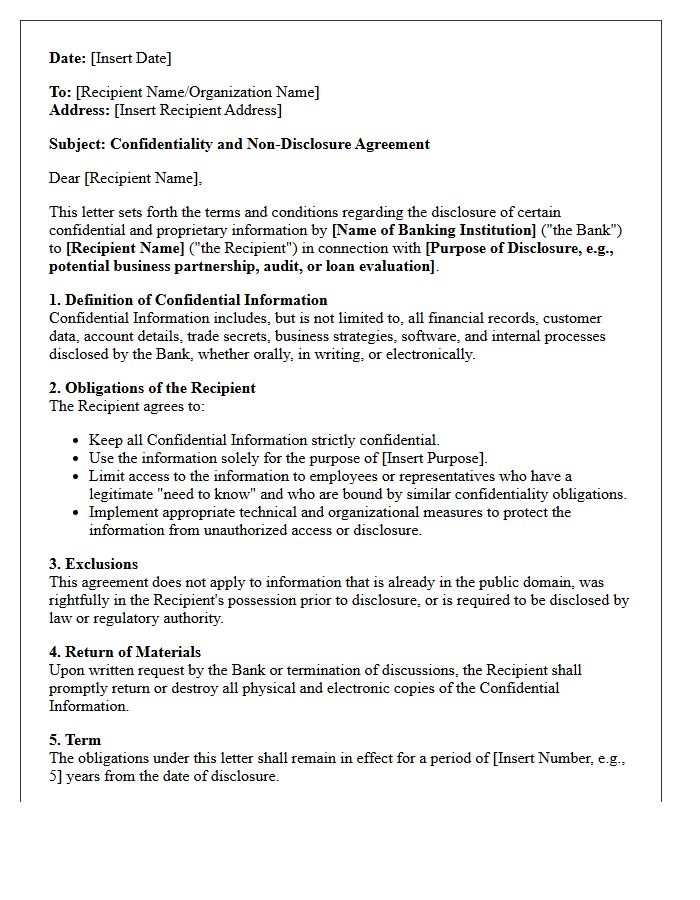

Banking Institution Confidentiality and Non-Disclosure Letter

A Banking Institution Confidentiality and Non-Disclosure Letter is a legal agreement designed to protect sensitive financial data. Its primary purpose is to ensure that proprietary information, trade secrets, and client details remain private during business negotiations or audits. By signing this document, parties commit to strict data protection protocols, preventing unauthorized disclosure to third parties. Understanding the scope of non-disclosure is essential, as breaching these terms can lead to severe legal penalties and financial liability. This letter serves as a foundational safeguard for maintaining institutional integrity and regulatory compliance within the financial sector.

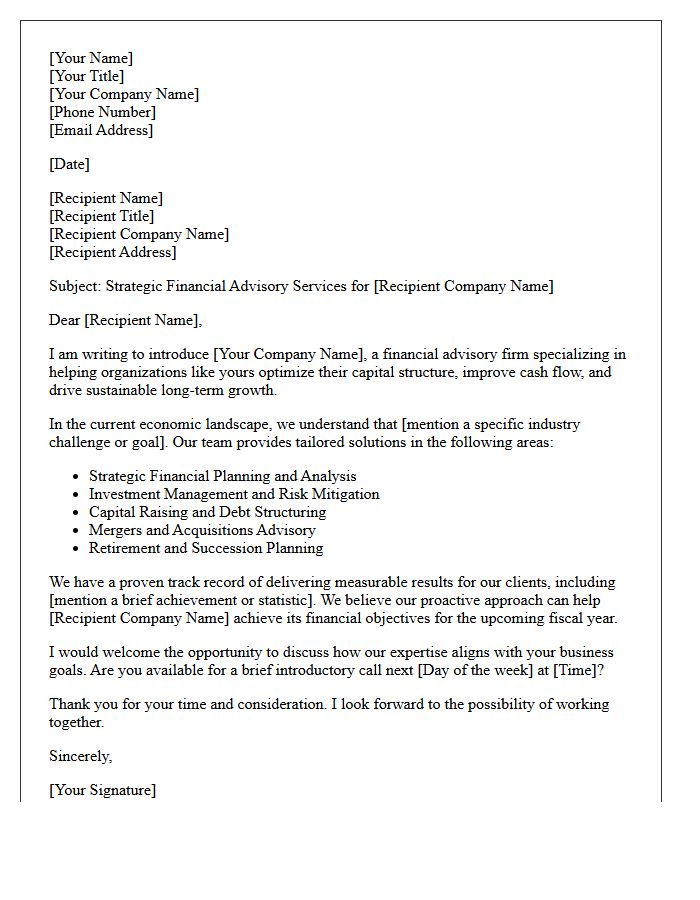

Financial Advisory Services Pitch Letter

A compelling financial advisory pitch letter must prioritize trust and value proposition. Start by addressing a specific financial pain point, such as retirement security or tax efficiency. Highlight your unique methodology and regulatory compliance to establish credibility. Use a client-centric tone that focuses on long-term wealth management goals rather than just product sales. A clear call to action is essential to convert prospects into consultations. Keep the language professional yet accessible to ensure your expertise resonates with the reader's needs and aspirations.

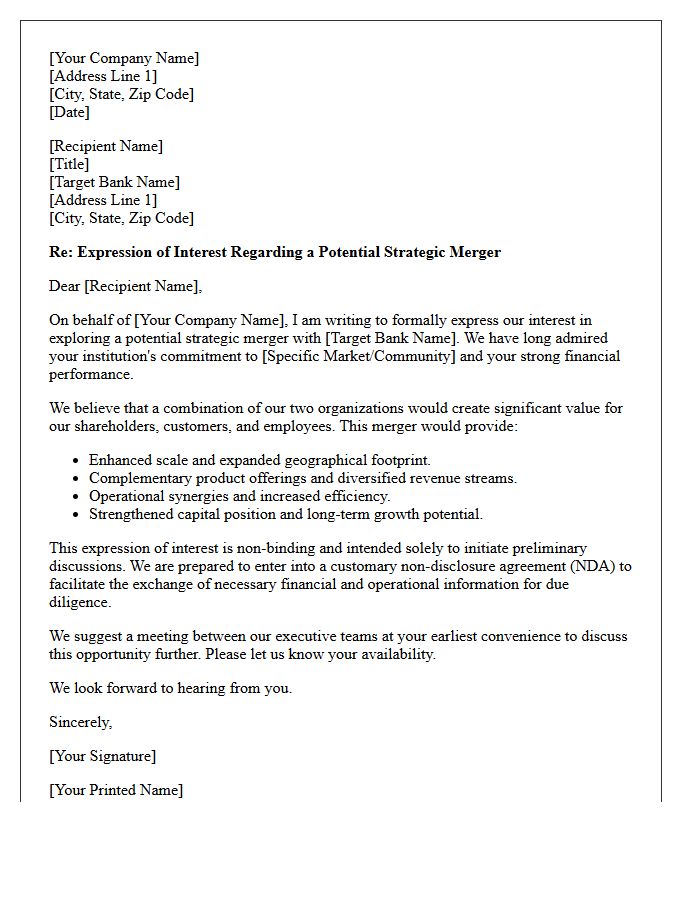

Banking Merger Expression of Interest Letter

A Banking Merger Expression of Interest (EOI) letter is a preliminary, non-binding document initiating a potential business combination. It outlines the strategic rationale, proposed valuation, and transaction structure. The most critical element is the confidentiality clause, which protects sensitive financial data during initial discussions. This formal letter of intent serves as a roadmap for due diligence, defining key terms and timelines before a definitive agreement is reached. It signals serious institutional interest while allowing both parties to evaluate cultural and operational synergy without immediate legal commitment.

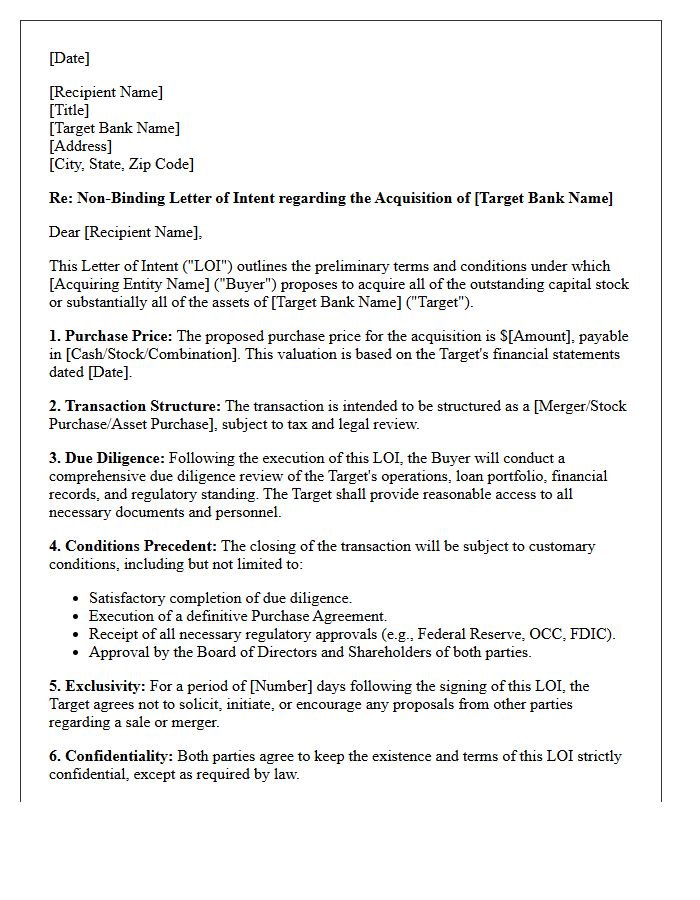

Non-Binding Letter of Intent for Bank Acquisition

A non-binding letter of intent (LOI) serves as a preliminary framework for a bank acquisition, outlining key deal terms like price and structure. Its primary purpose is to establish mutual intent before committing to expensive legal and regulatory costs. While the financial terms are typically non-obligatory, certain sections regarding exclusivity and confidentiality are legally enforceable. This document allows the acquirer to initiate detailed due diligence and seek necessary regulatory approvals, ensuring both parties are aligned on the fundamental objectives before executing a definitive purchase agreement.

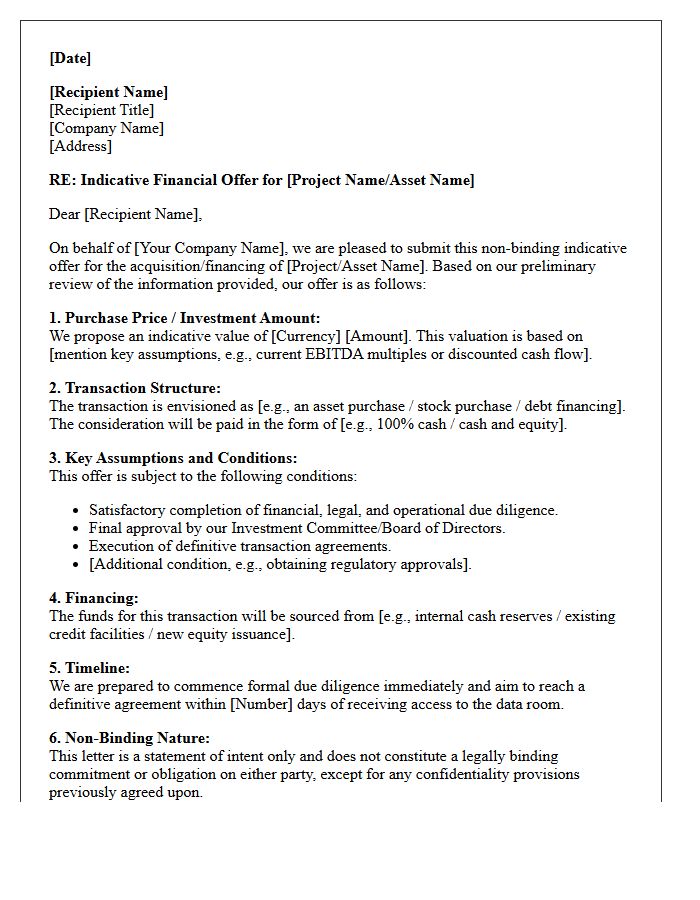

Indicative Financial Offer Letter

An Indicative Financial Offer Letter, often called a Soft Offer, is a non-binding document outlining the preliminary terms of a potential investment or acquisition. It serves as a strategic benchmark to demonstrate a buyer's serious intent before the formal due diligence process begins. Key elements typically include a valuation range, payment structure, and essential contingencies. While not a legal commitment to close the deal, it establishes the framework for future negotiations and helps sellers evaluate the credibility of competing interests in a professional transaction.

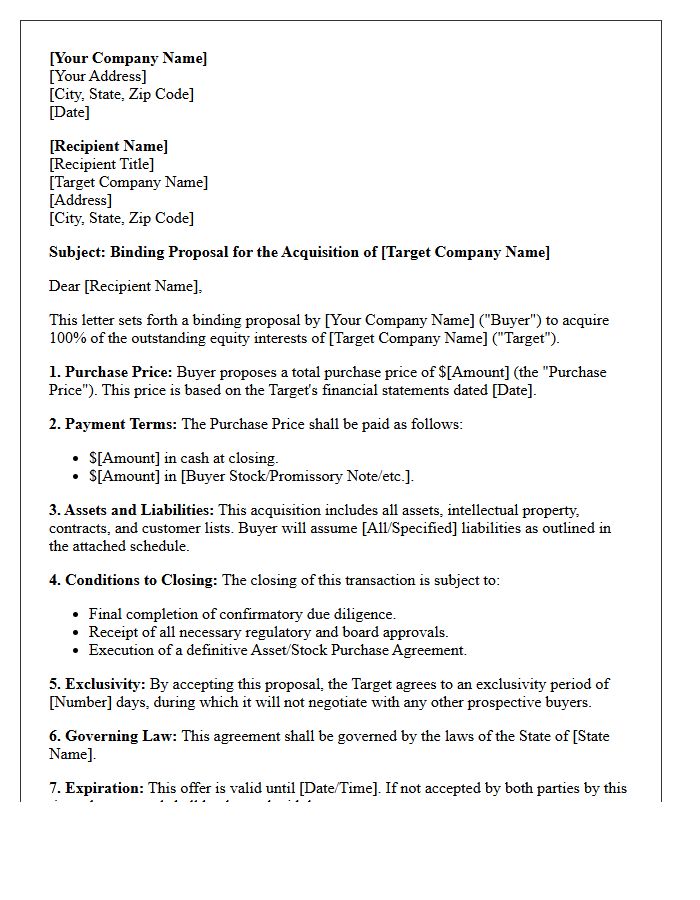

Binding Acquisition Proposal Letter

A Binding Acquisition Proposal Letter is a formal document outlining specific terms for a corporate buyout. Unlike an expression of interest, this letter constitutes a legally enforceable commitment to purchase the target company under defined conditions. It typically includes the purchase price, payment structure, and financing proof. Because it creates legal obligations, parties must ensure all contingencies and due diligence requirements are clearly stated to mitigate risks before final execution. This document serves as the definitive framework for the subsequent purchase agreement and closing process.

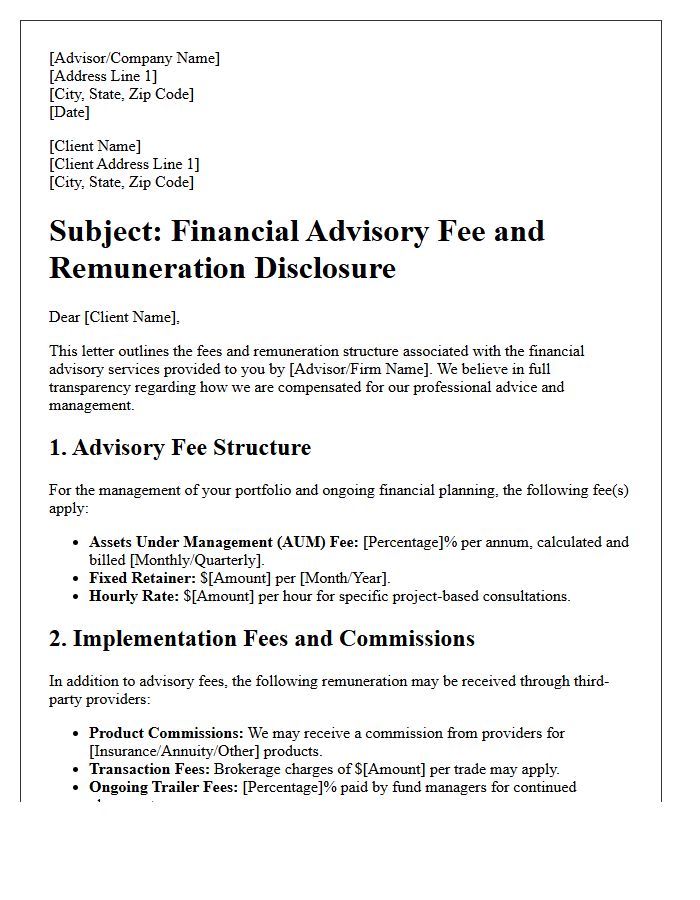

Financial Advisory Fee and Remuneration Letter

A Financial Advisory Fee and Remuneration Letter is a mandatory disclosure document ensuring transparency between advisors and clients. It outlines the specific cost structure, detailing whether services are paid via hourly rates, fixed retainers, or asset-based fees. Crucially, it identifies potential conflicts of interest by disclosing commissions received from third-party product providers. Reviewing this letter is essential for investors to understand the total expense of professional advice and to verify that the advisor's incentives align with their personal financial goals and long-term interests.

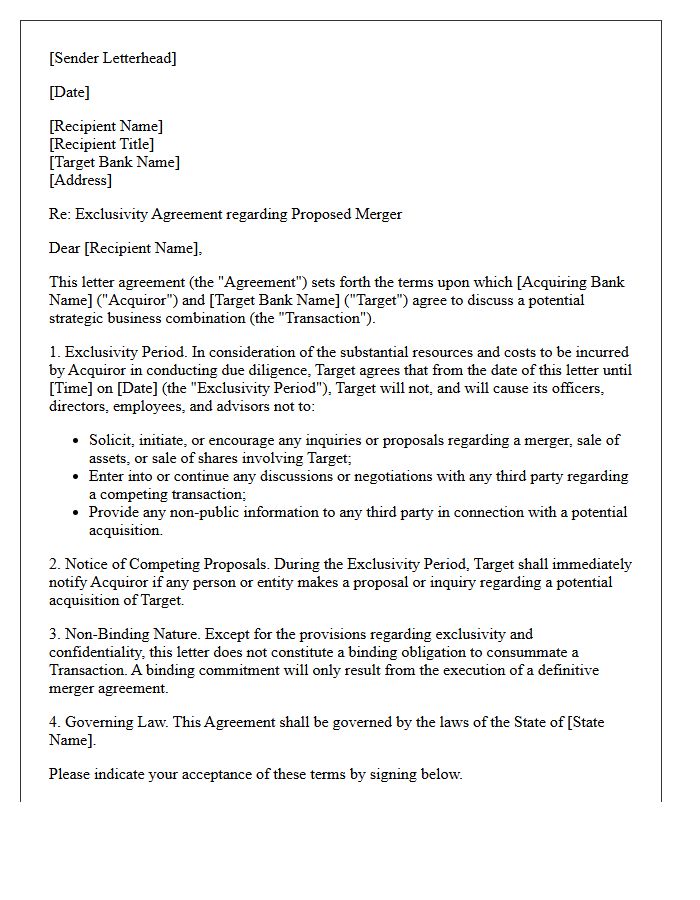

Bank Merger Target Exclusivity Letter

A Bank Merger Target Exclusivity Letter is a binding legal agreement that prevents a seller from negotiating with other potential buyers for a set timeframe. This standstill provision ensures the acquirer can conduct deep due diligence without the risk of being outbid by competitors. It protects the significant investment of time and capital required for regulatory evaluations. Establishing clear exclusivity periods and "no-shop" clauses is critical for maintaining deal momentum and securing a definitive purchase agreement in the highly regulated banking sector.

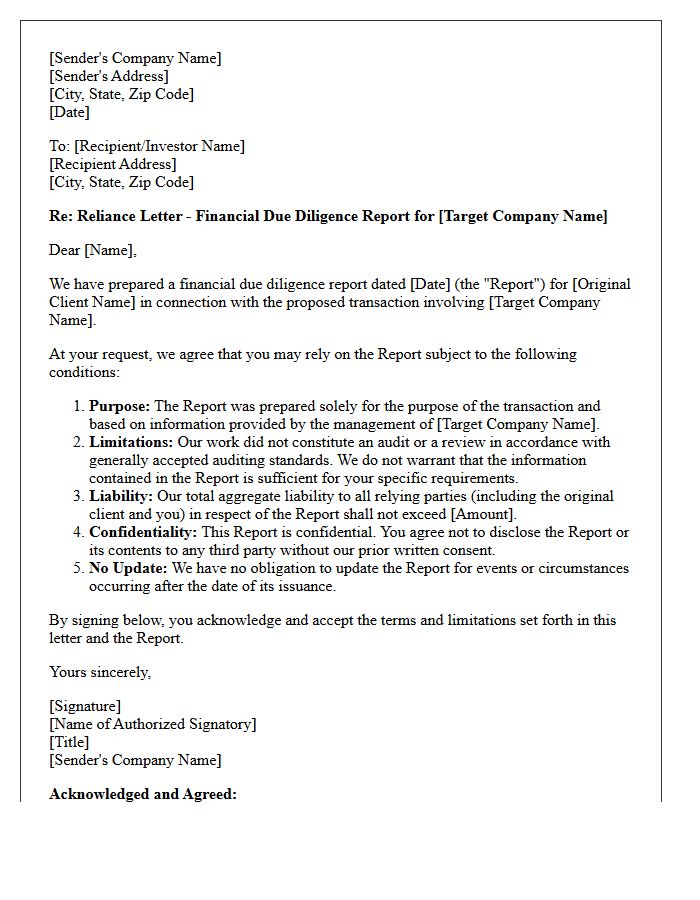

Financial Due Diligence Reliance Letter

A financial due diligence reliance letter is a formal document allowing a third party, such as a lender or investor, to legally rely on a non-disclosure report prepared for another entity. It establishes a duty of care between the advisor and the new user, defining the scope of liability and indemnification terms. This letter is essential for risk mitigation in mergers and acquisitions, ensuring that parties outside the primary engagement can trust the financial findings while acknowledging specific legal limitations and the date-sensitive nature of the underlying data.

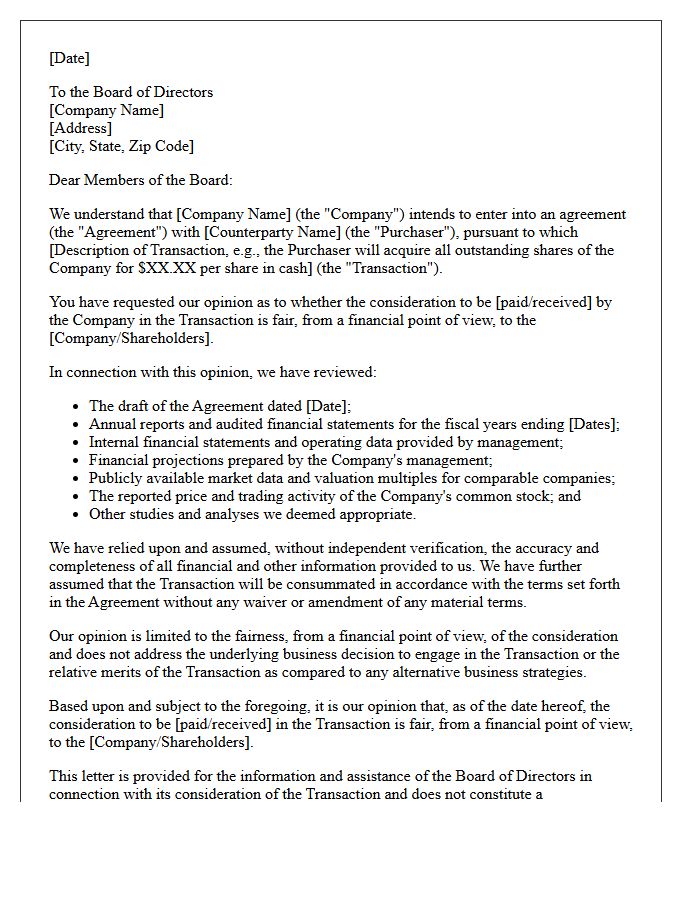

Transaction Fairness Opinion Letter

A fairness opinion is a professional report issued by an investment bank or financial advisor to a company's board of directors. It provides an objective assessment of whether the financial terms of a merger, acquisition, or significant transaction are fair from a financial point of view. This document serves as a crucial fiduciary tool, helping directors demonstrate that they acted with due care and in the best interests of shareholders. By validating the valuation, the letter mitigates legal risks and protects against potential shareholder litigation during complex corporate maneuvers.

Financial Sponsor Comfort Letter

A Financial Sponsor Comfort Letter is a formal document issued by a private equity firm to provide assurance regarding a subsidiary's ability to meet financial obligations. While typically not a legally binding guarantee, it demonstrates the parent entity's intent to support the portfolio company's liquidity or solvency. Auditors and lenders use these letters to mitigate perceived credit risks and confirm going concern status during debt financing or financial reporting. Understanding the specific wording is crucial, as it balances operational backing without creating an absolute legal liability for the sponsor.

Advisory Services Termination Letter

An Advisory Services Termination Letter is a formal document used to legally end a professional relationship between a consultant and a client. It must clearly state the effective date of cancellation to prevent future liabilities. This letter should reference specific termination clauses within the original contract, including notice periods and pending deliverables. Properly documenting the final settlement of fees and the return of confidential materials ensures a professional exit. Using a clear, concise tone helps mitigate legal risks and maintains a transparent record of the engagement's conclusion.

What is a Merger and Acquisition (M&A) financial advisory letter?

An M&A financial advisory letter, often referred to as an engagement letter, is a legally binding contract that defines the relationship between a company and an investment bank or financial advisor. It outlines the scope of services, compensation structures, and the specific terms under which the advisor will assist in a buy-side or sell-side transaction.

What are the typical fee structures included in an M&A advisory engagement letter?

Financial advisory letters typically include a non-refundable retainer fee, a success fee calculated as a percentage of the total transaction value (often following a Lehman Formula), and a reimbursement clause for out-of-pocket expenses incurred during the due diligence process.

Does an M&A advisory letter include a "tail period" clause?

Yes, most advisory letters contain a tail period clause, which ensures the financial advisor receives their success fee if the company completes a transaction with a party introduced by the advisor within a specific timeframe-usually 12 to 24 months-after the engagement has officially ended.

What is the "Scope of Services" defined in a financial advisory letter?

The scope of services details the advisor's responsibilities, which generally include valuation analysis, identifying potential buyers or targets, preparing marketing materials like the Confidential Information Memorandum (CIM), coordinating due diligence, and providing a fairness opinion to the board of directors.

Are exclusivity provisions standard in M&A financial advisory letters?

Yes, most financial advisory letters include an exclusivity provision that prevents the client from engaging other investment banks or financial advisors for the same transaction during the term of the agreement, ensuring the lead advisor is the sole intermediary for the deal.

Comments