An Audit Confirmation Letter is a formal request used by auditors to verify the details of an entity's Letter of Credit Outstanding with financial institutions. This process ensures the accuracy of reported contingent liabilities and financial obligations during year-end reporting. It confirms balances, expiry dates, and terms directly with the bank. To assist your documentation, below are some ready to use template.

Image cover: Mastering Letter of Credit Outstanding Audit Confirmations: Essential Samples and Templates

Letter Samples List

- Issuing Bank Letterhead and Date of Letter

- Auditor Address for the Confirmation Letter

- Client Consent for Letter of Credit Disclosure

- Irrevocable Letter of Credit Reference Number

- Applicant and Beneficiary of the Letter

- Issuance and Expiry Date of the Letter

- Outstanding Currency and Amount of the Letter

- Drafts Drawn Against the Letter of Credit

- Remaining Available Balance of the Letter

- Cash Margin Held for the Letter of Credit

- Exceptions or Amendments to the Letter

- Authorized Bank Signature for the Letter

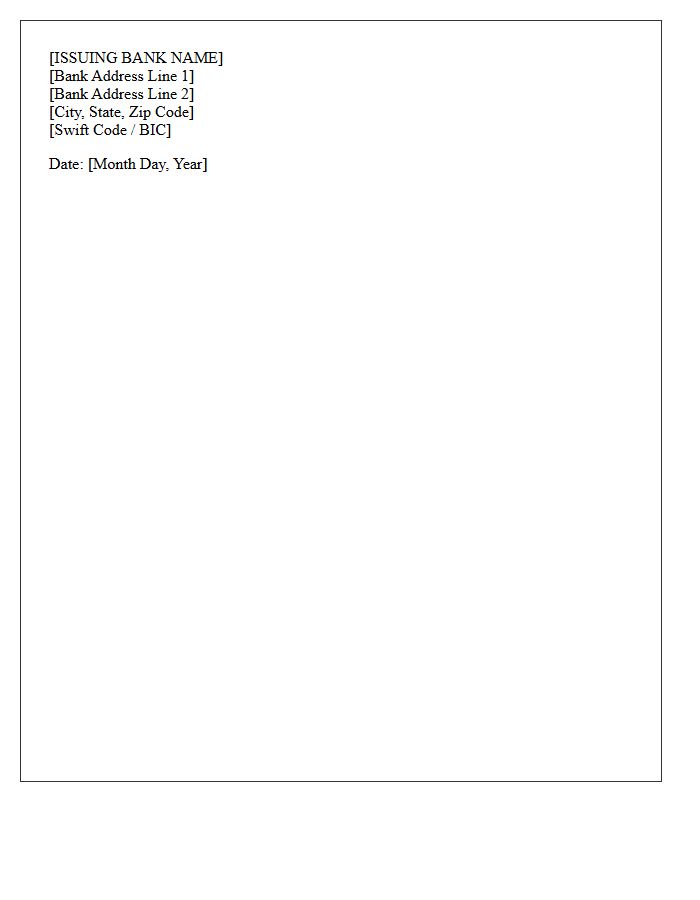

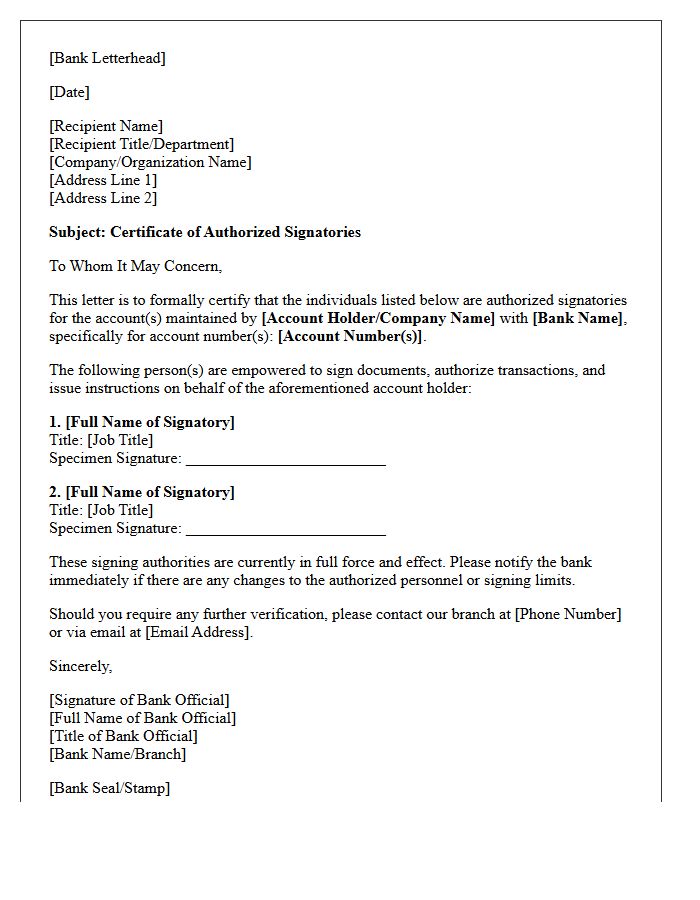

Issuing Bank Letterhead and Date of Letter

The Issuing Bank Letterhead serves as an essential authentication feature in trade finance. It confirms the document's legal origin and provides official contact details of the financial institution. Meanwhile, the Date of Letter establishes the specific point in time when the instrument becomes effective or is issued. These elements are critical for verifying documentary validity, ensuring compliance with international banking standards, and determining expiration timelines for letters of credit or guarantees. Missing or inconsistent header information can lead to immediate rejection by corresponding banks or regulatory authorities.

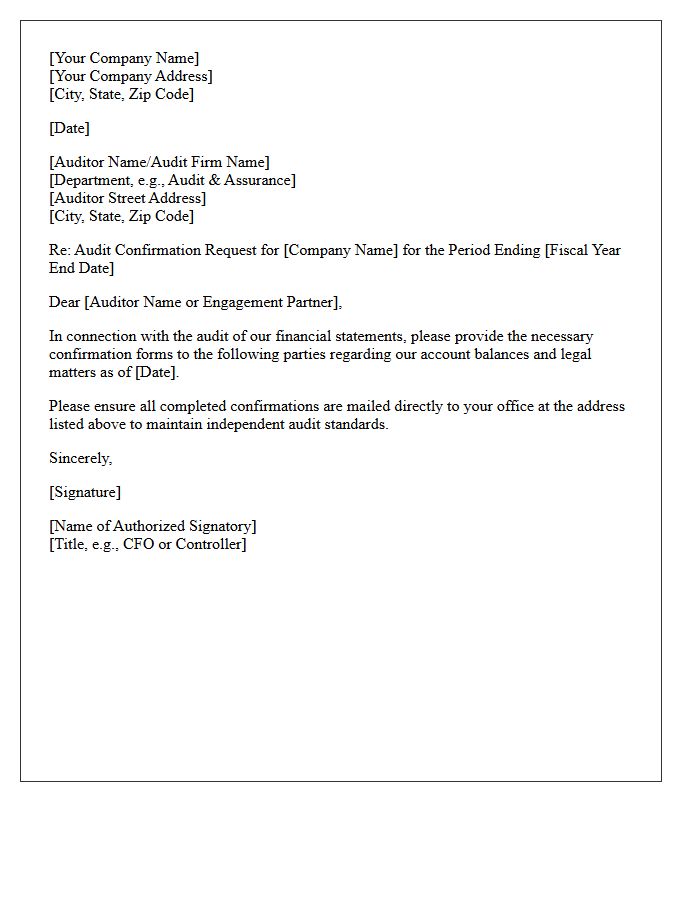

Auditor Address for the Confirmation Letter

The auditor address on a confirmation letter is the specific location where third parties must return financial verification documents. It is crucial to ensure this address reflects the audit firm's official office rather than the client's business site to maintain independence and prevent data tampering. Using the correct destination guarantees that confidential evidence, such as bank balances or accounts receivable, reaches the auditors directly. Always verify the full mailing details or secure digital portal links before dispatching requests to avoid processing delays during the financial statement audit.

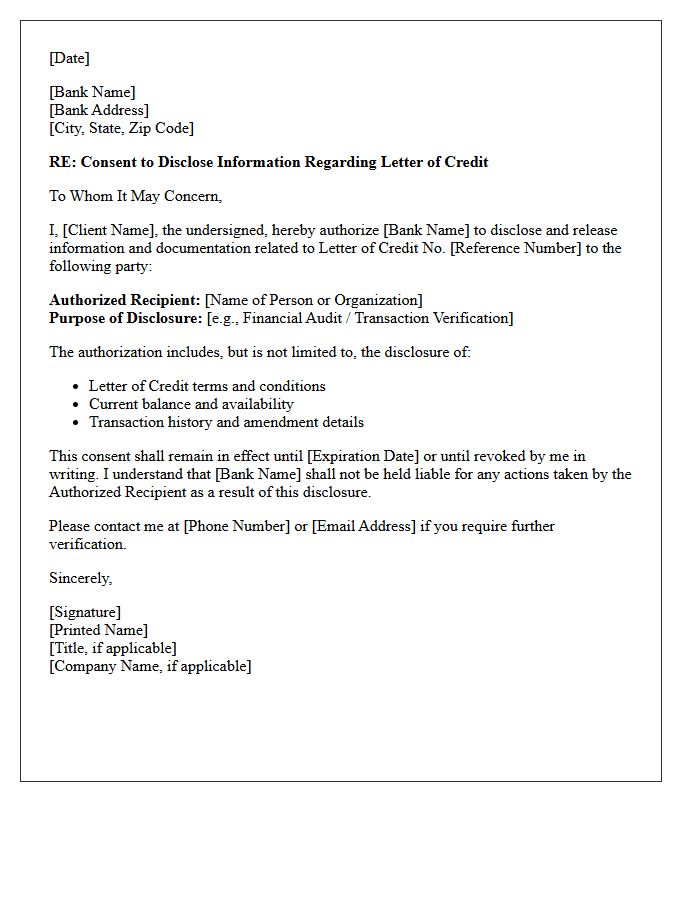

Client Consent for Letter of Credit Disclosure

Obtaining explicit client consent is essential before sharing sensitive transaction details with financial institutions. This authorization ensures compliance with confidentiality obligations and data protection regulations. Without a signed waiver or formal agreement, disclosing underlying commercial contracts to banks for a Letter of Credit issuance may lead to legal liability. Prioritizing informed consent safeguards the professional relationship while facilitating the secure verification of credit terms and trade documents during the financing process.

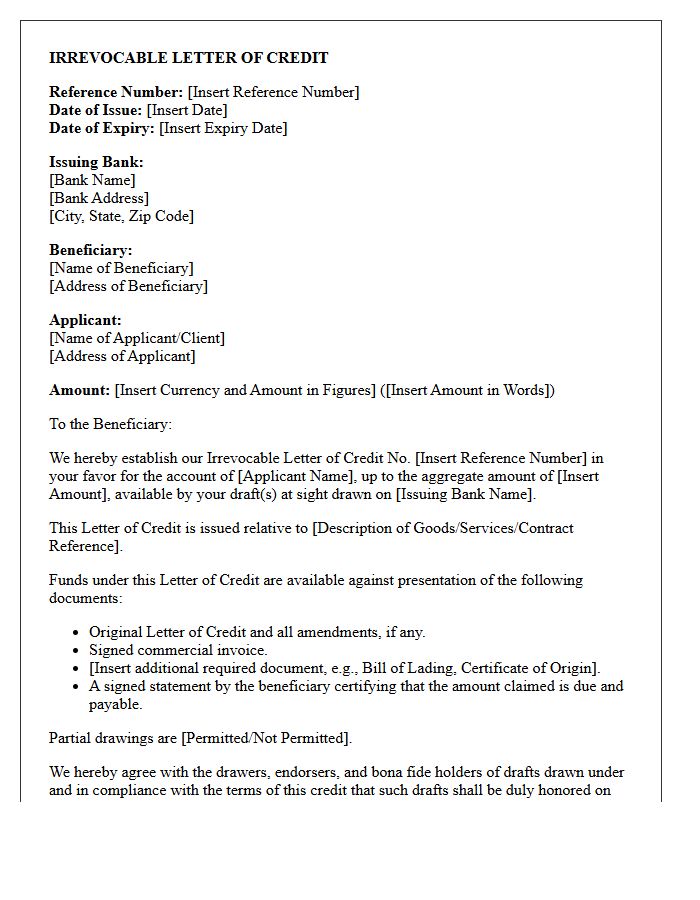

Irrevocable Letter of Credit Reference Number

The Irrevocable Letter of Credit Reference Number is a unique alphanumeric identifier used to track and manage guaranteed payment obligations in international trade. This specific code ensures that the issuing bank cannot cancel or modify the credit terms without the consent of all involved parties. It is essential for documentation, allowing exporters to verify the financial commitment and securely link shipping documents to the correct transaction. Precise use of this reference ensures efficient fund transfers and mitigates payment risks between buyers and sellers globally.

Applicant and Beneficiary of the Letter

In trade finance, the Applicant is the buyer or importer who requests a financial institution to issue a credit. They are responsible for providing collateral and defining transaction terms. Conversely, the Beneficiary is the seller or exporter who receives payment upon presenting compliant documents. Understanding these roles is crucial because the issuing bank represents the applicant's creditworthiness to the beneficiary. Ensuring accurate details for the party names and addresses is vital to avoid discrepancies, ensuring a secure transfer of funds between the involved international trading entities.

Issuance and Expiry Date of the Letter

When reviewing a letter of credit or official document, the Issuance Date marks the beginning of the legal obligation and contract validity. Equally critical is the expiry date, which establishes the final deadline for document presentation and credit utilization. Parties must ensure all terms are met before this cutoff, as a late submission typically results in a discrepancy and potential loss of payment rights. Always verify these dates against the shipping schedule to maintain full compliance and financial security throughout the transaction process.

Outstanding Currency and Amount of the Letter

The Outstanding Currency and amount represent the current financial obligation remaining under a credit facility. It is essential to verify the face value minus any processed drawings or expirations to determine the exact liability. This figure must align with the ISO currency code specified in the agreement to avoid exchange rate discrepancies. Monitoring these values ensures accurate credit limit management and prevents over-extension of trade finance obligations during the letter's validity period.

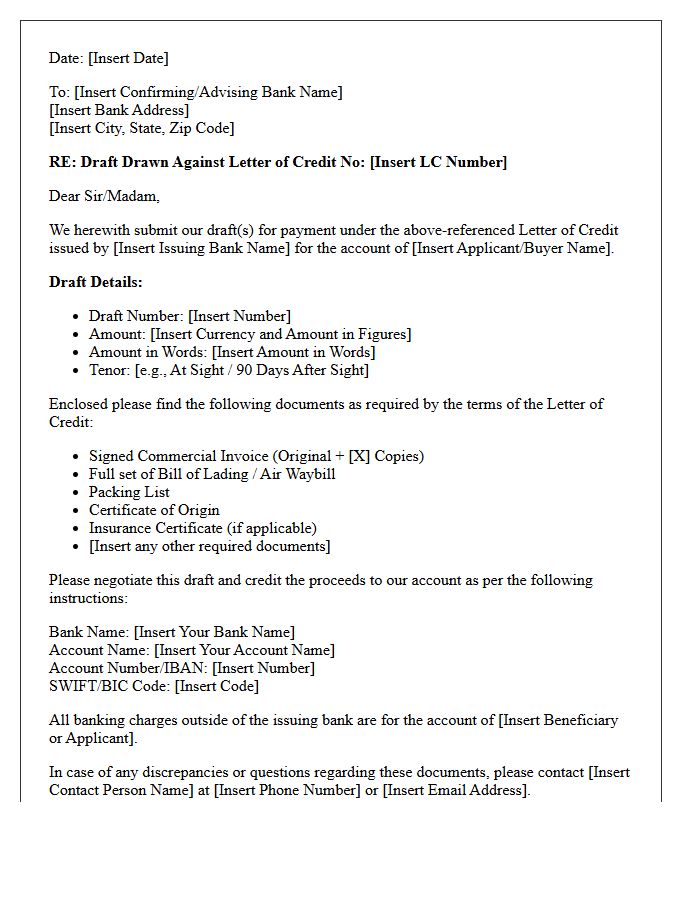

Drafts Drawn Against the Letter of Credit

Drafts drawn against a Letter of Credit act as formal demands for payment in international trade. These financial instruments, often called bills of exchange, ensure the seller receives funds once specific conditions are met. A sight draft requires immediate payment upon presentation, while a time draft allows for credit terms. Banks verify that all accompanying shipping documents strictly comply with the credit terms before honoring the draft. This mechanism mitigates risk for both exporters and importers by guaranteeing payment through a trusted financial intermediary rather than relying solely on the buyer's creditworthiness.

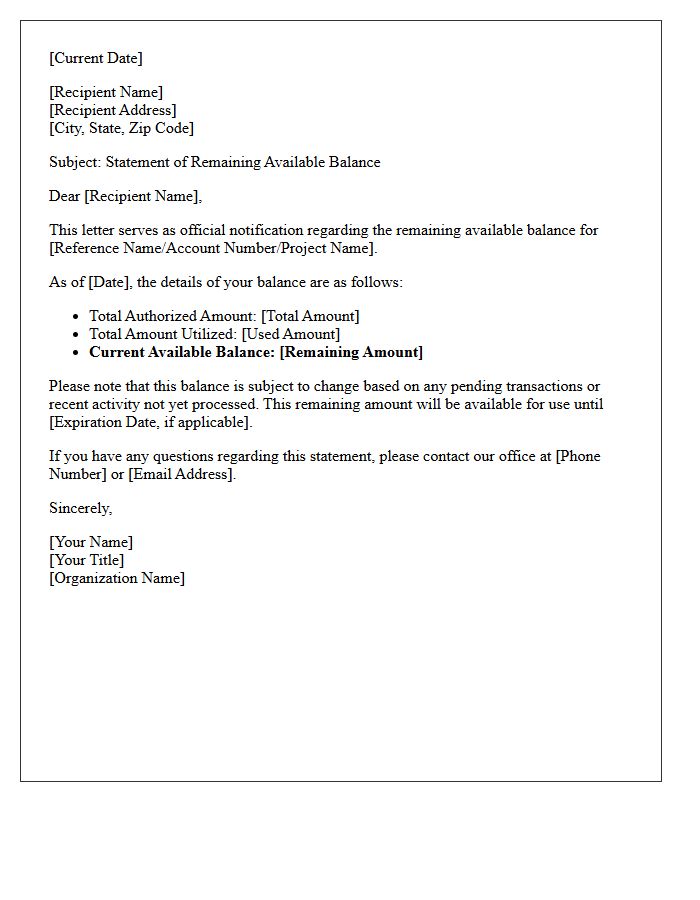

Remaining Available Balance of the Letter

The Remaining Available Balance of a Letter of Credit represents the current undrawn amount accessible to the beneficiary. This figure decreases each time a partial shipment or drawing is processed against the total credit value. Monitoring this balance is critical for managing credit limits and ensuring sufficient funds remain for future transactions. If the balance reaches zero, no further payments can be executed unless the credit is officially amended. Always verify this amount against bank statements to prevent discrepancies during the trade settlement process.

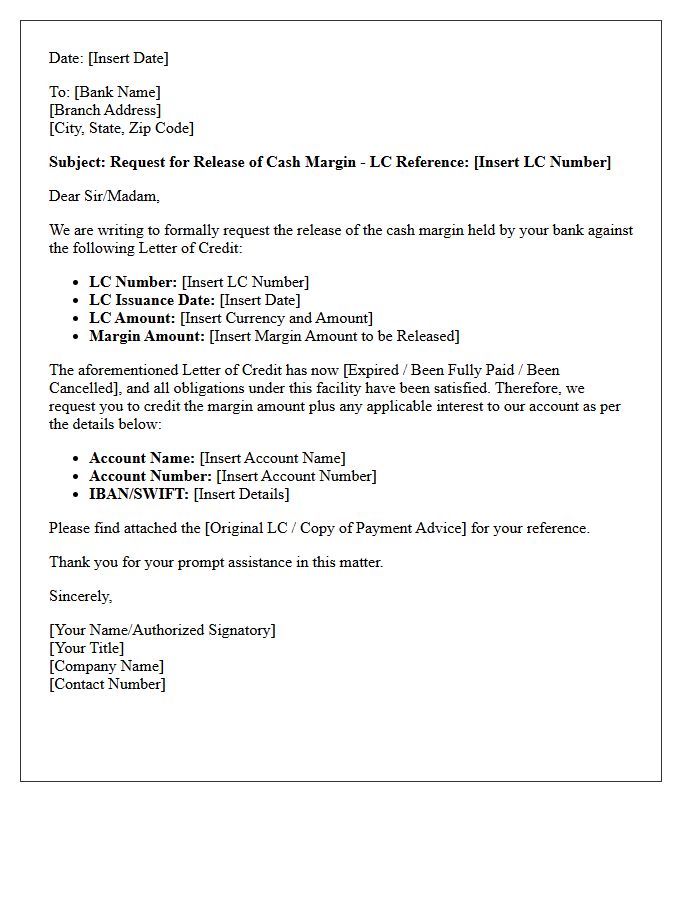

Cash Margin Held for the Letter of Credit

A cash margin is a security deposit held by a bank to mitigate credit risk when issuing a letter of credit. This collateral ensures the bank can fulfill payment obligations to the beneficiary if the applicant defaults. Depending on the buyer's creditworthiness, the bank may require a partial or full deposit of the total transaction value. These funds are typically restricted and remain inaccessible to the applicant until the instrument is settled or expires, providing financial security and facilitating international trade trust between parties.

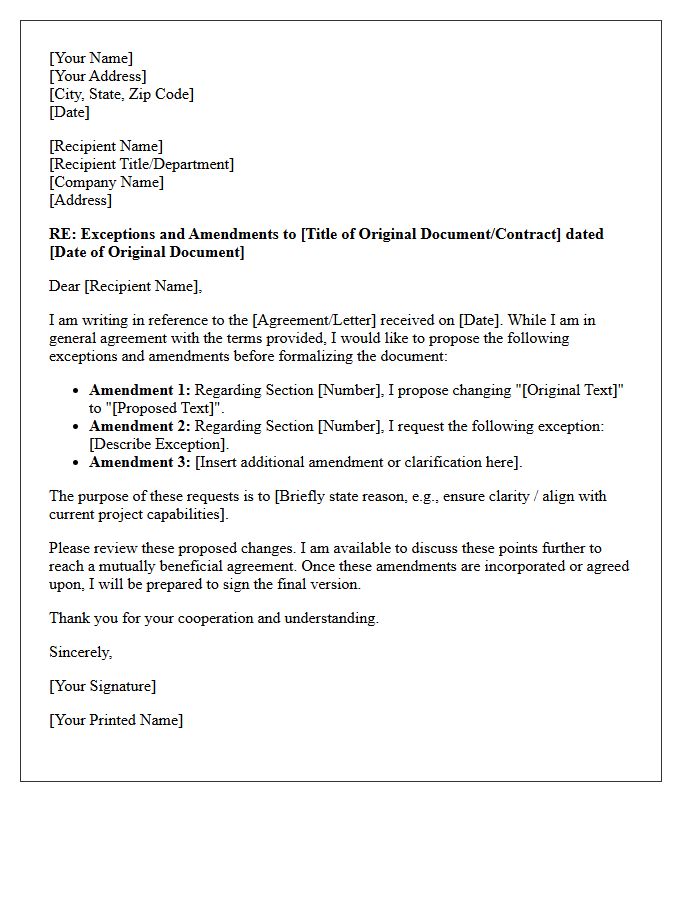

Exceptions or Amendments to the Letter

When dealing with legal correspondence, Exceptions or Amendments serve as critical modifications to the original terms. An amendment formally alters specific clauses, while an exception excludes certain conditions from enforcement. To ensure validity, these changes must be documented in writing and signed by all involved parties. This process maintains legal clarity and prevents future disputes. Always cross-reference any supplemental agreements with the primary letter to confirm that the most recent updates take precedence in a binding agreement.

Authorized Bank Signature for the Letter

An authorized bank signature is a formal validation confirming that a document is legally binding and recognized by the financial institution. It ensures the authenticity of the letter, verifying that the signatory possesses the necessary legal power to execute transactions or verify account details. For international business or credit facilities, this signature must often be accompanied by an official bank stamp or seal. Ensuring the signer has the correct mandate is essential to prevent processing delays and maintain the document's legal integrity in professional financial correspondence.

What is a Letter of Credit Outstanding Audit Confirmation Letter?

An audit confirmation letter for outstanding Letters of Credit is a formal request sent by an entity to its financial institution to verify the details, balances, and terms of all active documentary or standby letters of credit as of a specific reporting date.

Why do auditors require confirmation of outstanding Letters of Credit?

Auditors use these confirmations to verify the existence and accuracy of contingent liabilities, ensure all financial commitments are properly disclosed on the balance sheet, and mitigate the risk of unrecorded liabilities or financial misstatements.

What key information should be included in a Letter of Credit audit response?

A comprehensive response should include the letter of credit number, the expiry date, the total face value, the current outstanding balance, the name of the beneficiary, and any collateral or security interests held against the credit facility.

What is the difference between confirming a Standby Letter of Credit and a Commercial Letter of Credit?

While both require confirmation, a Commercial Letter of Credit is a primary payment mechanism for trade, whereas a Standby Letter of Credit acts as a secondary payment guarantee; auditors confirm both to assess different levels of risk and potential financial exposure.

How does an audit confirmation help in detecting undisclosed financial obligations?

By communicating directly with the bank (third-party verification), auditors can identify Letters of Credit that may have been omitted from the company's internal records, ensuring that all off-balance sheet arrangements and credit risks are transparently reported.

Comments