A Safe Custody and Pledged Securities Audit Confirmation Letter is an essential document used to verify the existence and status of investment assets held by third parties. It ensures financial reporting accuracy by confirming legal ownership and any existing liens or encumbrances. Streamline your verification process with our professional guidance; below are some ready to use template options.

Image cover: Mastering the Audit Confirmation Process for Safe Custody and Pledged Securities: Essential Templates and Best Practices

Letter Samples List

- Standard Safe Custody Audit Confirmation Letter

- Standard Pledged Securities Audit Confirmation Letter

- Third-Party Custodian Audit Confirmation Letter

- Client Authorization For Audit Disclosure Letter

- Pledged Collateral Verification Audit Letter

- Physical Securities Custody Audit Letter

- Dematerialized Securities Custody Audit Letter

- Government Bond Pledge Confirmation Letter

- Corporate Equity Safe Custody Audit Letter

- Safe Custody Discrepancy Resolution Letter

- Pledged Asset Release Audit Confirmation Letter

- Consolidated Securities Audit Confirmation Letter

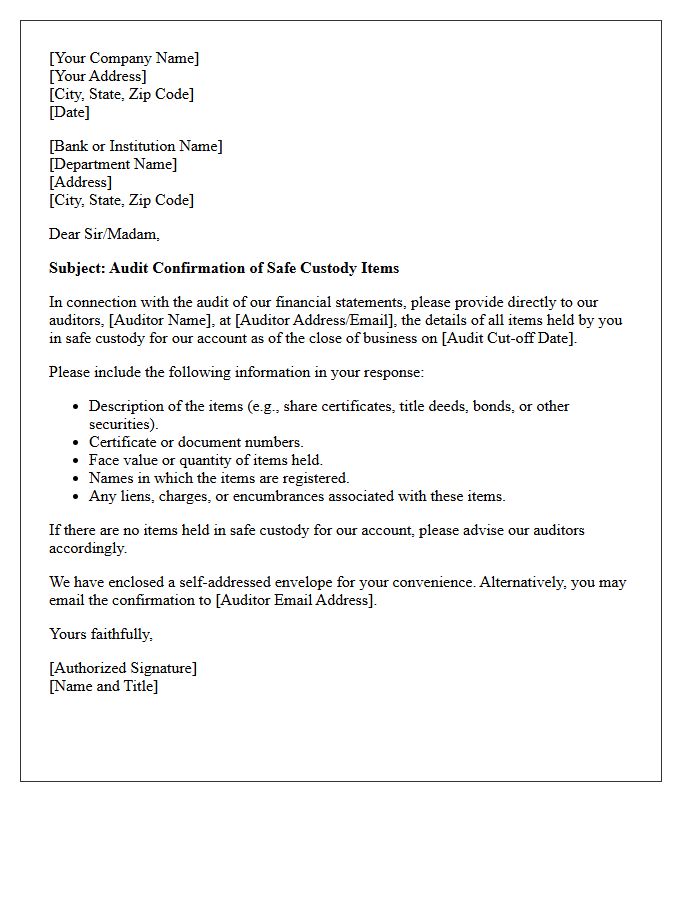

Standard Safe Custody Audit Confirmation Letter

A Standard Safe Custody Audit Confirmation Letter is a formal request used by auditors to verify assets held by a third-party custodian. This document ensures the existence and ownership of securities, gold, or title deeds kept in bank vaults. It serves as critical audit evidence to prevent financial misstatement. The custodian must confirm the specific details, quantities, and any encumbrances on the items held. Accurate reconciliation of these records is essential for maintaining regulatory compliance and ensuring the integrity of a company's financial reporting process.

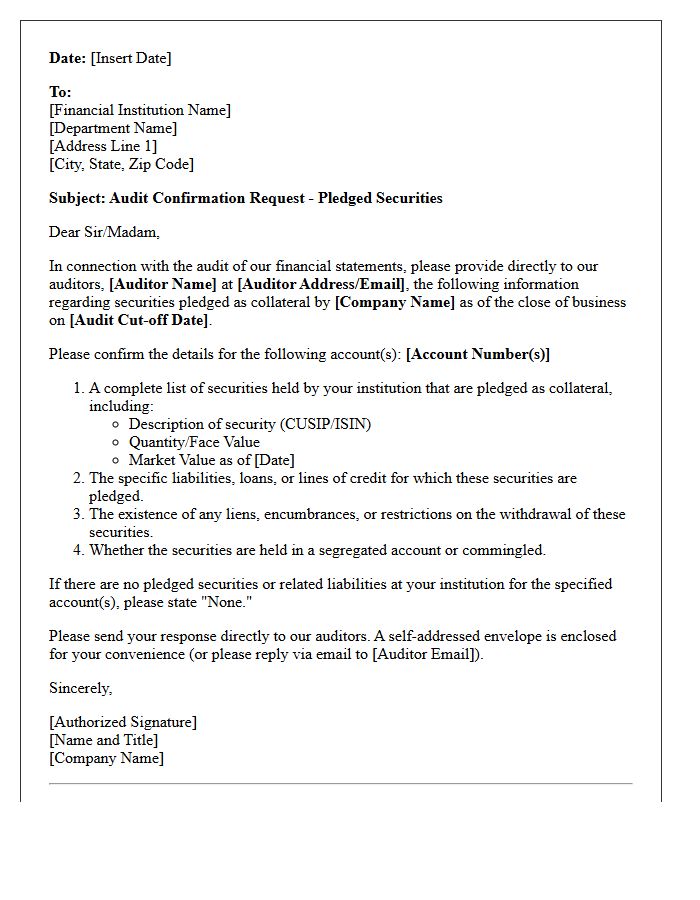

Standard Pledged Securities Audit Confirmation Letter

A Standard Pledged Securities Audit Confirmation Letter is a formal request used by auditors to verify the existence and details of assets held as collateral. This document ensures that securities pledged to third parties are accurately recorded on the balance sheet. It confirms critical information, including the quantity, market value, and specific terms of the lien or encumbrance. Accurate reporting is essential for maintaining financial transparency and identifying potential liquidity risks, providing stakeholders with assurance that all encumbered assets are disclosed according to accounting standards.

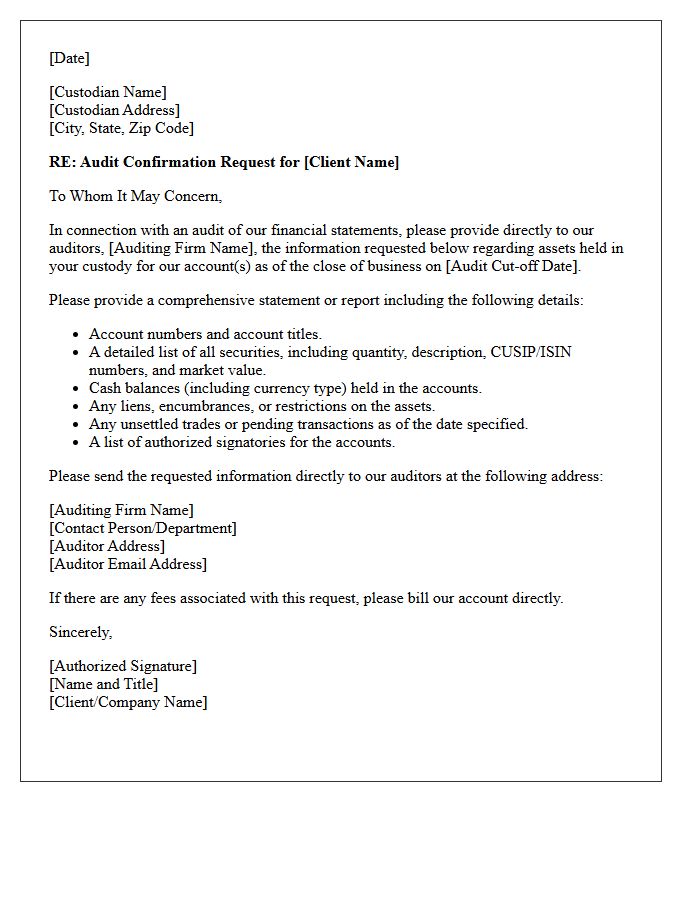

Third-Party Custodian Audit Confirmation Letter

A Third-Party Custodian Audit Confirmation Letter is a formal document used to verify the existence and ownership of assets held externally. During financial examinations, auditors send these requests to independent financial institutions to ensure asset valuation and quantities match the client's records. This process is a critical internal control that prevents fraud and confirms safekeeping compliance. By obtaining direct verification from the custodian, auditors gain high-quality evidence regarding the accuracy of financial statements and the physical security of investment holdings.

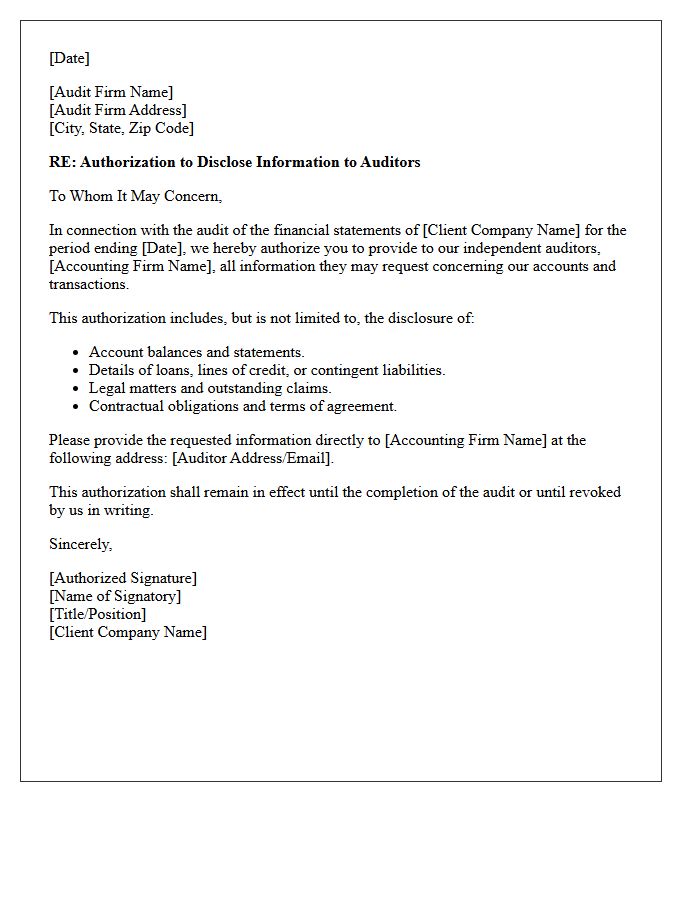

Client Authorization For Audit Disclosure Letter

A Client Authorization For Audit Disclosure Letter is a formal document that permits auditors to communicate directly with a client's legal counsel. This authorization is essential for verifying pending litigation, potential liabilities, and financial claims that could impact financial statements. By signing this waiver, the client allows the disclosure of privileged information, ensuring the audit complies with professional standards while maintaining transparency between auditors and attorneys. It is a critical component of the year-end financial reporting process to ensure accuracy and risk management.

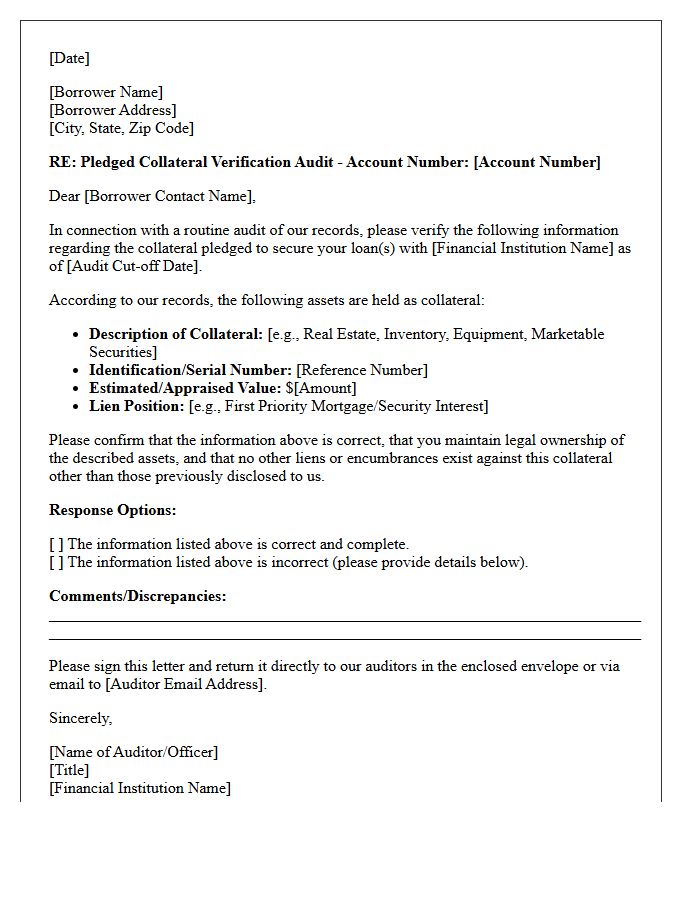

Pledged Collateral Verification Audit Letter

A Pledged Collateral Verification Audit Letter is a formal request sent by auditors to verify the existence and value of assets used as security for a loan. This document ensures that the collateral pledged to a lender remains restricted and accurately reported on financial statements. It confirms critical details such as asset descriptions, account balances, and lien status directly with the holding institution. Accurate verification is essential for regulatory compliance, risk management, and maintaining the integrity of secured lending agreements between creditors and borrowers.

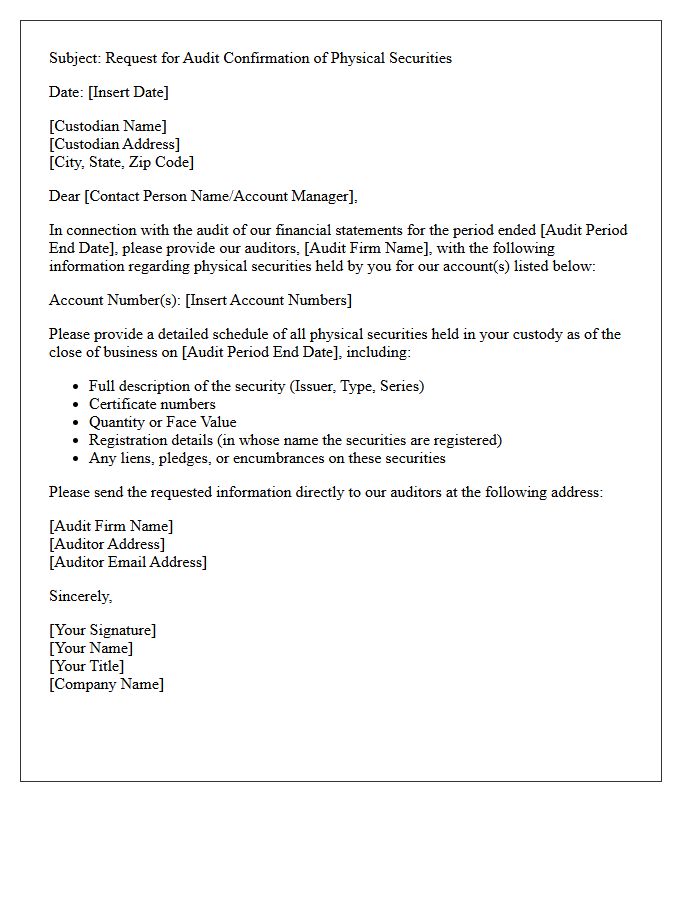

Physical Securities Custody Audit Letter

A Physical Securities Custody Audit Letter is a formal document verifying that a financial institution physically holds tangible asset certificates on behalf of investors. This independent verification ensures the existence and safekeeping of paper-based instruments like stock certificates or bonds. The audit mitigates risks of fraud, loss, or misappropriation by reconciling internal records with actual vault inventory. For high-net-worth individuals and institutional clients, this letter serves as essential regulatory proof of ownership and security for non-electronic holdings within a controlled custodial environment.

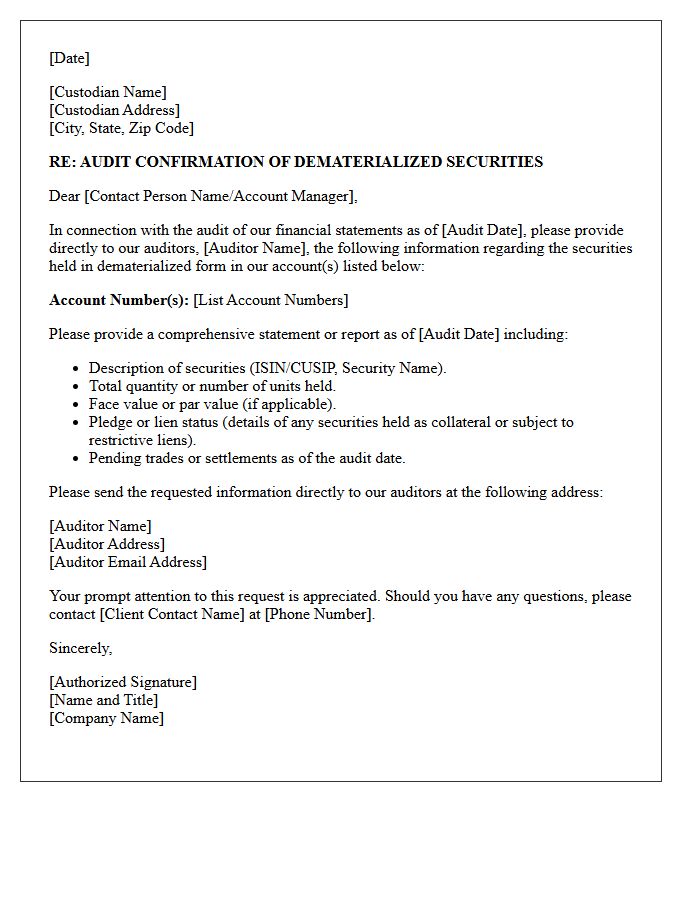

Dematerialized Securities Custody Audit Letter

A Dematerialized Securities Custody Audit Letter is a critical verification document issued by an independent auditor. It confirms the existence and ownership of digital financial assets held in a central depository rather than physical certificates. This report ensures that the custodian's records accurately reflect the client's holdings and comply with regulatory standards. For investors and institutions, this audit provides essential transparency, mitigates the risk of fraud, and validates the integrity of electronic security positions within the financial system.

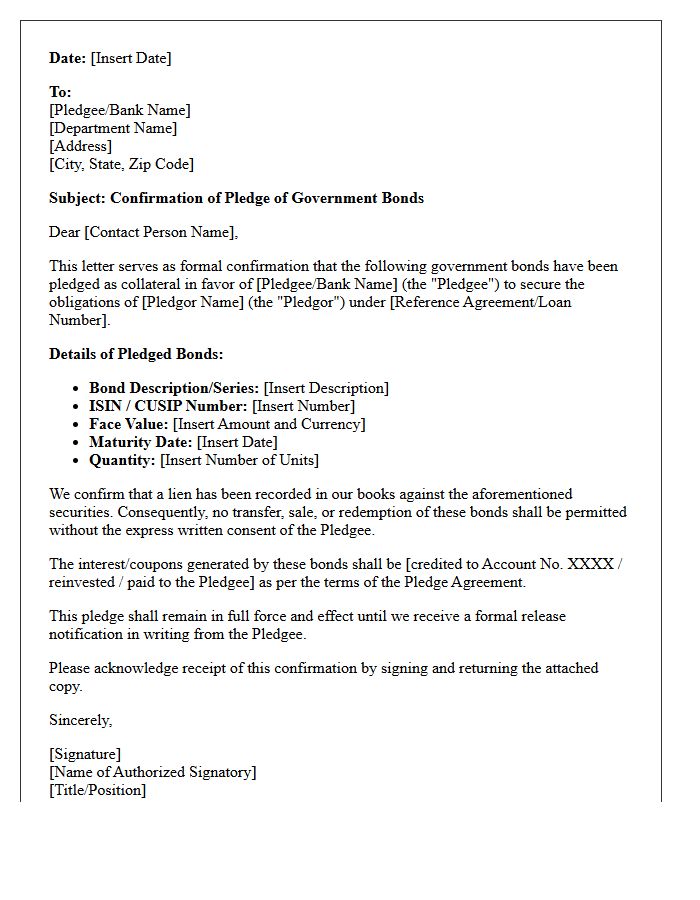

Government Bond Pledge Confirmation Letter

A Government Bond Pledge Confirmation Letter is an official document verifying that specific government securities are being used as collateral to secure a loan or credit facility. This letter confirms that the pledge has been formally recorded, restricting the owner from selling the assets until the obligation is met. It provides legal assurance to the lender regarding the existence and lien status of the bonds. Understanding this document is essential for maintaining transparency in financial transactions and ensuring the protection of both the borrower's assets and the creditor's interests.

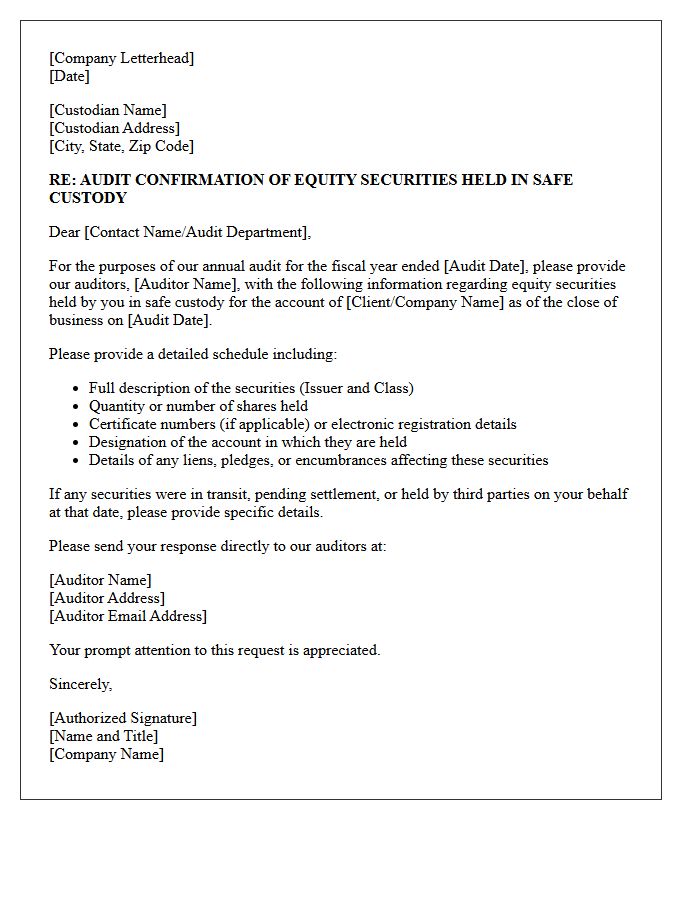

Corporate Equity Safe Custody Audit Letter

A Corporate Equity Safe Custody Audit Letter is a formal verification document confirming that an organization's share certificates and equity holdings are securely held. Independent auditors issue this letter to provide assurance that assets reported on the balance sheet physically exist and are protected against loss or unauthorized transfer. It plays a critical role in financial transparency and internal controls, ensuring that the legal ownership of securities is accurately represented during compliance audits and for stakeholder verification purposes.

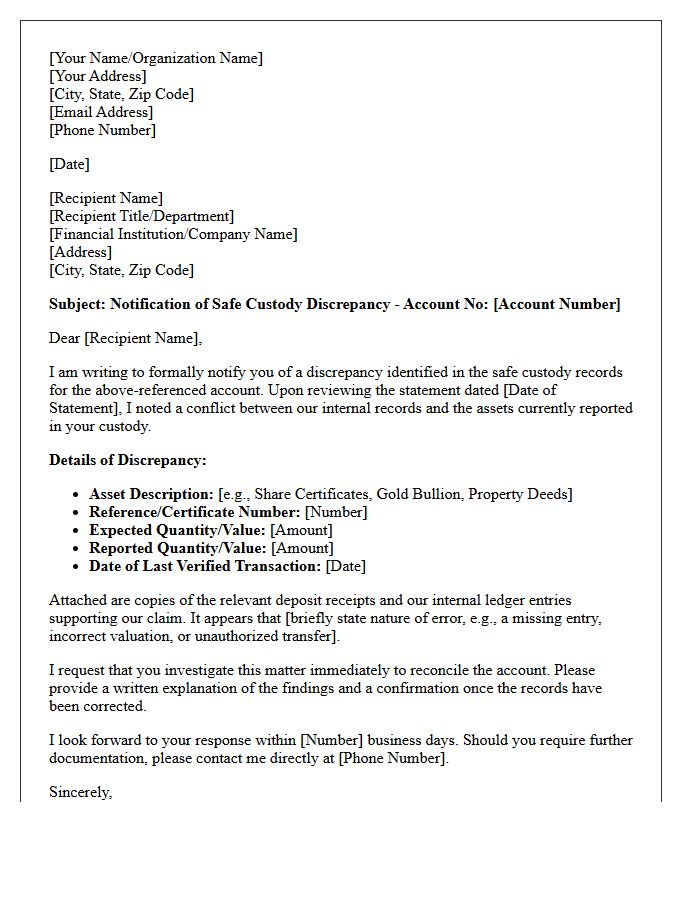

Safe Custody Discrepancy Resolution Letter

A Safe Custody Discrepancy Resolution Letter is a formal document used to rectify inconsistencies between physical assets and recorded inventory held in safekeeping. This letter initiates a reconciliation process by identifying specific errors in account balances, certificate numbers, or asset descriptions. It serves as essential legal evidence for audits and compliance, ensuring that custodial records accurately reflect held securities. Promptly issuing this letter is vital for mitigating financial risk, resolving administrative oversight, and protecting the integrity of high-value investments within a financial institution or private vault.

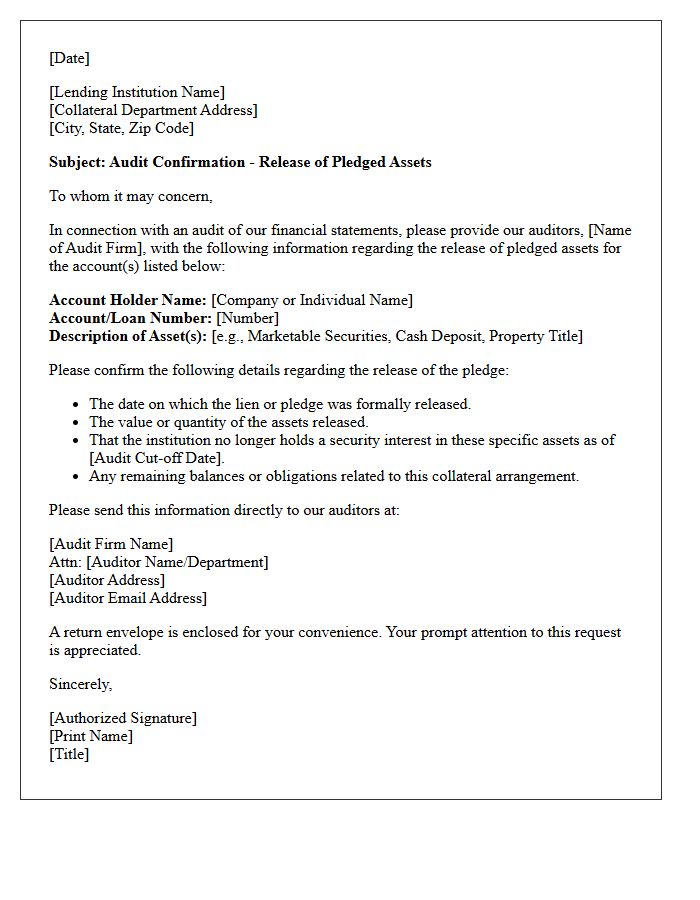

Pledged Asset Release Audit Confirmation Letter

A Pledged Asset Release Audit Confirmation Letter is a formal document sent by an auditor to a financial institution to verify that collateral previously used to secure a loan has been officially released. This process ensures the legal lien is terminated and the asset's status is accurately reflected in financial statements. It serves as critical third-party evidence that the debt obligation is satisfied and the owner regained full control over the asset. Accuracy in this confirmation is essential for maintaining regulatory compliance and transparent audit trails during corporate reviews.

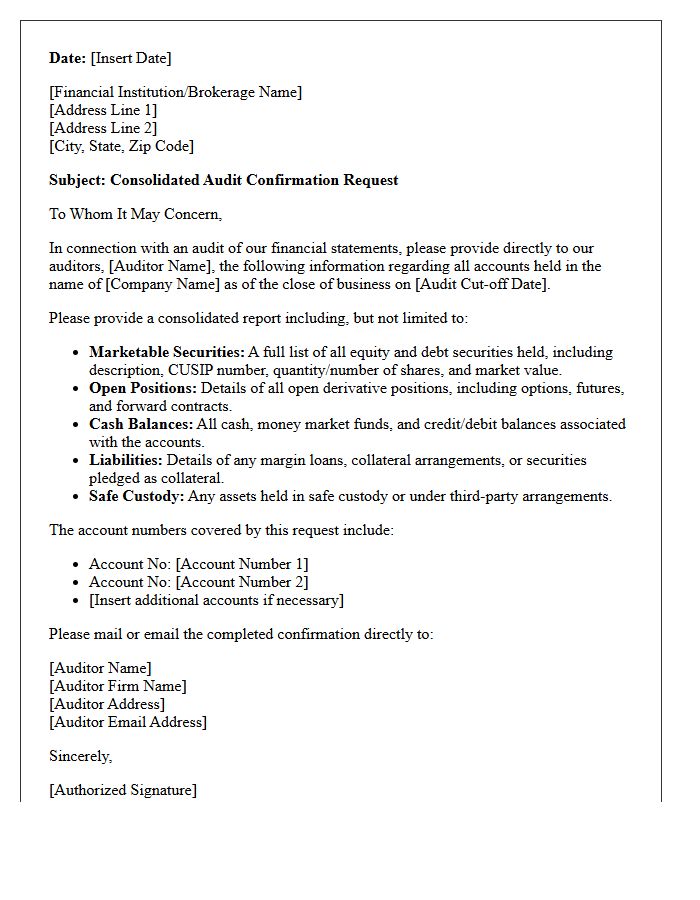

Consolidated Securities Audit Confirmation Letter

A Consolidated Securities Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify a client's asset holdings. This document ensures the existence, ownership, and valuation of diverse investment portfolios, including stocks and bonds. It serves as critical audit evidence to prevent financial misstatement and detect unrecorded liabilities. By centralizing multiple accounts into one report, it streamlines the verification process, providing independent third-party assurance that the financial statements accurately reflect the entity's true investment position at year-end.

What is a Safe Custody and Pledged Securities Audit Confirmation Letter?

An audit confirmation letter for safe custody and pledged securities is a formal request sent by auditors to financial institutions to verify the existence, ownership, and valuation of assets held in custody or used as collateral for loans as of a specific reporting date.

Why do auditors require verification of pledged securities?

Auditors verify pledged securities to ensure that any liens or encumbrances on an entity's assets are accurately disclosed in the financial statements and to confirm that the entity has legal title to the securities being reported.

What information is typically included in a safe custody confirmation?

A standard confirmation includes the description of the securities, unique identification numbers (such as ISIN or CUSIP), the quantity of shares or face value of bonds, the name of the registered holder, and the specific location or account where the assets are being held.

How does a pledge arrangement affect the audit of investment assets?

A pledge arrangement indicates that the securities are restricted and serve as security for a liability. Auditors must confirm the terms of the pledge to ensure the assets are not double-counted and that the associated risks and liquidity restrictions are properly reflected in the financial notes.

What is the difference between safe custody and pledged assets in an audit context?

Safe custody refers to assets held by a third party for safekeeping without any lien, while pledged assets are those specifically marked as collateral for a debt obligation. The audit confirmation distinguishes between these to verify asset availability and any potential claims against the company's resources.

Comments