An Auditor Comfort Letter is a critical financial document provided during securities offerings to verify financial data not covered by audited reports. It offers assurance to underwriters, helping them establish a "due diligence" defense against liability under securities laws. This essential bridge ensures transparency and builds trust between issuers and investors. To assist your process, below are some ready to use templates.

Image cover: The Comprehensive Guide to Auditor Comfort Letters for Underwriting Agreements: Samples and Templates

Letter Samples List

- Initial Public Offering Auditor Comfort Letter

- Bring-Down Auditor Comfort Letter

- Loan Loss Provisioning Financial Comfort Letter

- Capital Adequacy Ratio Verification Comfort Letter

- Interim Unaudited Financial Statement Comfort Letter

- Subsequent Events Review Comfort Letter

- Medium Term Note Debt Issuance Comfort Letter

- Asset-Backed Securitization Comfort Letter

- Pro Forma Financial Information Comfort Letter

- Regulatory Compliance and Controls Comfort Letter

- Basel Liquidity Coverage Ratio Comfort Letter

- Subordinated Tier Two Capital Issuance Comfort Letter

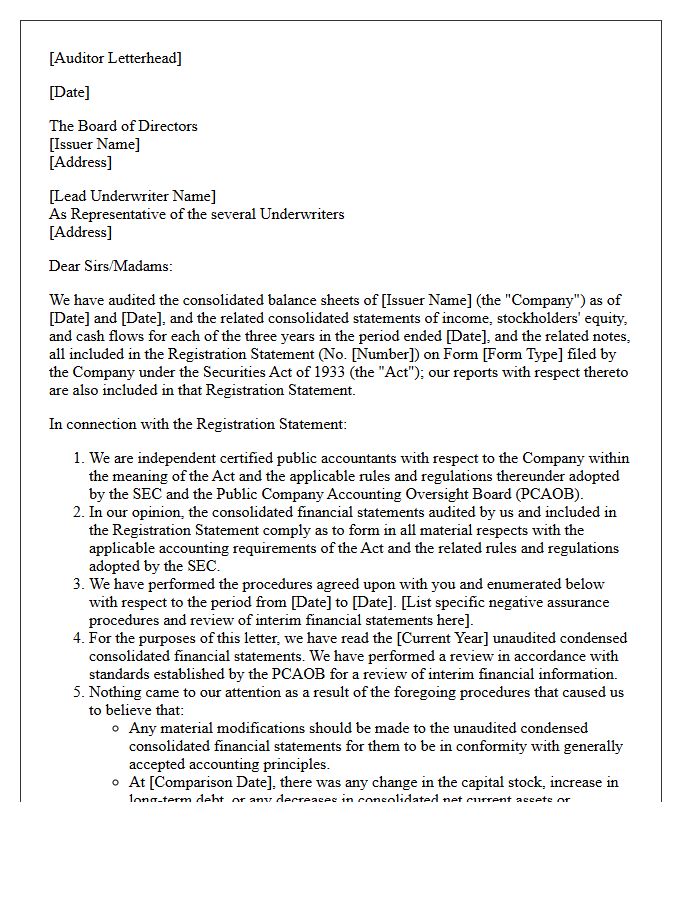

Initial Public Offering Auditor Comfort Letter

An Initial Public Offering (IPO) Auditor Comfort Letter is a critical document issued by accounting firms to underwriters to provide negative assurance regarding financial data. It minimizes legal liability by confirming that financial statements comply with SEC regulations and have undergone specific due diligence procedures. This letter bridges the gap between the last formal audit and the effective date of the prospectus, ensuring the accuracy of non-audited figures. It serves as a vital safeguard for investment banks during the capital markets transition, validating the integrity of a company's financial reporting before going public.

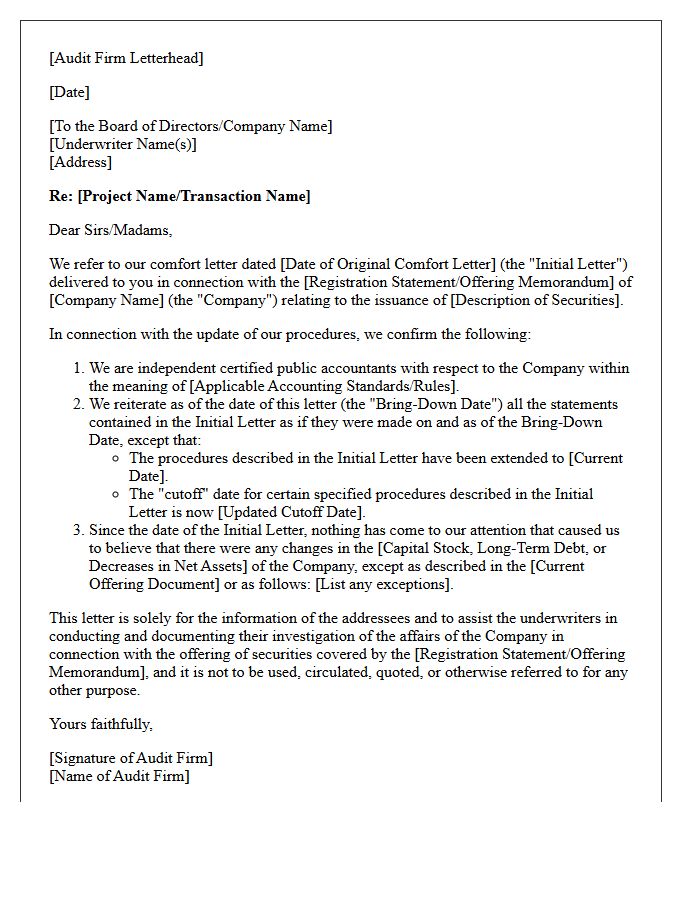

Bring-Down Auditor Comfort Letter

A Bring-Down Auditor Comfort Letter is a critical financial document issued by independent accountants during a securities offering. It serves as a reaffirmation of the initial comfort letter, confirming that no material adverse changes have occurred in the company's financial position between the effective date and the closing date. By performing "bring-down" procedures, auditors provide underwriters with essential due diligence protection. This process ensures that financial data remains accurate and reliable up until the final transaction, mitigating risk for all parties involved in the capital markets process.

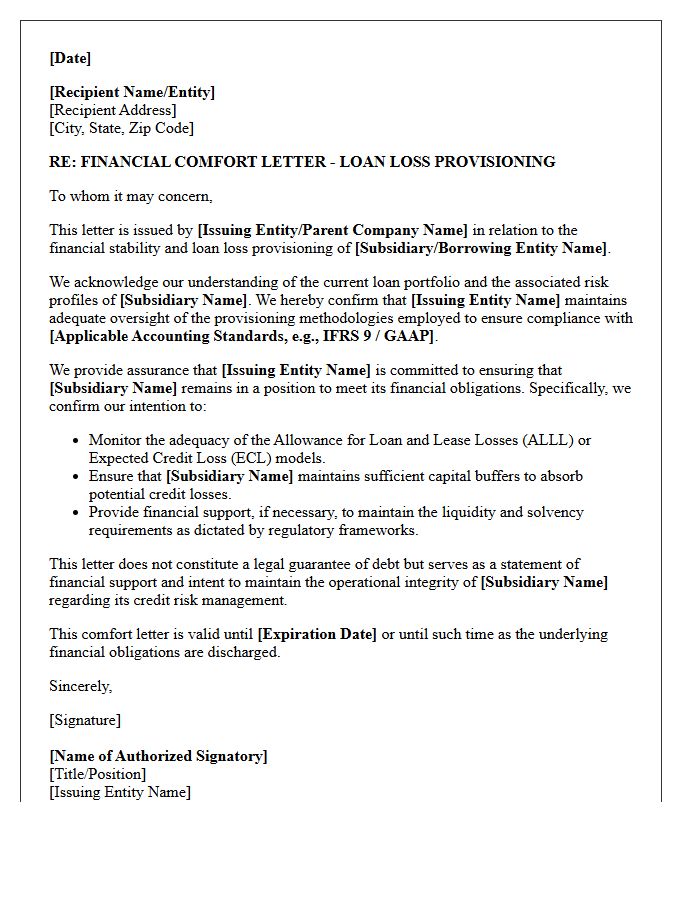

Loan Loss Provisioning Financial Comfort Letter

A Loan Loss Provisioning Financial Comfort Letter is a critical document used to assure stakeholders of a bank's capital adequacy. It confirms that the institution has allocated sufficient allowance for credit losses to cover potential defaults. This risk management tool demonstrates financial transparency by aligning reported earnings with actual asset quality. Auditors and regulators rely on these letters to verify that reserves are calculated using expected credit loss models, ensuring the bank maintains long-term solvency and stability during economic downturns or periods of heightened financial stress.

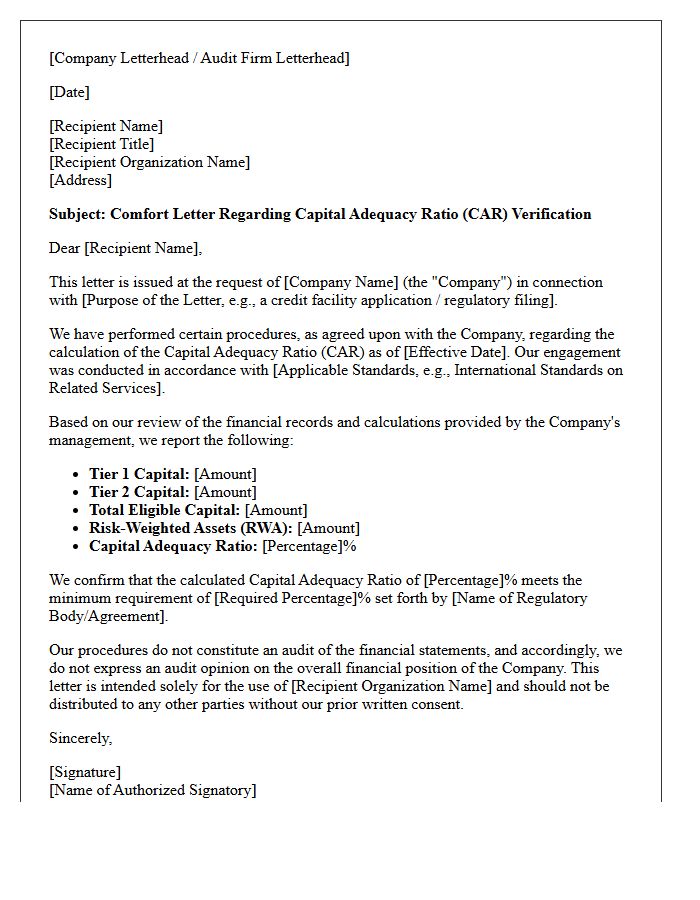

Capital Adequacy Ratio Verification Comfort Letter

A Capital Adequacy Ratio Verification Comfort Letter is a formal document issued by external auditors to provide assurance regarding a financial institution's solvency. It confirms that the entity maintains sufficient regulatory capital to support its risk-weighted assets, adhering to Basel III standards. This letter is crucial during securities offerings or mergers, offering stakeholders independent validation of financial stability. It minimizes investment risk by verifying that the reported capital ratios are accurate, consistent with accounting records, and compliant with specific banking regulations and jurisdictional requirements.

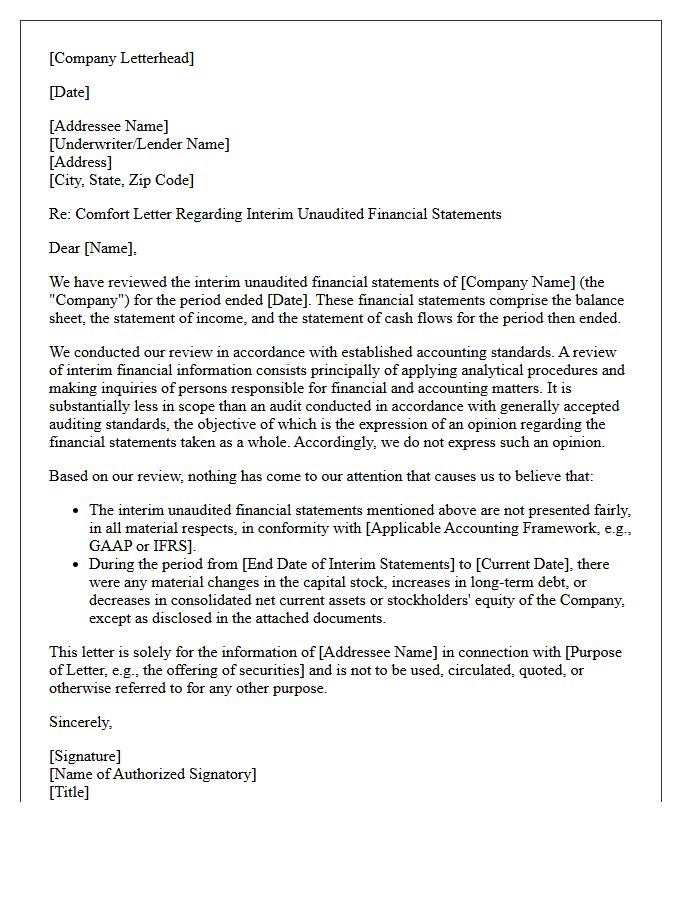

Interim Unaudited Financial Statement Comfort Letter

An Interim Unaudited Financial Statement Comfort Letter is a critical document issued by independent auditors to underwriters during securities offerings. It provides negative assurance, confirming that no material modifications are required for the interim data to align with accounting standards. Although these statements are not fully audited, the letter mitigates financial risk by verifying that the figures are consistent with the company's audited records. This process is essential for maintaining due diligence standards, protecting stakeholders, and ensuring the overall integrity of financial disclosures in volatile capital markets.

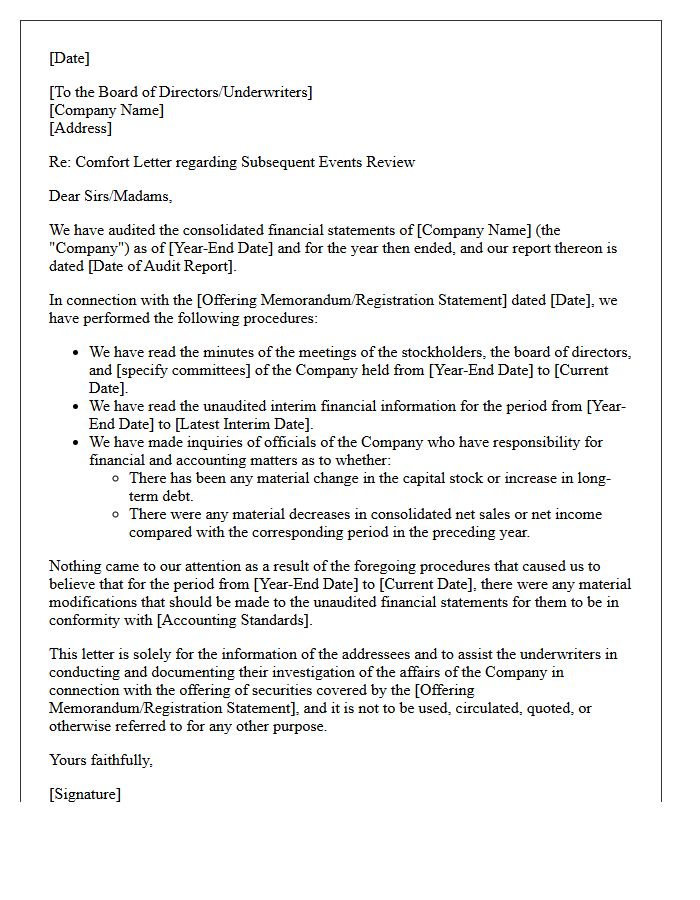

Subsequent Events Review Comfort Letter

A Subsequent Events Review is a critical procedure performed by auditors to identify material transactions occurring between the balance sheet date and the issuance of a Comfort Letter. This review ensures that underwriters receive assurance regarding any significant changes in the entity's financial position. Auditors typically perform inquiries and examine minutes to confirm that the registration statement remains accurate. Understanding these post-balance sheet developments is essential for managing risk and ensuring financial transparency during securities offerings, protecting both issuers and investors from undisclosed liabilities or performance shifts.

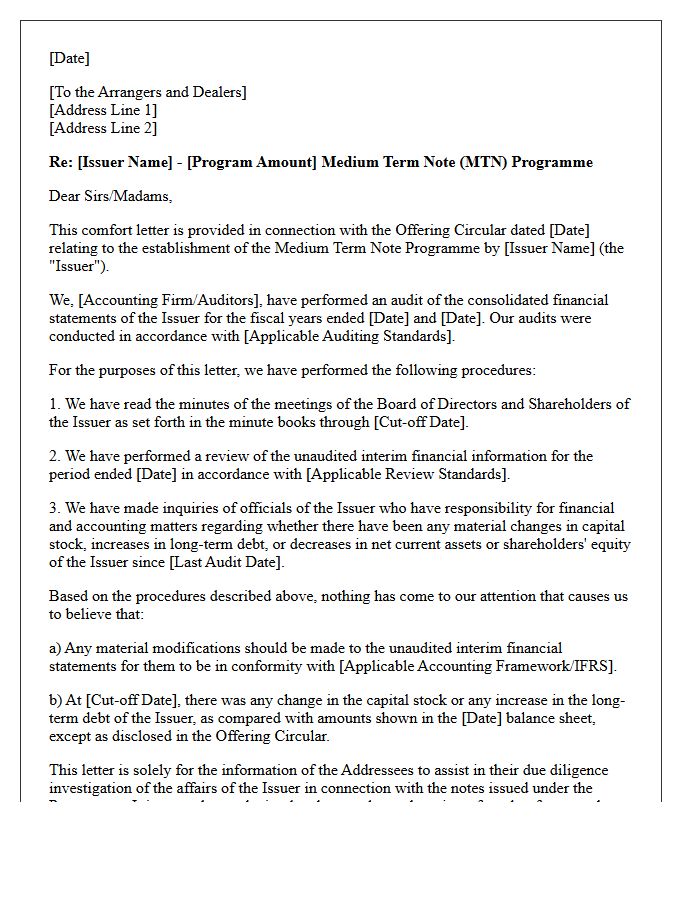

Medium Term Note Debt Issuance Comfort Letter

A Medium Term Note (MTN) Debt Issuance Comfort Letter is a critical document provided by auditors to underwriters during a securities offering. It provides negative assurance regarding the issuer's financial health and ensures that financial statements comply with accounting standards. This letter mitigates risk for dealers by validating that no material adverse changes have occurred since the last audit. By performing due diligence through this process, financial institutions confirm the accuracy of the offering memorandum, thereby protecting investors and ensuring legal compliance within the debt capital markets.

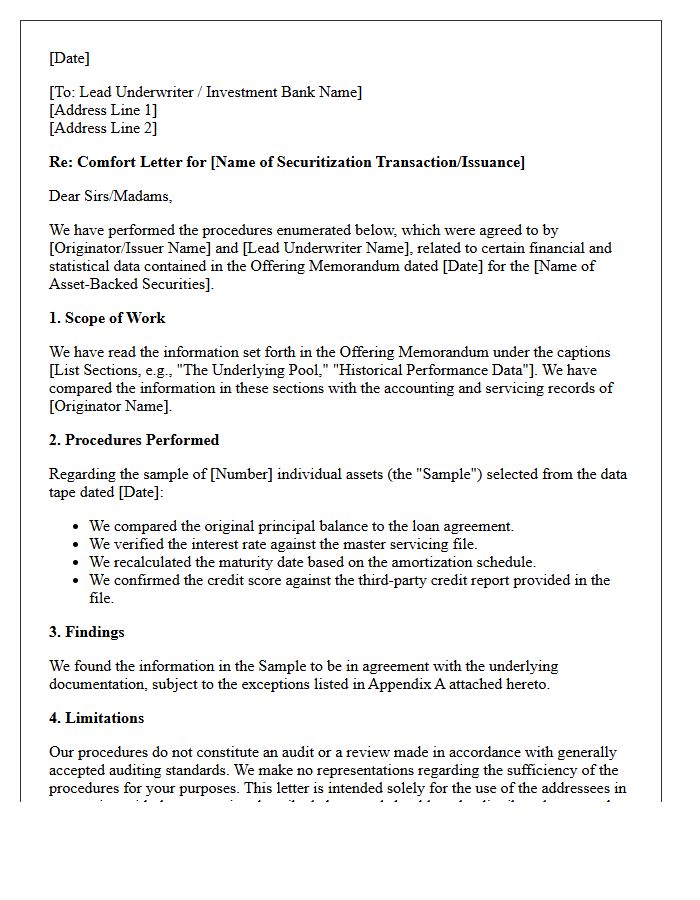

Asset-Backed Securitization Comfort Letter

An asset-backed securitization comfort letter is a critical document issued by independent auditors to provide assurance regarding the accuracy of financial data. It verifies that the underlying pool of assets matches the characteristics described in the offering memorandum. By performing specific agreed-upon procedures, auditors help mitigate risk for underwriters and investors. This document serves as a vital component of due diligence, ensuring transparency in the valuation and historical performance of the securitized loans or receivables before the securities are issued to the public market.

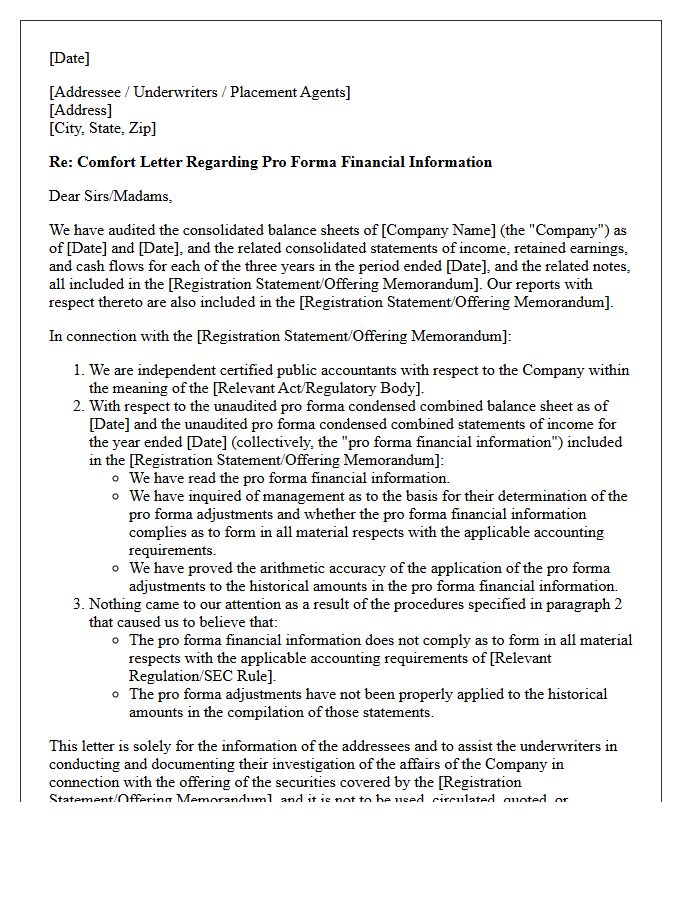

Pro Forma Financial Information Comfort Letter

A Pro Forma Financial Information Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It provides negative assurance that pro forma adjustments comply with specific accounting regulations, such as SEC Regulation S-X. This letter verifies that financial statements accurately reflect the hypothetical impact of significant events, like mergers or acquisitions, on historical data. By validating the methodology and calculations used, auditors help mitigate financial risk and enhance investor confidence in the projected fiscal health of the reporting entity during complex capital market transactions.

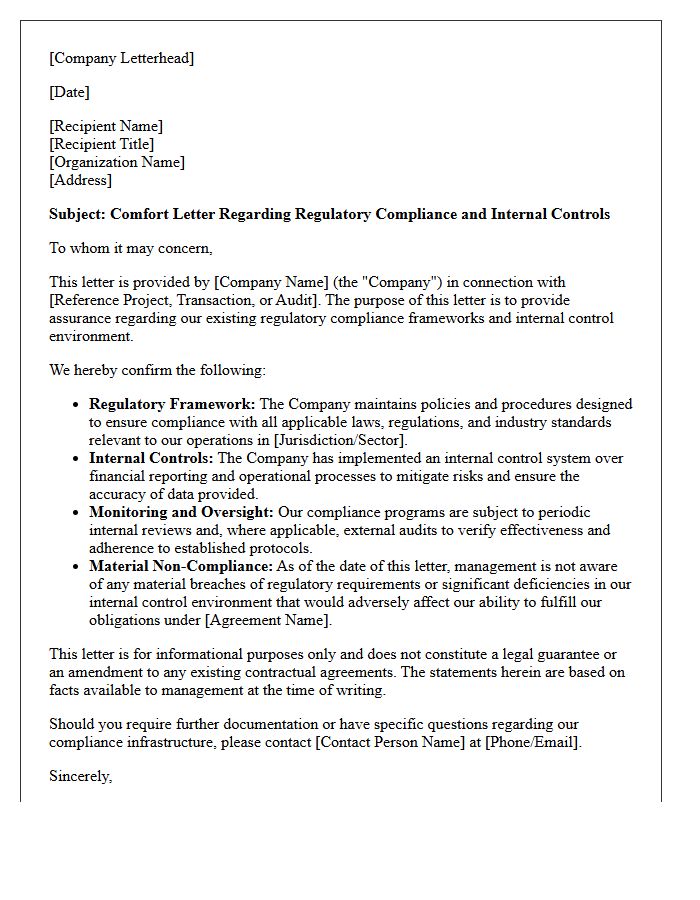

Regulatory Compliance and Controls Comfort Letter

A Regulatory Compliance and Controls Comfort Letter is a formal document issued by independent auditors to provide assurance regarding a company's adherence to specific legal frameworks and internal protocols. It is essential during financial transactions or audits to verify that internal controls are operating effectively. This letter mitigates risk for third parties by confirming that the entity follows mandatory regulatory standards, ensuring transparency and accountability. Understanding the scope of this letter is vital for stakeholders to evaluate risk management and legal standing in highly regulated industries.

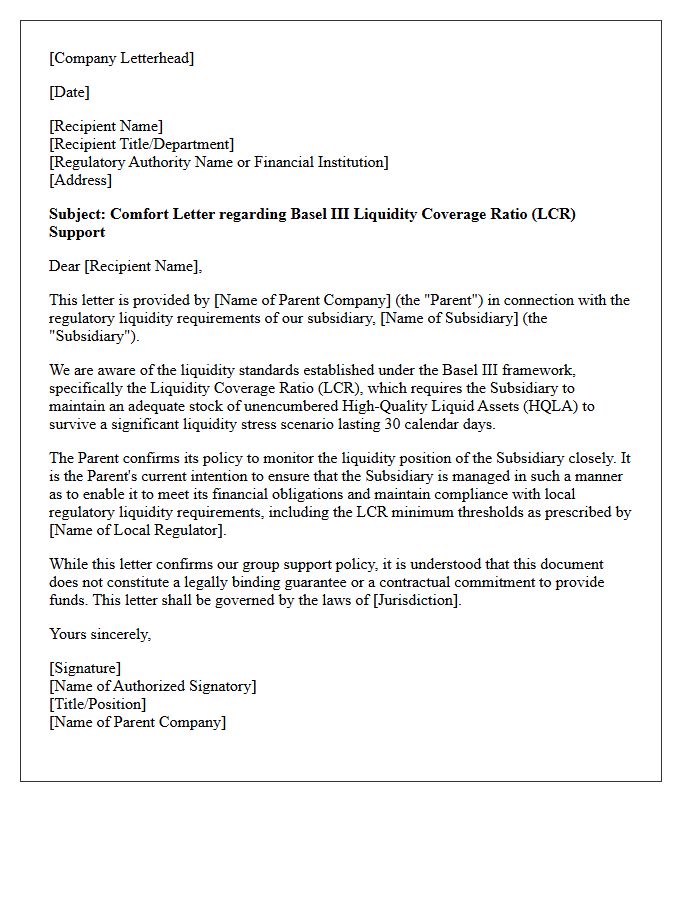

Basel Liquidity Coverage Ratio Comfort Letter

A Basel Liquidity Coverage Ratio (LCR) Comfort Letter is a formal document issued by a parent financial institution to a subsidiary or regulator. It provides conditional assurance that the parent company will maintain sufficient high-quality liquid assets to meet the subsidiary's short-term obligations during stress periods. While not a legally binding guarantee, it serves as a critical risk management tool to demonstrate group-wide compliance with Basel III standards, ensuring the entity remains solvent and meets regulatory liquidity benchmarks during financial volatility.

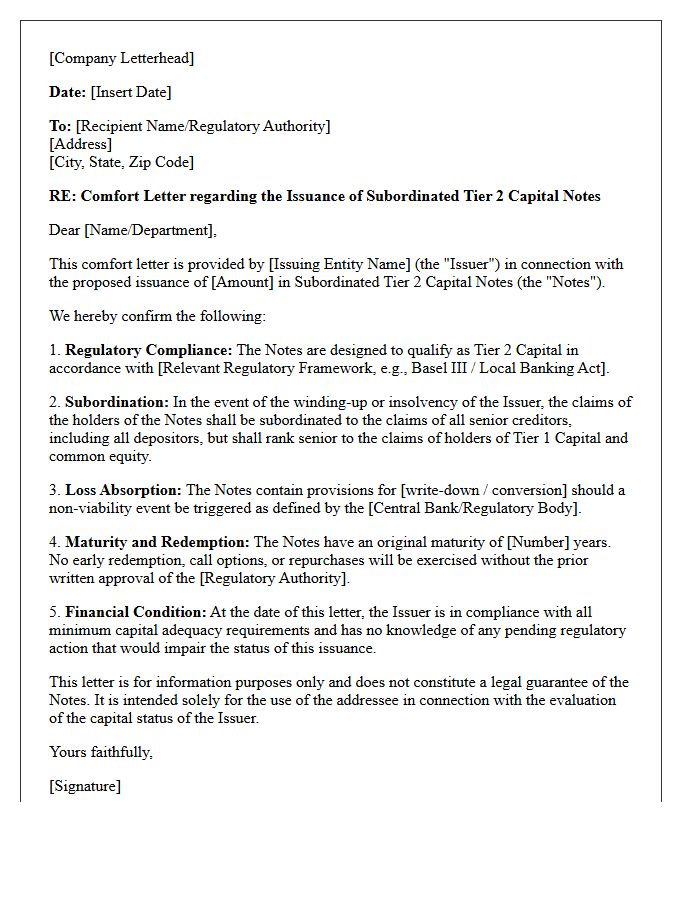

Subordinated Tier Two Capital Issuance Comfort Letter

A Subordinated Tier Two Capital Issuance Comfort Letter is a regulatory document issued by a parent bank to confirm its awareness of a subsidiary's debt issuance. It serves as an attestation that the instrument complies with Basel III standards for supplemental capital. While not a formal guarantee, it provides reassurance to regulators and investors that the issuance meets strict structural subordination and loss-absorbency requirements. This letter is crucial for ensuring the debt qualifies as Tier 2 capital, strengthening the financial institution's overall solvency ratio and meeting mandatory capital adequacy thresholds.

What is an Auditor Comfort Letter in an underwriting agreement?

An Auditor Comfort Letter is a document issued by an independent public accountant to underwriters during a securities offering. It provides negative assurance that the financial data in the registration statement, which is not covered by the formal audit report, complies with accounting standards and has undergone specific agreed-upon procedures.

Why do underwriters require a Comfort Letter during a public offering?

Underwriters require a Comfort Letter to establish a "due diligence" defense under Section 11 of the Securities Act of 1933. It serves as evidence that the underwriters performed a reasonable investigation into the accuracy of the financial information presented in the prospectus, thereby reducing their legal liability.

What are "Agreed-Upon Procedures" in the context of a Comfort Letter?

Agreed-Upon Procedures (AUP) are specific tests and reviews performed by the auditor at the request of the underwriters. These typically include comparing financial figures in the offering document to the company's accounting records, checking mathematical accuracy, and reviewing changes in financial statement line items since the last audited period.

What is the difference between positive and negative assurance in a Comfort Letter?

Positive assurance is provided for audited financial statements, stating they present fairly in all material respects. Negative assurance, which is the core of a Comfort Letter, states that "nothing came to the auditor's attention" during their review that would indicate the unaudited financial data or subsequent changes do not comply with applicable requirements.

When are the "bring-down" comfort letters typically delivered?

A "bring-down" comfort letter is typically delivered at the closing of the underwriting deal, usually a few days after the initial letter issued at the pricing date. It confirms that no material financial changes have occurred between the effective date of the registration statement and the final closing date of the offering.

Comments