A Comfort Letter is a vital document issued by auditors to underwriters during corporate bond issuances. It provides assurance regarding the accuracy of financial data and confirms that no significant changes have occurred since the last audit. This ensures transparency and builds investor confidence throughout the debt offering process. To assist your documentation, below are some ready to use template.

Image cover: Comprehensive Guide to Corporate Bond Comfort Letter Samples and Professional Templates

Letter Samples List

- Draft Comfort Letter For Underwriters

- Independent Auditors Comfort Letter

- Pricing Date Comfort Letter

- Negative Assurance Comfort Letter

- Financial Statement Comfort Letter

- Subsequent Events Comfort Letter

- Bring-Down Comfort Letter

- Closing Date Comfort Letter

- Pro Forma Financials Comfort Letter

- Capital Adequacy Comfort Letter

- Underwriters Reliance Comfort Letter

- Legal Compliance Comfort Letter

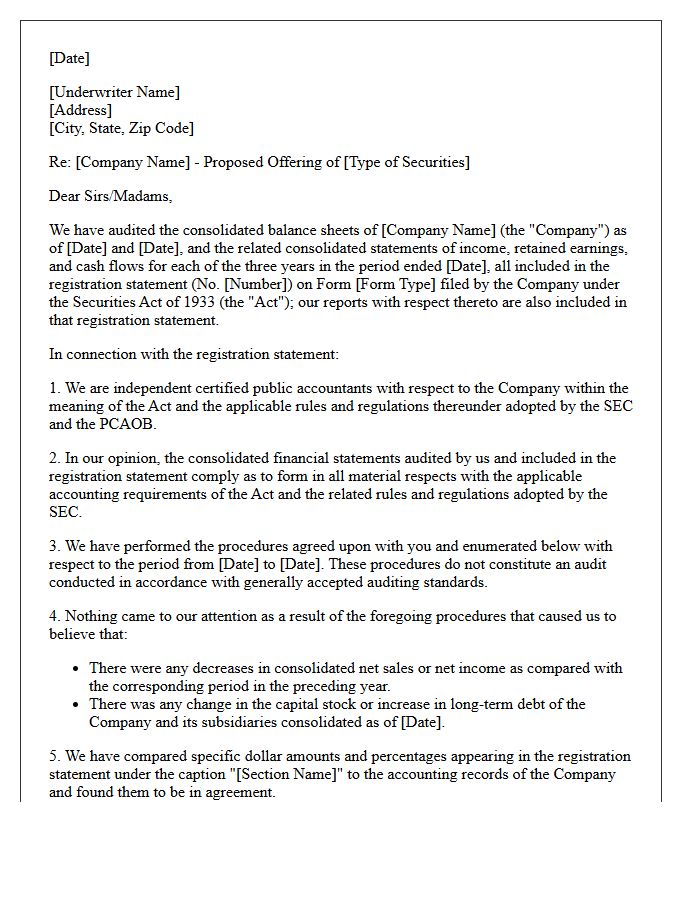

Draft Comfort Letter For Underwriters

A draft comfort letter is a critical financial due diligence document issued by independent auditors to underwriters during a securities offering. It provides negative assurance that the issuer's unaudited financial data complies with accounting standards and has not materially changed since the last audit. This document mitigates underwriter liability by demonstrating "due diligence" under the Securities Act. Negotiating the scope early is vital, as it confirms the accuracy of financial figures in the prospectus, ensuring investor protection and regulatory compliance before the final transaction closes.

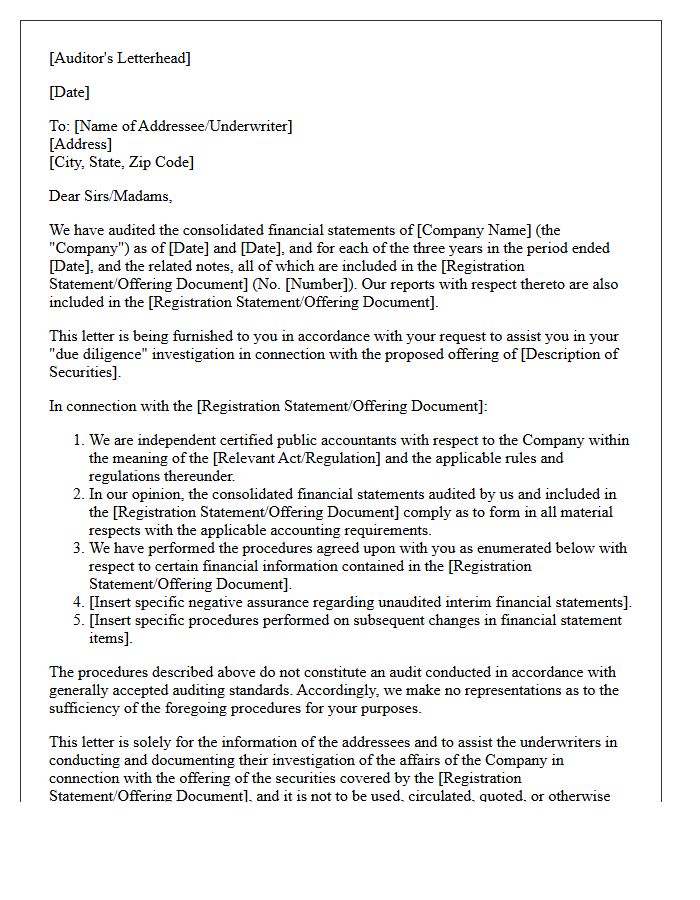

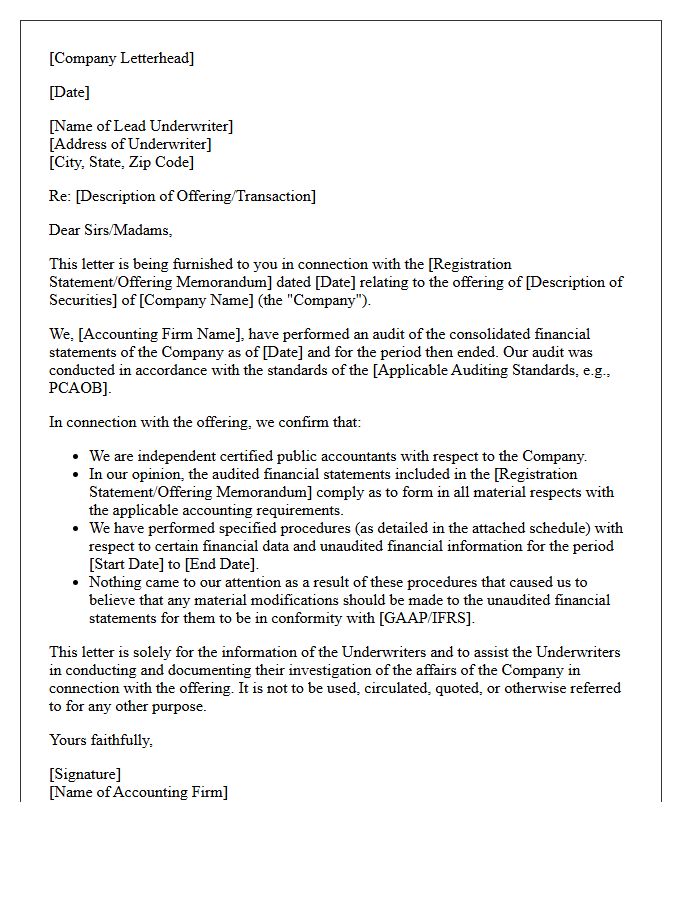

Independent Auditors Comfort Letter

An Independent Auditor's Comfort Letter is a vital document issued during securities offerings to provide assurance to underwriters. It verifies that financial data not covered by audited statements remains consistent with accounting records. This letter helps underwriters establish a due diligence defense by confirming that no material adverse changes occurred since the last audit. Typically, it includes negative assurance on unaudited interim figures and compliance with SEC regulations. Understanding its scope is essential for mitigating financial risk and ensuring regulatory transparency during capital market transactions.

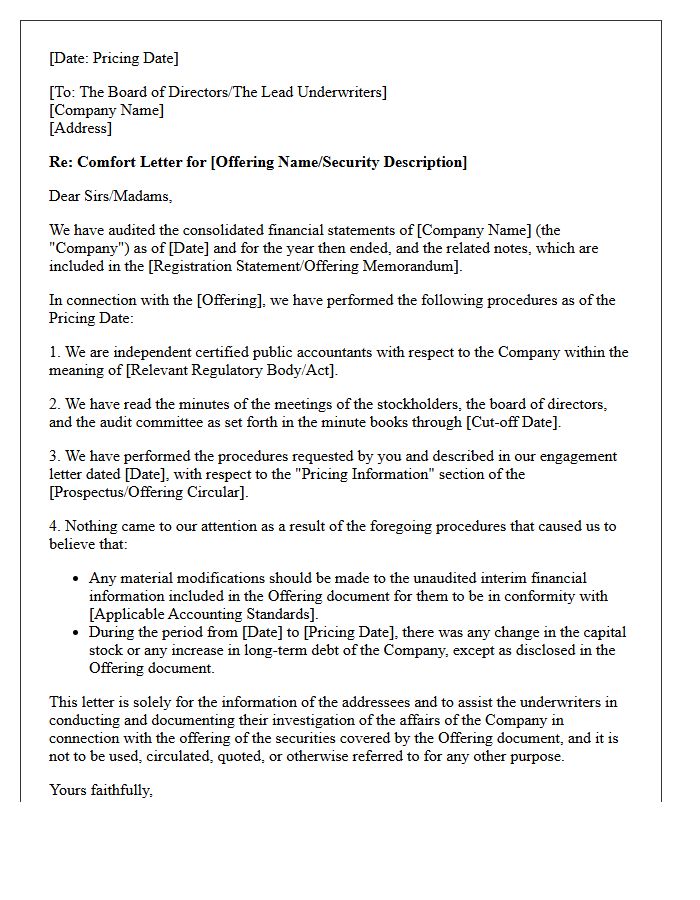

Pricing Date Comfort Letter

A Pricing Date Comfort Letter is a critical financial document issued by independent auditors to underwriters during a securities offering. It provides negative assurance that no material adverse changes have occurred in the issuer's financial position between the last audit and the specific pricing date. This letter verifies the accuracy of financial data within the prospectus, helping underwriters satisfy their due diligence requirements. By confirming that financial figures remain consistent and reliable, it mitigates legal risks and ensures transparency for investors before the final transaction terms are officially set.

Negative Assurance Comfort Letter

A Negative Assurance Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It provides limited assurance that, based on specific procedures, no material facts were discovered suggesting financial statements are misleading. Unlike a full audit, it does not offer a positive opinion. Instead, it confirms that nothing came to the auditors' attention to contradict the financial integrity of the registration statement. This serves as a vital component of the underwriters' due diligence process, helping mitigate legal liability under securities regulations by verifying unaudited financial data.

Financial Statement Comfort Letter

A financial statement comfort letter is a document issued by an independent auditor to underwriters during a securities offering. It provides negative assurance that no material changes have occurred in the company's financial position since the last audit. This letter helps underwriters establish due diligence and reduces legal liability by verifying that financial data in the prospectus aligns with audited records. It is a critical component for ensuring transparency and maintaining investor confidence during capital market transactions.

Subsequent Events Comfort Letter

A Subsequent Events Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It provides negative assurance that no material adverse changes have occurred in a company's financial position since the last audit. This letter helps underwriters establish a due diligence defense under securities laws by verifying that the prospectus remains accurate up to the closing date. It bridges the information gap between the historical financial statements and the effective date of the offering, ensuring investor protection through rigorous financial verification.

Bring-Down Comfort Letter

A Bring-Down Comfort Letter is a critical financial document issued by auditors to underwriters during a securities offering. It serves to verify that no significant negative changes have occurred in a company's financial position since the issuance of the initial comfort letter. This process is essential for establishing due diligence and protecting parties from liability under securities laws. By confirming continued financial accuracy up to the closing date, the letter provides necessary assurance to investors and lenders involved in the transaction.

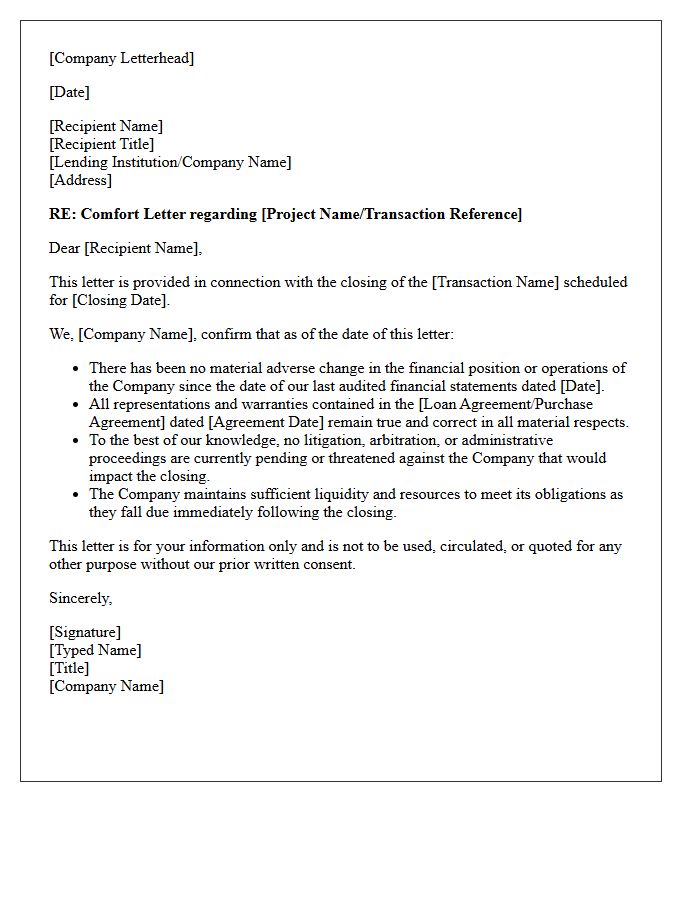

Closing Date Comfort Letter

A Closing Date Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It provides negative assurance that no material financial changes occurred between the last audit and the transaction date. This letter verifies that financial data in the prospectus remains accurate up to the final closing. By confirming financial consistency and performing "subsequent events" reviews, it mitigates risk for investors and fulfills due diligence requirements. It ensures all parties that the issuer's financial position has not significantly deteriorated before the deal officially concludes.

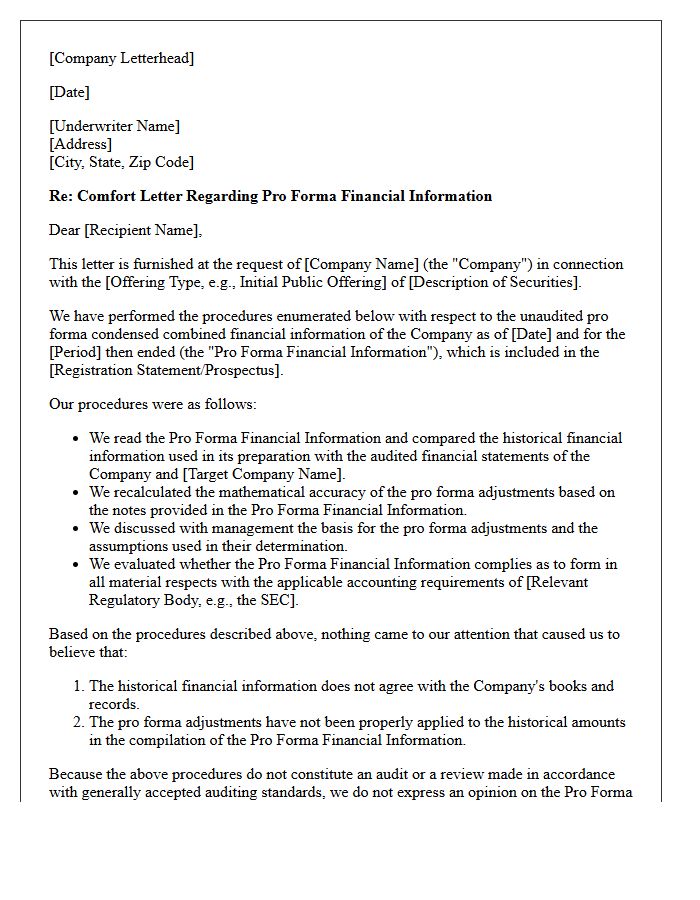

Pro Forma Financials Comfort Letter

A Pro Forma Financials Comfort Letter is a critical document issued by independent auditors to underwriters during securities offerings. It provides negative assurance that pro forma financial information complies with applicable accounting regulations and reflects adjustments based on reasonable assumptions. This letter helps underwriters fulfill their due diligence obligations by verifying that hypothetical financial scenarios are prepared consistently with historical data. Essentially, it serves as a professional validation layer, ensuring that adjusted financial projections presented to potential investors are structurally sound and mathematically accurate under AICPA standards.

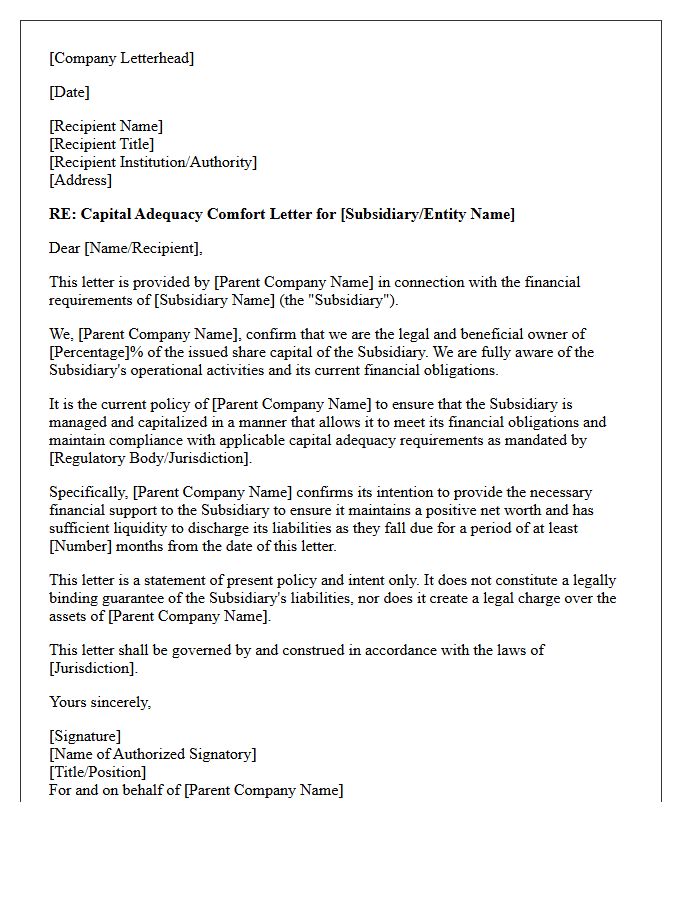

Capital Adequacy Comfort Letter

A Capital Adequacy Comfort Letter is a formal document issued by a parent company or financial institution to assure stakeholders of a subsidiary's financial stability. It confirms that the entity maintains sufficient capital to meet its regulatory requirements and operational obligations. While often not legally binding, it serves as a critical credit enhancement tool, boosting investor confidence and facilitating smoother auditing processes. This letter demonstrates a commitment to financial solvency, ensuring the subsidiary can absorb potential losses without risking systemic failure or breaching essential capital thresholds within the banking and investment sectors.

Underwriters Reliance Comfort Letter

An Underwriters Reliance Comfort Letter, typically issued by auditors under standards like AS 6101, provides negative assurance regarding a company's financial health during an offering. It helps underwriters establish a due diligence defense by verifying that no material adverse changes occurred since the last audited statement. This document bridges the gap between audited data and the effective date of a securities offering, ensuring financial disclosures remain accurate and reducing legal liability for all parties involved in the capital raising process.

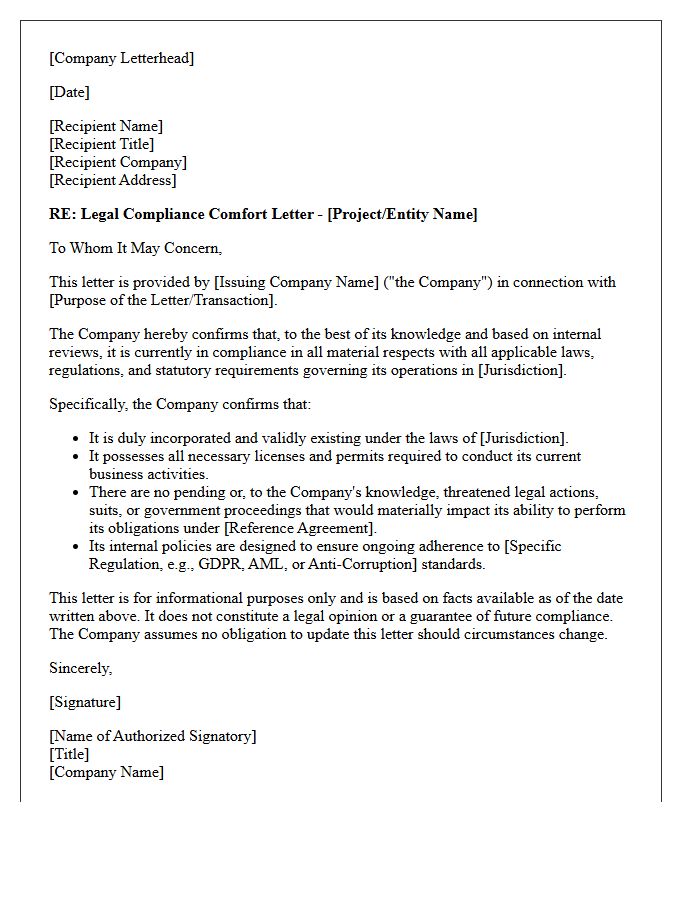

Legal Compliance Comfort Letter

A Legal Compliance Comfort Letter is a formal document issued by legal counsel or auditors to provide assurance regarding a company's adherence to specific regulations or contractual obligations. It is typically required during due diligence for mergers, acquisitions, or securities offerings to mitigate financial risk. While not a definitive legal guarantee, it confirms that no material non-compliance was discovered during review. This letter enhances investor confidence by verifying that the entity operates within the regulatory framework, ensuring transparency and reducing the likelihood of future litigation or penalties.

What is a comfort letter in corporate bond issuances?

A comfort letter is a document issued by an independent auditor to the underwriters of a corporate bond offering, providing negative assurance that the financial statements are prepared in accordance with accounting standards and that no material adverse changes have occurred since the last audit.

Why do underwriters require a comfort letter for bond offerings?

Underwriters require a comfort letter as part of their "due diligence" defense under securities laws. It helps verify the accuracy of the financial data included in the offering prospectus and reduces the underwriters' legal liability regarding potential financial misstatements.

What are the typical contents of a comfort letter?

A typical comfort letter includes statements on the auditor's independence, the compliance of the financial statements with SEC requirements, and negative assurance on unaudited interim financial data and subsequent changes in specific financial statement items.

What is the difference between positive and negative assurance in a comfort letter?

Positive assurance is a definitive statement that financial statements are fairly presented, usually found in audit reports. Negative assurance, standard in comfort letters, states that "nothing has come to the auditor's attention" that indicates the financial data is incorrect or non-compliant.

When is a comfort letter officially issued during the bond issuance process?

A comfort letter is typically issued twice: first on the "pricing date" (when the final terms of the bond are set) and again on the "closing date" (the bring-down letter) to confirm that no material financial changes occurred between pricing and the delivery of funds.

Comments