A Comfort Letter is a critical document issued by auditors to underwriters during an Initial Public Offering. It provides financial assurance, verifying that the unaudited data in the prospectus aligns with accounting standards to mitigate liability risks. This process ensures transparency and builds investor confidence during the transition to a public entity. To assist your filing, below are some ready to use template.

Image cover: Mastering Comfort Letters: Professional Samples and Templates for IPO Success

Letter Samples List

- Standard Auditor Comfort Letter for Banking Initial Public Offerings

- Bring-Down Comfort Letter for Underwriters in Bank Offerings

- Negative Assurance Comfort Letter on Bank Financial Statements

- Independent Accountant Comfort Letter on Loan Portfolio Quality

- Statutory Auditor Comfort Letter on Capital Adequacy Ratios

- Legal Counsel Comfort Letter on Banking Regulatory Compliance

- Financial Advisor Comfort Letter on Pro Forma Banking Metrics

- Certified Public Accountant Comfort Letter on Deposit Liabilities

- Executive Management Representation Letter for Initial Public Offerings

- Subsequent Events Comfort Letter for Banking Institutions

- Internal Audit Comfort Letter on Financial Reporting Controls

- Risk Management Comfort Letter on Asset Quality Provisions

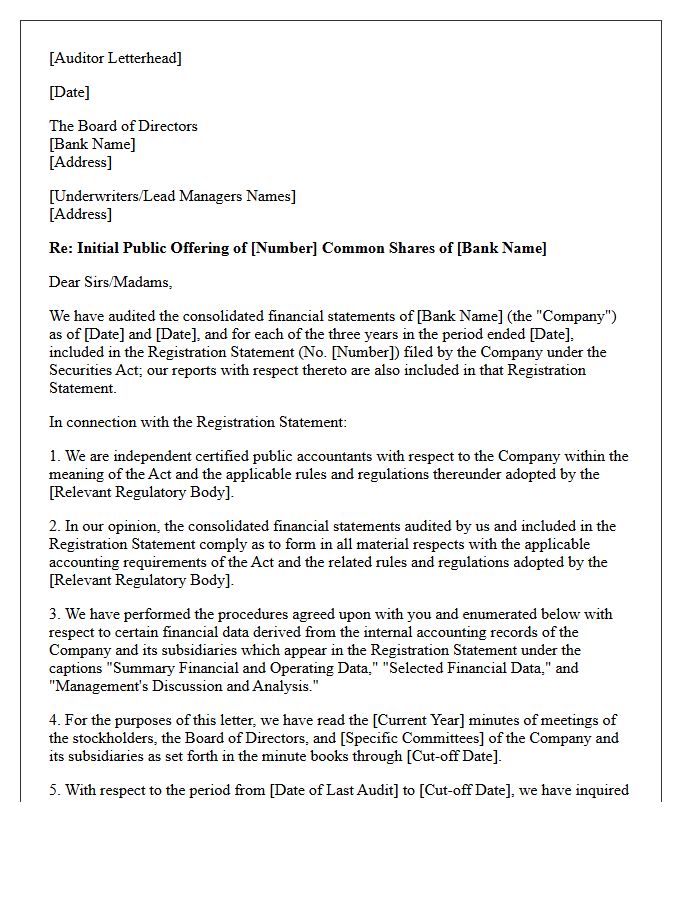

Standard Auditor Comfort Letter for Banking Initial Public Offerings

A standard auditor comfort letter is a critical document provided by accountants to underwriters during a banking IPO. It ensures financial due diligence by verifying that unaudited financial data aligns with audited records. This letter mitigates underwriter liability under securities laws by confirming "negative assurance" on interim changes. It bridges the gap between the last audit and the effective date of the offering, providing essential comfort that the financial statements remain accurate and consistent, thereby protecting stakeholders involved in the capital markets transition.

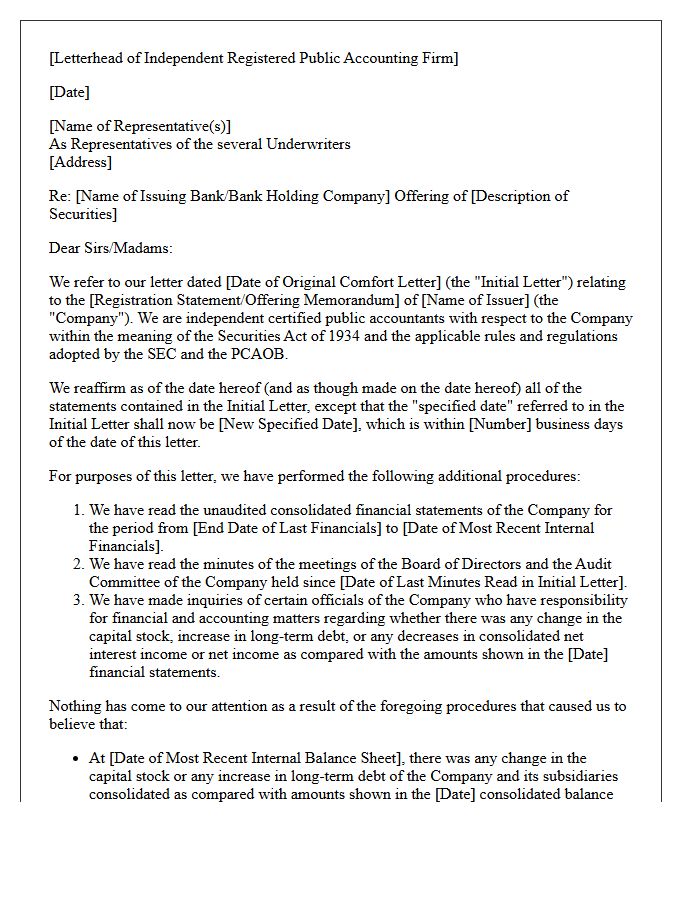

Bring-Down Comfort Letter for Underwriters in Bank Offerings

A Bring-Down Comfort Letter is a vital closing document issued by independent auditors to underwriters during bank offerings. It serves to reconfirm the financial data previously reported, ensuring no material adverse changes have occurred since the initial comfort letter. This process mitigates underwriter liability by providing due diligence evidence regarding the issuer's financial health. By verifying that financial statements remain accurate up to the effective date, it protects parties against undisclosed risks and maintains the integrity of the capital markets transaction during the final stages of the offering.

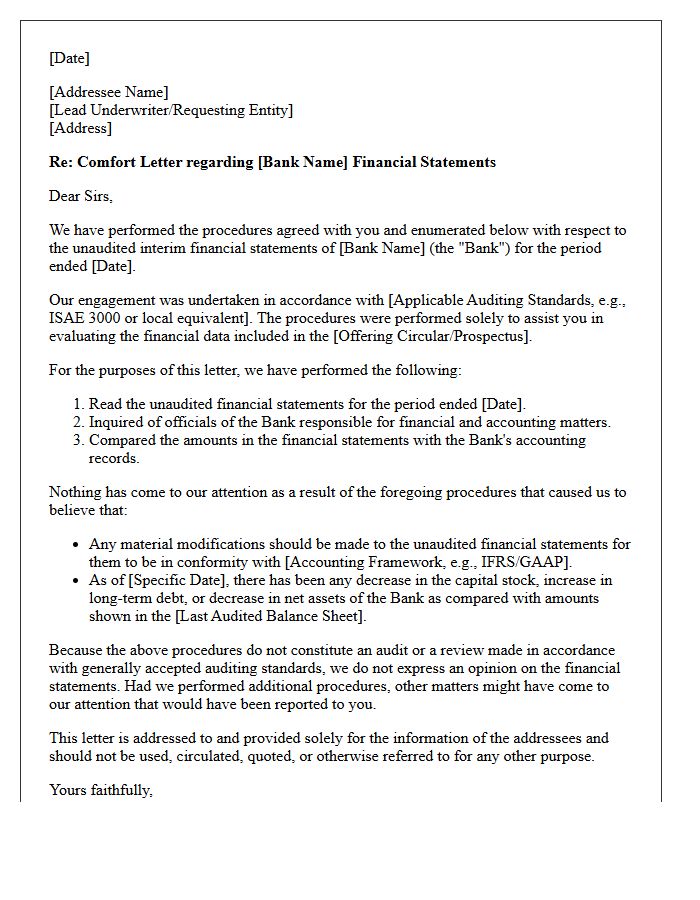

Negative Assurance Comfort Letter on Bank Financial Statements

A Negative Assurance Comfort Letter provides a statement by independent auditors that no material modifications are required for financial statements to conform with reporting standards. Unlike an audit, it does not provide an absolute opinion but confirms that nothing came to the auditors' attention indicating errors. In banking, these letters are essential during securities offerings to reduce underwriter liability and provide due diligence. They ensure that unaudited financial data and subsequent changes remain consistent with previously audited figures, offering critical, though limited, financial reliability to institutional investors and regulators.

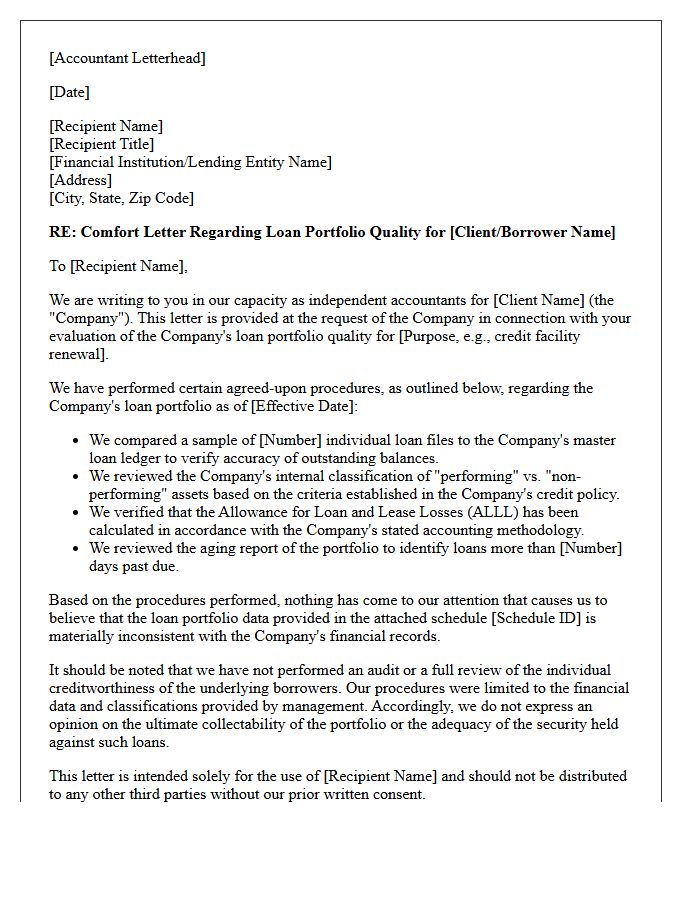

Independent Accountant Comfort Letter on Loan Portfolio Quality

An Independent Accountant Comfort Letter provides institutional lenders with negative assurance regarding a loan portfolio quality. During capital market transactions, auditors perform agreed-upon procedures to verify data integrity and risk metrics. This document mitigates financial risk by validating that the underlying assets meet specific underwriting standards and regulatory criteria. It serves as a critical tool for due diligence, ensuring transparency and enhancing investor confidence in the accuracy of reported financial disclosures. Ultimately, the letter confirms that the portfolio's performance data is consistent with audited financial statements and internal controls.

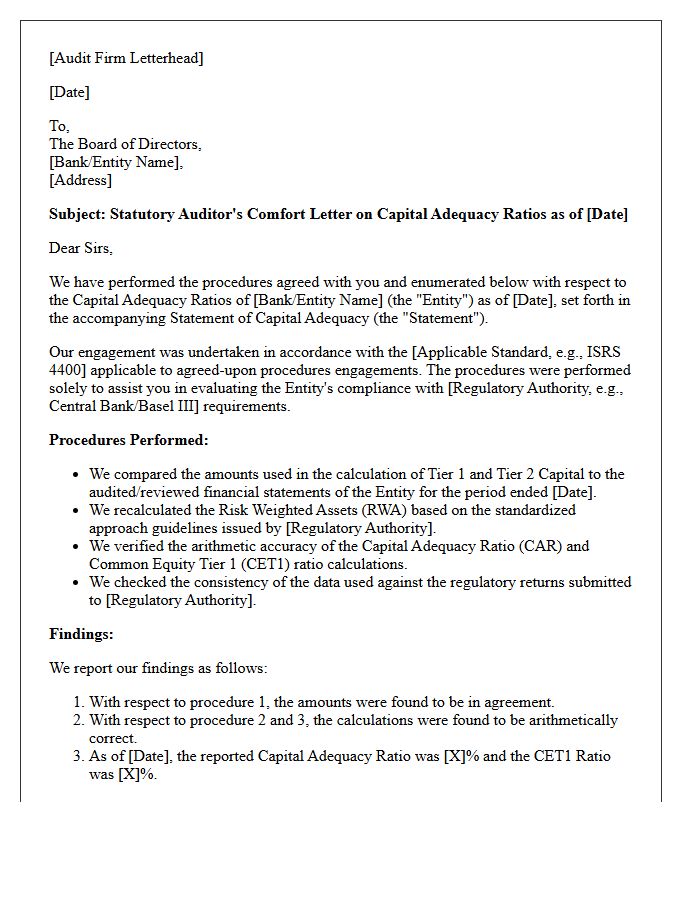

Statutory Auditor Comfort Letter on Capital Adequacy Ratios

A statutory auditor comfort letter on capital adequacy ratios provides independent assurance regarding a financial institution's regulatory compliance. It confirms that calculations for Common Equity Tier 1 (CET1) and total capital meet specific Basel III or national standards. This document is crucial for investors and regulators during capital raises, verifying that the reported figures are mathematically accurate and derived from audited financial statements. By validating these risk-weighted assets and solvency levels, auditors mitigate risk for stakeholders, ensuring the entity maintains a sufficient capital buffer to absorb potential operational losses.

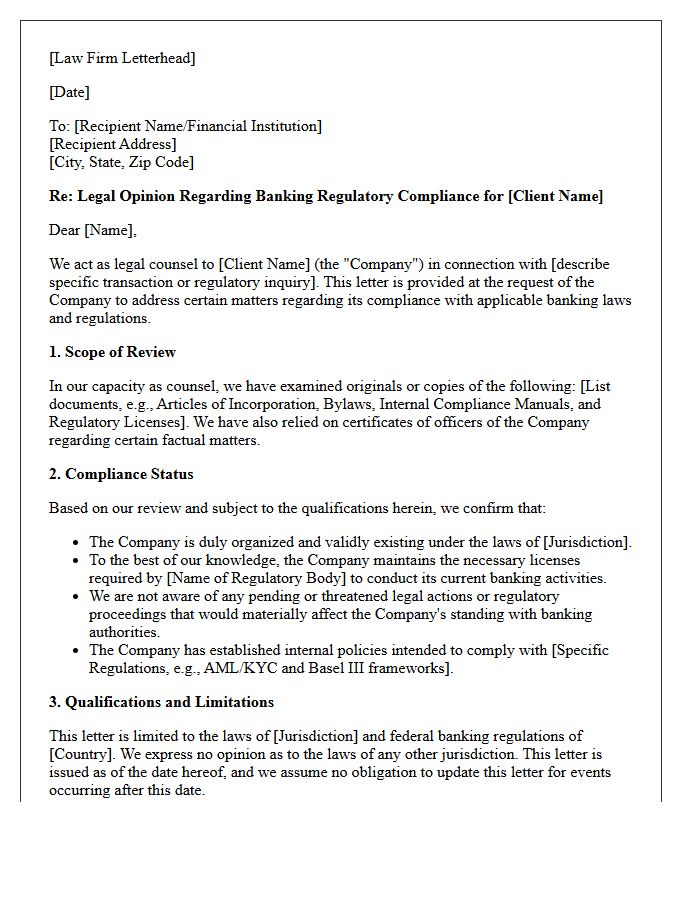

Legal Counsel Comfort Letter on Banking Regulatory Compliance

A Legal Counsel Comfort Letter serves as a formal assurance provided by an attorney to financial institutions or investors. It confirms that a client's internal operations and transactions align with complex banking regulatory compliance frameworks. While not a legal guarantee, it mitigates risk by verifying adherence to statutes like AML, KYC, and capital adequacy requirements. This document is essential during audits or high-stakes deals, as it builds institutional trust by certifying that the entity is operating within the necessary legal boundaries of the financial sector.

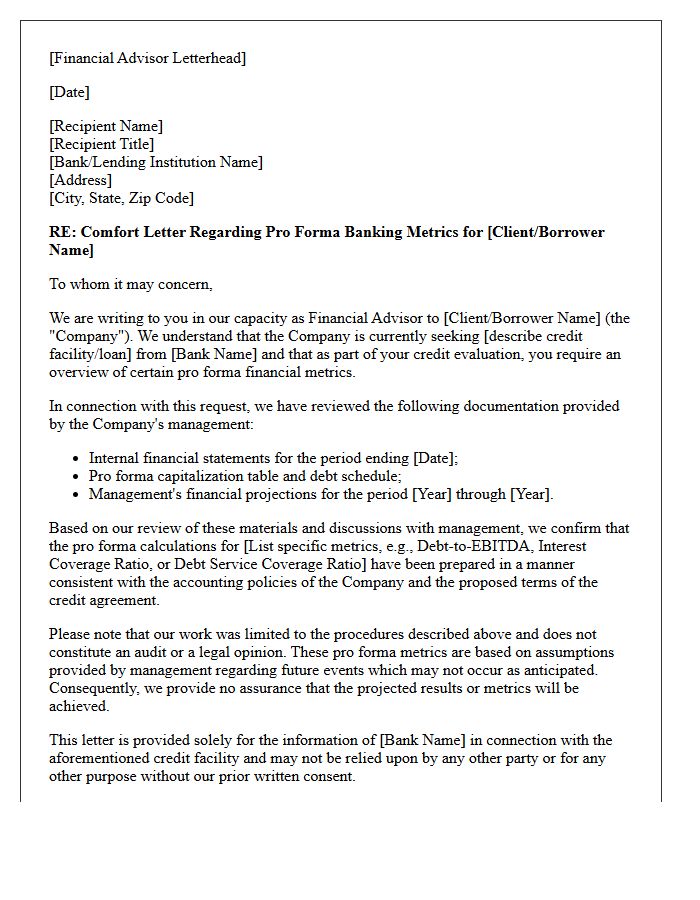

Financial Advisor Comfort Letter on Pro Forma Banking Metrics

A financial advisor comfort letter provides a level of assurance to lenders regarding a borrower's pro forma banking metrics. This document verifies that projected financial statements, following an acquisition or restructuring, are prepared based on reasonable assumptions and accurate calculations. While not an audit, it validates the methodology used to derive key leverage and interest coverage ratios. For institutions, these letters are essential for risk assessment and ensuring compliance with debt covenants during the loan underwriting process, bridging the gap between historical performance and future financial obligations.

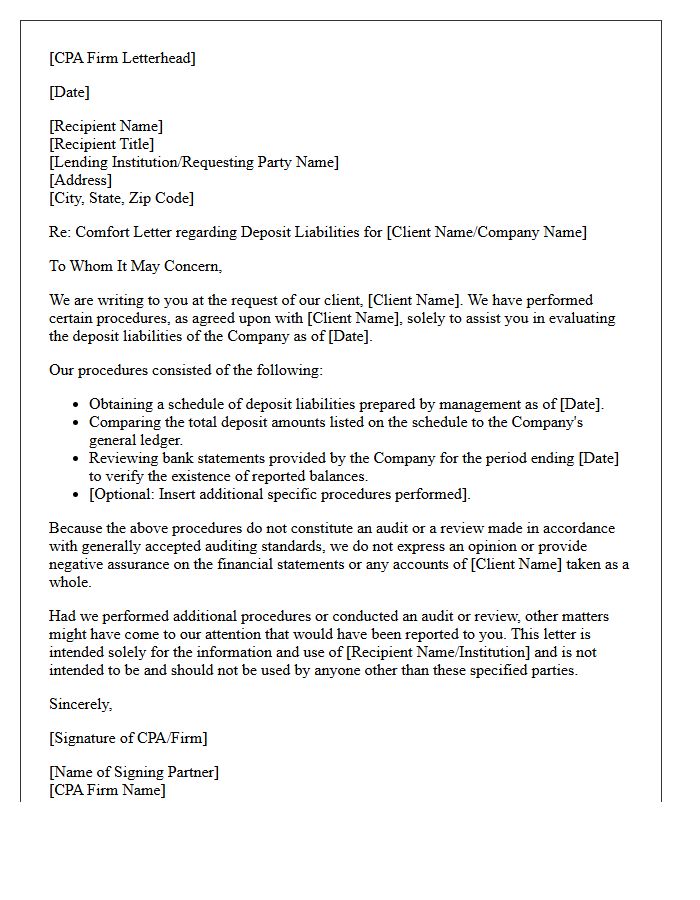

Certified Public Accountant Comfort Letter on Deposit Liabilities

A CPA Comfort Letter on deposit liabilities is a document issued by an independent auditor to provide negative assurance regarding a financial institution's reported holdings. It confirms that specific deposit balances and account data align with audited financial statements or internal records. Lenders and underwriters rely on these letters during due diligence to verify liquidity and fund availability. However, CPAs must follow strict professional standards, ensuring the scope is limited to matters subject to financial audit procedures to manage professional liability and maintain regulatory compliance.

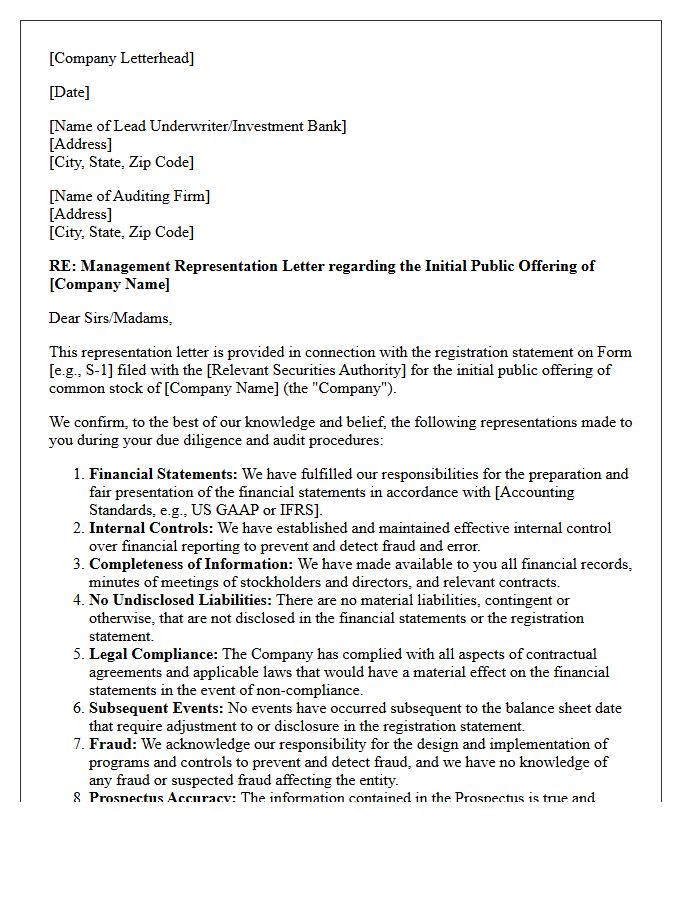

Executive Management Representation Letter for Initial Public Offerings

The Executive Management Representation Letter is a critical legal document provided to auditors during an Initial Public Offering (IPO). It serves as formal confirmation that all financial statements, data, and disclosures provided for the prospectus are accurate and complete. By signing this, executives assume personal accountability for the internal controls and the absence of undisclosed fraud. This letter reduces auditor liability by establishing that management has fulfilled its fiduciary duty, ensuring high transparency and investor confidence during the public listing process.

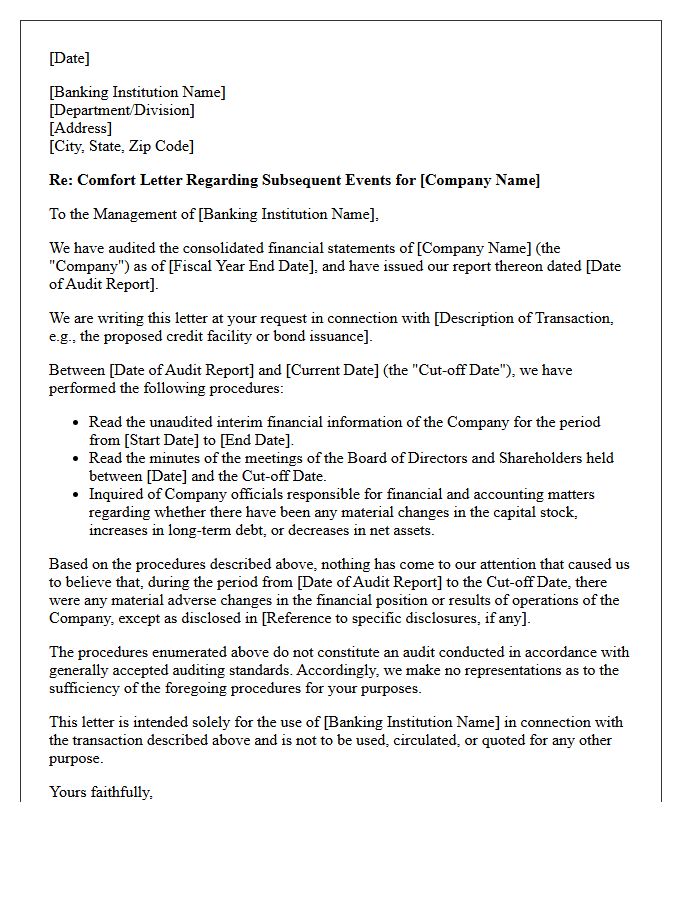

Subsequent Events Comfort Letter for Banking Institutions

A subsequent events comfort letter is a vital auditor verification provided to banking institutions during securities offerings. It confirms that no material changes occurred in the issuer's financial position between the last audit and the effective date of the transaction. This document offers negative assurance, helping underwriters establish due diligence defenses under securities laws. By bridging the reporting gap, it ensures banks rely on the most current financial data, mitigating risks associated with undisclosed liabilities or adverse trends emerging after the formal financial statements were finalized.

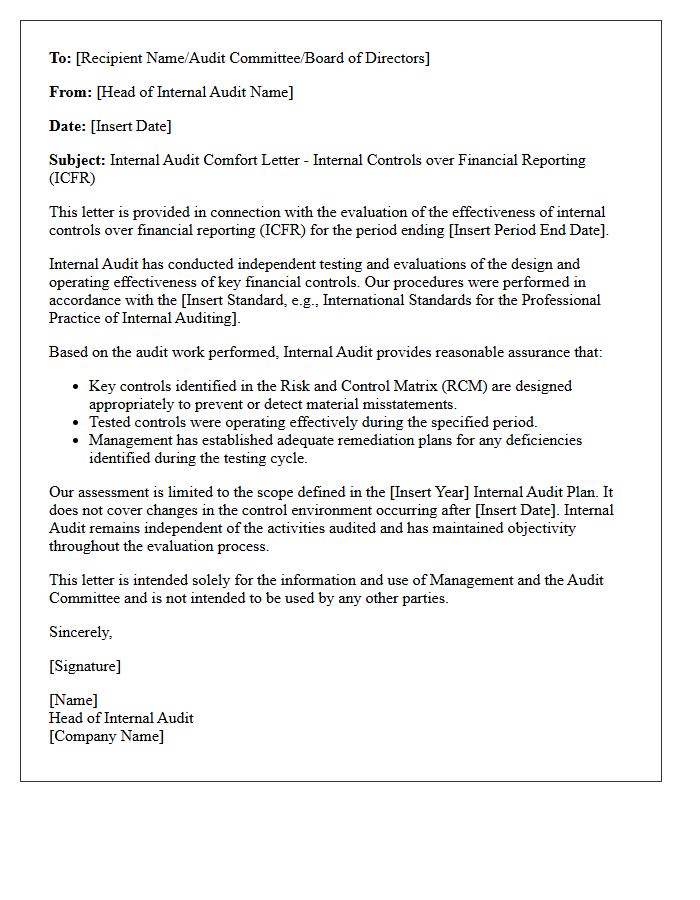

Internal Audit Comfort Letter on Financial Reporting Controls

An Internal Audit Comfort Letter provides independent assurance regarding the effectiveness of an organization's financial reporting controls. It serves as a formal statement confirming that internal systems are rigorously monitored to prevent material misstatements. Stakeholders, such as boards and external auditors, rely on this document to gain confidence in the integrity of internal financial data. By validating internal control over financial reporting (ICFR), the letter mitigates risk, ensures regulatory compliance, and reinforces the overall reliability of the company's financial disclosures during audits or corporate transactions.

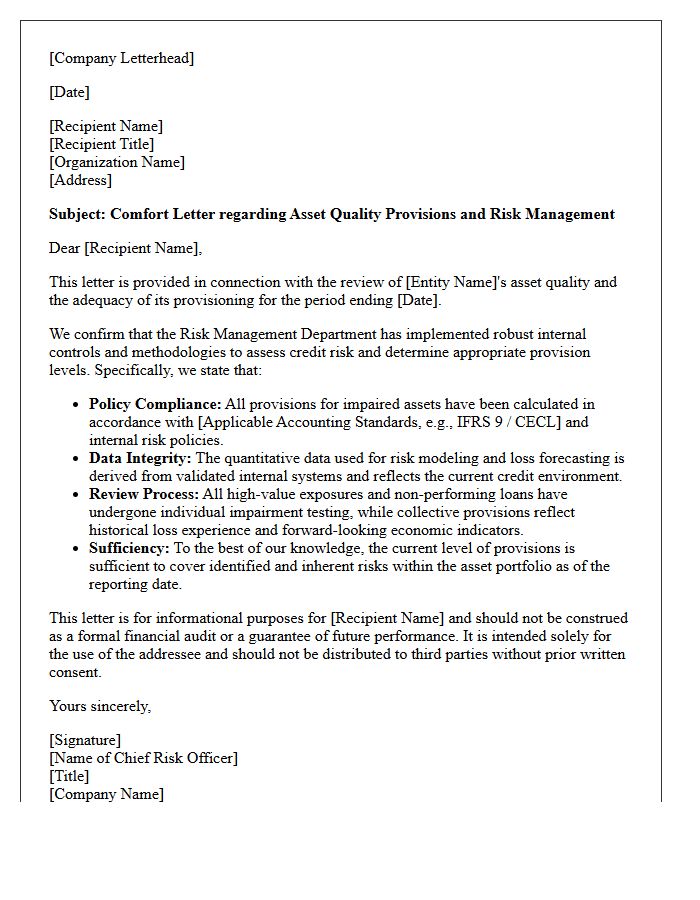

Risk Management Comfort Letter on Asset Quality Provisions

A Risk Management Comfort Letter serves as a formal assurance regarding Asset Quality Provisions, validating that a financial institution has allocated sufficient reserves for potential loan losses. It confirms that the valuation methodologies and impairment assessments align with regulatory standards and internal risk frameworks. This document provides stakeholders with confidence in the entity's financial stability and risk mitigation practices. By detailing the adequacy of provisions against non-performing assets, the letter ensures transparency in credit risk reporting and supports informed decision-making for investors and auditors during financial reviews.

What is a comfort letter in the context of an Initial Public Offering (IPO)?

A comfort letter is a document issued by an issuer's independent auditors to the underwriters of an IPO. It provides negative assurance that the financial statements and specific financial data in the registration statement comply with accounting standards and have undergone specified verification procedures.

Why do underwriters require a comfort letter during the IPO process?

Underwriters require a comfort letter as part of their "due diligence" defense under securities laws. It helps demonstrate that they have performed a reasonable investigation into the accuracy of the financial information presented in the prospectus, thereby reducing their legal liability.

What financial information is typically covered in an IPO comfort letter?

The letter typically covers audited financial statements, unaudited interim financial information, and "capsule" data. It also includes a "tick-and-tie" section where auditors verify specific percentages, dollar amounts, and financial ratios found throughout the prospectus against the company's internal accounting records.

What is the difference between positive and negative assurance in a comfort letter?

Positive assurance is a definitive statement that financial statements comply with GAAP, usually reserved for audited periods. Negative assurance, more common in comfort letters, states that "nothing came to the auditor's attention" to indicate that the unaudited financial data does not comply with standards or requires material modification.

When are comfort letters typically delivered during the IPO timeline?

There are generally two deliveries: the "initial comfort letter" is provided on the date the underwriting agreement is signed (the pricing date), and a "bring-down comfort letter" is provided on the closing date to confirm that no material financial changes have occurred in the interim.

Comments