A Comfort Letter for Regulatory Capital Compliance is a formal document issued by auditors or parent companies to assure regulators of a financial institution's solvency and capital adequacy. It bridges the gap between audited financial statements and real-time regulatory requirements, ensuring stability and trust within the banking sector. To help you draft yours, below are some ready to use template.

Image cover: Professional Comfort Letter Samples and Templates for Regulatory Capital Compliance

Letter Samples List

- Comfort Letter for Tier One Capital Adequacy

- Regulatory Capital Compliance Comfort Letter

- Comfort Letter for Basel III Framework Adherence

- Parent Company Comfort Letter for Subsidiary Capitalization

- Auditor Comfort Letter for Capital Instrument Issuance

- Comfort Letter for Stress Testing and Capital Buffer Compliance

- Risk-Weighted Assets Verification Comfort Letter

- Comfort Letter for Capital Conservation Buffer Requirements

- Liquidity Coverage Ratio Compliance Comfort Letter

- Comfort Letter for Subordinated Debt Capital Recognition

- Central Bank Regulatory Capital Reporting Comfort Letter

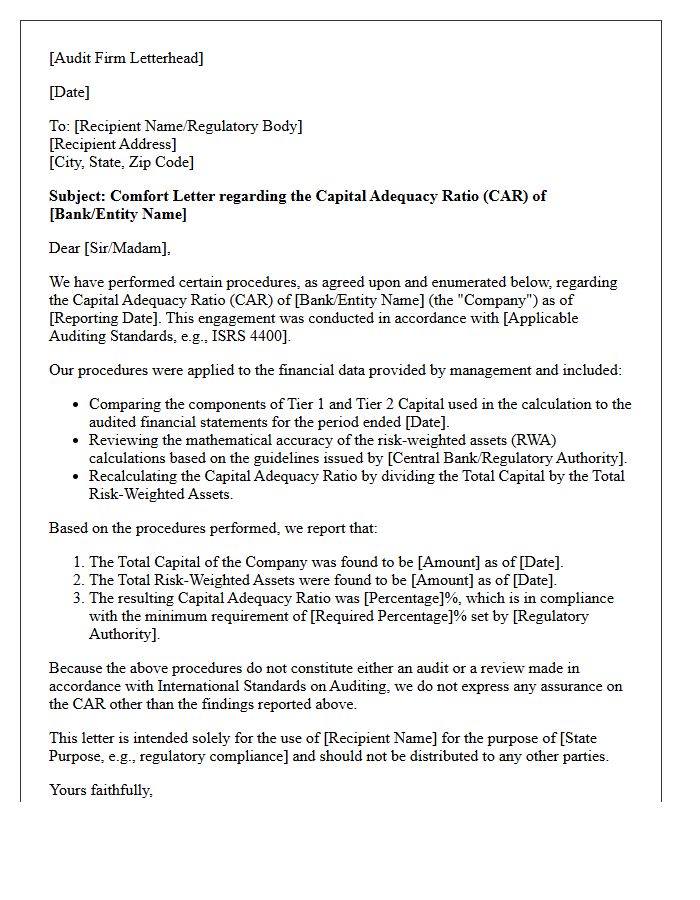

- External Audit Comfort Letter for Capital Adequacy Ratio

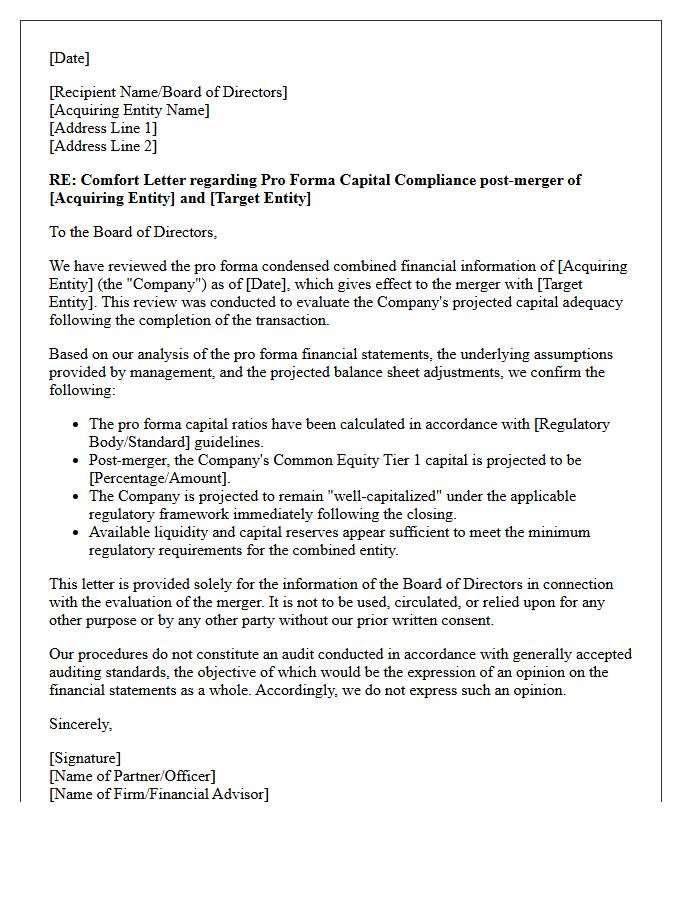

- Comfort Letter for Pro Forma Capital Compliance Post-Merger

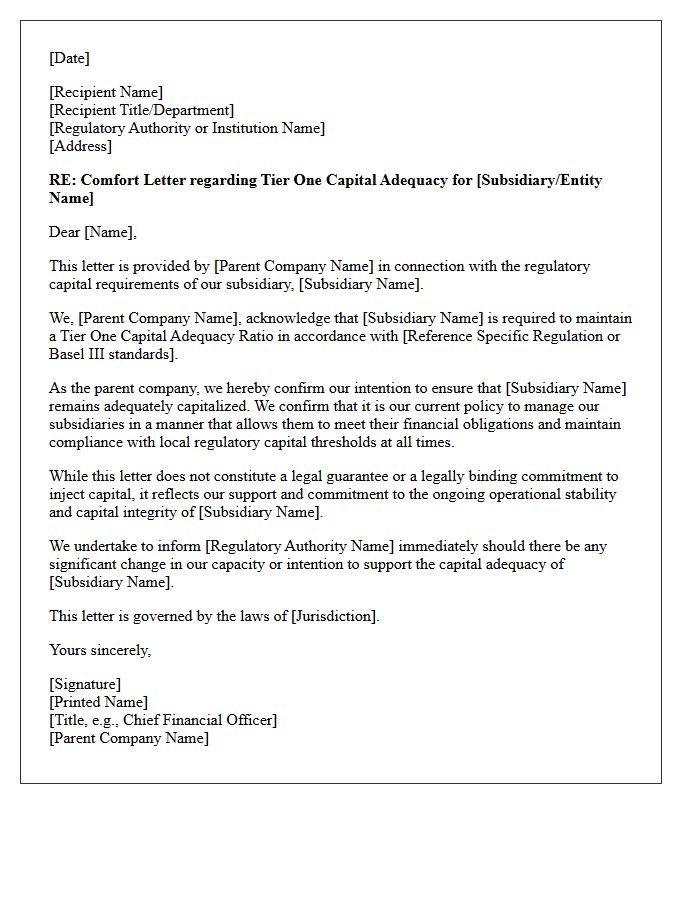

Comfort Letter for Tier One Capital Adequacy

A Comfort Letter for Tier One Capital Adequacy is a formal document issued by independent auditors to reassure regulators and investors regarding a bank's financial stability. It verifies that the Common Equity Tier 1 capital meets strict regulatory thresholds under Basel III frameworks. This letter confirms that the data used to calculate solvency ratios is accurate and consistent with audited financial statements. By providing an external layer of validation, it ensures that the institution maintains sufficient high-quality liquid assets to absorb unexpected losses during periods of financial stress.

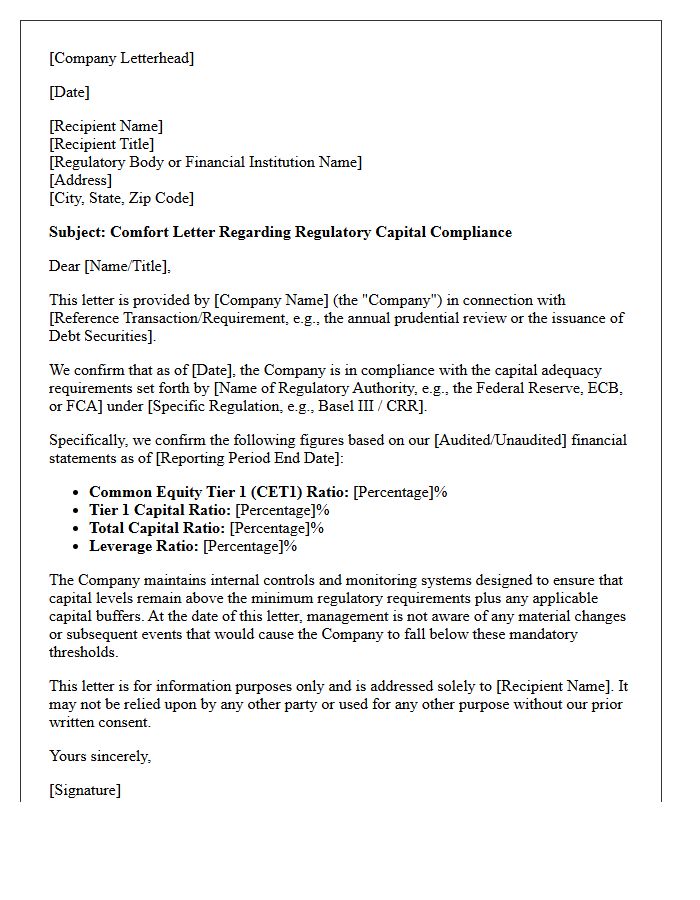

Regulatory Capital Compliance Comfort Letter

A Regulatory Capital Compliance Comfort Letter is a formal document issued by independent auditors to financial institutions or underwriters. It provides negative assurance that an entity's capital adequacy ratios align with specific regulatory frameworks, such as Basel III. This letter validates that financial data used for reporting maintains consistency with audited statements. It is a critical tool for risk management, ensuring that banks meet the mandatory minimum capital requirements to absorb potential losses, thereby maintaining market confidence and ensuring legal compliance during complex securities offerings or structural financial transactions.

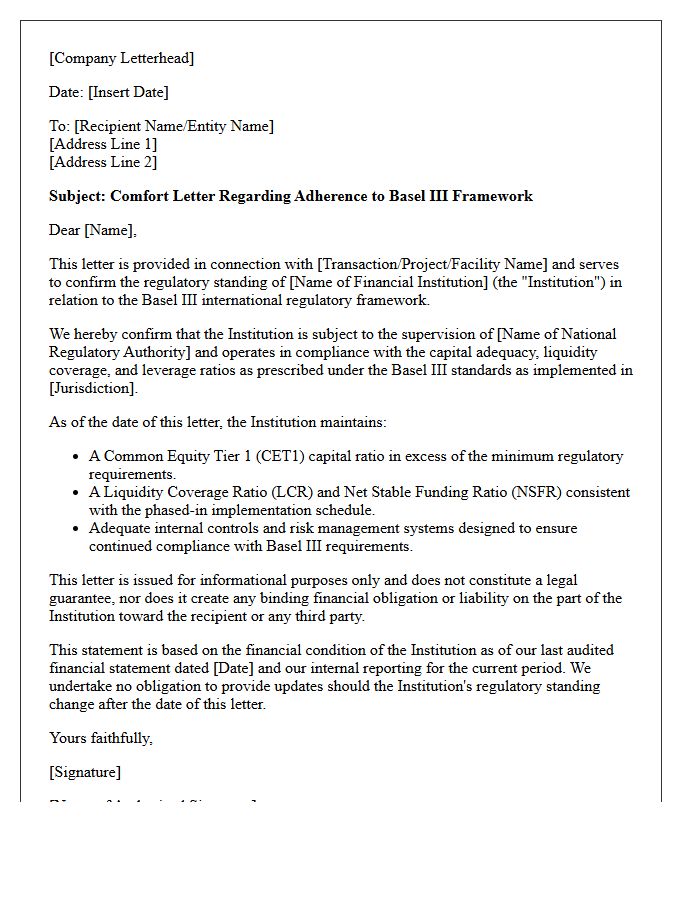

Comfort Letter for Basel III Framework Adherence

A Comfort Letter serves as a non-binding attestation provided by a parent company or auditor to regulators. It confirms a financial institution's commitment to maintain capital adequacy and liquidity standards mandated by the Basel III Framework. This document reassures stakeholders that the entity will support its subsidiary to ensure regulatory compliance and financial stability. While not a formal legal guarantee, it is a crucial tool for enhancing transparency and building trust within the global banking system by signaling a strong internal risk management culture and financial oversight.

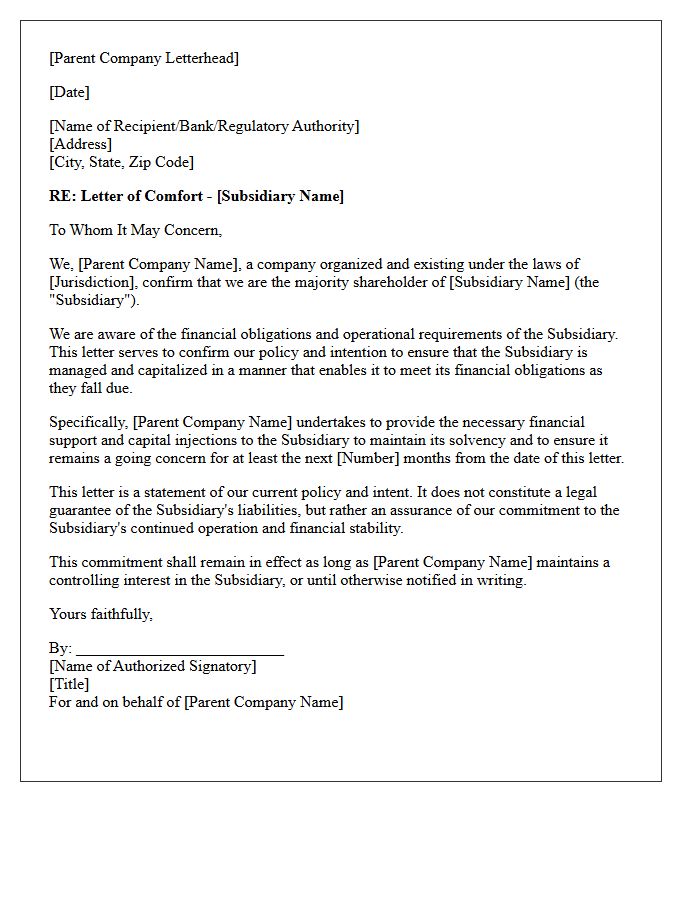

Parent Company Comfort Letter for Subsidiary Capitalization

A parent company comfort letter is a financial support declaration issued to auditors or regulators. It confirms the parent's intent to maintain the subsidiary capitalization and ensure its ongoing liquidity. While often not a legally binding guarantee, it provides critical assurance that the subsidiary can meet its liabilities and continue as a going concern. This document is essential during audits to mitigate solvency risks when a subsidiary lacks sufficient independent assets. Understanding the legal enforceability and specific wording is vital for both lenders and stakeholders assessing corporate group stability.

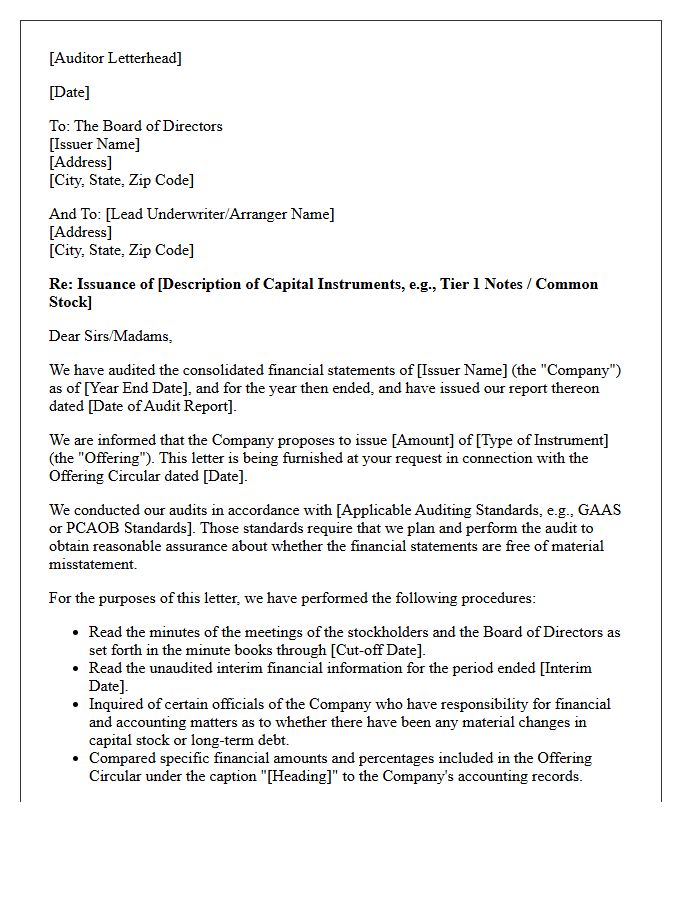

Auditor Comfort Letter for Capital Instrument Issuance

An Auditor Comfort Letter is a critical document issued by independent accountants to underwriters during a capital instrument issuance. It provides negative assurance that financial data in the prospectus aligns with audited records and hasn't materially changed since the last audit. This letter helps underwriters establish due diligence defenses under securities laws by verifying non-audited financial information. It reduces investment risk by ensuring financial transparency and accuracy, confirming that no significant adverse movements have occurred in the issuer's financial position before the securities are officially launched on the market.

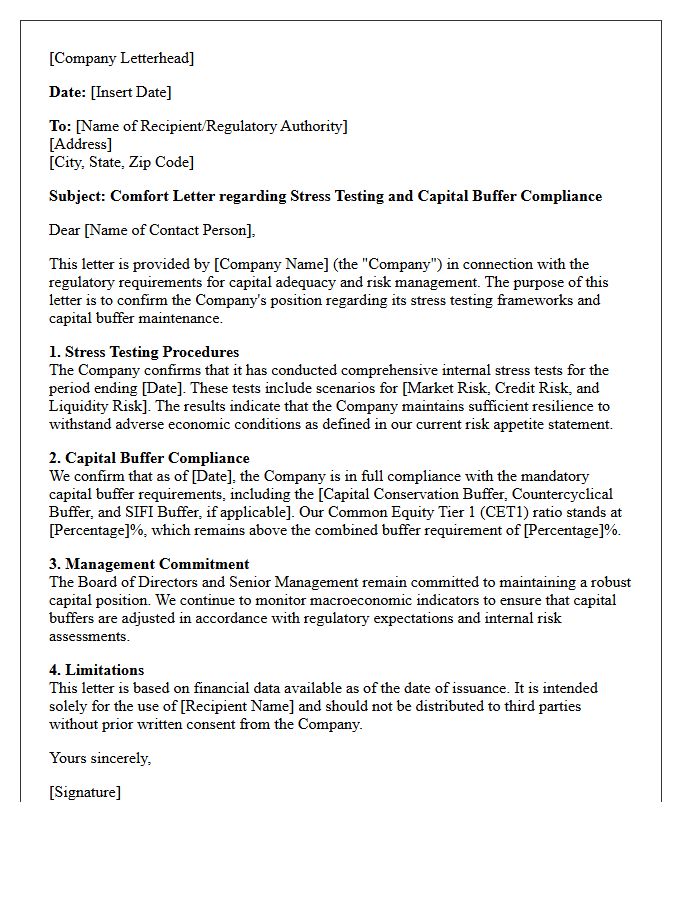

Comfort Letter for Stress Testing and Capital Buffer Compliance

A Comfort Letter is a formal document issued by an auditor or parent company to reassure regulators about a firm's financial resilience. It confirms that the entity maintains a sufficient capital buffer to withstand economic shocks identified during stress testing. This letter serves as a crucial compliance tool, demonstrating a commitment to solvency requirements and risk management standards. By validating projected capital levels under adverse scenarios, it provides authorities with the necessary confidence that the institution can absorb losses without breaching regulatory thresholds or requiring external bailouts.

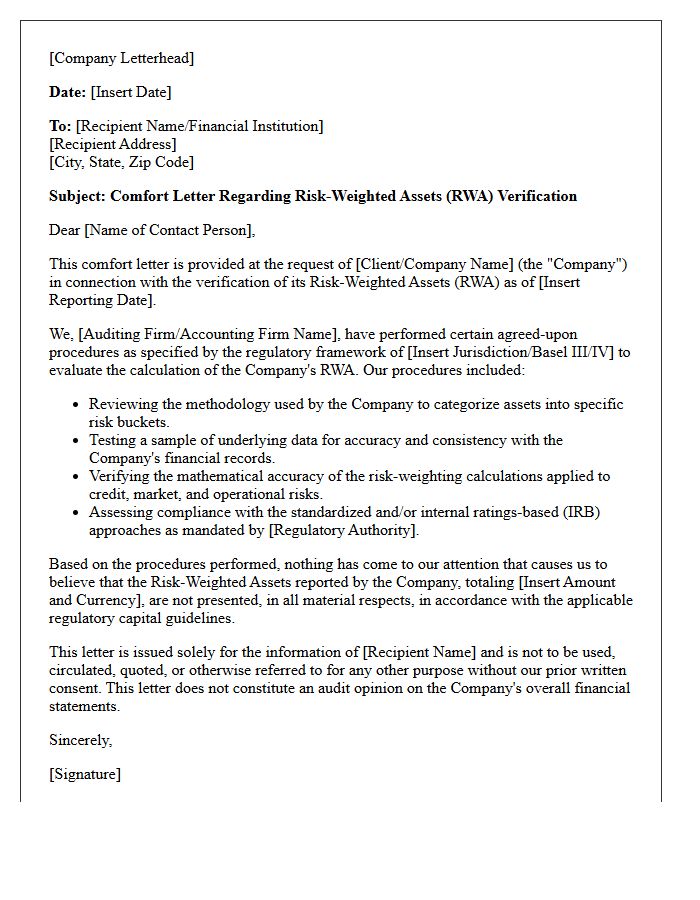

Risk-Weighted Assets Verification Comfort Letter

A Risk-Weighted Assets Verification Comfort Letter is a formal document issued by independent auditors to provide assurance regarding the accuracy of a bank's reported capital adequacy. It confirms that the calculation of assets, adjusted for credit risk and market exposure, aligns with regulatory frameworks like Basel III. This letter serves as a validation tool for investors and regulators during capital raises, ensuring that the institution maintains sufficient buffers. It builds market confidence by verifying that the risk-weighting methodology is consistent, transparent, and compliant with established financial standards.

Comfort Letter for Capital Conservation Buffer Requirements

A Comfort Letter is a formal document issued by a parent company or auditor to assure regulators of financial support regarding Capital Conservation Buffer (CCB) requirements. Under Basel III, banks must maintain this extra capital layer to absorb losses during economic stress. The letter signifies a commitment to monitor and maintain adequate CET1 capital levels, ensuring the institution remains above the minimum regulatory threshold. It provides supervisory confidence that the entity can withstand market volatility without breaching mandatory solvency ratios or facing restrictive distribution constraints.

Liquidity Coverage Ratio Compliance Comfort Letter

A Liquidity Coverage Ratio (LCR) Compliance Comfort Letter is a formal document issued by an auditor or parent company to assure regulators of a financial institution's liquidity health. It confirms that the entity maintains sufficient high-quality liquid assets to survive a 30-day stress scenario. For multinational banks, these letters serve as a regulatory guarantee that local subsidiaries can meet short-term obligations independently. Providing this assurance is critical for maintaining market confidence and ensuring compliance with Basel III standards, effectively bridging information gaps between stakeholders and internal management.

Comfort Letter for Subordinated Debt Capital Recognition

A comfort letter for subordinated debt is a critical document issued by an auditor or parent company to provide assurance regarding financial stability. Its primary purpose is to satisfy regulatory requirements for capital recognition, ensuring the debt qualifies as Tier 2 or supplementary capital. The letter confirms that the instrument's terms meet specific regulatory standards, such as loss-absorption capacity and maturity. By validating the legal and financial structure of the debt, it grants regulators confidence that the funds are reliably available to protect depositors and maintain overall solvency.

Central Bank Regulatory Capital Reporting Comfort Letter

A Central Bank Regulatory Capital Reporting Comfort Letter is a formal document issued by external auditors to provide limited assurance regarding a financial institution's compliance with regulatory capital adequacy requirements. It confirms that capital ratios and calculations align with specific central bank guidelines. This letter offers stakeholders and regulators increased confidence in the accuracy of reported data, serving as a critical risk management tool during audits or debt issuances. It bridges the gap between internal financial reporting and official regulatory expectations, ensuring transparency in a bank's solvency and financial stability.

External Audit Comfort Letter for Capital Adequacy Ratio

An External Audit Comfort Letter is a critical document issued by independent auditors to provide negative assurance regarding a bank's Capital Adequacy Ratio (CAR). It confirms that the financial data used to calculate regulatory capital aligns with audited statements and Basel III standards. Investors and regulators rely on this letter during capital raising to verify financial stability. By validating the risk-weighted assets and capital base, the letter enhances market confidence, ensuring the institution maintains sufficient buffers to absorb potential losses and meet legal solvency requirements effectively.

Comfort Letter for Pro Forma Capital Compliance Post-Merger

A comfort letter for pro forma capital compliance is a critical document issued by independent auditors to underwriters during a merger. It provides negative assurance that the combined entity's financial statements align with regulatory capital requirements. This process ensures that pro forma adjustments are mathematically accurate and based on reasonable assumptions. For investors, it verifies that the post-merger company maintains sufficient liquidity and solvency, mitigating financial risk. Obtaining this letter is a standard due diligence step to confirm the accuracy of capital projections before finalizing the transaction.

What is a Comfort Letter for regulatory capital compliance?

A Comfort Letter for regulatory capital compliance is a formal document issued by an independent auditor to regulators or underwriters, providing negative assurance that a financial institution's capital adequacy calculations align with specific regulatory frameworks, such as Basel III or local banking statutes.

Why do regulators require Comfort Letters for capital adequacy?

Regulators and stakeholders require these letters to gain independent verification that a bank's reported risk-weighted assets (RWA) and Tier 1 capital ratios are prepared using consistent accounting policies and accurate financial data during a capital raise or reporting cycle.

What specific financial metrics are typically covered in a regulatory Comfort Letter?

The letter generally covers the Common Equity Tier 1 (CET1) ratio, the Total Capital Ratio, the Leverage Ratio, and the verification of Risk-Weighted Assets (RWAs) against the figures presented in the institution's audited financial statements.

Does a Comfort Letter constitute a full audit of regulatory capital?

No, a Comfort Letter is not a full audit; it is based on "agreed-upon procedures" (AUP) and provides limited assurance. It confirms that the financial information matches the audited records and that no material changes have occurred since the last reporting date that would breach capital requirements.

How does a Comfort Letter support a bank's Tier 2 capital issuance?

For Tier 2 capital instruments, such as subordinated debt, a Comfort Letter provides investors and underwriters with the necessary due diligence, ensuring that the issuance meets the specific regulatory criteria to be recognized as supplementary capital by the relevant central bank or authority.

Comments