A Mezzanine Debt Facility Commitment Letter is a formal agreement where a lender commits to providing subordinate financing to a borrower. This document outlines the key terms, interest rates, and conditions for the hybrid debt-equity capital used in complex corporate transactions. It serves as a critical milestone before final funding. To help you get started, below are some ready to use template.

Image cover: Mastering Mezzanine Debt Commitment Letters: Essential Samples and Templates

Letter Samples List

- Draft Mezzanine Debt Facility Commitment Letter

- Binding Mezzanine Debt Facility Commitment Letter

- Conditional Mezzanine Debt Facility Commitment Letter

- Uncommitted Mezzanine Debt Facility Discussion Letter

- Mezzanine Debt Facility Fee Letter

- Mezzanine Debt Facility Syndication Engagement Letter

- Amended Mezzanine Debt Facility Commitment Letter

- Restated Mezzanine Debt Facility Commitment Letter

- Mezzanine Debt Facility Commitment Extension Letter

- Mezzanine Debt Facility Commitment Termination Letter

- Mezzanine Debt Facility Sponsor Comfort Letter

- Mezzanine Debt Facility Commitment Reallocation Letter

- Mezzanine Debt Facility Commitment Transfer Letter

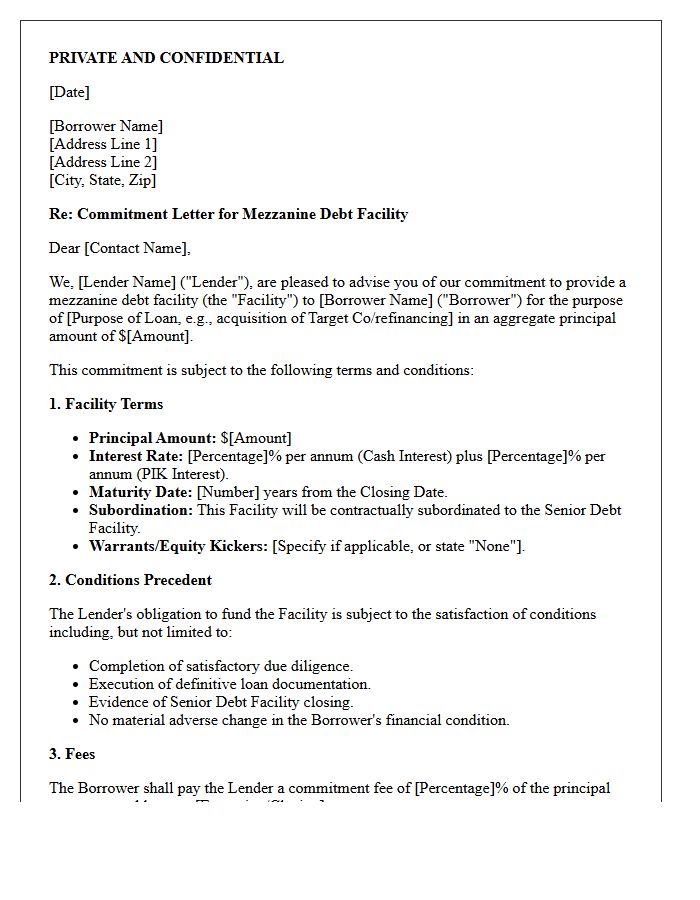

Draft Mezzanine Debt Facility Commitment Letter

A Draft Mezzanine Debt Facility Commitment Letter is a critical legal document outlining the binding agreement between a lender and borrower for subordinate financing. It specifies essential terms such as interest rates, repayment schedules, and equity warrants. This document serves as a formal roadmap for the transaction, ensuring all parties agree on the financial structure before final closing. Key components include funding conditions and fee structures, providing the necessary assurance to senior lenders that the gap financing is secured to complete the capital stack for large-scale acquisitions or development projects.

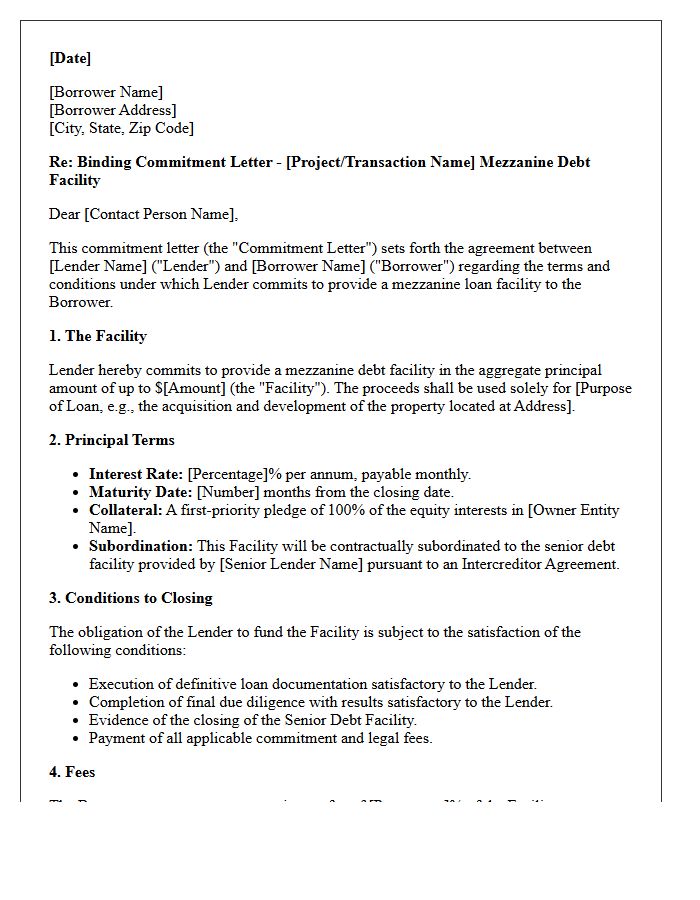

Binding Mezzanine Debt Facility Commitment Letter

A Binding Mezzanine Debt Facility Commitment Letter is a critical legal agreement where a lender formally pledges to provide subordinate financing for a transaction. This document outlines essential financial terms, including interest rates, repayment schedules, and specific conditions precedent. Unlike a highly confident letter, this commitment is legally enforceable, subject to the satisfaction of stated requirements. It provides the necessary certainty for sponsors to execute leveraged buyouts or real estate developments, signaling to all parties that the mezzanine funding is secured to bridge the gap between senior debt and equity.

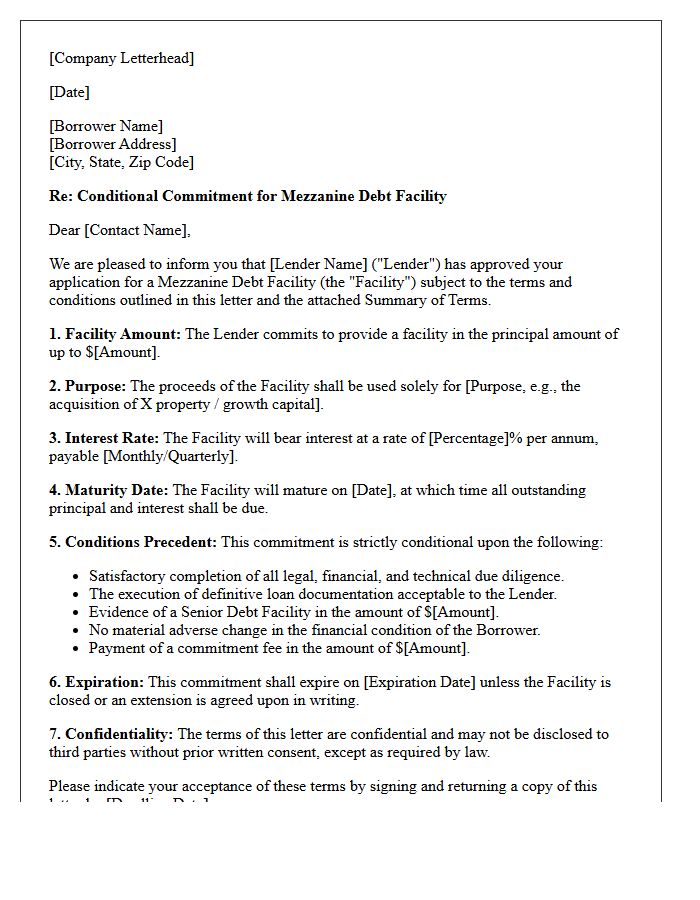

Conditional Mezzanine Debt Facility Commitment Letter

A Conditional Mezzanine Debt Facility Commitment Letter is a formal document where a lender outlines the specific terms for providing secondary financing. This subordinate debt bridges the gap between senior loans and equity, often used in complex acquisitions. The commitment is "conditional," meaning funding depends on the borrower meeting strict financial covenants, completing due diligence, and maintaining specific credit standards. It establishes the legal framework for interest rates, repayment schedules, and conversion rights before final loan agreements are executed, providing certainty for high-leverage capital structures.

Uncommitted Mezzanine Debt Facility Discussion Letter

An Uncommitted Mezzanine Debt Facility Discussion Letter serves as a preliminary, non-binding outline for potential junior financing. It details proposed subordinated debt terms, including interest rates, warrants, and repayment hierarchies. Since it is "uncommitted," the lender is not legally obligated to provide funds until final credit approval and definitive documentation are completed. This document acts as a critical roadmap for negotiations, allowing borrowers and lenders to align on capital structure and risk appetite before incurring significant legal expenses during the formal due diligence phase.

Mezzanine Debt Facility Fee Letter

A Mezzanine Debt Facility Fee Letter is a confidential agreement detailing the transaction costs associated with secondary financing. It outlines specific upfront fees, commitment charges, and arrangement expenses owed to lenders. This document remains separate from the main loan agreement to maintain privacy regarding sensitive commercial terms. Understanding these obligations is crucial for calculating the total cost of capital, as non-payment often triggers a default. It ensures transparency between the borrower and the mezzanine provider regarding the financial compensation required to execute and maintain the facility.

Mezzanine Debt Facility Syndication Engagement Letter

A Mezzanine Debt Facility Syndication Engagement Letter is a critical mandate between a borrower and a lead arranger. It outlines the best efforts or underwritten commitment to structure junior capital. Key provisions include syndication strategy, fee structures, and the "market flex" clause, allowing lenders to adjust terms based on investor demand. This document establishes the exclusive rights of the financial institution to manage the transaction. Understanding these terms is essential for securing flexible, high-yield financing while navigating the complexities of subordinated debt markets and intercreditor dynamics.

Amended Mezzanine Debt Facility Commitment Letter

An Amended Mezzanine Debt Facility Commitment Letter updates the terms of secondary financing, sitting between senior debt and equity. It legally outlines modified lending conditions, such as revised interest rates, warrants, or maturity dates. This document is essential for subordinated creditors and borrowers to formalize changes in the capital structure before closing. Understanding the intercreditor agreement implications within this letter ensures all parties agree on repayment priority and security rights during corporate acquisitions or refinancing processes.

Restated Mezzanine Debt Facility Commitment Letter

A Restated Mezzanine Debt Facility Commitment Letter is a legally binding document that modifies and supersedes a previous financing agreement. It outlines updated terms for subordinate debt, often bridging the gap between equity and senior loans. This document is crucial for debt restructuring and ensuring all parties agree to revised interest rates, repayment schedules, and subordination clauses. It provides the final framework for funding certainty before the formal closing of a leveraged buyout or large-scale real estate transaction, reflecting the most current financial obligations of the borrower.

Mezzanine Debt Facility Commitment Extension Letter

A Mezzanine Debt Facility Commitment Extension Letter is a legal document used to prolong the availability period of secondary financing. It allows borrowers additional time to meet funding conditions or close a transaction before the initial commitment expires. This letter typically outlines specific terms, such as updated maturity dates, extension fees, and any revised covenants. It is a critical tool for maintaining liquidity access during complex corporate restructuring or delayed acquisitions, ensuring that the junior capital remains committed while final closing requirements are finalized between the lender and the borrower.

Mezzanine Debt Facility Commitment Termination Letter

A Mezzanine Debt Facility Commitment Termination Letter is a formal legal document that officially ends a lender's obligation to provide subordinated financing. It typically occurs when the availability period expires, the borrower secures alternative funding, or conditions precedent are not met. This letter ensures that all accrued fees are settled and future borrowing capacities are cancelled, providing legal closure to the credit facility. It is a critical step in debt restructuring or final payoff scenarios to release parties from further contractual commitments and financial liabilities.

Mezzanine Debt Facility Sponsor Comfort Letter

A Mezzanine Debt Facility Sponsor Comfort Letter is a critical document provided by a private equity sponsor to subordinated lenders. It serves as a non-binding moral commitment to support the borrower's operations and maintain management oversight. While not a financial guarantee, it mitigates risk by detailing the sponsor's intent to provide operational guidance and potentially future equity injections. Lenders require this to ensure alignment of interests between the sponsor and the debt provider, bridging the gap between senior secured loans and equity in complex leveraged finance transactions.

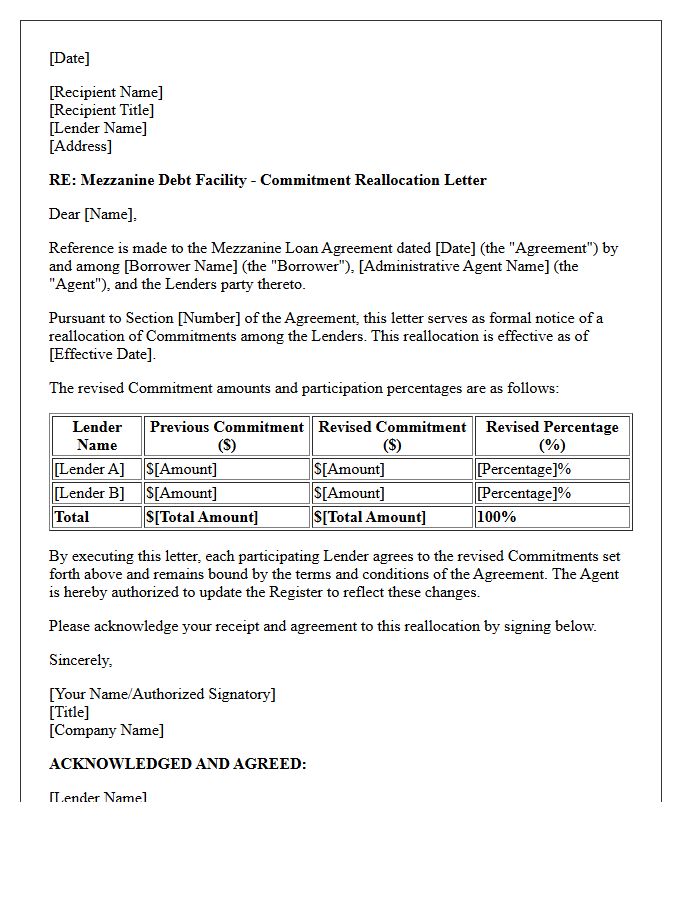

Mezzanine Debt Facility Commitment Reallocation Letter

A Mezzanine Debt Facility Commitment Reallocation Letter is a formal document used to redistribute lending obligations among creditors within a junior debt tier. It facilitates the transfer of commitment portions between existing or new lenders, typically during a syndication phase or restructuring. This letter ensures that the total facility limit remains constant while updating the specific financial exposure of each participant. It is crucial for maintaining accurate repayment schedules and legal alignment among stakeholders in complex leveraged finance arrangements.

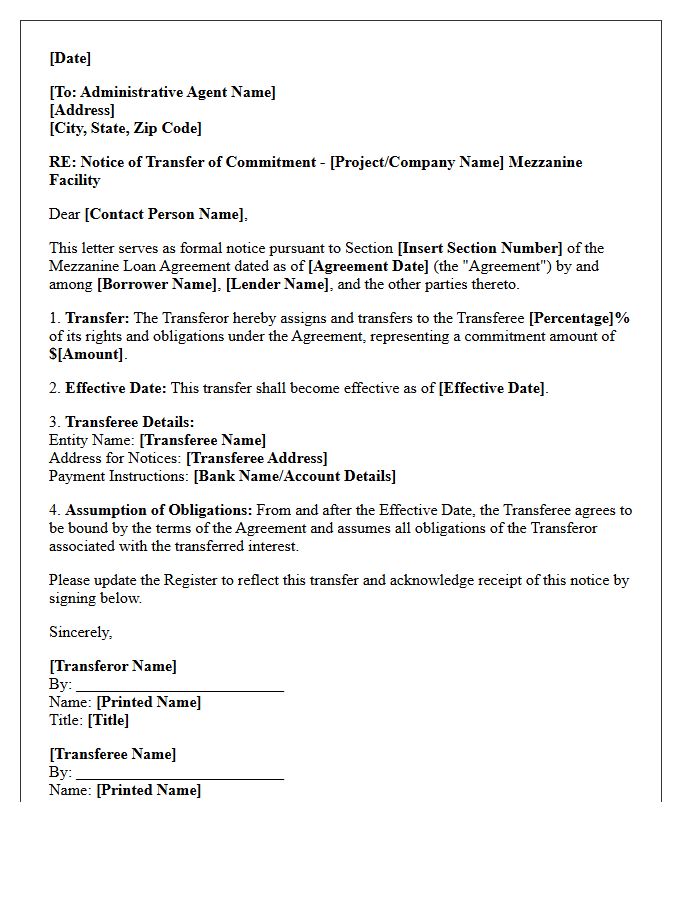

Mezzanine Debt Facility Commitment Transfer Letter

A Mezzanine Debt Facility Commitment Transfer Letter is a formal legal document used to reassign lending obligations from an existing lender to a new participant. This instrument ensures a seamless assignment of rights and liabilities within a subordinated debt structure. It is essential for maintaining liquidity in private equity and leveraged finance markets. Key elements include the transferor's release from future funding requirements and the transferee's legal assumption of debt. Proper execution ensures that the junior capital layer remains fully funded while allowing financial institutions to manage their balance sheet exposure effectively.

What is a Mezzanine Debt Facility Commitment Letter?

A Mezzanine Debt Facility Commitment Letter is a legally binding document issued by a lender outlining the specific terms and conditions under which they agree to provide subordinated financing to a borrower, typically for acquisitions, buyouts, or major capital expansions.

What are the typical conditions precedent found in a mezzanine commitment letter?

Common conditions precedent include the successful completion of due diligence, final credit committee approval, the execution of definitive loan documentation, intercreditor agreement finalization, and the maintenance of a specific maximum leverage ratio.

How does a commitment letter address the ranking of mezzanine debt?

The letter specifies that the debt is junior or subordinated to senior bank loans but senior to equity, often requiring an intercreditor agreement that defines the "standstill" periods and payment blockage rights held by senior lenders.

Are the terms in a mezzanine debt commitment letter legally binding?

While the commitment to fund is subject to satisfied conditions, the "market mac" (Material Adverse Change) clauses, fee letters, confidentiality agreements, and expense reimbursement provisions are typically immediately binding upon execution by both parties.

What financial covenants are usually outlined in a mezzanine commitment letter?

Mezzanine commitment letters generally outline restrictive covenants including a minimum Fixed Charge Coverage Ratio (FCCR), total leverage caps, limitations on further indebtedness, and restrictions on dividend distributions to equity holders.

Comments