A Truth in Lending Act Disclosure Letter is a mandatory document ensuring transparency by revealing the total cost of credit, including interest rates and fees. It empowers consumers to compare loan offers and understand their financial obligations clearly under federal law. To help you maintain compliance and accuracy, below are some ready to use template.

Image cover: Your Guide to Truth in Lending Act Disclosure Templates and Compliant Letter Samples

Letter Samples List

- Initial Truth in Lending Act Disclosure Letter

- Final Truth in Lending Act Disclosure Letter

- Right of Rescission Truth in Lending Act Letter

- Adjustable Rate Mortgage Truth in Lending Act Disclosure Letter

- Early Truth in Lending Act Disclosure Letter

- Credit Card Truth in Lending Act Disclosure Letter

- Personal Loan Truth in Lending Act Disclosure Letter

- Auto Loan Truth in Lending Act Disclosure Letter

- Home Equity Line of Credit Truth in Lending Act Letter

- Change of Terms Truth in Lending Act Disclosure Letter

- Closed-End Credit Truth in Lending Act Disclosure Letter

- Open-End Credit Truth in Lending Act Disclosure Letter

- Refinance Truth in Lending Act Disclosure Letter

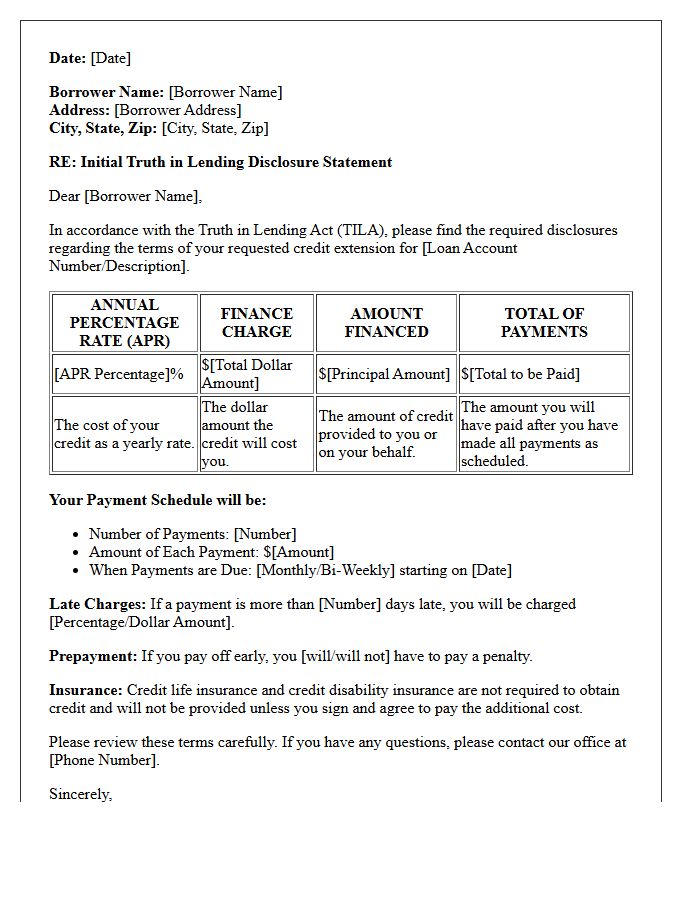

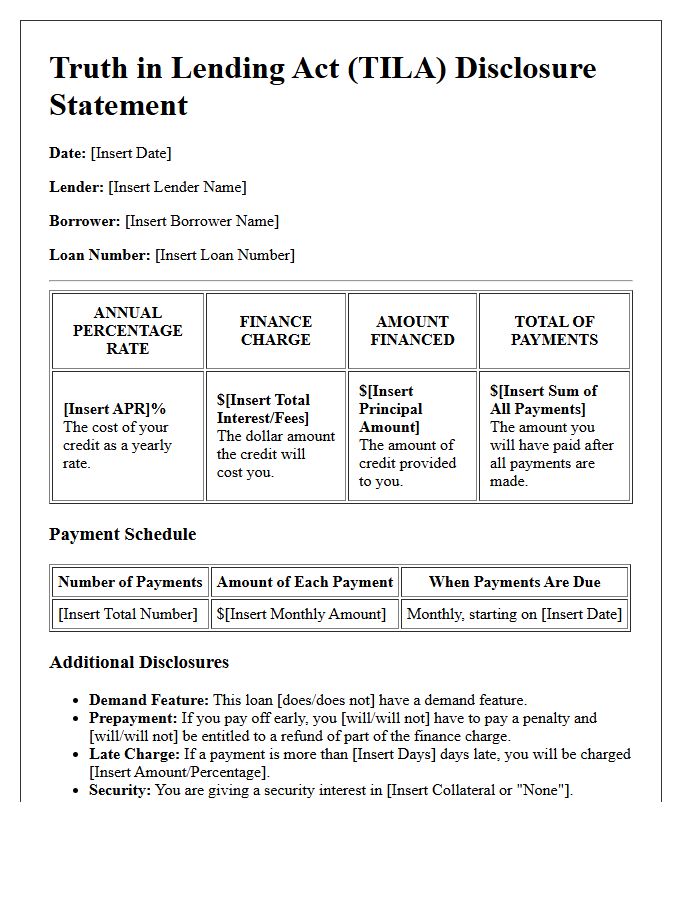

Initial Truth in Lending Act Disclosure Letter

The Initial Truth in Lending Act Disclosure Letter is a mandatory document providing transparency for borrowers. It outlines the Annual Percentage Rate (APR), total finance charges, amount financed, and the complete payment schedule. This disclosure ensures consumers can compare loan costs effectively before finalizing an agreement. By highlighting the cost of credit as a yearly rate, it prevents hidden fees and promotes informed financial decisions. Reviewing this letter is essential to understand your long-term financial obligations and the true expense of borrowing money from a lender.

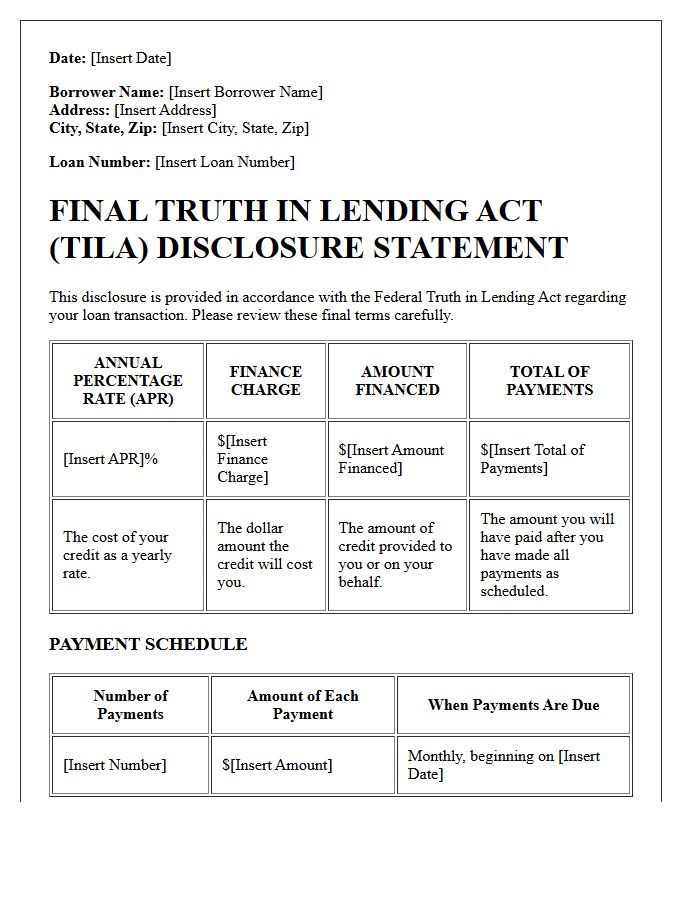

Final Truth in Lending Act Disclosure Letter

The Final Truth in Lending Act (TILA) Disclosure is a critical document provided by lenders before closing. It ensures transparency by detailing the Annual Percentage Rate (APR), finance charges, total amount financed, and the complete payment schedule. This disclosure allows borrowers to understand the true cost of credit and compare loan offers accurately. You must review these loan terms carefully to verify that the interest rate and fees align with your initial estimate before signing the legally binding agreement.

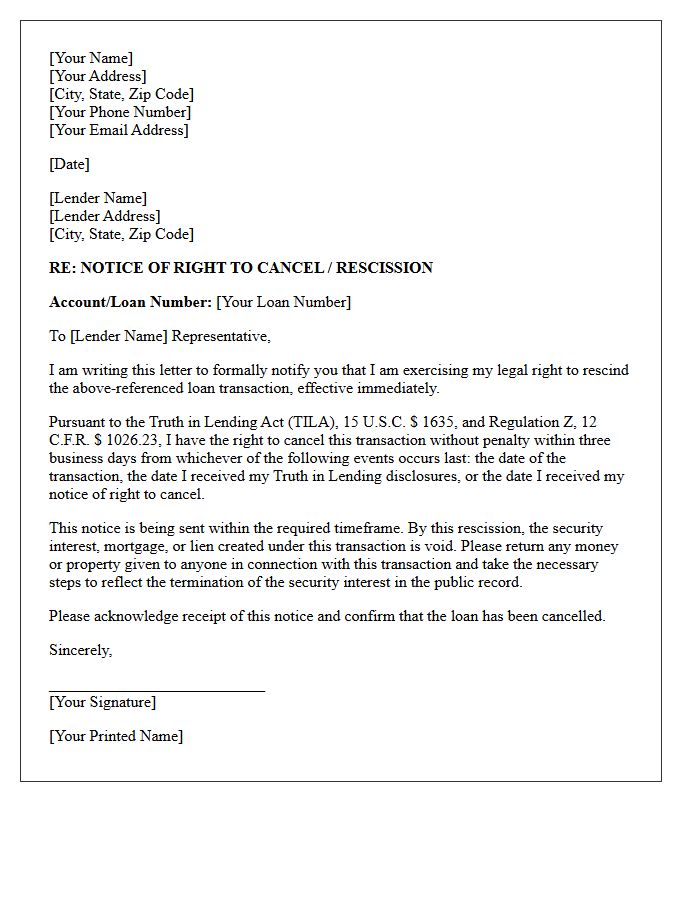

Right of Rescission Truth in Lending Act Letter

Under the Truth in Lending Act, the Right of Rescission allows homeowners to cancel certain mortgage-related loans within three business days. To exercise this protection, you must submit a formal rescission letter to your lender before the midnight deadline. This cooling-off period typically applies to home equity lines of credit or refinances on a primary residence. If the lender failed to provide mandatory disclosures, the right to cancel may extend up to three years. Always send your notice via certified mail to ensure documented proof of your timely cancellation.

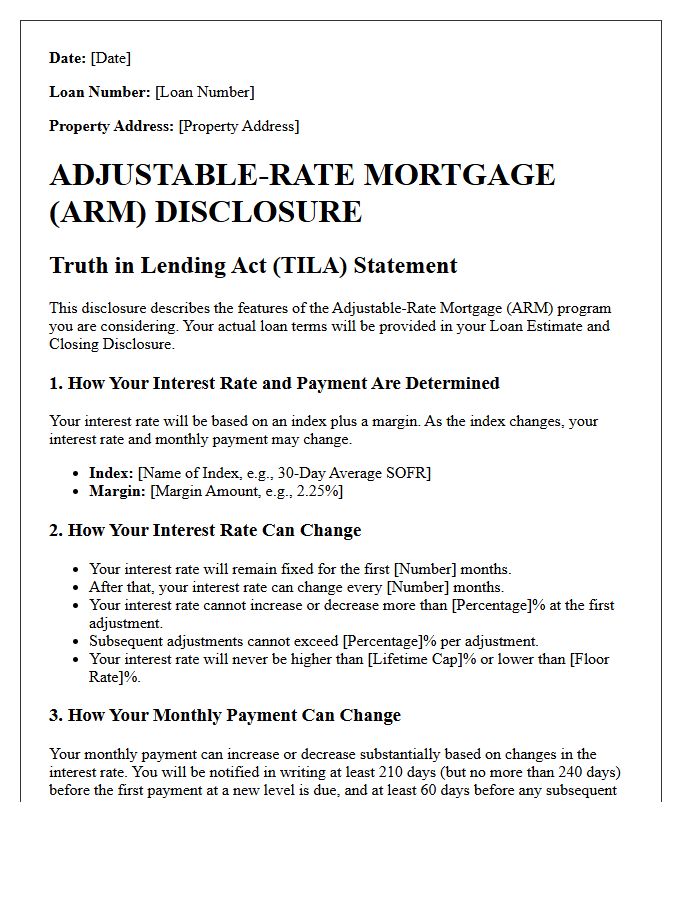

Adjustable Rate Mortgage Truth in Lending Act Disclosure Letter

The Adjustable Rate Mortgage Truth in Lending Act Disclosure Letter is a mandatory federal document ensuring transparency for borrowers. It highlights critical details about your loan, including the initial interest rate, payment schedule, and potential maximum costs. The most vital feature is the interest rate adjustment disclosure, which explains how and when your monthly payments might change based on market indices. By reviewing this letter, you gain a clear understanding of the financial risks and total Annual Percentage Rate (APR) before finalizing your home financing commitment.

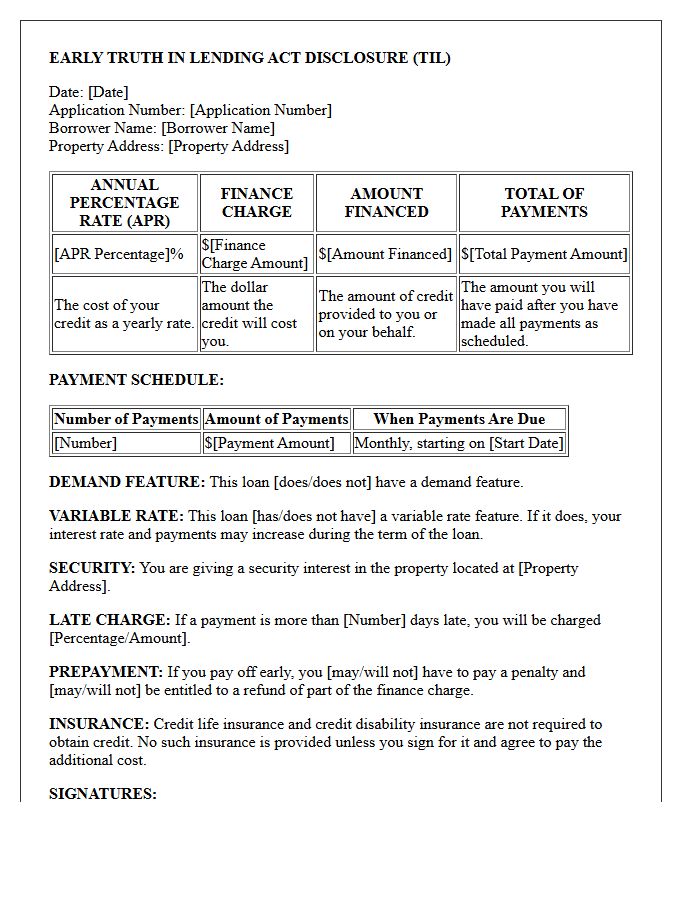

Early Truth in Lending Act Disclosure Letter

The Early Truth in Lending Act Disclosure Letter is a critical document provided to borrowers within three business days of a mortgage application. It ensures transparency by highlighting the Annual Percentage Rate (APR), which reflects the total cost of credit. This disclosure allows consumers to compare loan offers effectively by detailing the finance charge, amount financed, and total payment schedule. Understanding these standardized terms helps borrowers identify the true long-term expense of their loan before committing to a binding agreement, protecting them from hidden fees and predatory lending practices.

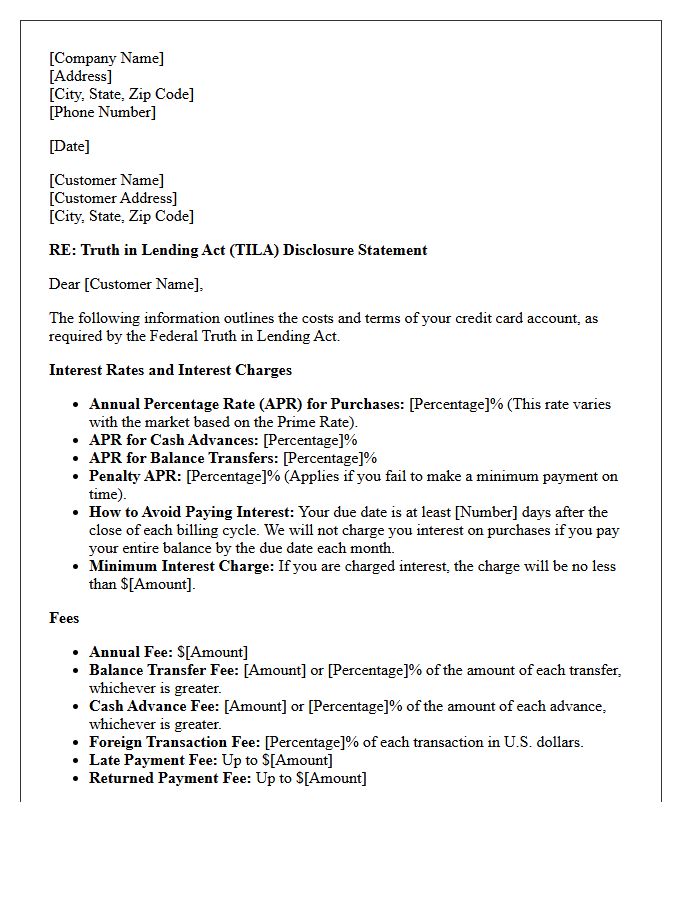

Credit Card Truth in Lending Act Disclosure Letter

A Credit Card Truth in Lending Act Disclosure Letter is a mandatory document ensuring transparency in consumer credit. It provides standardized financial terms so borrowers can compare costs effectively. The most critical element is the Schumer Box, which highlights the Annual Percentage Rate (APR), interest rates, and transaction fees. By law, lenders must disclose grace periods and penalty charges before an account is opened. Understanding this disclosure protects consumers from hidden costs and predatory lending practices, fostering informed financial decisions through clear, regulated communication of all potential credit obligations.

Personal Loan Truth in Lending Act Disclosure Letter

A Personal Loan Truth in Lending Act (TILA) Disclosure Letter is a mandatory document ensuring transparency in consumer credit. The most critical component is the Annual Percentage Rate (APR), which reflects the total yearly cost of borrowing. This disclosure explicitly outlines the finance charge, amount financed, and total payment schedule. By law, lenders must provide these standardized terms before you sign a contract, allowing borrowers to compare offers accurately. Reviewing this document helps you understand the true long-term expense and avoid hidden fees associated with your personal loan.

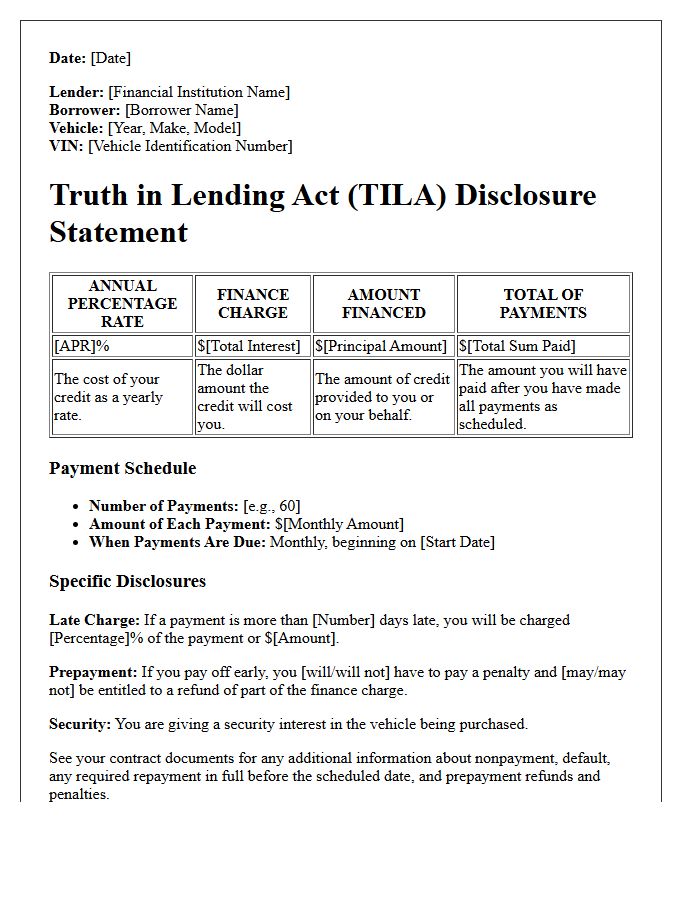

Auto Loan Truth in Lending Act Disclosure Letter

An Auto Loan Truth in Lending Act (TILA) Disclosure Letter is a vital document ensuring transparency in vehicle financing. It mandates that lenders provide a clear breakdown of the Annual Percentage Rate (APR), total finance charges, and the amount financed. This standardized form allows consumers to compare loan offers accurately by revealing the true cost of credit over time. Key details include your monthly payment schedule and any late fees, protecting you from hidden costs and ensuring informed financial decisions before signing a binding contract.

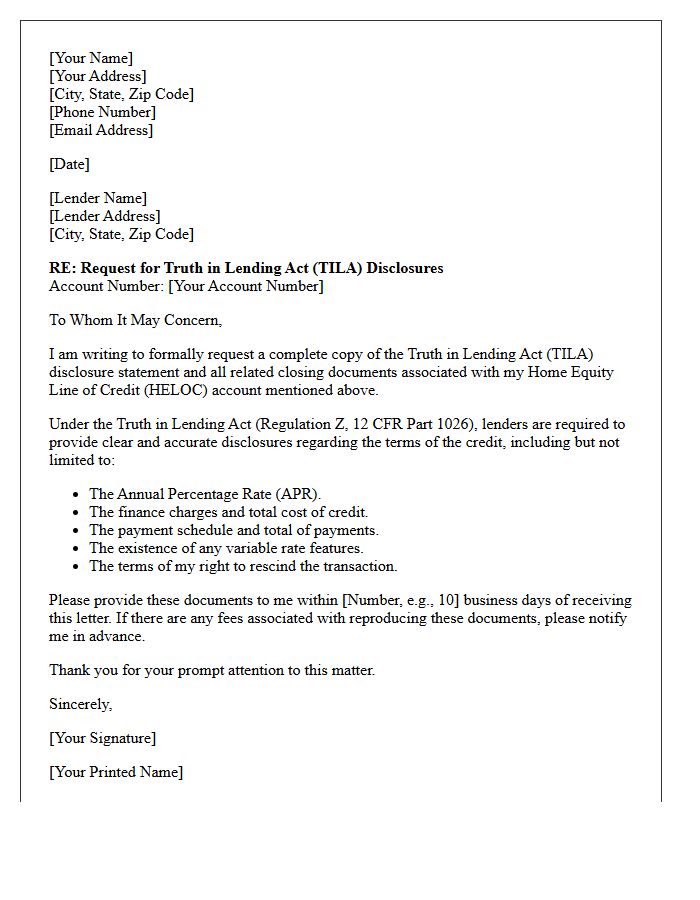

Home Equity Line of Credit Truth in Lending Act Letter

The HELOC Truth in Lending Act (TILA) Letter provides critical transparency regarding your credit terms. This mandatory disclosure ensures you understand the Annual Percentage Rate, payment schedules, and total financing costs. It protects consumers by requiring lenders to reveal hidden fees and variable interest rate structures before the loan is finalized. Reviewing this document is essential to identify your maximum interest rate cap and potential balloon payments. Under TILA, you also typically receive a three-day right of rescission, allowing you to cancel the agreement without penalty if you change your mind.

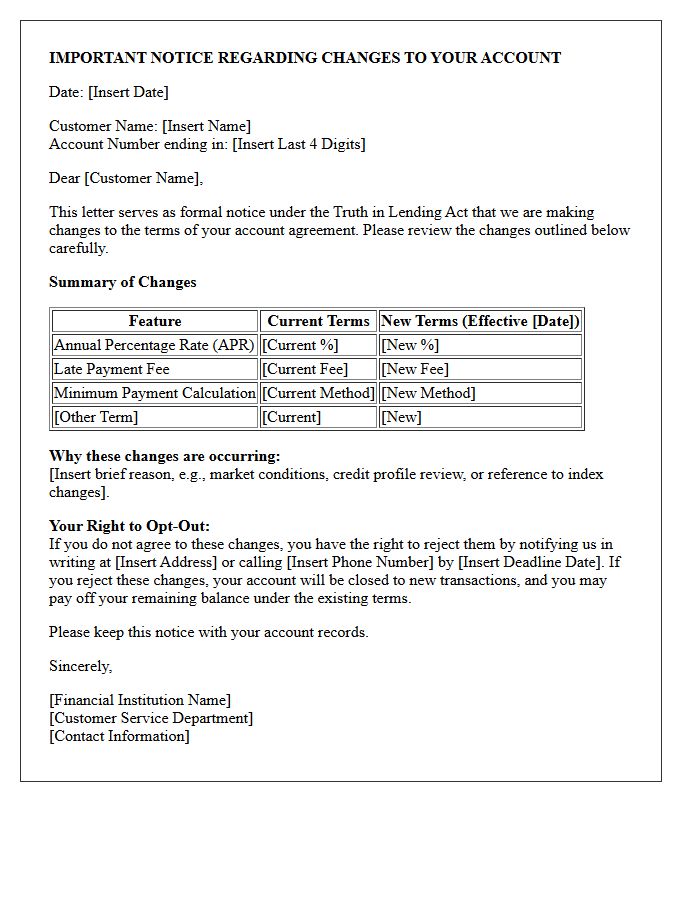

Change of Terms Truth in Lending Act Disclosure Letter

A Change of Terms Truth in Lending Act Disclosure Letter is a mandatory legal notice issued by creditors to inform consumers about significant amendments to their credit agreements. Under Regulation Z, lenders must provide this written notification at least 45 days before changes take effect. It typically covers adjustments to annual percentage rates, penalty fees, or payment calculations. Reviewing this document is essential to understand how your financial obligations evolve, ensuring you can manage debt effectively or opt to close the account before new, potentially higher costs are applied to your balance.

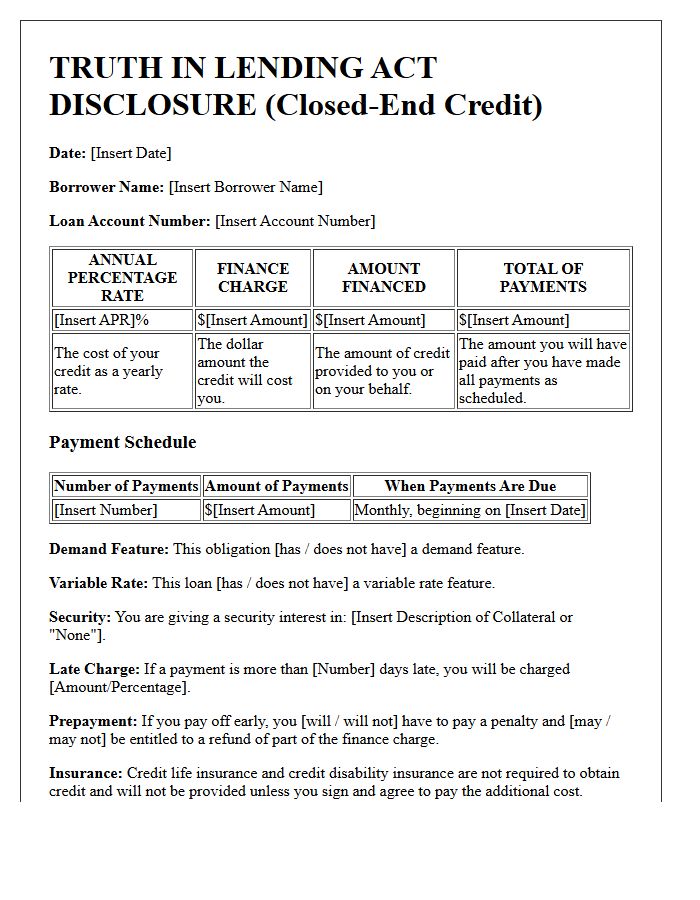

Closed-End Credit Truth in Lending Act Disclosure Letter

A Closed-End Credit Truth in Lending Act Disclosure Letter is a mandatory document ensuring transparency in fixed-term loans. Regulated by Regulation Z, it requires lenders to clearly state the Annual Percentage Rate (APR), total finance charges, amount financed, and total payments. This standardized disclosure protects consumers by allowing them to compare borrowing costs effectively. It must also detail the payment schedule, late fees, and prepayment penalties. Understanding these key figures helps borrowers evaluate the long-term financial commitment before signing a credit agreement, preventing hidden costs in mortgages or auto loans.

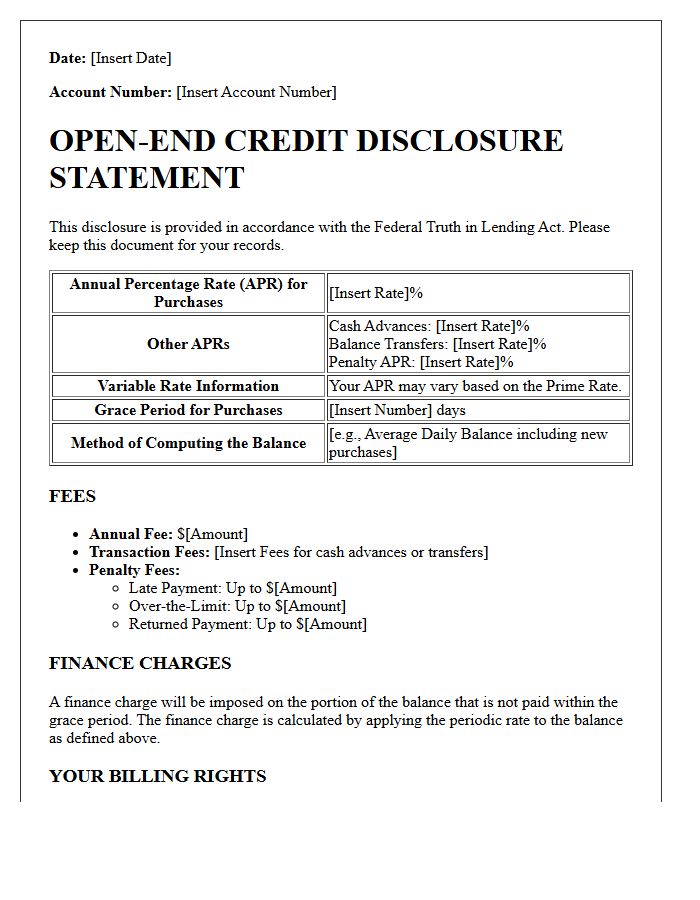

Open-End Credit Truth in Lending Act Disclosure Letter

An Open-End Credit Disclosure is a mandatory document required by the Truth in Lending Act (TILA). It ensures transparency by outlining critical financial terms before you use a revolving line of credit, such as a credit card. The letter must clearly state the Annual Percentage Rate (APR), periodic interest rates, and any applicable finance charges or membership fees. By standardizing how costs are presented, it allows consumers to compare offers effectively and understand their legal rights regarding billing errors and payment calculations.

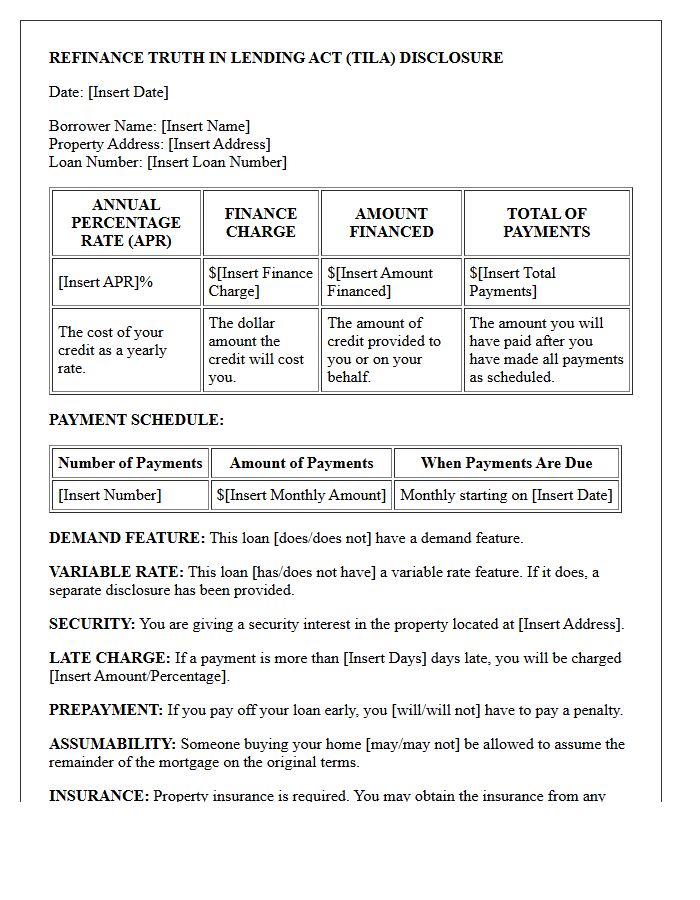

Refinance Truth in Lending Act Disclosure Letter

The Refinance Truth in Lending Act Disclosure is a mandatory document ensuring transparency in credit transactions. It highlights the Annual Percentage Rate (APR), which reflects the total cost of borrowing, including interest and fees. Borrowers must review the finance charge, total amount financed, and payment schedule to evaluate the loan's long-term affordability. Under federal law, this letter also grants a Right of Rescission, allowing homeowners three business days to cancel the refinance without penalty. Understanding these standardized terms protects consumers from hidden costs and predatory lending practices during the refinancing process.

What is a Truth in Lending Act (TILA) Disclosure Letter?

A TILA Disclosure Letter is a mandatory document provided by lenders that outlines the total cost of credit, including the annual percentage rate (APR), finance charges, the amount financed, and the total payment schedule to ensure transparency for the borrower.

What are the four primary disclosures required under the Truth in Lending Act?

The four critical pieces of information required are the Annual Percentage Rate (APR), the Finance Charge (the dollar amount the credit will cost), the Amount Financed (the amount of credit provided), and the Total of Payments (the sum of all payments made over the life of the loan).

When must a lender provide the TILA Disclosure to a borrower?

For most consumer loans, the disclosure must be provided before credit is extended. In the case of residential mortgage loans, a preliminary "Loan Estimate" containing these disclosures must be delivered within three business days of receiving the loan application.

Does a TILA Disclosure Letter include information about late payment fees?

Yes, the Truth in Lending Act requires lenders to disclose the consequences of late payments, including the specific dollar amount or the percentage-based formula used to calculate late fees.

What is the difference between the interest rate and the APR in a TILA Disclosure?

The interest rate is the percentage charged on the principal balance, while the APR represents the total annual cost of the loan, including both the interest rate and other prepaid finance charges or loan fees, providing a more accurate tool for comparing different loan offers.

Comments