A Risk-Based Pricing Notice is a mandatory disclosure sent to consumers when they are offered less favorable credit terms based on their credit reports. This legal requirement under the Fair Credit Reporting Act ensures transparency regarding how financial data impacts loan rates and insurance premiums. Understanding these notices helps consumers monitor their credit health. Below are some ready to use templates.

Image cover: Mastering Risk-Based Pricing Notices: Essential Templates and Compliance Samples

Letter Samples List

- Auto Loan Risk-Based Pricing Notice Letter

- Mortgage Loan Risk-Based Pricing Notice Letter

- Credit Card Approval Risk-Based Pricing Notice Letter

- Personal Installment Loan Risk-Based Pricing Notice Letter

- Home Equity Line of Credit Risk-Based Pricing Notice Letter

- Student Education Loan Risk-Based Pricing Notice Letter

- Tiered Pricing Method Risk-Based Pricing Notice Letter

- Account Review Risk-Based Pricing Notice Letter

- Credit Score Disclosure Exception Notice Letter

- Direct Auto Finance Risk-Based Pricing Notice Letter

- Retail Installment Contract Risk-Based Pricing Notice Letter

- Unsecured Credit Limit Risk-Based Pricing Notice Letter

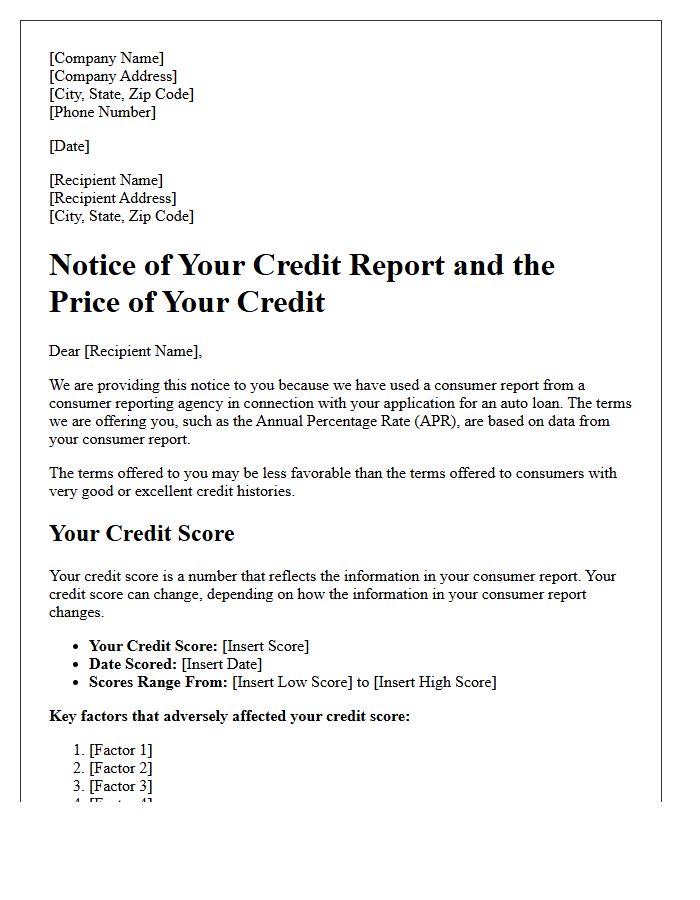

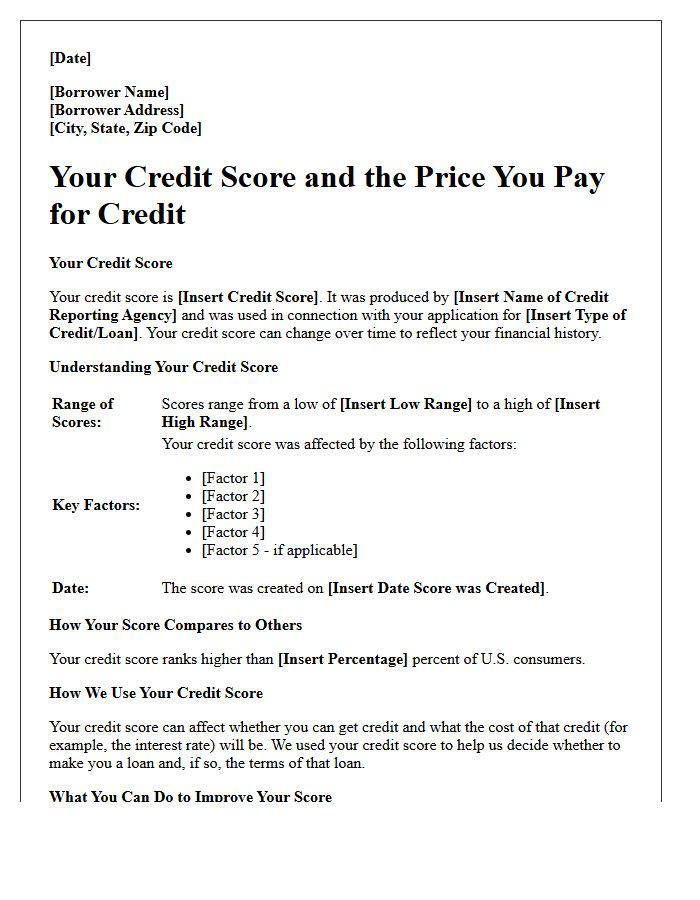

Auto Loan Risk-Based Pricing Notice Letter

An Auto Loan Risk-Based Pricing Notice is a legal disclosure sent when a lender offers you credit on less favorable terms than other consumers based on your credit report. This letter informs you that your credit score influenced the specific interest rate or loan conditions provided. It serves as a transparency tool, allowing you to verify the accuracy of your credit history and understand how financial behaviors impact borrowing costs. Receiving this notice provides a right to a free credit report to ensure your profile is error-free.

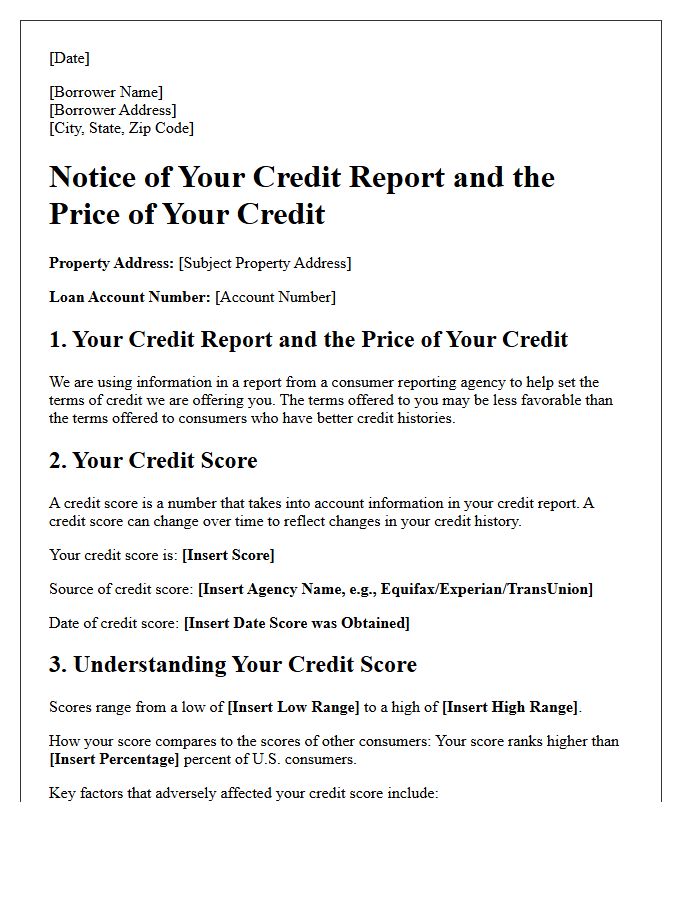

Mortgage Loan Risk-Based Pricing Notice Letter

A Mortgage Loan Risk-Based Pricing Notice is a mandatory disclosure sent when a lender offers less favorable terms based on your credit report. This letter is crucial because it informs you that your credit score directly influenced the interest rate or loan costs provided. It serves as a transparency tool, allowing you to verify the accuracy of your financial data and understand how your creditworthiness impacts borrowing power. Always review this document to identify potential errors in your credit history that could be negatively affecting your mortgage pricing.

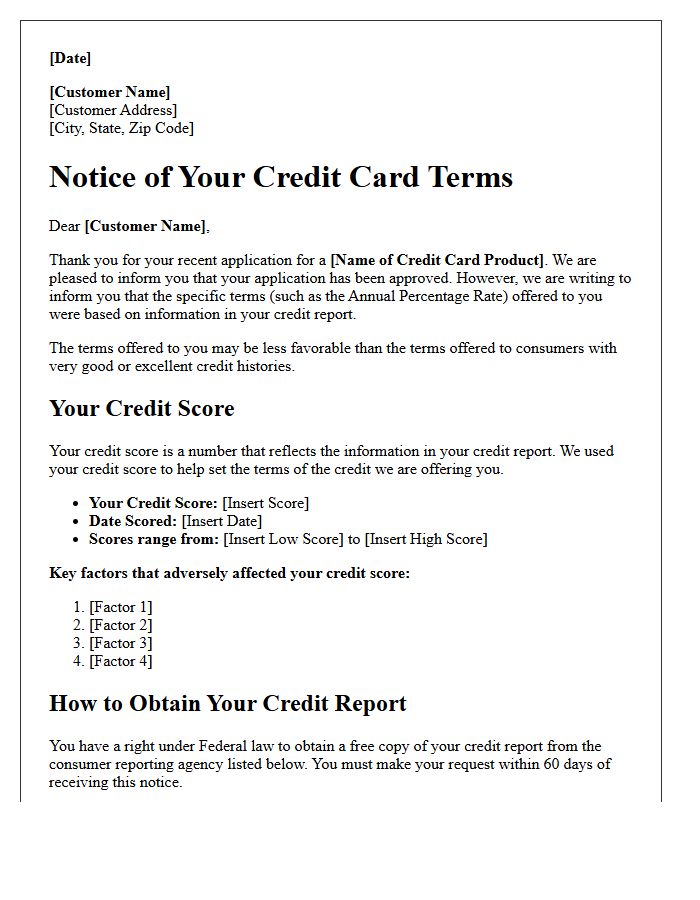

Credit Card Approval Risk-Based Pricing Notice Letter

A Risk-Based Pricing Notice is a legal document lenders must send when offering you credit on less favorable terms than other consumers. This typically happens if your credit report contains negative information, leading to higher interest rates. The letter aims to inform you how your creditworthiness influenced the decision, providing transparency under federal law. It includes your credit score used for the evaluation and instructions on how to obtain a free report to verify accuracy. Understanding this notice helps you identify potential errors and improve your financial profile for better future rates.

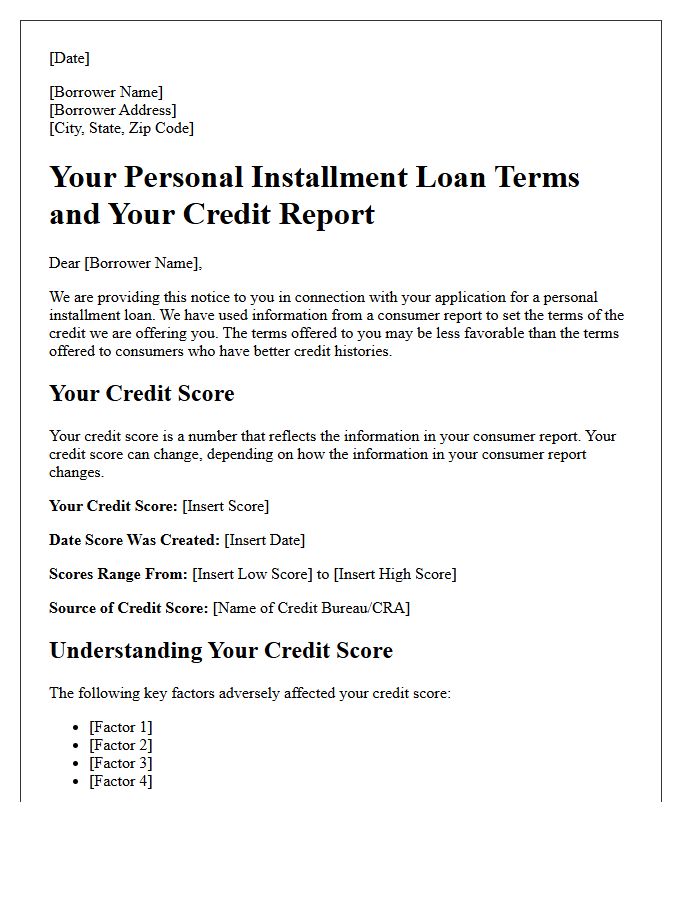

Personal Installment Loan Risk-Based Pricing Notice Letter

A Personal Installment Loan Risk-Based Pricing Notice is a mandatory letter sent when a lender offers you credit on less favorable terms than other consumers. This typically occurs because information in your credit report indicates a higher risk profile. The Risk-Based Pricing Notice must include your credit score, how it compares to others, and the specific factors that influenced the lender's decision. Receiving this notice does not mean you were denied; rather, it explains why you did not qualify for the best available interest rates or lowest fees.

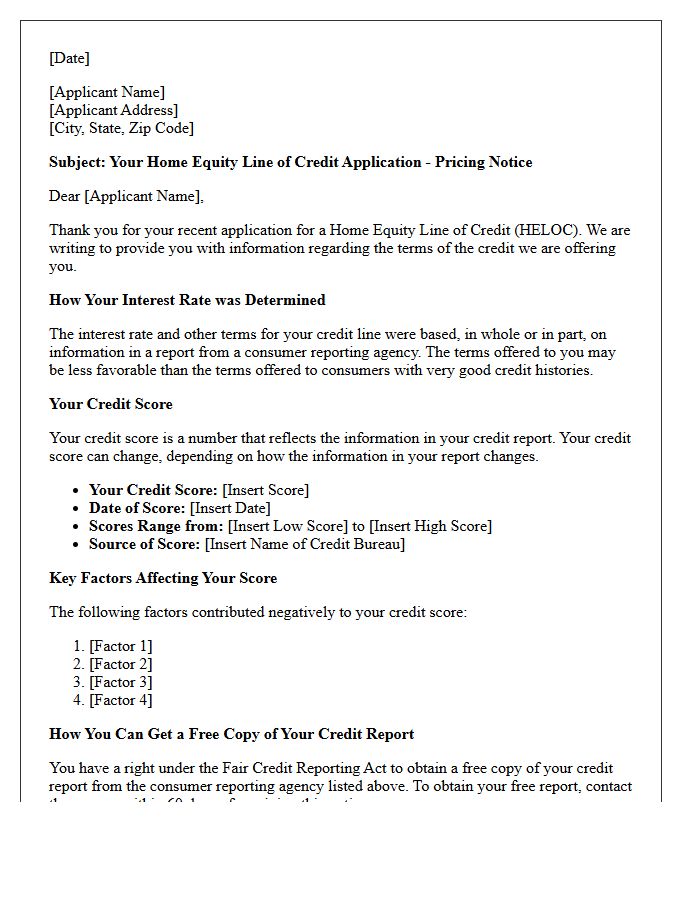

Home Equity Line of Credit Risk-Based Pricing Notice Letter

A Home Equity Line of Credit (HELOC) Risk-Based Pricing Notice is a mandatory letter sent when a lender offers you less favorable loan terms based on your credit report. This document explains that your specific credit history, including your score and debt-to-income ratio, influenced the interest rate or credit limit provided. It is a critical transparency tool that allows you to verify the accuracy of your financial data. If you receive this notice, you are entitled to a free copy of your credit report to check for potential errors or identity theft.

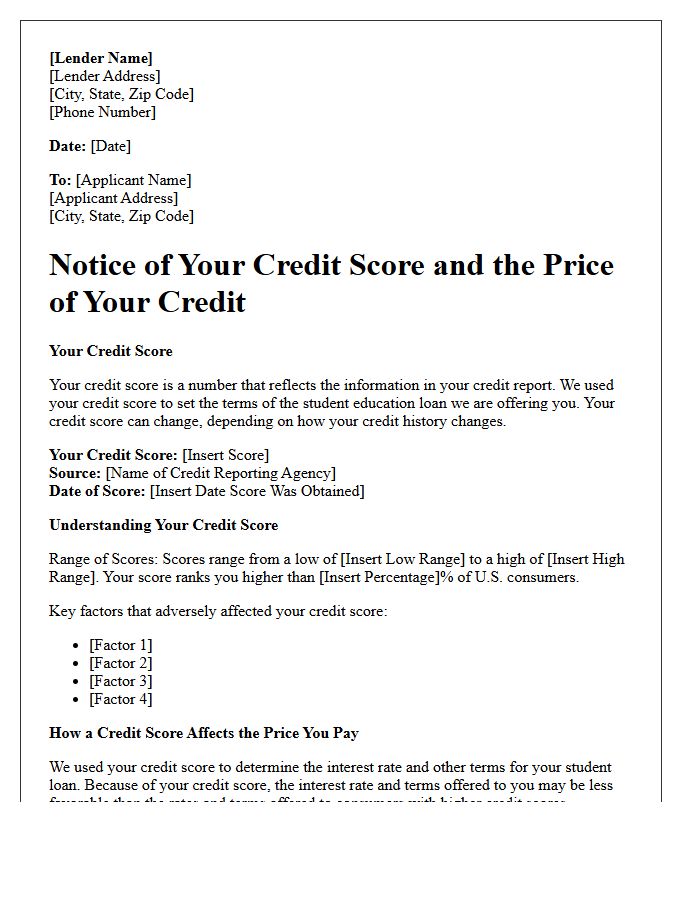

Student Education Loan Risk-Based Pricing Notice Letter

A Student Education Loan Risk-Based Pricing Notice is a mandatory letter sent when your credit report influences the terms of your financing. It informs you that the interest rate or loan conditions offered are less favorable than those given to applicants with superior credit scores. This document is essential because it highlights how your creditworthiness directly impacts your borrowing costs. It provides your specific credit score, the range of possible scores, and instructions on how to obtain a free credit report to verify information accuracy or dispute potential errors affecting your rates.

Tiered Pricing Method Risk-Based Pricing Notice Letter

A Tiered Pricing Method Risk-Based Pricing Notice is a mandatory disclosure sent to consumers when their credit report results in less favorable loan terms. Under the FCRA, lenders must inform applicants if they are placed in a higher-priced tier compared to others. This letter provides transparency, showing the consumer's credit score and how it influenced the final interest rate. Understanding this notice is crucial for identifying potential reporting errors and improving financial standing to qualify for better rates in the future.

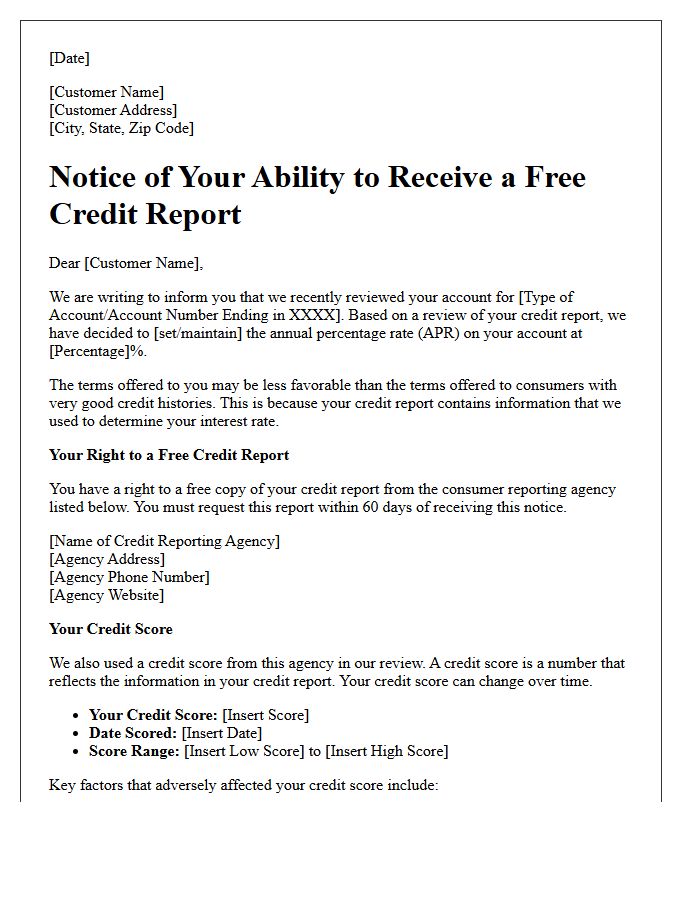

Account Review Risk-Based Pricing Notice Letter

An Account Review Risk-Based Pricing Notice is a legal disclosure sent when a creditor reviews your existing credit line and increases your interest rate based on a decline in your creditworthiness. Unlike standard notices, this specific letter informs you that your credit score or report data triggered less favorable terms during a periodic review. Key elements include your current score, the factors negatively impacting it, and your right to a free credit report to verify accuracy and contest potential errors influencing the rate hike.

Credit Score Disclosure Exception Notice Letter

A Credit Score Disclosure Exception Notice is a mandatory document sent by lenders when they use your credit data to offer less favorable terms than those given to others. This Risk-Based Pricing notice ensures transparency in the lending process. It provides your current credit score, the source agency, and how your ranking compares to other consumers. The most important thing to know is that this letter grants you the right to a free credit report, allowing you to verify accuracy and dispute potential errors that may be negatively impacting your financial standing.

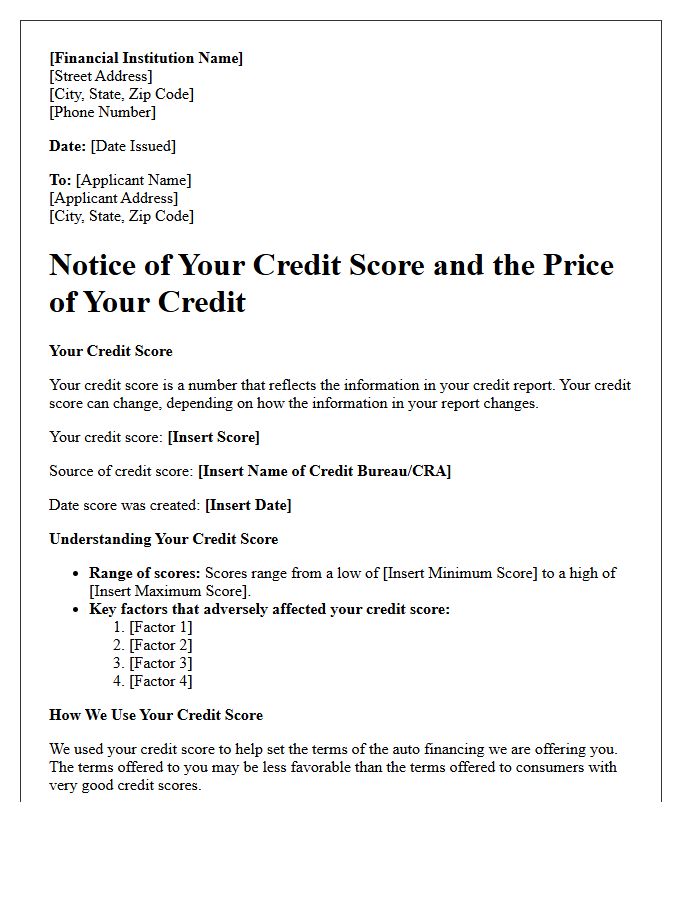

Direct Auto Finance Risk-Based Pricing Notice Letter

A Direct Auto Finance Risk-Based Pricing Notice is a mandatory disclosure sent when a lender offers you credit terms less favorable than those given to other consumers based on your credit report. This letter is crucial because it informs you that your credit history influenced the higher annual percentage rate (APR) or costs assigned to your loan. It provides your credit score and details on how to obtain a free report to verify accuracy, ensuring transparency in the lending process and protecting your rights under federal law.

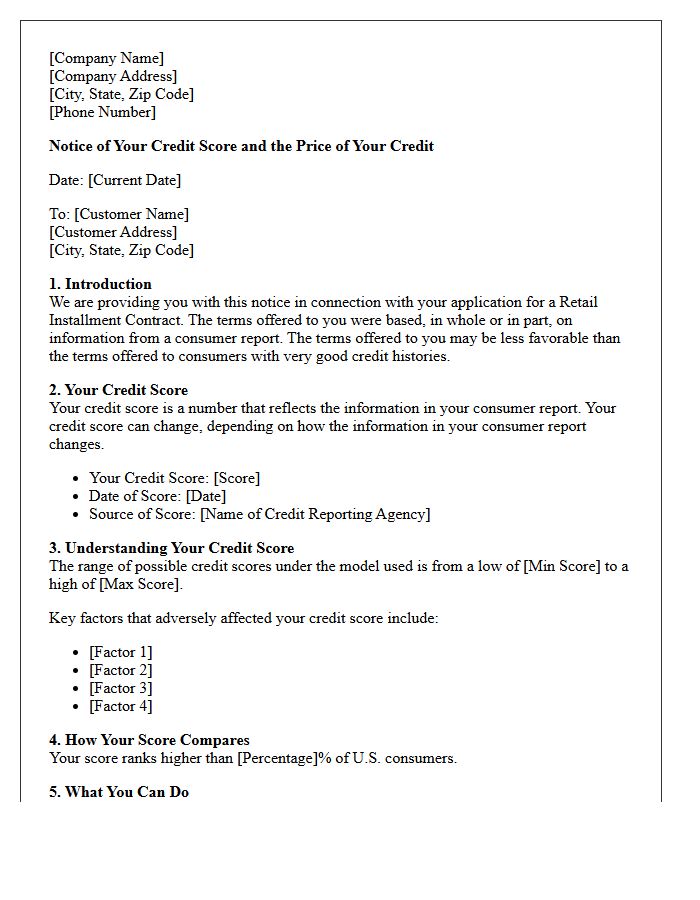

Retail Installment Contract Risk-Based Pricing Notice Letter

A Retail Installment Contract Risk-Based Pricing Notice is a mandatory disclosure sent to consumers when their credit report results in less favorable financing terms than those offered to others. This document highlights that your credit score significantly influenced the specific interest rate or terms provided in the sales agreement. Under federal law, lenders must provide this notice to ensure transparency and inform you of your right to obtain a free credit report to verify data accuracy and address potential errors that may impact your financial standing.

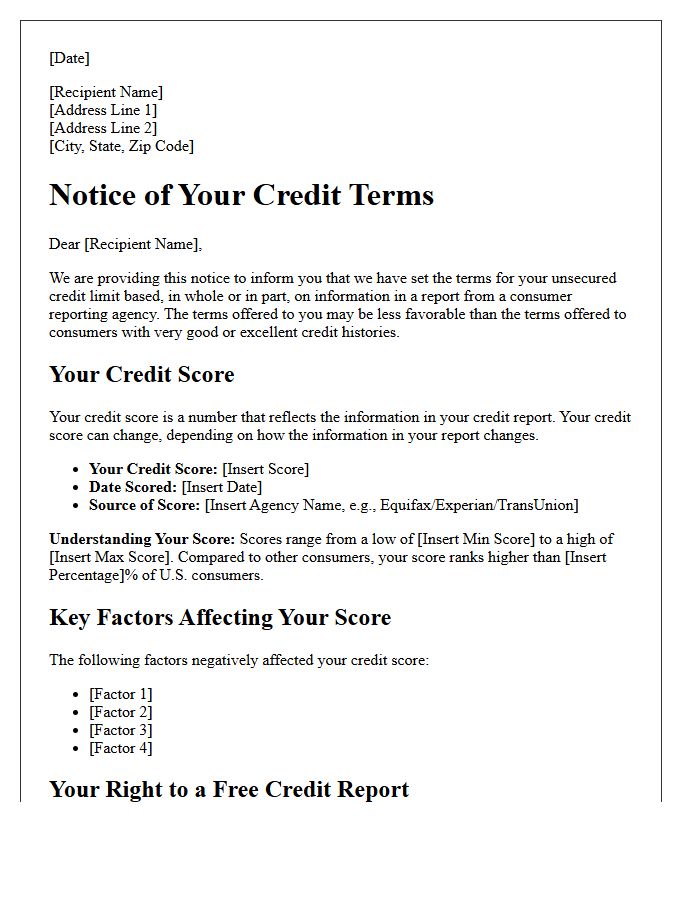

Unsecured Credit Limit Risk-Based Pricing Notice Letter

An Unsecured Credit Limit Risk-Based Pricing Notice is a mandatory disclosure sent when a lender grants a credit line with less favorable terms than those offered to other consumers. This typically happens because your credit score or financial profile indicates a higher risk level. The letter must explain the specific factors from your credit report that influenced the decision, such as payment history or debt-to-income ratio. Reviewing this document helps you understand how your creditworthiness affects your interest rates and provides an opportunity to correct potential reporting errors.

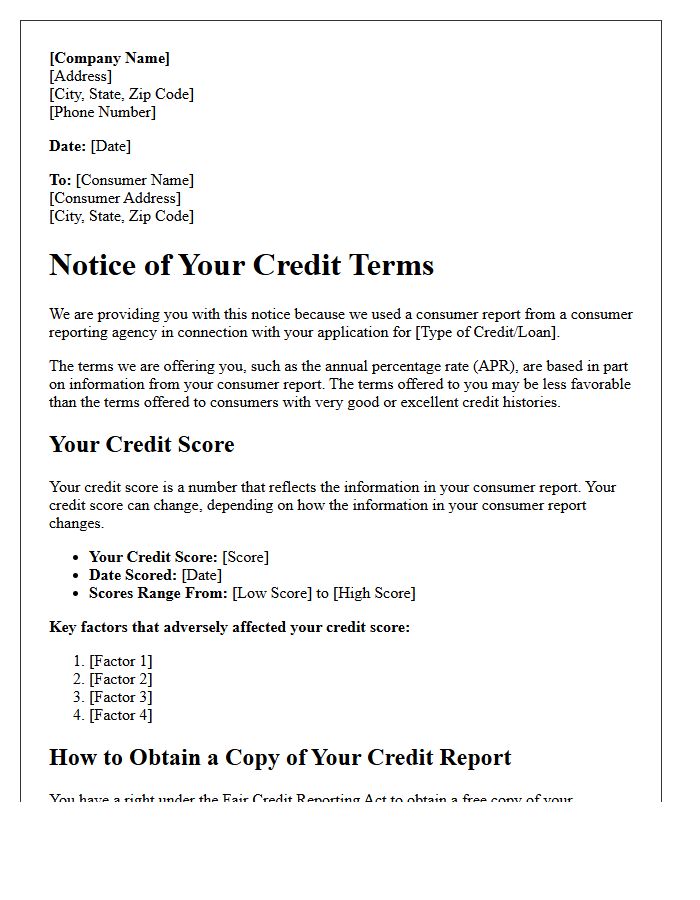

What is a Risk-Based Pricing Notice Letter?

A Risk-Based Pricing Notice is a letter sent by lenders to consumers who are granted credit on terms less favorable than those offered to other consumers. This notice is required under the Fair Credit Reporting Act (FCRA) when a lender uses information from a credit report to set higher interest rates or less attractive loan terms.

Why did I receive a Risk-Based Pricing Notice?

You received this notice because the creditor used your credit score or credit history to determine the terms of your loan, and those terms are less favorable than the best terms available to a substantial portion of other customers. Receiving this letter does not mean your application was denied; it simply explains that your credit profile influenced the pricing of your credit offer.

Does receiving this notice negatively affect my credit score?

No, receiving a Risk-Based Pricing Notice does not impact your credit score. The letter is a mandatory disclosure intended to inform you about how your credit data was used. It is a tool for consumer transparency and does not constitute a hard inquiry or a negative mark on your credit report.

What information is included in a Risk-Based Pricing Notice?

The letter must include your credit score, the range of possible scores under the model used, the key factors that adversely affected your score, and the name of the credit bureau that provided the data. It also includes instructions on how to obtain a free copy of your credit report to check for inaccuracies.

What should I do after receiving a Risk-Based Pricing Notice Letter?

Upon receiving the notice, you should review the specific factors that impacted your credit score. You are entitled to a free copy of your credit report from the bureau listed in the letter. You should use this opportunity to verify that all reported information is accurate and dispute any errors that may be causing you to pay higher interest rates.

Comments