A Notice of Postponement of Foreclosure Sale is a formal legal document that officially delays a scheduled property auction to a later date. This delay can occur due to borrower negotiations, legal requirements, or procedural changes. Understanding this notice is vital for homeowners seeking to save their equity. To help you draft one, below are some ready to use template.

Image cover: Official Notice of Postponement of Foreclosure Sale: Professional Templates and Examples

Letter Samples List

- Notice of Postponement of Foreclosure Sale Letter for Residential Property

- Commercial Real Estate Foreclosure Sale Postponement Letter

- Mutual Agreement Foreclosure Postponement Notice Letter

- Borrower Requested Foreclosure Postponement Letter

- Bank Initiated Foreclosure Sale Postponement Letter

- Loss Mitigation Review Foreclosure Postponement Letter

- Bankruptcy Automatic Stay Foreclosure Postponement Letter

- Short Sale Pending Foreclosure Postponement Letter

- Loan Modification Trial Foreclosure Postponement Letter

- Administrative Delay Foreclosure Sale Postponement Letter

- State of Emergency Foreclosure Postponement Letter

- Deed in Lieu Processing Foreclosure Postponement Letter

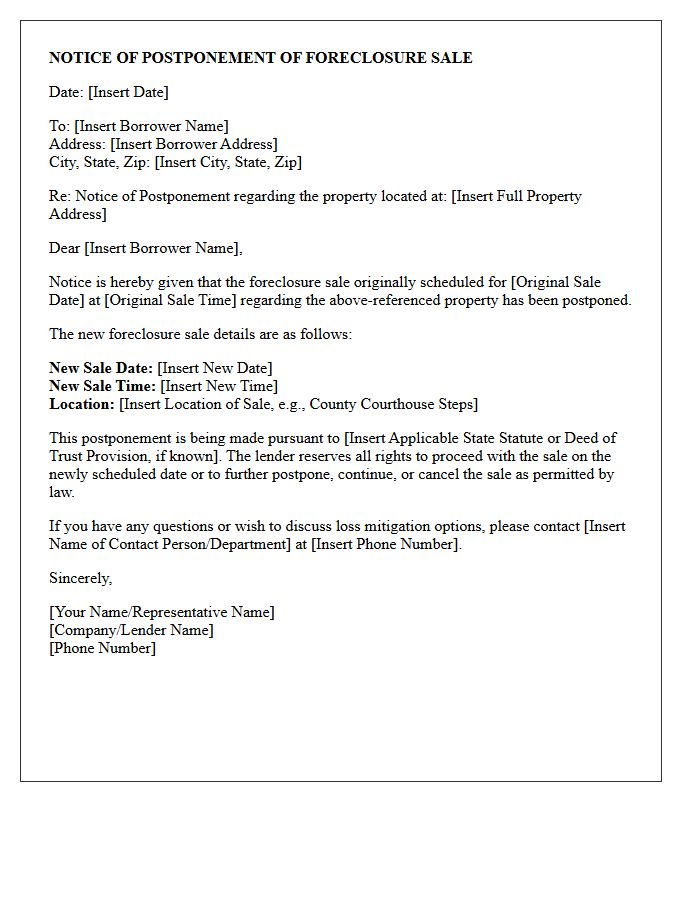

Notice of Postponement of Foreclosure Sale Letter for Residential Property

A Notice of Postponement is a formal legal document informing borrowers that a scheduled foreclosure auction has been delayed to a later date. This letter typically specifies the original sale date and the newly rescheduled time. It is a critical communication because it provides homeowners additional time to explore loss mitigation options, such as a loan modification, short sale, or repayment plan. Receiving this notice does not cancel the foreclosure process; it merely pauses it, meaning the lender retains the right to proceed unless a permanent resolution is reached.

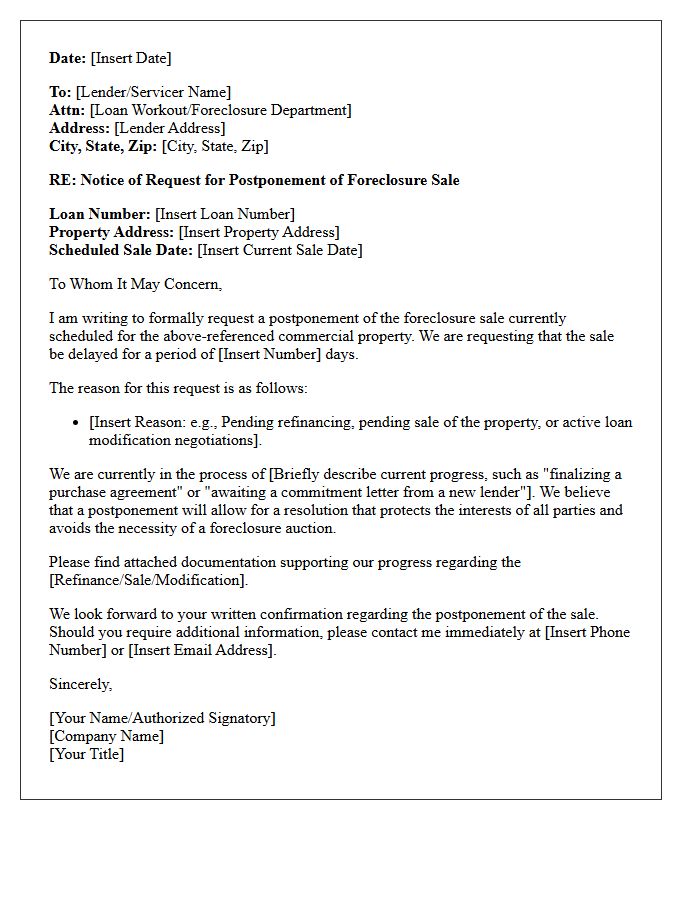

Commercial Real Estate Foreclosure Sale Postponement Letter

A Foreclosure Sale Postponement Letter is a formal request sent to a lender or trustee to delay the auction of a commercial property. To be effective, the borrower must demonstrate a viable workout plan, such as a pending refinance, an active purchase contract, or a restructuring agreement. Timely submission is critical to pause legal proceedings and provide additional time to cure defaults. This document serves as a vital negotiation tool to preserve equity and prevent the permanent loss of commercial assets through the foreclosure process.

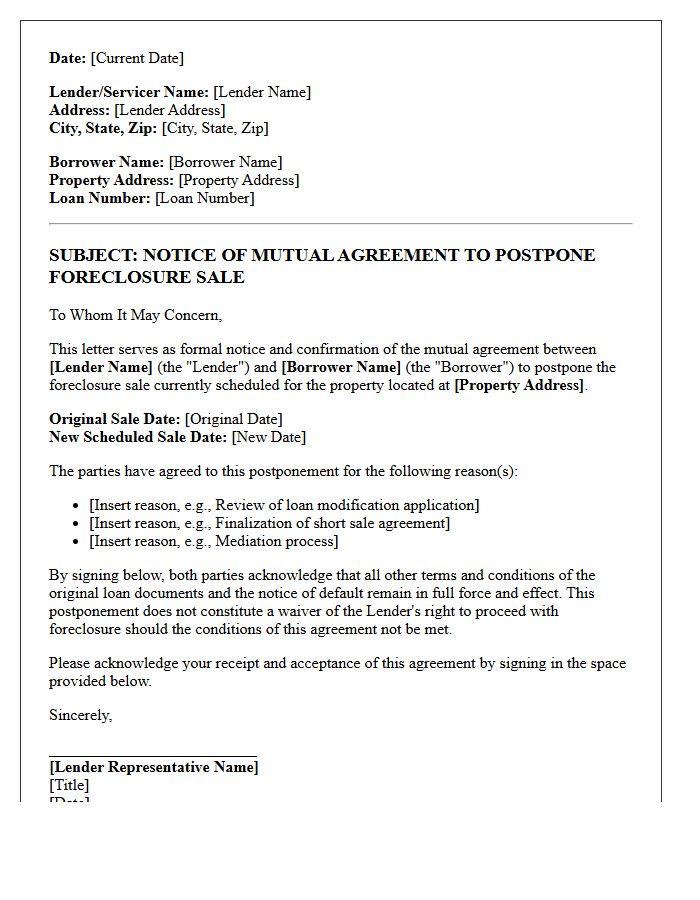

Mutual Agreement Foreclosure Postponement Notice Letter

A Mutual Agreement Foreclosure Postponement Notice Letter is a formal legal document used when a lender and borrower agree to delay a scheduled trustee sale. This written notice serves as critical evidence that both parties have consented to pause legal proceedings, often to finalize a loan modification or short sale. It is essential to ensure this agreement is recorded properly to prevent accidental property loss. Homeowners must verify that the new sale date is clearly specified to maintain legal protections and avoid foreclosure during active negotiations.

Borrower Requested Foreclosure Postponement Letter

A Borrower Requested Foreclosure Postponement Letter is a formal written appeal sent to a lender to delay a trustee sale. This document is essential for homeowners seeking loss mitigation options, such as a loan modification or short sale. To be effective, the letter should clearly state the reason for financial hardship and provide a specific timeframe for resolution. Timely submission is critical, as most states require these requests well before the scheduled auction date to legally halt proceedings and protect your property rights.

Bank Initiated Foreclosure Sale Postponement Letter

A Bank Initiated Foreclosure Sale Postponement Letter is a formal notification confirming that the lender has voluntarily delayed a scheduled auction. This legal notice officially halts immediate foreclosure proceedings, providing a temporary reprieve for the homeowner. Reasons for such delays often include ongoing loan modification reviews, short sale negotiations, or procedural compliance requirements. It is crucial for borrowers to understand that while the sale date is pushed back, the underlying debt remains. Homeowners should utilize this additional time to finalize loss mitigation options and prevent the eventual loss of their property.

Loss Mitigation Review Foreclosure Postponement Letter

A Loss Mitigation Review Foreclosure Postponement Letter is a formal notice confirming that your lender has paused the foreclosure sale to evaluate your application for mortgage assistance. This legal protection, often required by RESPA regulations, prevents "dual tracking" while your file is under review. Receiving this letter ensures your home cannot be auctioned until a final decision is reached or the review period expires. Homeowners should verify the specific postponement date mentioned to ensure their rights are protected during the loan modification process.

Bankruptcy Automatic Stay Foreclosure Postponement Letter

A bankruptcy automatic stay is a powerful legal injunction that halts all collection activities, including home foreclosure. Once you file for bankruptcy, the court issues this stay to provide immediate relief. To ensure your lender complies, you must send a formal foreclosure postponement letter notifying them of your case number. This written notice legally obligates the mortgage servicer to stop the sale process immediately. This strategic move buys essential time to reorganize your finances or negotiate a loan modification while protecting your property from immediate loss under federal law.

Short Sale Pending Foreclosure Postponement Letter

A Short Sale Pending Foreclosure Postponement Letter is a formal request sent to a mortgage servicer to delay an auction date. It informs the lender that a binding sales contract exists, requiring additional time to finalize the transaction. Including a signed purchase agreement and a pre-approval letter is essential to prove the sale's viability. This document serves as a critical tool to prevent immediate loss of the home while ensuring the lender recovers more value than a traditional foreclosure sale would typically provide.

Loan Modification Trial Foreclosure Postponement Letter

A Loan Modification Trial Foreclosure Postponement Letter is a formal document confirming that your lender has paused legal action. This legal stay is granted because you have entered a temporary trial payment plan. It is crucial to understand that the foreclosure process is only deferred, not cancelled. You must make every trial payment on time and provide all requested documentation to secure a permanent modification. Failure to meet these specific terms allows the bank to immediately resume the sale of your property without further notice.

Administrative Delay Foreclosure Sale Postponement Letter

An Administrative Delay Foreclosure Sale Postponement Letter is a formal notification issued by a lender or servicer to pause an auction due to internal processing errors or legal compliance issues. This document serves as official evidence that the scheduled sale date is no longer active. Borrowers should use this legal stay to seek mediation or loan modification. Understanding this procedural freeze is critical because it provides a temporary window to resolve delinquency and prevent the final loss of property ownership through a rescheduled trustee sale.

State of Emergency Foreclosure Postponement Letter

A State of Emergency Foreclosure Postponement Letter is a legal document used to halt foreclosure proceedings during government-declared crises. Homeowners must submit this request to their lender to invoke emergency protections or temporary moratoriums that prevent the loss of property. This letter typically cites specific state or federal mandates designed to provide financial relief during disasters. It is essential to include your loan number and evidence of hardship to ensure the legal stay is properly applied to your mortgage account while the emergency declaration remains in effect.

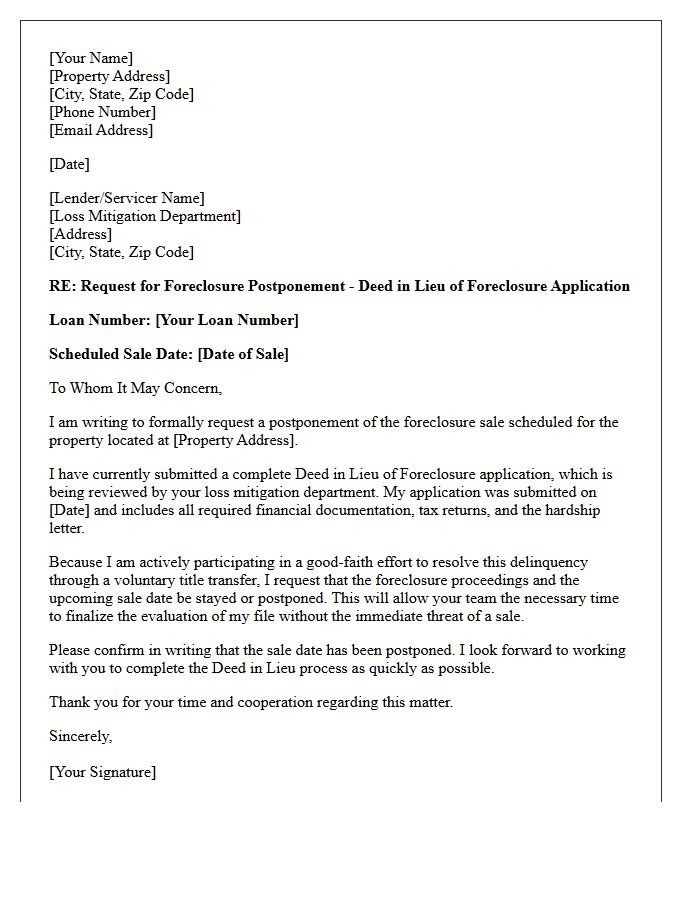

Deed in Lieu Processing Foreclosure Postponement Letter

A Deed in Lieu Processing Foreclosure Postponement Letter is a formal request sent to lenders to suspend legal sale dates while evaluating a voluntary property transfer. This document provides the necessary time to finalize paperwork, helping homeowners avoid a formal foreclosure on their credit report. To be effective, the letter must include the specific loan number and proof that a complete application package is under review. Timely submission is critical to ensure the foreclosure stay is granted before the scheduled auction occurs, protecting the borrower's future financial eligibility.

What is a Notice of Postponement of Foreclosure Sale?

A Notice of Postponement is a formal legal document that officially delays a scheduled trustee sale or foreclosure auction to a later date or time. This notice must be announced publicly at the original time and location of the sale to maintain the legal validity of the foreclosure process.

What are the most common reasons for a foreclosure postponement?

Foreclosure sales are typically postponed due to a mutual agreement between the lender and borrower, the filing of a Chapter 7 or Chapter 13 bankruptcy, a pending loan modification application, or a legal requirement to correct errors in the original filing process.

How can a homeowner find out if a foreclosure sale has been postponed?

Homeowners can verify a postponement by contacting the trustee listed on the Notice of Sale, checking the county recorder's office website, or attending the auction site where the trustee must publicly announce the new date and time of the sale.

How many times can a lender postpone a foreclosure sale?

The number of allowed postponements varies by state law; however, many jurisdictions allow a lender to postpone a sale multiple times. In some states, if the sale is postponed beyond a specific timeframe (such as 365 days), a new Notice of Sale must be recorded and mailed.

Does a Notice of Postponement stop the foreclosure process permanently?

No, a Notice of Postponement only delays the auction. It does not cancel the foreclosure or resolve the underlying debt. To permanently stop the foreclosure, the homeowner must typically reinstate the loan, complete a successful loan modification, sell the property, or reach a settlement with the lender.

Comments