Islamic finance utilizes Kafalah as a Sharia-compliant guarantee mechanism where a guarantor assumes liability for a third party's obligations. This ensures ethical risk management and financial security in commercial transactions. Understanding its legal framework is essential for businesses seeking interest-free alternatives to traditional bank guarantees. To help you get started, below are some ready to use template.

Image cover: Professional Islamic Finance Kafalah Guarantee Letter Templates and Samples

Letter Samples List

- Kafalah Bid Bond Guarantee Letter

- Kafalah Performance Bond Guarantee Letter

- Kafalah Advance Payment Guarantee Letter

- Kafalah Financial Obligation Guarantee Letter

- Kafalah Shipping Guarantee Letter

- Kafalah Retention Money Guarantee Letter

- Kafalah Maintenance Period Guarantee Letter

- Kafalah Customs Clearance Guarantee Letter

- Kafalah Deferred Payment Guarantee Letter

- Kafalah Trade Facility Guarantee Letter

- Kafalah Corporate Credit Guarantee Letter

- Kafalah Supply Contract Guarantee Letter

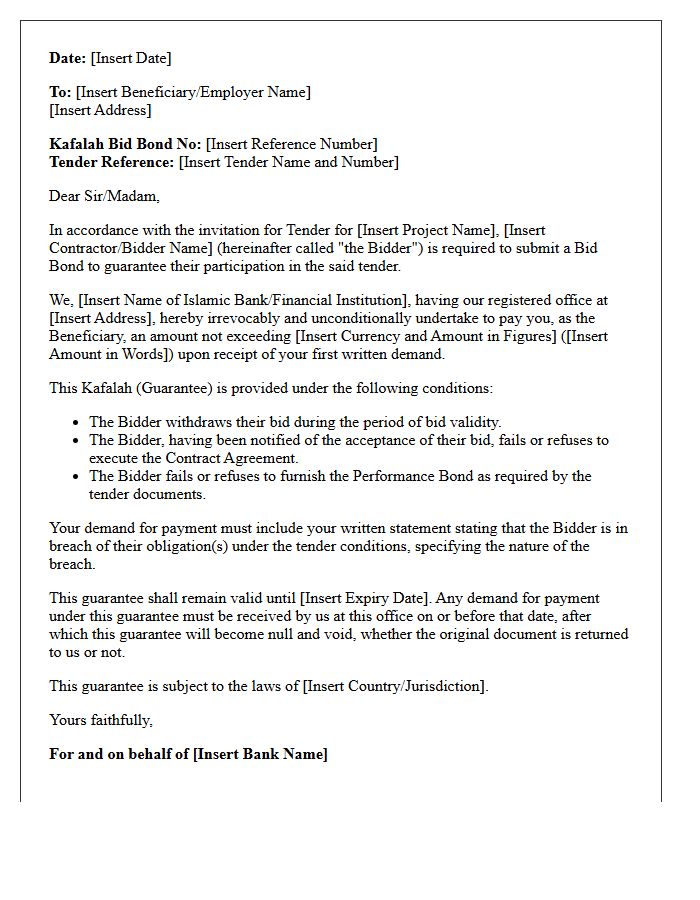

Kafalah Bid Bond Guarantee Letter

A Kafalah Bid Bond Guarantee Letter is a Shariah-compliant financial instrument used in competitive tendering. Issued by a bank, it provides a guarantee that a contractor will honor their bid and sign the contract if selected. Unlike conventional bonds based on interest, Kafalah operates on the Islamic principle of suretyship, where the bank acts as a guarantor for the bidder's obligations. This document protects project owners from financial loss during the procurement process while ensuring full compliance with ethical Islamic finance standards.

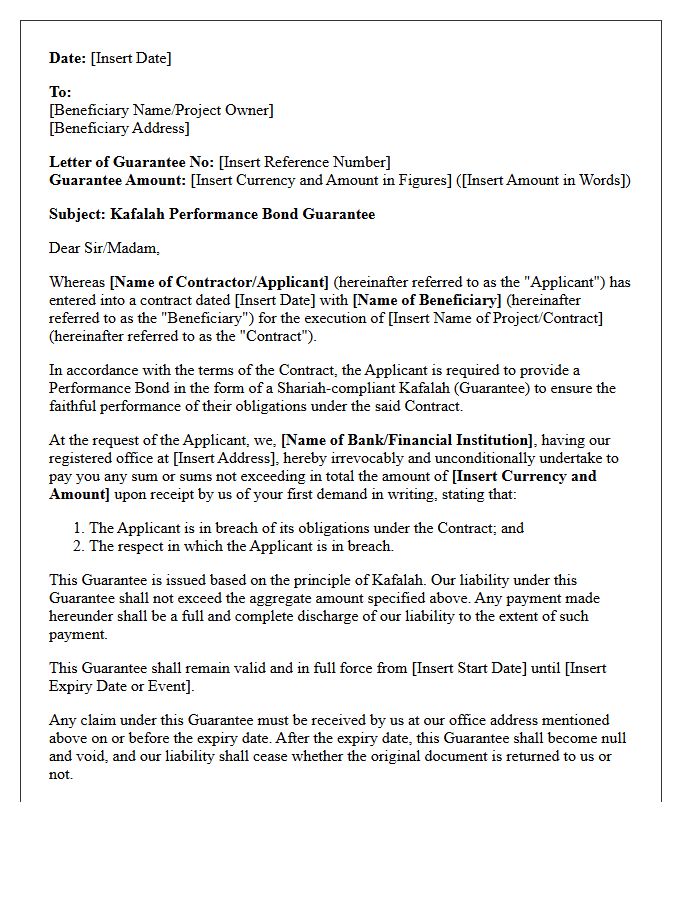

Kafalah Performance Bond Guarantee Letter

A Kafalah Performance Bond Guarantee Letter is a Shariah-compliant security issued by a financial institution to ensure a contractor fulfills their contractual obligations. Under the Kafalah concept, the guarantor assumes responsibility if the party fails to deliver agreed services. It protects the project owner against financial loss due to non-performance or breach of contract. This Islamic finance alternative to conventional bonds provides a legally binding commitment, ensuring projects are completed according to specified terms while maintaining ethical compliance and financial security for all stakeholders involved in the agreement.

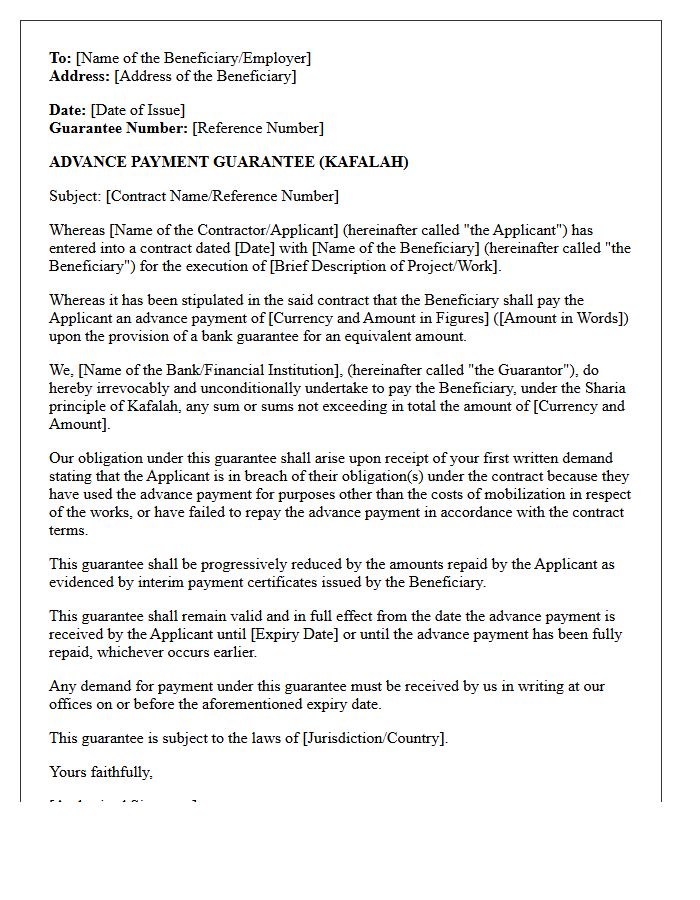

Kafalah Advance Payment Guarantee Letter

A Kafalah Advance Payment Guarantee is a Sharia-compliant instrument issued by a financial institution to secure funds paid upfront to a contractor. It ensures that the project owner can recover the disbursed amount if the provider fails to fulfill contractual obligations. Based on the principle of guaranty, it replaces interest-based models with ethical risk-sharing. This document is essential for maintaining cash flow in construction and supply sectors while providing legal protection against non-performance, ensuring that advance payments are utilized strictly for the intended project milestones.

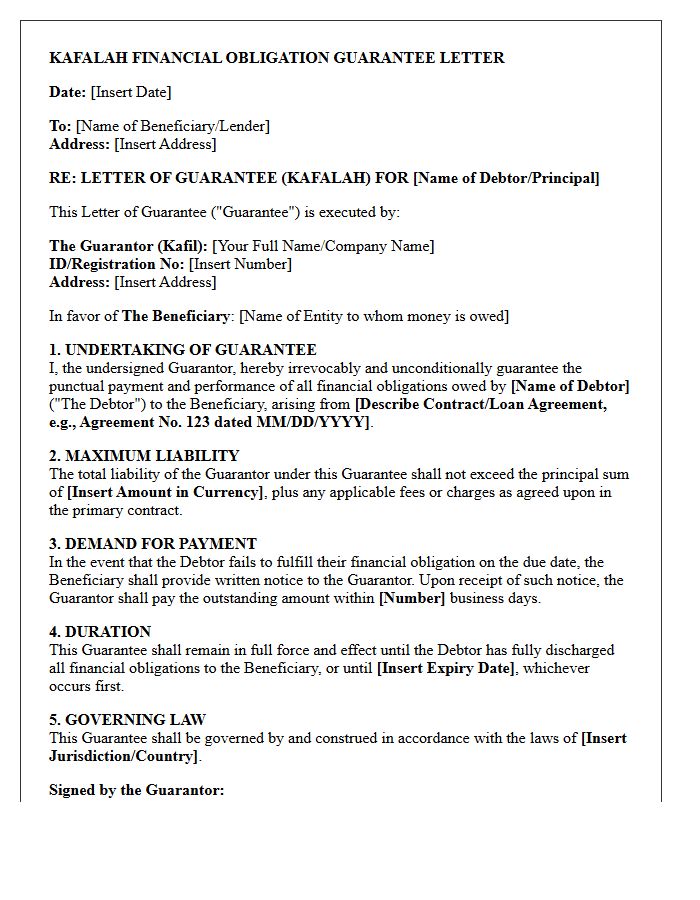

Kafalah Financial Obligation Guarantee Letter

A Kafalah Financial Obligation Guarantee Letter is a legal commitment issued by a guarantor to ensure a debtor fulfills their financial liabilities. This instrument provides creditors with security against potential defaults, facilitating trust in commercial transactions and Sharia-compliant financing. By utilizing this guarantee, businesses can access credit or contracts that require third-party assurance of payment. Understanding the terms is essential, as the guarantor becomes legally responsible for the debt if the primary party fails to pay, ensuring repayment certainty for the beneficiary.

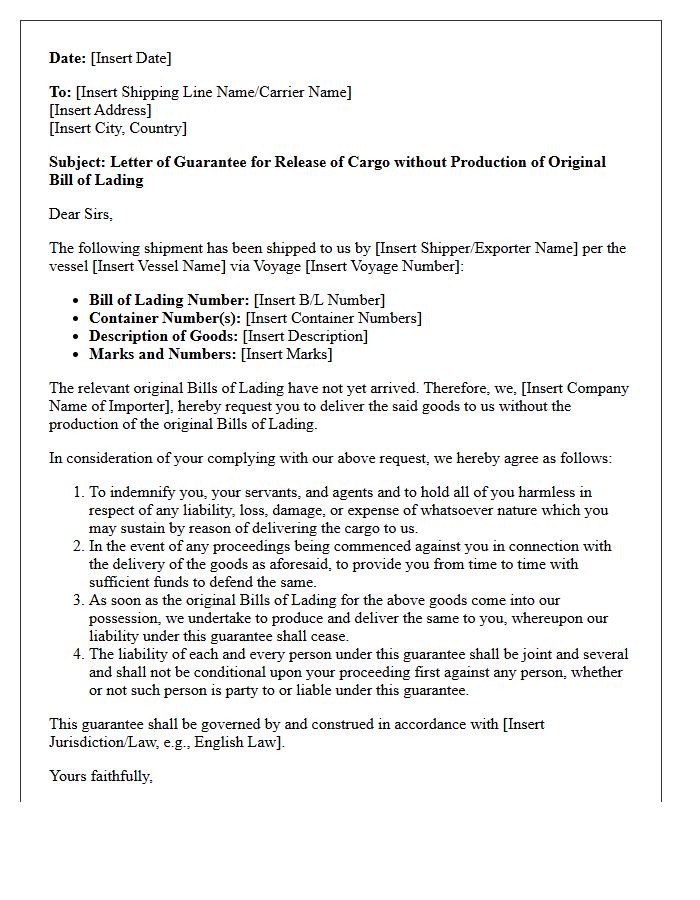

Kafalah Shipping Guarantee Letter

A Kafalah Shipping Guarantee Letter is a Shariah-compliant instrument used in Islamic trade finance to facilitate the immediate release of goods when the bill of lading is delayed. Under the principle of Kafalah (suretyship), the bank acts as a guarantor, indemnifying the shipping carrier against potential liabilities. This arrangement prevents costly demurrage charges at the port and ensures seamless supply chain operations. It effectively bridges the gap between the arrival of cargo and the receipt of official title documents, maintaining commercial efficiency while adhering to ethical financial standards.

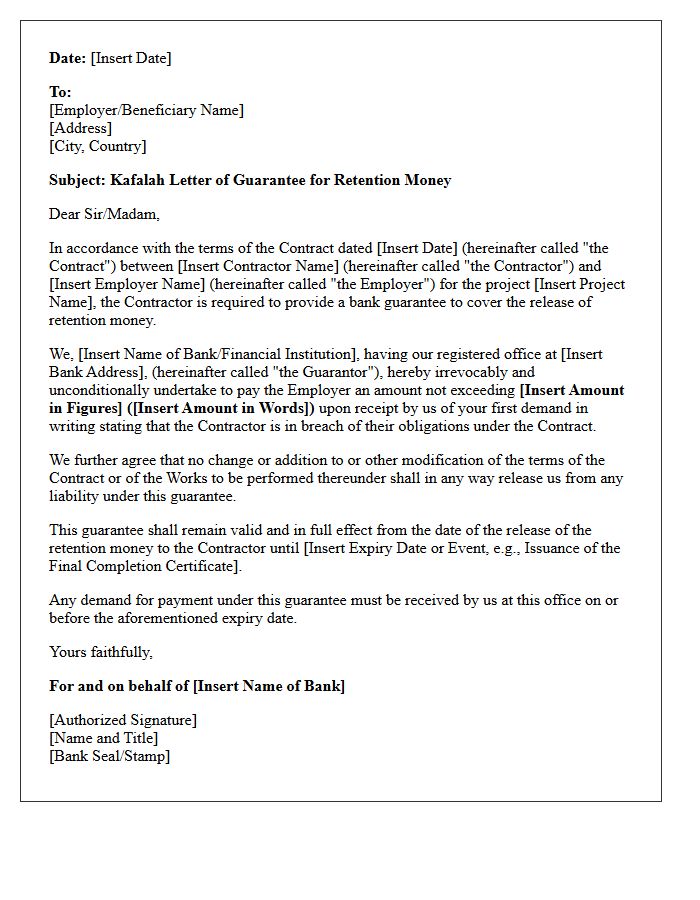

Kafalah Retention Money Guarantee Letter

A Kafalah Retention Money Guarantee Letter acts as a financial security instrument in construction contracts. It allows contractors to receive their full retention funds early, rather than waiting for the defects liability period to end. By substituting withheld cash with this bank-backed guarantee, firms significantly improve their liquidity and working capital. This ensures the employer remains protected against potential workmanship issues while providing the contractor with immediate cash flow to fund ongoing project operations and resources efficiently.

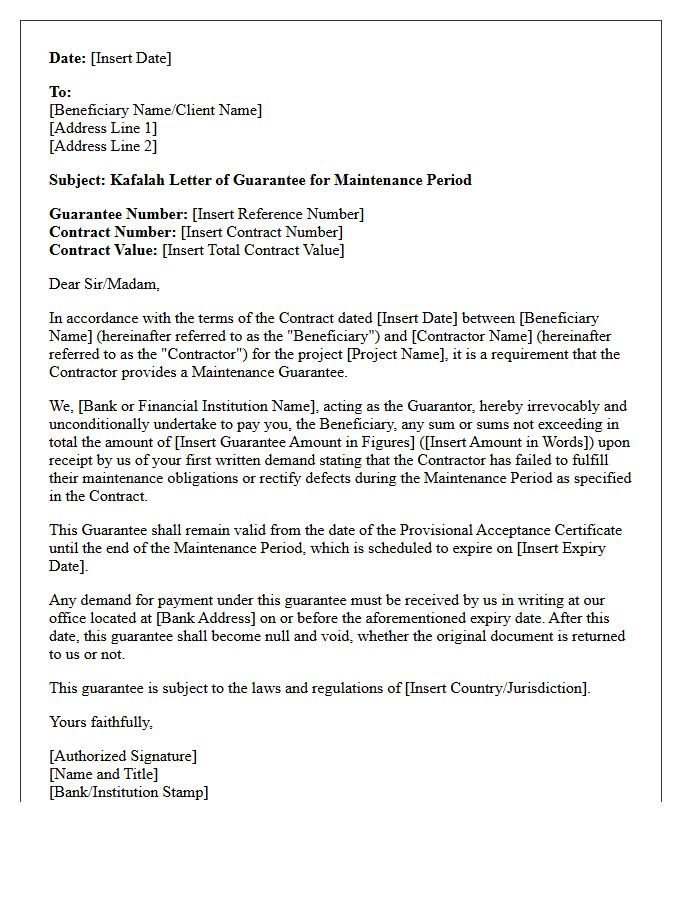

Kafalah Maintenance Period Guarantee Letter

A Kafalah Maintenance Period Guarantee Letter is a formal commitment issued by a financial institution to ensure a contractor fulfills rectification obligations after project completion. It protects the employer against defects or poor workmanship discovered during the maintenance phase. If the contractor fails to fix identified issues, the guarantee provides financial compensation to cover repair costs. This instrument is essential for risk mitigation in construction contracts, ensuring long-term project quality and compliance with agreed specifications before the final release of retention sums.

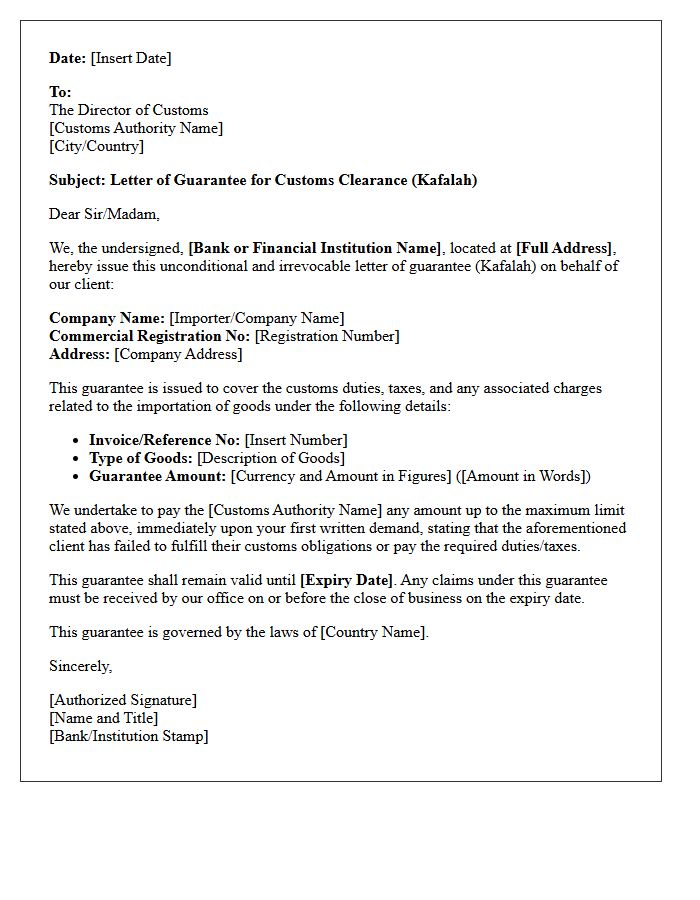

Kafalah Customs Clearance Guarantee Letter

A Kafalah Customs Clearance Guarantee Letter is a financial instrument issued by the Small and Medium Enterprises Loan Guarantee Program in Saudi Arabia. It acts as a surety for businesses, allowing them to defer the payment of customs duties and taxes during the import process. This mechanism improves liquidity for SMEs by replacing cash deposits with a formal guarantee. By utilizing this letter, importers can ensure the seamless release of goods from ports while maintaining healthy cash flow and complying with Zakat, Tax and Customs Authority regulations.

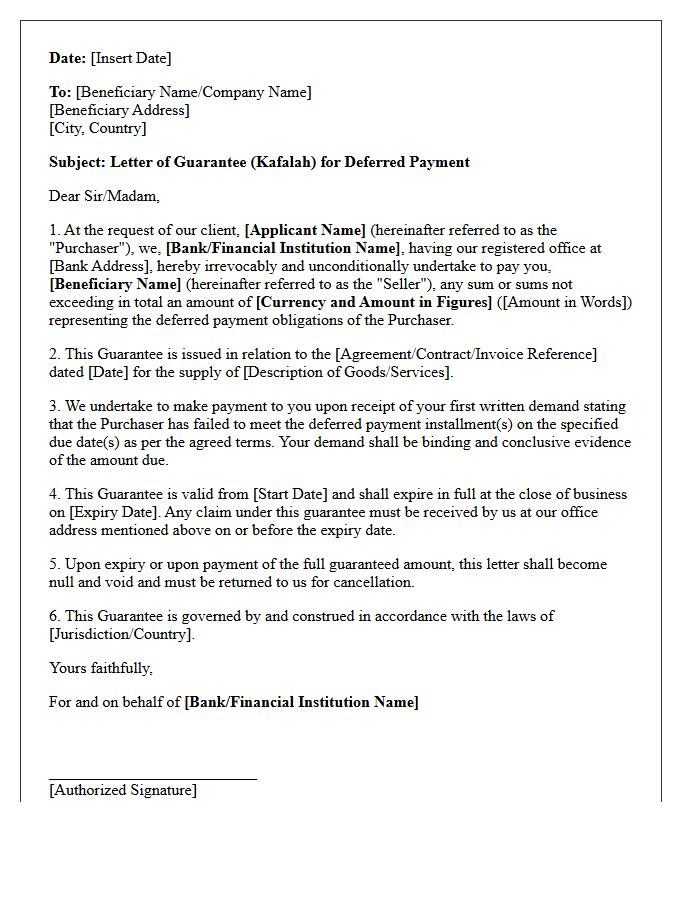

Kafalah Deferred Payment Guarantee Letter

A Kafalah Deferred Payment Guarantee Letter is a Shariah-compliant instrument where a guarantor assumes responsibility for a debtor's financial obligations. This irrevocable commitment ensures that if the buyer fails to settle a deferred payment, the bank fulfills the debt to the beneficiary. It is widely used in Islamic trade finance to provide security and credit enhancement. By mitigating default risks, it facilitates smoother commercial transactions and fosters trust between parties, allowing businesses to procure goods or services now while delaying settlement according to an agreed-upon schedule.

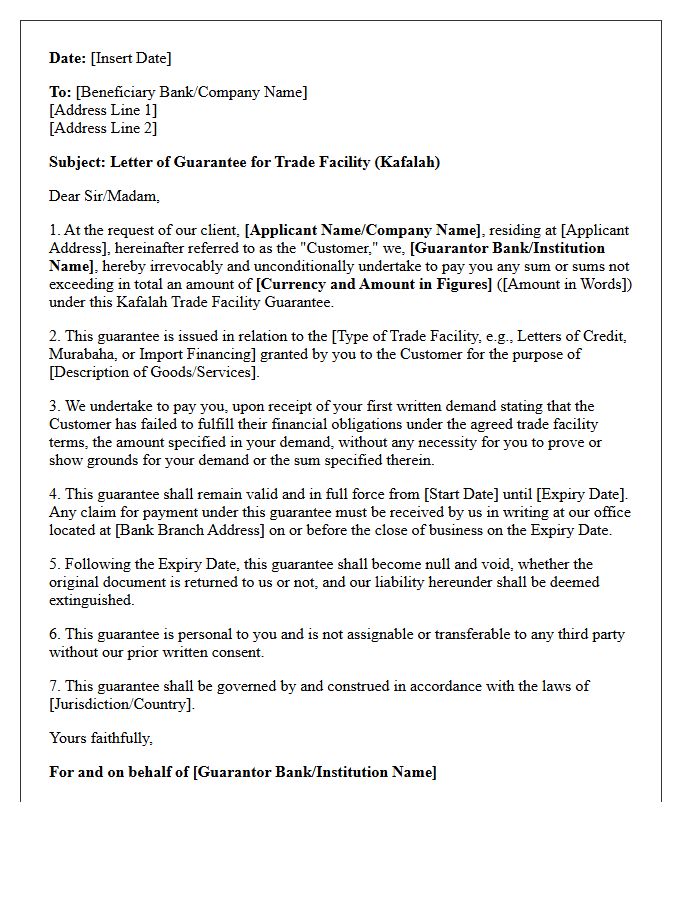

Kafalah Trade Facility Guarantee Letter

A Kafalah Trade Facility Guarantee Letter is a specialized Islamic finance instrument where a third party provides a corporate guarantee to support business transactions. It facilitates trade by ensuring payment security for suppliers, effectively enhancing a buyer's creditworthiness. This Sharia-compliant tool eliminates the need for 100% cash margins, improving liquidity management for SMEs. By mitigating default risks, it builds trust between trading partners, allowing businesses to secure better credit terms and expand operations within a regulated, ethical framework. It is essential for managing international trade risks efficiently.

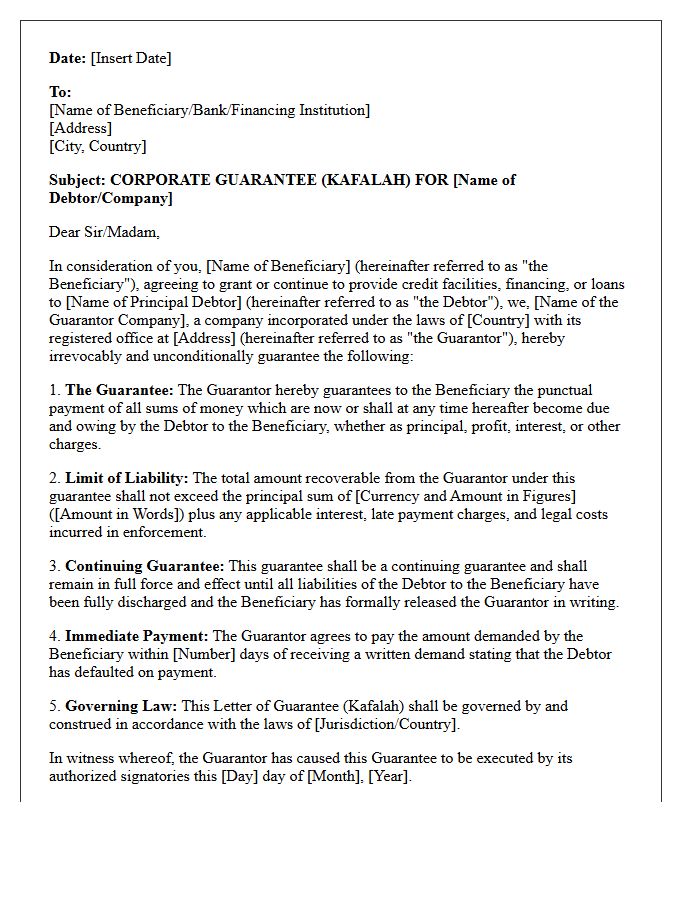

Kafalah Corporate Credit Guarantee Letter

A Kafalah Corporate Credit Guarantee Letter is a formal financial instrument where a third-party guarantor, often a specialized institution, provides a payment guarantee to a lender. It secures corporate financing by ensuring the lender is reimbursed if the borrower defaults. This credit enhancement reduces risk for financial institutions, making it easier for businesses to access capital and obtain more favorable loan terms. Primarily used in Islamic finance and trade, it bridges the gap between small-to-medium enterprises and potential investors by strengthening the borrower's overall creditworthiness and reliability in competitive global markets.

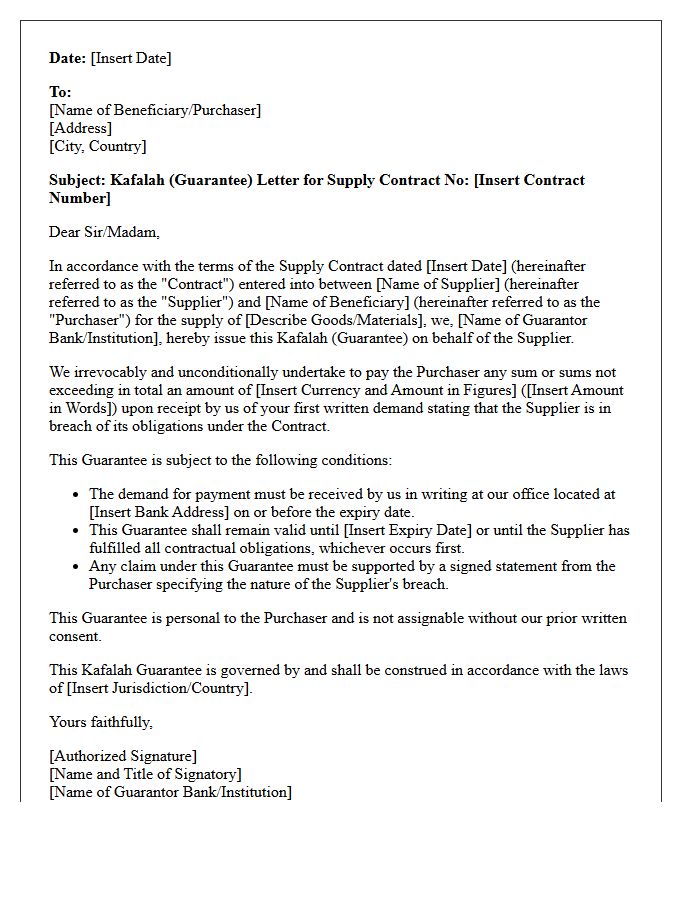

Kafalah Supply Contract Guarantee Letter

A Kafalah Supply Contract Guarantee Letter is a Sharia-compliant financial instrument where a guarantor ensures a supplier's performance or payment obligations. It serves as a collateral substitute, providing security to the beneficiary that contractual terms will be met. This Islamic guarantee facilitates trade by mitigating risk without interest-based components. It is essential for securing procurement deals, ensuring that if the applicant defaults, the guarantor compensates the supplier. Understanding the legal obligations and specific terms within the letter is vital for maintaining trust and liquidity in supply chain financing.

What is a Kafalah Guarantee Letter in Islamic Finance?

A Kafalah Guarantee Letter is a Shariah-compliant contract where a guarantor (Kafil) provides a formal undertaking to a creditor (Makful Lahu) to discharge the liability or obligation of a third party (Makful âAnhu) in the event of default. Unlike conventional guarantees, it must strictly adhere to the prohibition of Riba (interest) and Gharar (uncertainty).

What are the primary types of Kafalah used in corporate banking?

In Islamic corporate banking, the most common types include Kafalah Bi al-Mal (guarantee of property or debt), Kafalah Bi al-Nafs (guarantee of physical presence), and performance-based guarantees for construction or trade projects. These are often used as Bid Bonds, Performance Bonds, or Advance Payment Guarantees.

Can a bank charge a fee for issuing a Kafalah Guarantee?

Yes, Shariah scholars generally permit the bank to charge a fee for the administrative services provided in issuing the letter (Kafalah Bi al-Ujr). This fee is justified as a service charge for the operational work involved in the credit assessment and documentation, rather than a charge for the "risk" or "credit" itself, which would resemble interest.

How does a Kafalah Guarantee differ from a conventional Letter of Credit?

While both serve to mitigate risk, a Kafalah Guarantee is based on the principle of "joining" liabilities (Dhamm al-Dhimmah), where the guarantor becomes a secondary debtor. It must be free from interest-based penalties and cannot be utilized for projects involving non-halal activities, such as gambling, alcohol, or conventional financial services.

What happens if the guaranteed party defaults under a Kafalah agreement?

Upon default, the creditor makes a claim against the guarantor (the bank). The bank is then legally and religiously obligated to fulfill the financial commitment specified in the Kafalah Guarantee. Once the bank pays the creditor, it seeks reimbursement from the guaranteed party for the exact amount paid, without adding interest-based surcharges.

Comments