Secure essential funding for your business growth with a formal Inventory Financing Approval Letter. This document confirms a lender's commitment to financing your stock, detailing credit limits, interest rates, and repayment terms. Understanding this approval helps business owners manage cash flow and scale operations effectively. To streamline your application process, below are some ready to use template.

Image cover: Securing Capital: Inventory Financing Approval Letter Guide and Templates

Letter Samples List

- Standard Inventory Financing Approval Letter

- Conditional Inventory Financing Approval Letter

- Final Inventory Facility Approval Letter

- Revolving Inventory Credit Approval Letter

- Floor Plan Inventory Financing Approval Letter

- Warehouse Receipt Financing Approval Letter

- Dealer Inventory Financing Approval Letter

- Secured Inventory Loan Approval Letter

- Commercial Inventory Advance Approval Letter

- Working Capital Inventory Approval Letter

- Syndicated Inventory Financing Approval Letter

- Seasonal Inventory Credit Approval Letter

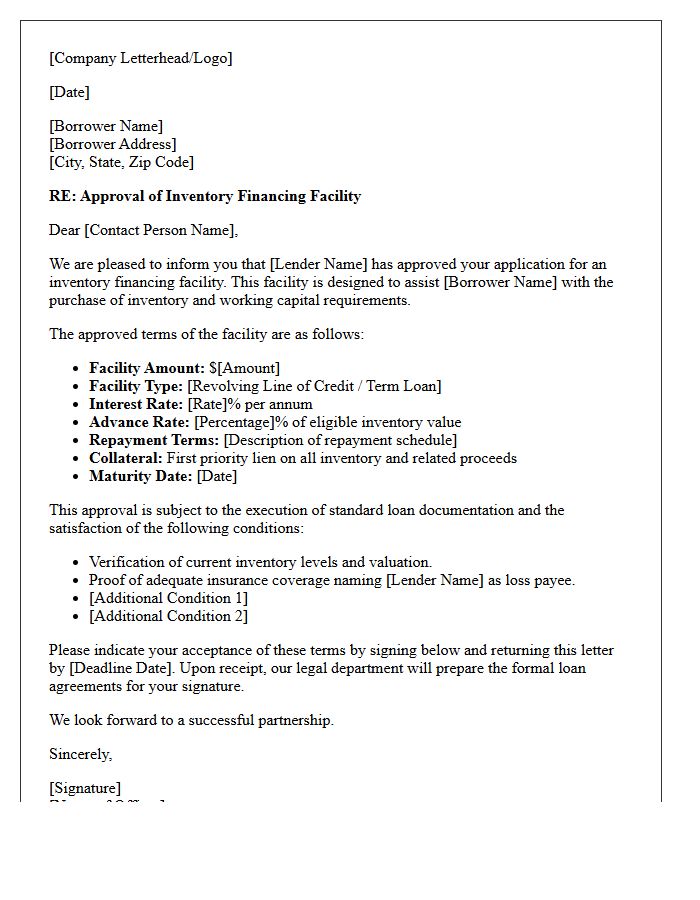

Standard Inventory Financing Approval Letter

A Standard Inventory Financing Approval Letter is a formal commitment from a lender to provide working capital secured by inventory. This document specifies the maximum credit limit, interest rates, and advance rates based on asset valuation. It serves as essential proof of funding for businesses looking to optimize supply chain operations and manage seasonal stock fluctuations. Key terms include reporting requirements and collateral benchmarks, ensuring the borrower maintains sufficient inventory levels to support the loan. Obtaining this letter validates financial credibility and facilitates smoother procurement processes with vendors.

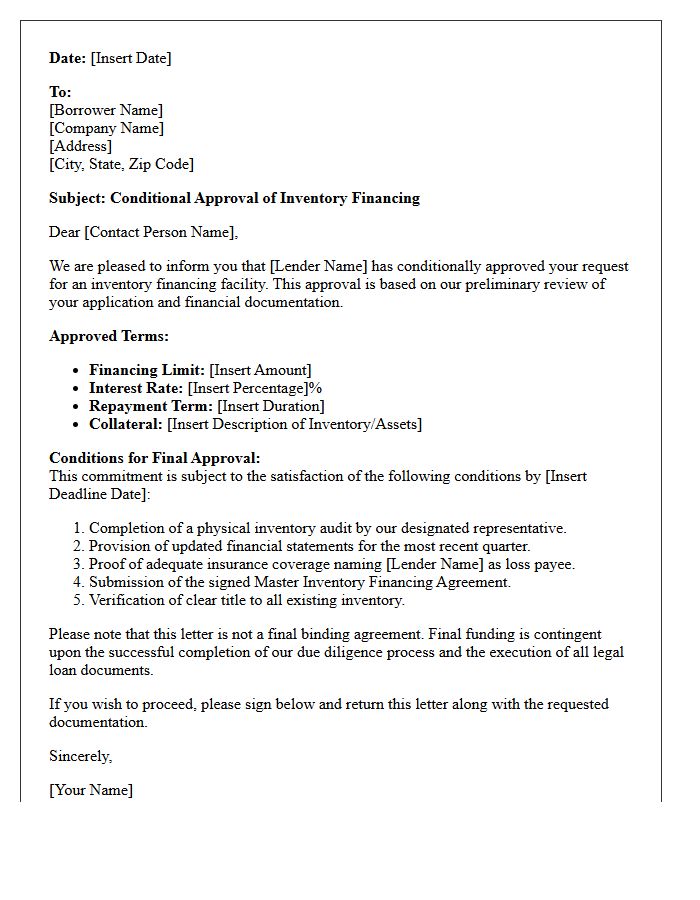

Conditional Inventory Financing Approval Letter

A Conditional Inventory Financing Approval Letter is a formal document issued by a lender stating preliminary intent to fund stock purchases. It outlines specific contingencies, such as financial audits or collateral appraisals, that must be satisfied before final funding. This letter serves as proof of creditworthiness to suppliers, helping businesses secure better purchasing terms. However, it is not a binding contract; actual capital is only disbursed once all underwriting requirements are met and final loan agreements are signed by both parties.

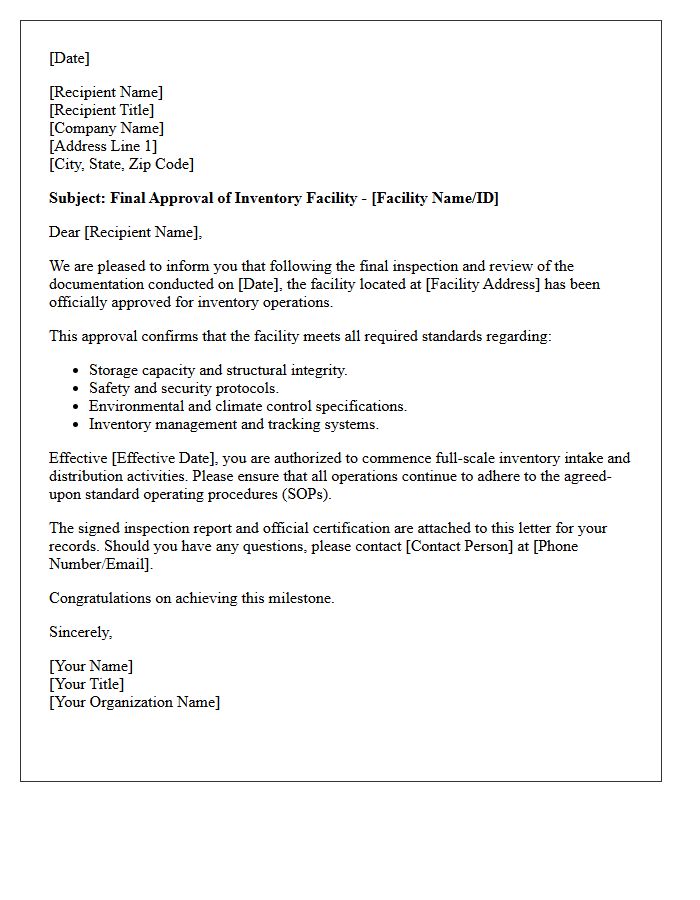

Final Inventory Facility Approval Letter

The Final Inventory Facility Approval Letter is a formal document issued by regulatory authorities or management confirming that a site meets all compliance standards for storage. This letter signifies the successful completion of inspections and technical reviews. It serves as official authorization to begin full-scale operations or decommissioning, ensuring that safety protocols and inventory accuracy are fully verified. Receiving this approval is the final regulatory milestone required to validate that a facility is legally and operationally prepared to handle specific materials or goods.

Revolving Inventory Credit Approval Letter

A Revolving Inventory Credit Approval Letter is a formal document confirming a lender's commitment to provide asset-based financing. This revolving facility allows businesses to borrow against inventory value, providing essential working capital to purchase stock. Unlike fixed loans, the available credit fluctuates based on current inventory levels. Key terms include the maximum borrowing limit, interest rates, and specific eligibility criteria for goods. Securing this letter demonstrates financial flexibility, ensuring a company can maintain optimal supply levels and meet seasonal demand while improving overall liquidity management for operational growth.

Floor Plan Inventory Financing Approval Letter

A Floor Plan Inventory Financing Approval Letter is a critical document issued by lenders to vehicle or equipment dealerships. It confirms a specific credit line available to purchase inventory directly from manufacturers. This letter demonstrates financial credibility, allowing dealers to stock their showrooms without immediate cash outlays. Key details include the approved borrowing limit, interest rates, and repayment terms. Having this approval is essential for maintaining operational liquidity and scaling inventory levels to meet consumer demand efficiently within the retail automotive or heavy equipment industries.

Warehouse Receipt Financing Approval Letter

A Warehouse Receipt Financing Approval Letter is a formal commitment from a lender to provide liquidity based on stored inventory. It serves as verification that the goods held in a certified warehouse are eligible collateral for a loan. This document outlines the specific loan-to-value ratio, interest rates, and compliance conditions required to access capital. By leveraging this letter, businesses can improve cash flow and manage operational costs without selling stock prematurely, ensuring a stable financial bridge between production and final sale.

Dealer Inventory Financing Approval Letter

A Dealer Inventory Financing Approval Letter, or floor plan approval, is a formal document confirming a lender's commitment to finance a dealership's vehicle stock. This letter outlines the approved credit limit, interest rates, and repayment terms. It serves as essential proof of purchasing power, allowing dealers to acquire inventory from manufacturers or auctions immediately. For lenders, it represents a calculated risk assessment, while for dealers, it is the primary tool for maintaining liquidity and ensuring a consistent flow of showroom units to meet customer demand and drive sales growth.

Secured Inventory Loan Approval Letter

A Secured Inventory Loan Approval Letter is a formal commitment from a lender to provide financing backed by a business's physical stock. This document outlines the maximum loan amount, interest rates, and specific advance rates based on the inventory's appraised value. It serves as a critical indicator of creditworthiness, confirming that the lender has completed their due diligence and risk assessment. Receiving this letter allows a company to optimize its working capital and maintain sufficient product levels to meet market demand effectively while using assets as collateral.

Commercial Inventory Advance Approval Letter

A Commercial Inventory Advance Approval Letter is a critical document issued by lenders to confirm the pre-authorized financing of specific business stock. It serves as a formal guarantee that funds are available for inventory acquisition, allowing businesses to secure goods from suppliers quickly. This letter outlines the maximum loan amount, interest rates, and required collateral. By streamlining the procurement process, it enhances cash flow management and builds trust with vendors, ensuring that high-demand products are purchased without immediate capital outlays or lengthy manual approval delays during peak cycles.

Working Capital Inventory Approval Letter

A Working Capital Inventory Approval Letter is a formal document from a lender confirming the authorization of funds specifically to purchase or leverage stock. This letter outlines the maximum borrowing base allowed, interest rates, and collateral requirements. It is essential for maintaining healthy cash flow and ensuring a business can meet customer demand without liquid capital shortages. For many retailers and wholesalers, this approval serves as a vital financial guarantee, allowing them to scale operations and optimize supply chain management effectively during peak seasonal cycles.

Syndicated Inventory Financing Approval Letter

A Syndicated Inventory Financing Approval Letter is a formal commitment where a group of lenders, rather than a single bank, agrees to fund a business's stock. This document outlines the credit limit, interest rates, and collateral requirements. It is essential for large-scale retailers needing significant capital to maintain supply chains. The letter proves financial backing to suppliers, ensuring seamless inventory procurement. Understanding the participation roles and repayment terms within the syndicate is crucial for managing operational cash flow and maintaining leveraged liquidity for business expansion.

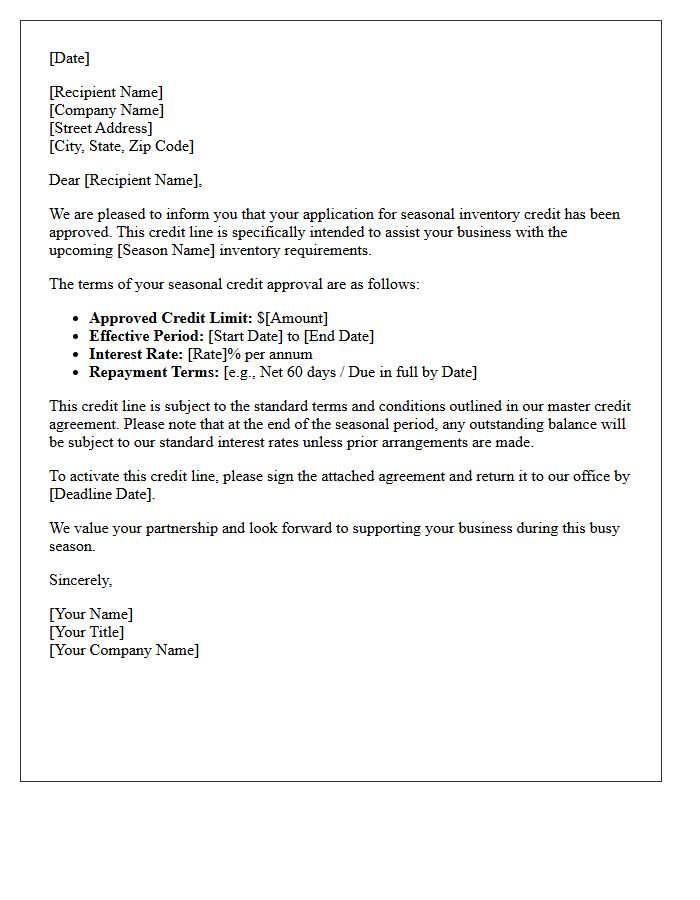

Seasonal Inventory Credit Approval Letter

A Seasonal Inventory Credit Approval Letter is a formal document from a lender authorizing short-term financing to manage peak stock demands. It outlines specific terms like the credit limit, interest rates, and the repayment schedule tailored to your business's sales cycle. This letter is crucial for maintaining liquidity during high-volume periods without straining working capital. Ensure you review the expiration date and collateral requirements to maintain compliance and secure your supply chain readiness for the upcoming season.

What is an Inventory Financing Approval Letter?

An inventory financing approval letter is an official document issued by a lender confirming that a business has been cleared to receive a revolving line of credit or loan specifically for purchasing raw materials or finished goods. It outlines the maximum credit limit, interest rates, and the specific terms required to activate the funding.

What key information is included in an inventory loan commitment letter?

A standard approval letter includes the total facility amount, the advance rate (the percentage of inventory value the lender will fund), the applicable interest rate, repayment schedules, and any collateral requirements or financial covenants the borrower must maintain.

How long does it take to receive an approval letter for inventory financing?

The timeline typically ranges from 2 to 4 weeks depending on the lender. This period involves a thorough audit of current inventory turnover ratios, financial statements, and a physical appraisal of the stock to determine its liquidation value.

Does an approval letter guarantee immediate funding for inventory?

No, an approval letter is a conditional commitment. Funding is usually contingent upon "closing conditions," such as the final execution of security agreements, proof of insurance, and the successful filing of a UCC-1 financing statement to secure the lender's interest in the inventory.

Why would a lender rescind an inventory financing approval?

A lender may revoke an approval if there is a significant decrease in the borrower's credit score, a discovery of undisclosed liens on assets, or if the market value of the inventory drops sharply before the final loan documents are signed.

Comments