A Mortgage Pre-Approval Letter is a formal document from a lender stating the specific loan amount you qualify for based on your credit and finances. It strengthens your offer by proving to sellers that you are a serious, qualified buyer. Understanding this step is essential for a successful home search. Below are some ready to use template.

Image cover: Mortgage Pre-Approval Letter: Professional Templates and Proven Examples

Letter Samples List

- Mortgage Pre-Approval Letter

- Mortgage Pre-Qualification Letter

- Conditional Mortgage Approval Letter

- Final Mortgage Commitment Letter

- Adverse Action Mortgage Denial Letter

- Verification of Employment Letter

- Verification of Deposit Letter

- Mortgage Rate Lock Confirmation Letter

- Gift Funds Documentation Letter

- Credit Inquiry Explanation Letter

- Mortgage Loan Estimate Cover Letter

- Notice of Incomplete Application Letter

- Clear to Close Authorization Letter

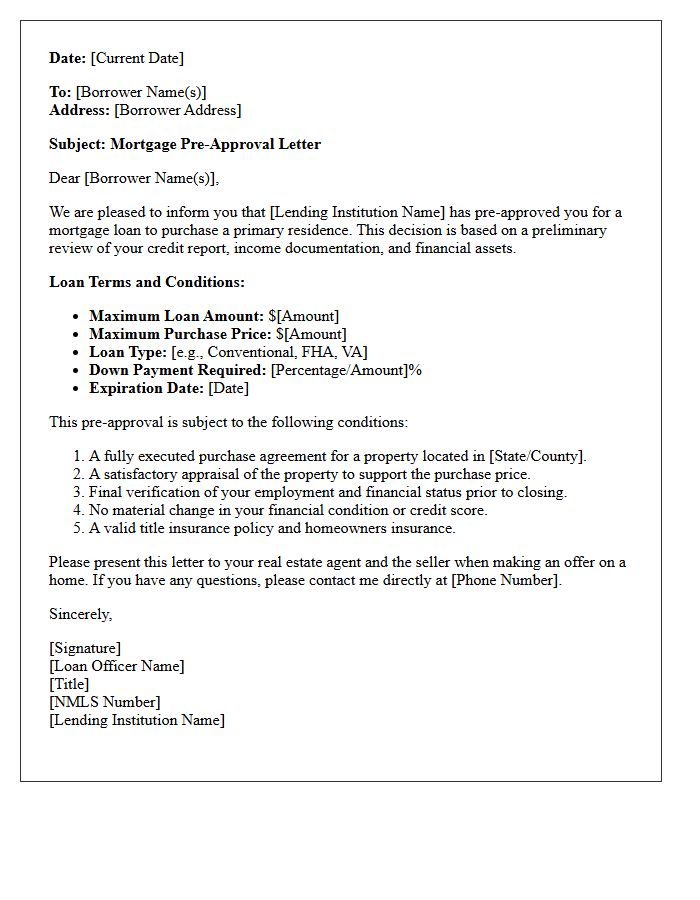

Mortgage Pre-Approval Letter

A Mortgage Pre-Approval Letter is a document from a lender stating the specific loan amount you qualify to borrow. It is an essential first step in the home-buying process because it proves to sellers that you are a financially credible buyer with verified income and credit. Unlike a pre-qualification, this letter involves a rigorous financial review, giving you a competitive edge during negotiations. Having this document ensures you focus on properties within your budget while demonstrating your purchasing power to real estate agents and listing parties.

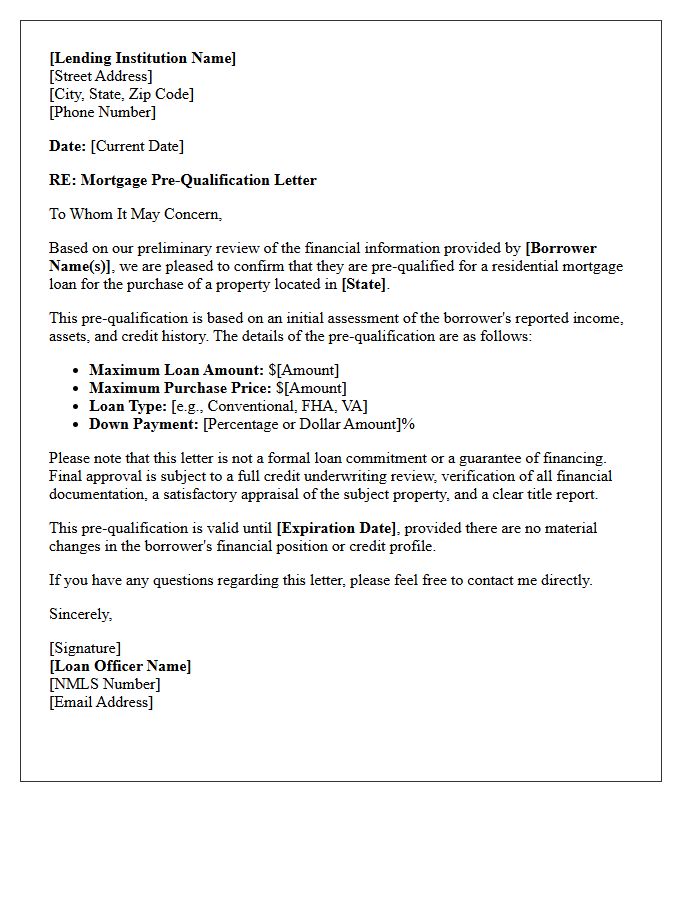

Mortgage Pre-Qualification Letter

A Mortgage Pre-Qualification Letter provides an initial estimate of how much you can afford to borrow. It is based on self-reported financial data, such as income, assets, and debt, without an in-depth credit check. While not a formal loan commitment, it is an essential first step in the home-buying process. This document helps you understand your budget and demonstrates to sellers that you are a serious buyer. For a stronger competitive edge in real estate negotiations, many lenders recommend upgrading to a verified pre-approval later.

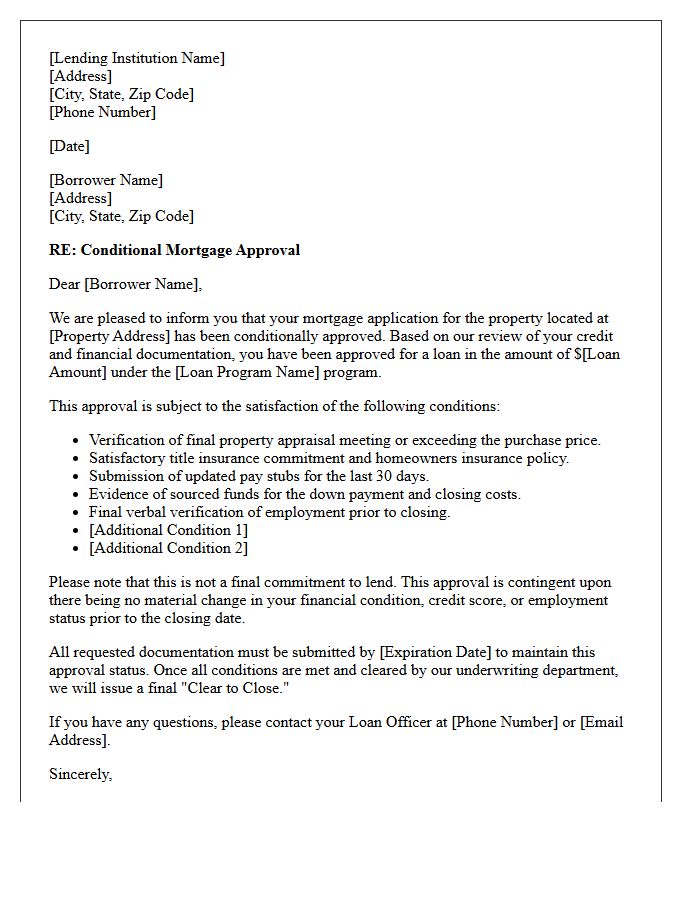

Conditional Mortgage Approval Letter

A conditional mortgage approval letter is a formal statement from a lender indicating they are willing to fund your home loan, provided specific outstanding requirements are met. Unlike a pre-approval, this document follows an initial underwriter review. To secure final funding, borrowers must resolve conditions such as updated pay stubs, tax returns, or a satisfactory property appraisal. Obtaining this letter brings you closer to the closing table, but it is not a guaranteed commitment until all contingencies are fully cleared and verified by the bank.

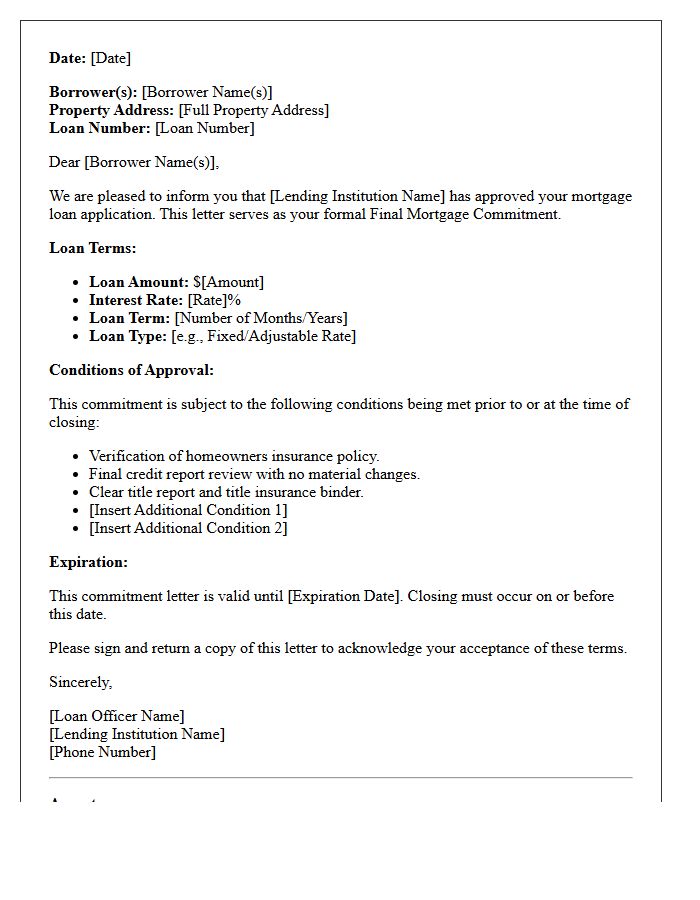

Final Mortgage Commitment Letter

A Final Mortgage Commitment Letter is a formal document from a lender confirming that your home loan is officially approved. Unlike a pre-approval, this letter is issued only after underwriting is complete and all conditions, such as appraisals and title searches, are satisfied. It outlines the final loan amount, interest rate, and specific terms of the agreement. Receiving this document is the last major milestone before the closing process, signifying that the bank is legally committed to funding your property purchase.

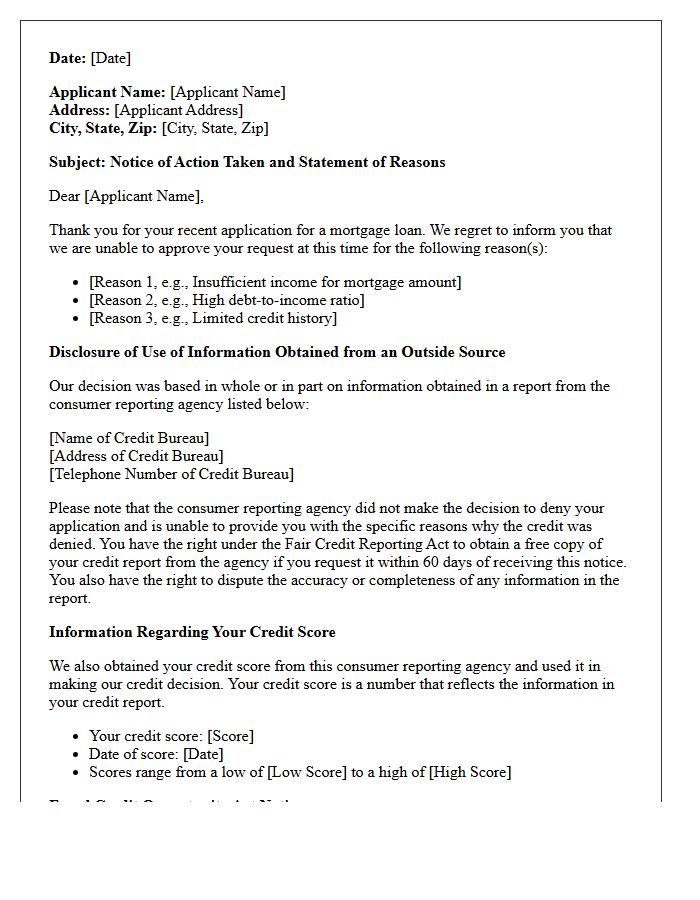

Adverse Action Mortgage Denial Letter

An Adverse Action Mortgage Denial Letter is a legally required document issued when a lender rejects your loan application. It must clearly state the specific reasons for the denial, such as a low credit score or insufficient income. Under the Equal Credit Opportunity Act, this notice ensures transparency and protects you against discrimination. Additionally, it provides contact information for the credit reporting agency used, allowing you to dispute inaccuracies. Reviewing this letter is essential for understanding your financial standing and improving your eligibility for future mortgage approvals.

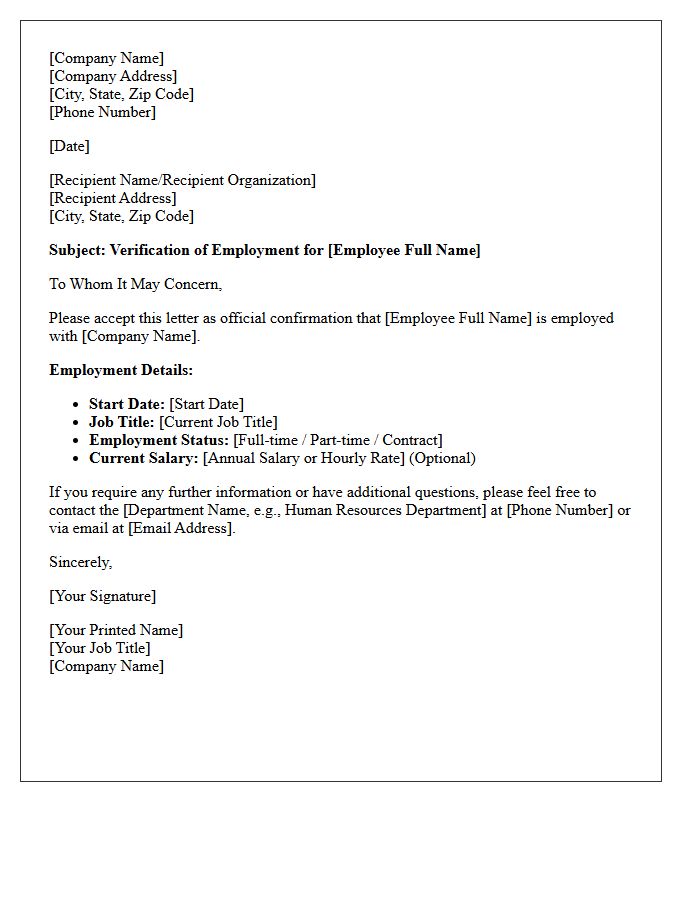

Verification of Employment Letter

A Verification of Employment (VOE) letter is a formal document used to confirm an individual's current or past job status, title, and salary. Lenders, landlords, and government agencies typically require this official proof to assess financial stability and creditworthiness. It serves as validated evidence that an employee possesses a steady income stream. Employers must ensure the letter is accurate, professional, and authorized to prevent delays in loan approvals or background checks. Providing this documentation promptly is essential for a smooth verification process during significant life transactions.

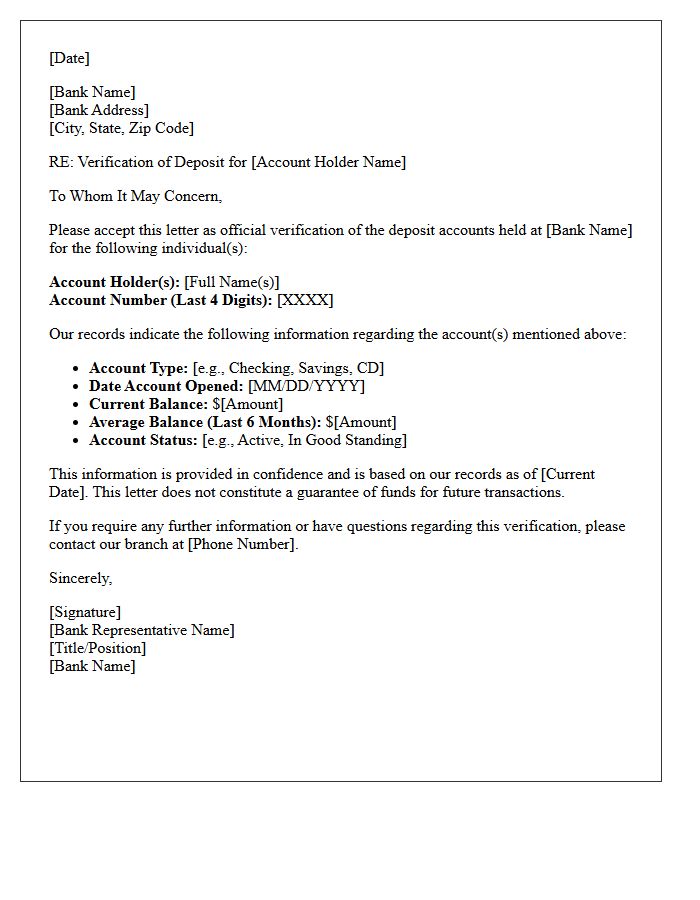

Verification of Deposit Letter

A Verification of Deposit (VOD) letter is an official document issued by a financial institution to confirm a borrower's account balances and history. It serves as essential proof of liquidity during the mortgage application process, ensuring lenders that the applicant possesses sufficient funds for down payments and closing costs. This document validates the authenticity of assets, helping to prevent fraud and assess overall creditworthiness. For a smooth loan approval, ensure your bank accurately reflects current totals and that all financial statements align with the information provided to the lender.

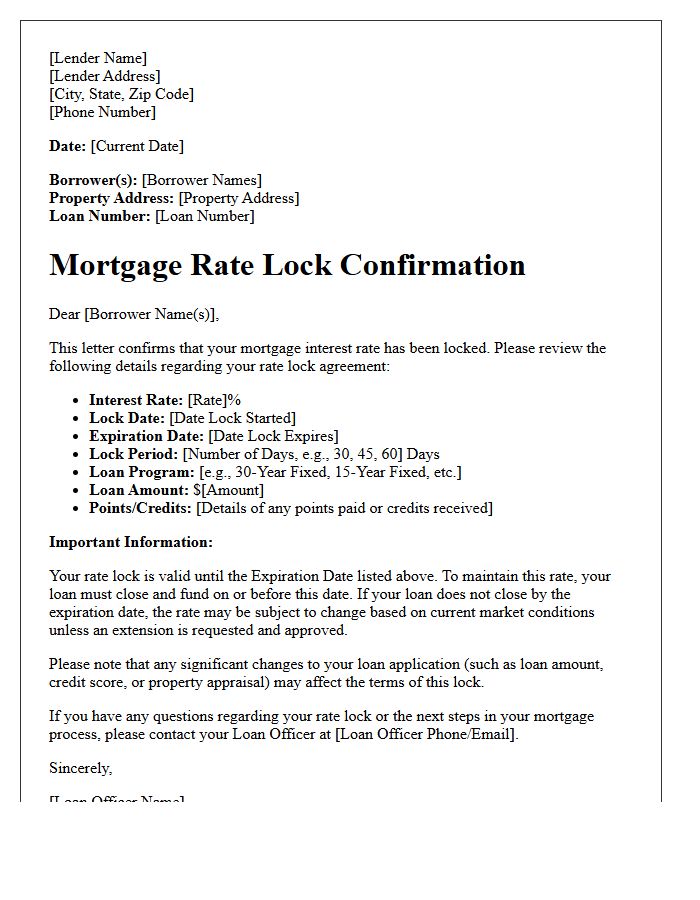

Mortgage Rate Lock Confirmation Letter

A Mortgage Rate Lock Confirmation Letter is a formal document from your lender guaranteeing a specific interest rate for a set period. It protects you from market fluctuations while your loan is processed. Key details include the expiration date, agreed rate, and points. If your loan does not close before the lock expires, your rate may increase. Always verify that the terms match your verbal agreement to ensure financial certainty during the homebuying process. This letter serves as your legal proof of the secured pricing and loan program terms.

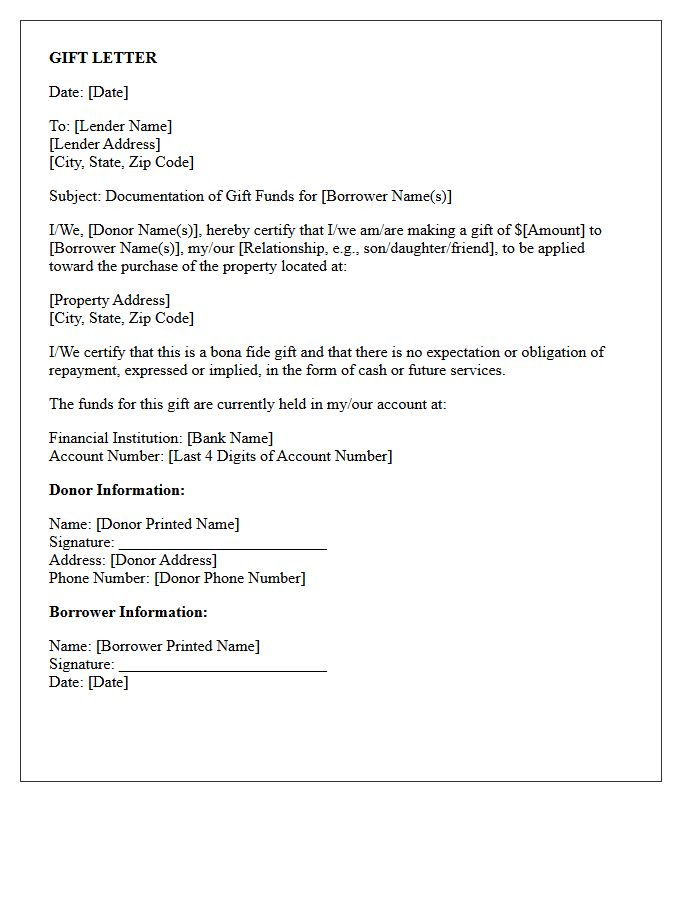

Gift Funds Documentation Letter

A Gift Funds Documentation Letter serves as formal proof that money transferred for a mortgage down payment is a bona fide gift, not a loan. Lenders require this document to ensure the homebuyer has no hidden repayment obligations. The letter must clearly state the donor's relationship to the borrower, the specific dollar amount, and a signed declaration that no repayment is expected. Accompanying bank statements are typically necessary to verify the source of funds and maintain strict compliance with anti-money laundering regulations during the underwriting process.

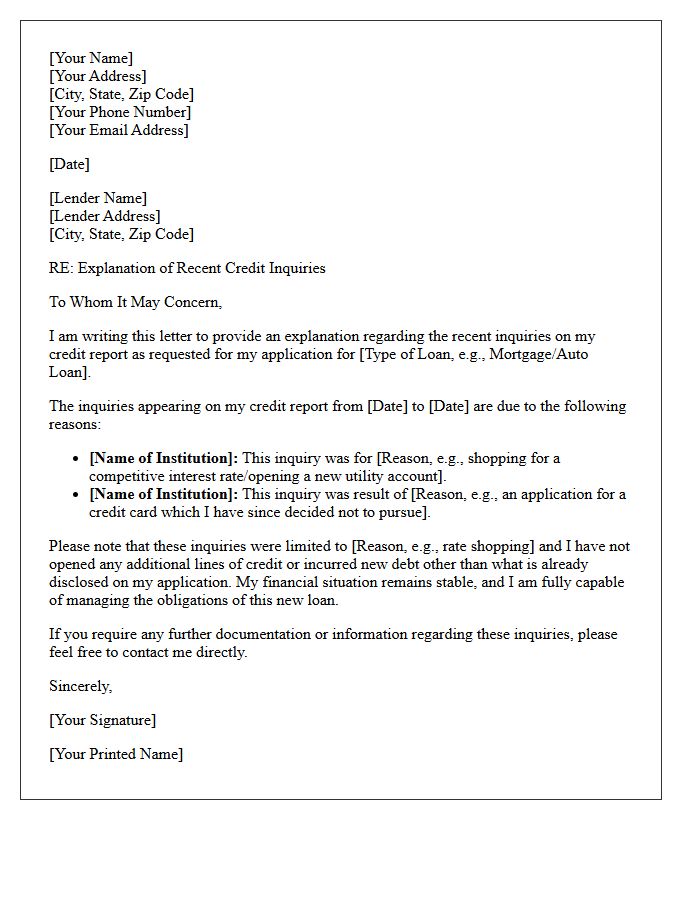

Credit Inquiry Explanation Letter

A credit inquiry explanation letter is a formal document sent to lenders to clarify hard inquiries on your credit report. This letter helps justify why you were seeking credit, such as for a mortgage or auto loan, to reassure underwriters that you are not overextending financially. Clearly state the purpose of each inquiry and confirm if new credit was actually opened. Providing a detailed explanation can mitigate the negative impact of multiple applications, ultimately improving your chances of loan approval by demonstrating fiscal responsibility and transparency.

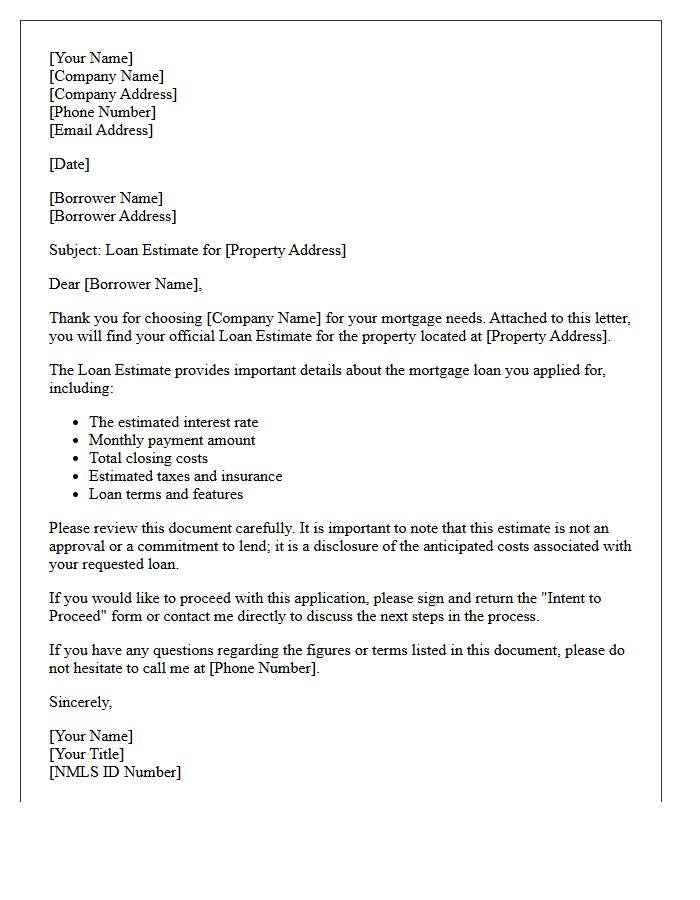

Mortgage Loan Estimate Cover Letter

A mortgage loan estimate cover letter is a professional introduction to your official loan disclosure. It serves as a summary guide, highlighting key details like your projected interest rate, monthly payments, and estimated closing costs. Reviewing this document helps you understand the terms offered by the lender before committing. It is essential to verify accuracy and compare it against other offers to ensure you are receiving the most competitive financing agreement available. Always clarify any discrepancies with your loan officer immediately to avoid future processing delays.

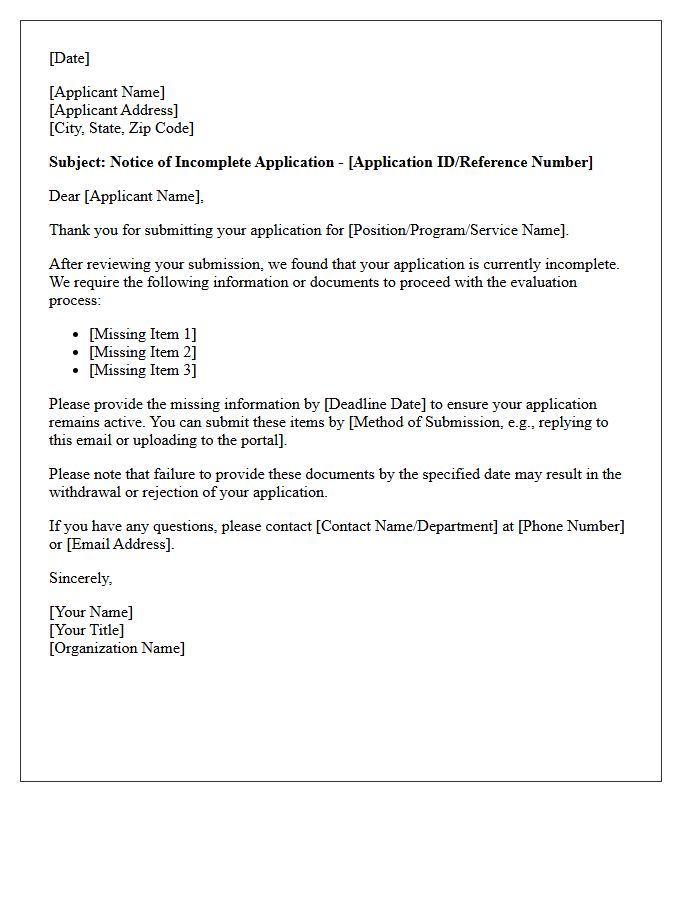

Notice of Incomplete Application Letter

A Notice of Incomplete Application Letter is a formal document issued by an organization or government agency stating that a submission is missing required information. It is crucial to review the specific deficiencies listed to avoid processing delays or potential denial. Applicants must submit the requested documentation within the stated deadline to keep the application active. This notification serves as a vital communication link, ensuring that the evaluation process can proceed once all necessary criteria are met. Promptly addressing these gaps is the most important step in securing a successful outcome.

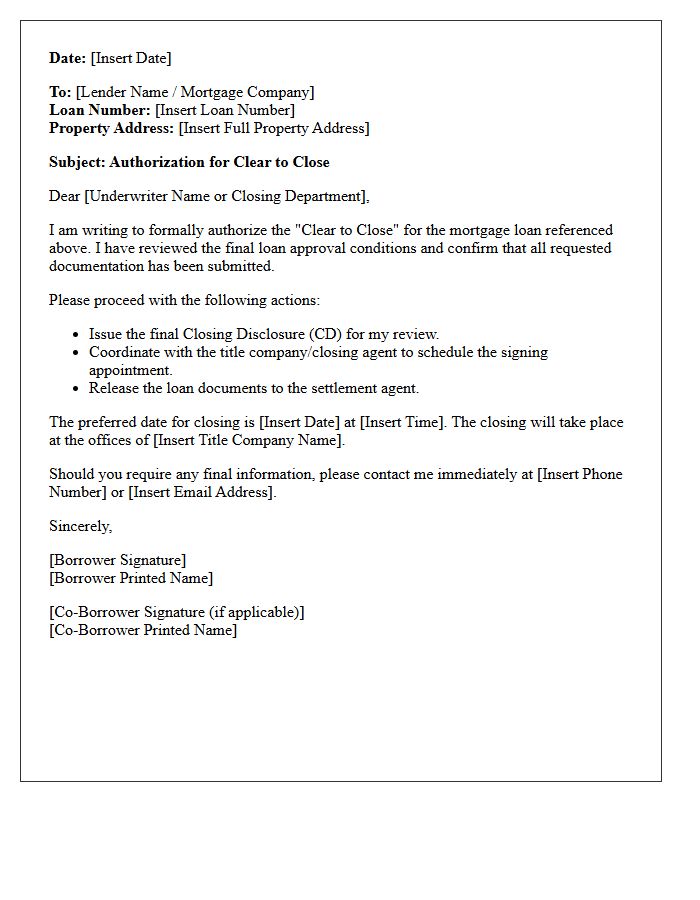

Clear to Close Authorization Letter

A Clear to Close (CTC) authorization letter is the final confirmation from a mortgage lender that all underwriting conditions are met. This legal clearance signifies the loan is fully approved and ready for funding. Once issued, the lender prepares the closing disclosure and schedules the signing appointment. It is the most critical milestone for homebuyers, confirming that financial vetting is complete. To maintain this status, avoid any new debts, job changes, or large bank transfers until the property deed is officially recorded.

What is a mortgage pre-approval letter?

A mortgage pre-approval letter is a document from a lender stating the specific loan amount you are qualified to borrow based on a preliminary review of your credit score, income, and financial documentation. It signals to home sellers that you are a serious, qualified buyer.

How do I get a mortgage pre-approval letter?

To obtain a pre-approval letter, you must submit a formal loan application to a lender and provide supporting documentation, including W-2s, pay stubs, bank statements, and tax returns. The lender will also perform a hard credit pull to verify your debt-to-income ratio and creditworthiness.

How long does a mortgage pre-approval letter last?

Most mortgage pre-approval letters are valid for 60 to 90 days. Because financial situations and interest rates fluctuate, lenders require periodic updates to your documentation to ensure you still meet the qualification criteria after the initial letter expires.

What is the difference between pre-qualification and pre-approval?

Pre-qualification is a basic estimate of borrowing power based on unverified information provided by the borrower. In contrast, a pre-approval is a conditional commitment from a lender that involves a rigorous verification of financial records and a credit check, making it much stronger during a home offer.

Does getting a mortgage pre-approval letter affect my credit score?

Yes, getting pre-approved typically involves a hard credit inquiry, which may cause a temporary dip of five points or less in your credit score. However, if you apply with multiple lenders within a 14-to-45-day window, credit scoring models usually treat them as a single inquiry for "rate shopping" purposes.

Comments