Staying informed about changes to your loan or savings terms is essential for financial stability. A Notification of Interest Rate Adjustment provides transparent updates regarding rate hikes or decreases, ensuring compliance and clear communication with clients. Understanding these shifts helps you manage expectations and adjust your budget effectively. To simplify your process, below are some ready to use template.

Image cover: Upcoming Interest Rate Adjustments: Essential Notice Templates and Samples

Letter Samples List

- Mortgage Interest Rate Adjustment Notification Letter

- Credit Card Annual Percentage Rate Adjustment Letter

- Personal Loan Interest Rate Revision Letter

- Savings Account Yield Adjustment Notification Letter

- Commercial Loan Variable Rate Adjustment Letter

- Bank Base Lending Rate Modification Letter

- Fixed Deposit Renewal And Rate Adjustment Letter

- Overdraft Facility Interest Rate Change Letter

- Automobile Loan Variable Rate Adjustment Letter

- Educational Loan Interest Rate Notification Letter

- Promotional Interest Rate Expiration Adjustment Letter

- Home Equity Line Of Credit Rate Adjustment Letter

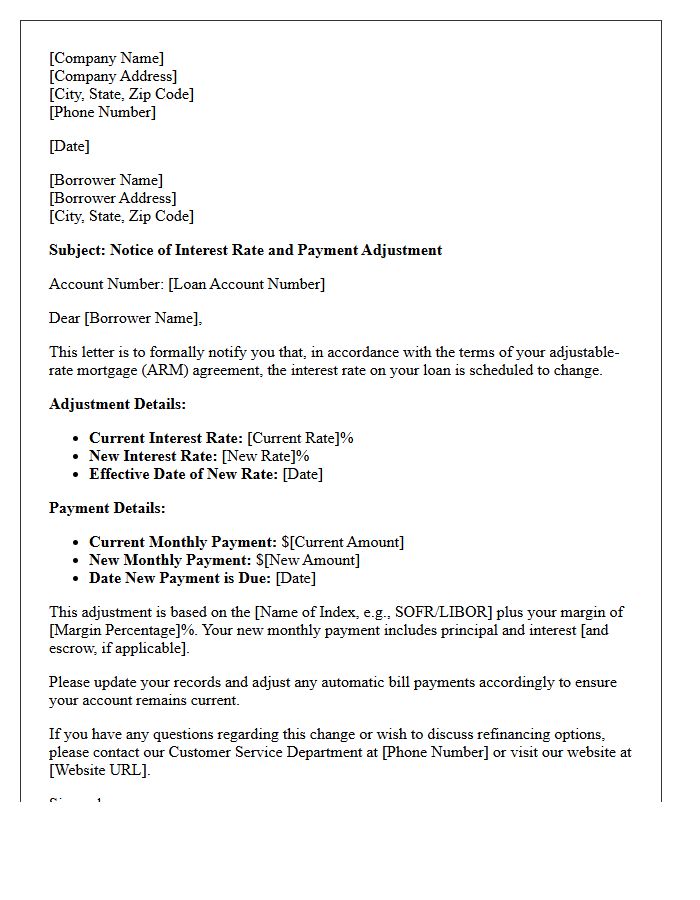

Mortgage Interest Rate Adjustment Notification Letter

A Mortgage Interest Rate Adjustment Notification Letter is a legal document sent by lenders to inform borrowers about changes in their monthly payments. This ARM disclosure must be sent at least 60 to 120 days before the new rate takes effect. It details the new interest rate, the specific index used, and the upcoming payment amount. Reviewing this notice is crucial for budgeting and evaluating refinancing options to avoid payment shock from unexpected increases in your housing costs.

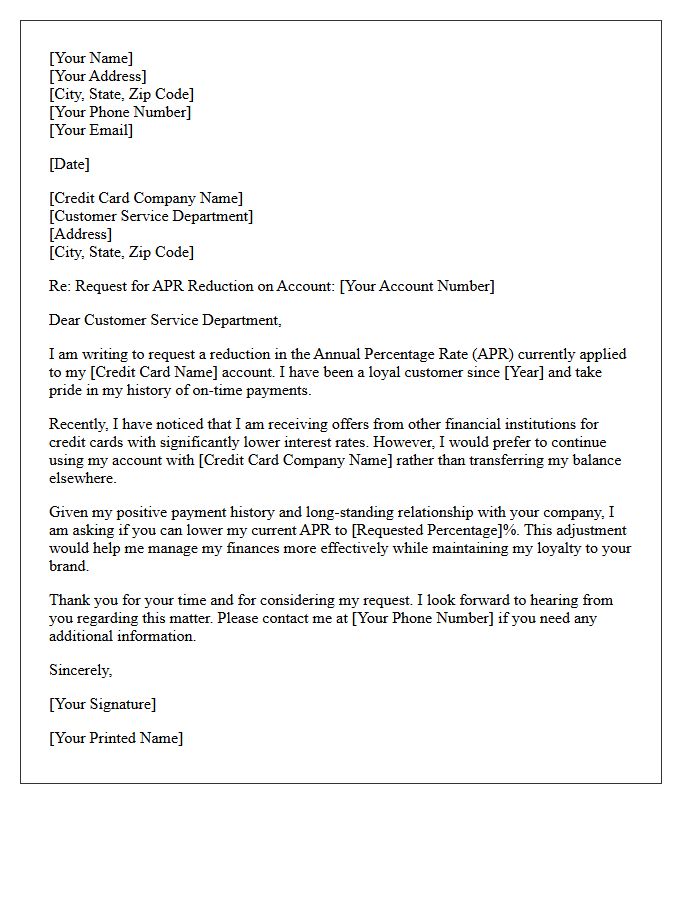

Credit Card Annual Percentage Rate Adjustment Letter

A Credit Card Annual Percentage Rate Adjustment Letter is a formal notice from your issuer regarding a change in your interest rate. This document typically arrives 45 days before the new rate applies, as required by law. It highlights adjustments often triggered by prime rate changes or shifts in your credit profile. Understanding this letter is crucial for managing your monthly finance charges. Review the effective date and the variable rate calculation to determine how these changes impact your outstanding balance and overall debt management strategy.

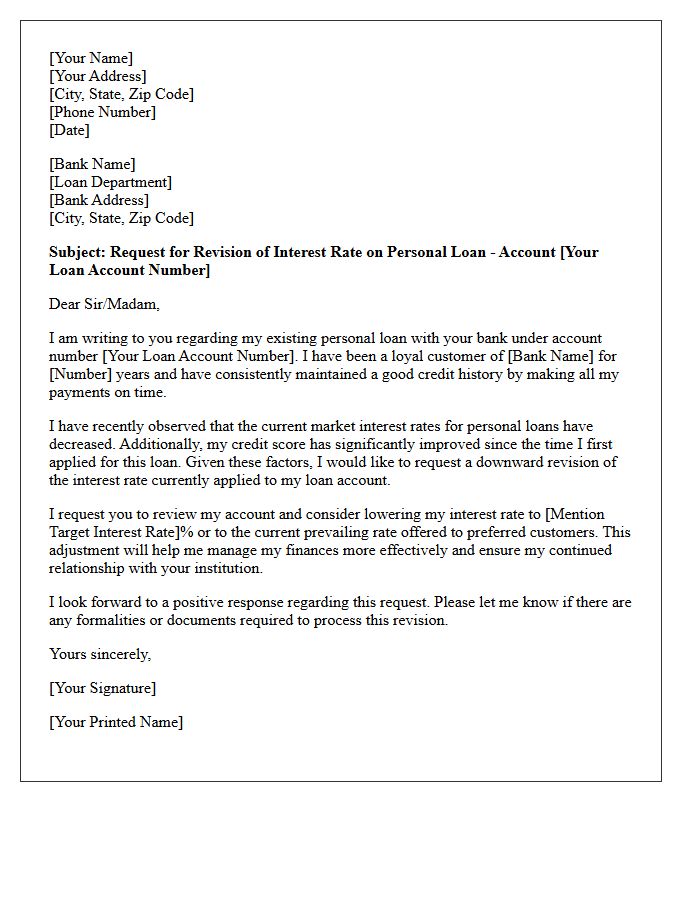

Personal Loan Interest Rate Revision Letter

A Personal Loan Interest Rate Revision Letter is a formal notification from a lender informing the borrower about a change in their annual percentage rate. This document outlines the new interest rate, the effective date of the adjustment, and how it impacts your monthly installments or total loan tenure. It is essential to review this letter to understand your updated repayment obligations, especially in a floating rate environment. Always verify the calculation against your original loan agreement to ensure transparency and maintain financial stability during the repayment period.

Savings Account Yield Adjustment Notification Letter

A Savings Account Yield Adjustment Notification Letter informs customers that the annual percentage yield (APY) on their account has changed. This adjustment typically follows shifts in Federal Reserve interest rates or market conditions. Banks are required to provide this notice to ensure transparency regarding your earnings potential. It is crucial to review how this new rate impacts your financial goals. If the yield decreases, consider comparing other high-yield savings options to maintain optimal growth for your capital and ensure your money continues working effectively for you.

Commercial Loan Variable Rate Adjustment Letter

A Commercial Loan Variable Rate Adjustment Letter is a formal notification from a lender informing a borrower of a change in their interest rate. This document specifies the new index rate, the margin applied, and the resulting monthly payment adjustment. It is crucial for financial planning, as it reflects fluctuations in market benchmarks like LIBOR or SOFR. Borrowers should verify the accuracy of the reset date and ensure their amortization schedule remains aligned with the original loan agreement to avoid unexpected capital shortfalls.

Bank Base Lending Rate Modification Letter

A Bank Base Lending Rate Modification Letter is an official notification informing borrowers of a change in interest rates. This document outlines the adjusted monthly repayments and the effective date of the new rate. It is crucial to review this letter to understand how monetary policy shifts impact your debt obligations. Monitoring these updates helps in managing personal cash flow and long-term financial planning, ensuring you remain compliant with your loan agreement during economic fluctuations.

Fixed Deposit Renewal And Rate Adjustment Letter

A Fixed Deposit Renewal And Rate Adjustment Letter is a formal notification sent by banks to inform depositors about an upcoming maturity. It details the new interest rates applied upon renewal, ensuring transparency regarding investment growth. It is essential to review the renewal period and updated terms to decide between automatic reinvestment or fund withdrawal. Timely action prevents your capital from earning lower default rates. Always verify the effective date and maturity instructions to maximize your financial returns and maintain portfolio stability effectively.

Overdraft Facility Interest Rate Change Letter

An Overdraft Facility Interest Rate Change Letter is a formal notification from your bank regarding adjustments to borrowing costs. It is crucial to review the effective date and the new Annual Percentage Rate (APR) to understand how your monthly repayments or debt obligations will fluctuate. These changes often occur due to shifts in central bank benchmarks or internal policy updates. Carefully assess your financial liquidity and consider alternative credit options if the increased rates impact your ability to manage outstanding balances effectively.

Automobile Loan Variable Rate Adjustment Letter

An Automobile Loan Variable Rate Adjustment Letter is a formal notice informing borrowers that their monthly payments or loan terms have changed. This occurs because the loan is tied to a fluctuating index, such as the prime rate. When market interest rates rise or fall, your lender must send this document to disclose the new interest rate, the effective date, and the updated payment amount. Reviewing these notices is crucial for effective budgeting and ensuring your vehicle financing remains manageable throughout the life of the loan.

Educational Loan Interest Rate Notification Letter

An Educational Loan Interest Rate Notification Letter is a formal document informing borrowers of changes to their interest rates. It provides critical updates on monthly repayment amounts and the overall cost of borrowing. Understanding these adjustments is essential for effective financial planning and debt management. Borrowers should carefully review the effective date and any potential impacts on their amortization schedule. This legal notice ensures transparency between the lender and the student, helping individuals adjust their budgets to accommodate fluctuating loan obligations and maintain fiscal health throughout their repayment period.

Promotional Interest Rate Expiration Adjustment Letter

A Promotional Interest Rate Expiration Adjustment Letter is a formal notification from your lender stating that a temporary introductory rate is ending. This document specifies the date your interest will increase and details the new variable or fixed rate that will apply moving forward. It is crucial to review this letter immediately to understand how your monthly payments will change. Use this notice to evaluate your budget or consider refinancing options before the higher interest costs take effect on your next billing cycle.

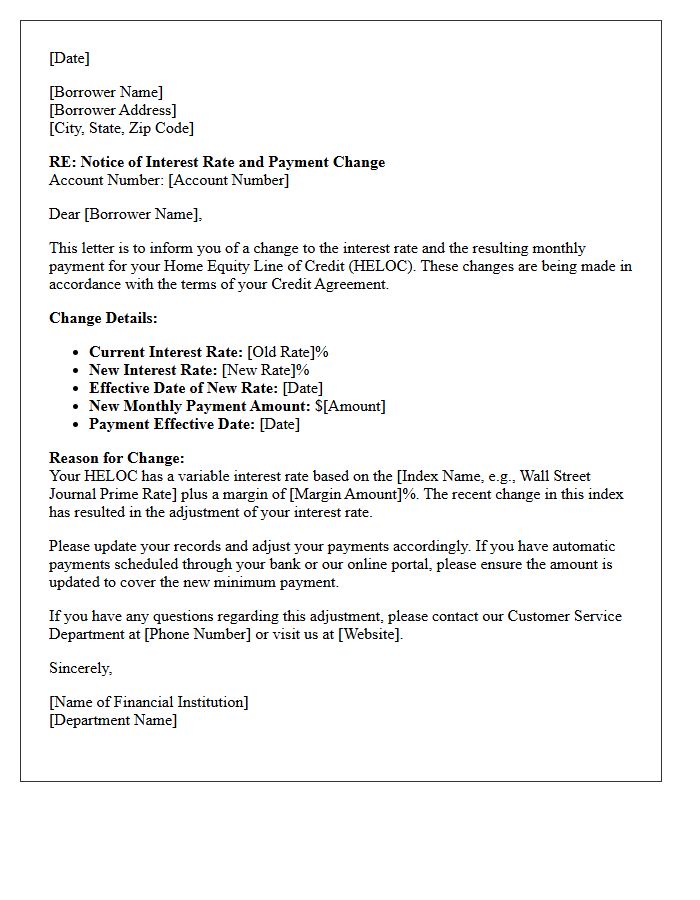

Home Equity Line Of Credit Rate Adjustment Letter

A Home Equity Line of Credit (HELOC) rate adjustment letter is a formal notice informing you of a change in your variable interest rate. This document typically outlines your new monthly payment, the current index value, and the margin applied by your lender. It is crucial to review these updates to manage your repayment budget effectively. Since HELOCs are secured by your property, understanding how these adjustments impact your debt obligations is essential for maintaining financial stability and avoiding potential foreclosure risks during periods of rising market rates.

What is a Notification of Interest Rate Adjustment?

A Notification of Interest Rate Adjustment is a formal communication sent by a lender to inform a borrower that the interest rate on their variable-rate loan or mortgage is changing. This notice outlines the new rate, the effective date, and the updated monthly payment amount.

When will I receive notice of an interest rate change?

Lenders are typically required to provide notice at least 30 to 45 days before the first payment at the new rate is due. This timeframe allows borrowers to adjust their budgets or explore refinancing options before the higher or lower payment takes effect.

Why did my loan's interest rate adjust?

Your interest rate adjusted because your loan is a variable or adjustable-rate product tied to a specific financial index, such as the SOFR or Prime Rate. When market benchmarks fluctuate, your rate is recalculated by adding a predetermined margin to the current index value.

How is my new monthly payment calculated after an adjustment?

The new monthly payment is calculated based on the remaining principal balance of your loan, the newly adjusted interest rate, and the remaining term of the loan. This ensures that the loan will still be fully paid off by the original maturity date.

Can I dispute an interest rate adjustment?

Interest rate adjustments are dictated by the terms of your original loan agreement. However, if you believe there is a calculation error or if the notice period violates your contract, you should contact your loan servicer immediately to request a formal review of the adjustment.

Comments