The Market Risk Supervisory Letter provides essential regulatory guidance for financial institutions to manage exposure effectively. It outlines expectations for robust internal controls, stress testing, and valuation methodologies to ensure capital adequacy against market fluctuations. This document is vital for compliance officers navigating evolving banking standards. To streamline your reporting process, below are some ready to use template.

Image cover: Effective Market Risk Supervisory Letter Templates and Best Practices

Letter Samples List

- Market Risk Examination Supervisory Letter

- Interest Rate Risk Management Supervisory Letter

- Trading Book Exposure Assessment Letter

- Foreign Exchange Risk Supervisory Letter

- Value At Risk Model Validation Supervisory Letter

- Market Risk Capital Adequacy Supervisory Letter

- Asset Liability Management Supervisory Letter

- Derivatives Trading Market Risk Letter

- Systemic Market Risk Evaluation Letter

- Commodity Price Risk Supervisory Letter

- Market Risk Stress Testing Supervisory Letter

- Market Risk Governance Assessment Letter

- Hedging Strategy Compliance Supervisory Letter

- Liquidity And Market Risk Evaluation Letter

Market Risk Examination Supervisory Letter

The Market Risk Examination Supervisory Letter is a critical regulatory document issued by banking supervisors to evaluate a financial institution's exposure to market volatility. It assesses the adequacy of internal controls, risk measurement techniques, and capital adequacy frameworks. Regulators use these findings to ensure banks can withstand adverse price movements in interest rates, equities, and commodities. Compliance requires robust stress testing and governance practices to mitigate systemic threats. Understanding these guidelines is essential for maintaining regulatory standing and ensuring the long-term financial stability of trading and investment portfolios.

Interest Rate Risk Management Supervisory Letter

The Interest Rate Risk Management Supervisory Letter outlines critical expectations for financial institutions to identify and mitigate balance sheet vulnerabilities. Regulators emphasize that boards must maintain active oversight and robust modeling techniques to measure sensitivity. Effective management requires stress testing against significant rate fluctuations and ensuring adequate capital buffers. Institutions should implement comprehensive internal controls and independent audits to validate their risk assessment frameworks. Adhering to these guidelines helps maintain liquidity and long-term financial stability in volatile market environments.

Trading Book Exposure Assessment Letter

The Trading Book Exposure Assessment Letter is a critical regulatory document used by financial institutions to verify the classification of assets. It ensures that market risk exposures are accurately mapped to the trading book rather than the banking book. This assessment is vital for calculating Capital Adequacy Ratio (CAR) requirements under Basel III frameworks. By documenting liquidity and intent, banks demonstrate compliance to regulators, preventing capital arbitrage and ensuring that risk-weighted assets are transparently reported and properly buffered against potential market volatility.

Foreign Exchange Risk Supervisory Letter

The Foreign Exchange Risk Supervisory Letter provides critical guidance on managing currency exposure within financial institutions. It emphasizes that banks must implement robust internal controls to mitigate potential losses from fluctuating exchange rates. Key focus areas include maintaining adequate capital buffers, conducting regular stress tests, and ensuring comprehensive board oversight. By following these regulatory expectations, organizations protect their solvency and maintain market stability. Understanding these compliance standards is essential for any entity engaged in international transactions to avoid systemic financial risk and regulatory penalties.

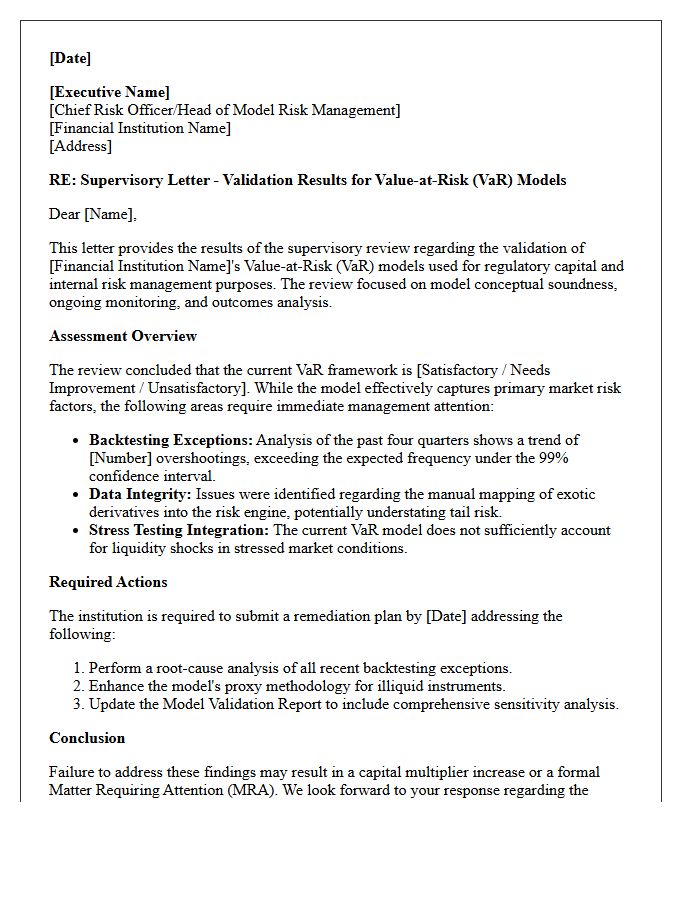

Value At Risk Model Validation Supervisory Letter

The SR 11-7 supervisory letter establishes critical regulatory expectations for Model Risk Management. It mandates that a Value at Risk (VaR) model must undergo rigorous independent validation to ensure accuracy. This process includes evaluating conceptual soundness, ongoing monitoring, and outcomes analysis like backtesting. Effective validation mitigates financial risk by identifying model limitations and potential reporting errors. Financial institutions must maintain comprehensive documentation and strong internal governance to comply with these standards, ensuring that risk estimates remain reliable under diverse market conditions.

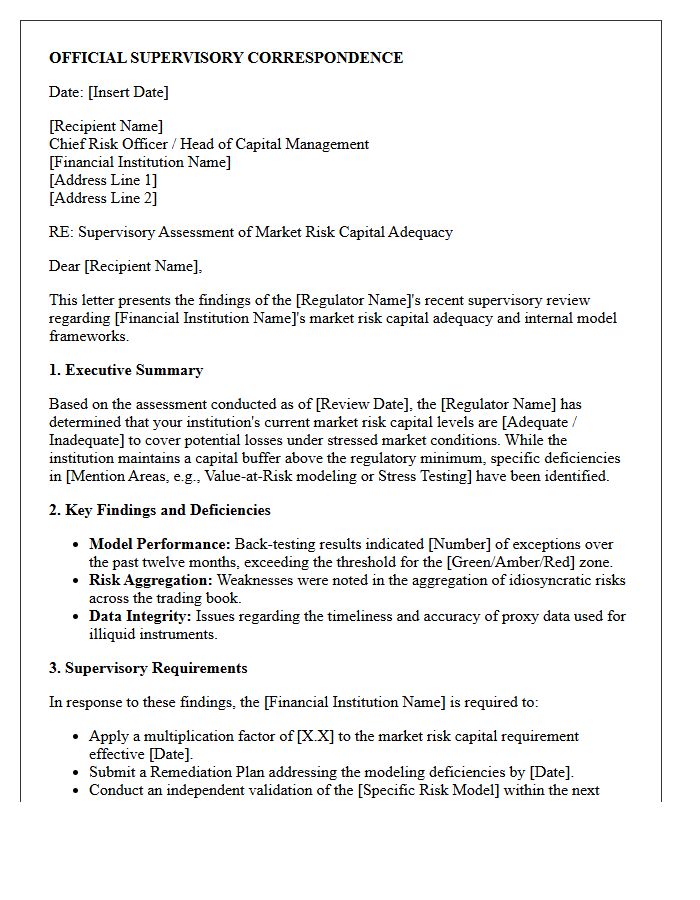

Market Risk Capital Adequacy Supervisory Letter

The Market Risk Capital Adequacy supervisory letter outlines essential regulatory expectations for financial institutions managing trading book exposures. It focuses on the Fundamental Review of the Trading Book (FRTB) standards to ensure banks maintain sufficient buffers against price volatility. Key requirements include robust internal models, standardized risk measurement approaches, and strict liquidity horizons. Compliance ensures financial stability by aligning capital requirements with actual portfolio risks. Supervisors use these guidelines to evaluate a firm's risk management framework and its ability to withstand extreme market stress events through rigorous sensitivity analysis and reporting.

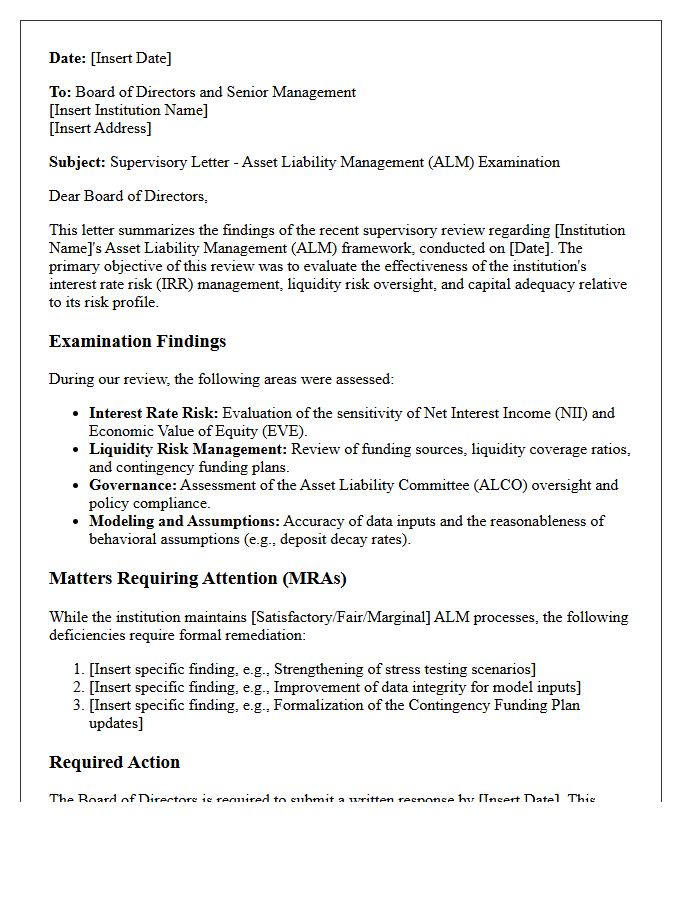

Asset Liability Management Supervisory Letter

The Asset Liability Management (ALM) Supervisory Letter provides critical regulatory guidance for financial institutions to manage interest rate risk and liquidity. It outlines expectations for robust board oversight, comprehensive risk modeling, and effective stress testing frameworks. Examiners use these standards to ensure banks maintain adequate capital buffers against market volatility. Compliance requires a disciplined balance sheet strategy to mitigate mismatches between assets and liabilities, ensuring long-term financial stability and institutional safety.

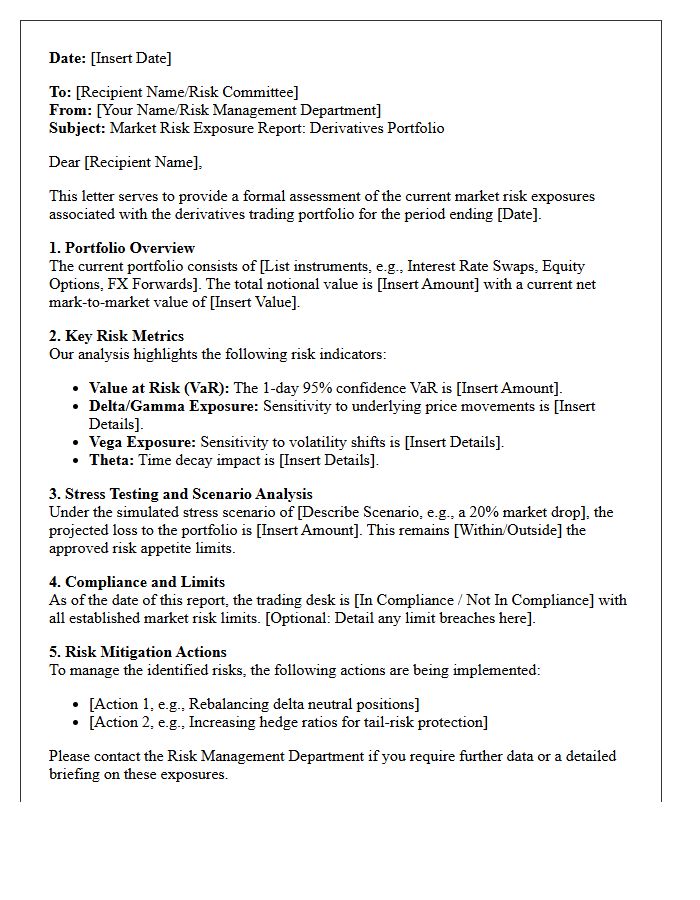

Derivatives Trading Market Risk Letter

A Derivatives Trading Market Risk Letter is a formal document used to outline potential financial exposures resulting from price fluctuations. It serves as a risk disclosure statement, ensuring that all parties understand the volatility and leverage inherent in derivative contracts. The letter typically specifies internal limits, hedging strategies, and compliance protocols required to mitigate adverse market movements. Its primary goal is to establish transparency and institutional accountability, protecting the firm's capital against unexpected shifts in interest rates, currencies, or underlying asset values during active trading periods.

Systemic Market Risk Evaluation Letter

A Systemic Market Risk Evaluation Letter is a formal notification issued by regulators or financial institutions to identify potential instability within the broader financial ecosystem. It focuses on contagion effects where the failure of one entity could trigger a widespread market collapse. These letters outline specific vulnerabilities, such as excessive leverage or liquidity shortages, requiring firms to implement immediate mitigation strategies. Understanding this evaluation is crucial for maintaining financial oversight and ensuring that individual institutional weaknesses do not evolve into systemic crises that threaten global economic security.

Commodity Price Risk Supervisory Letter

The Commodity Price Risk Supervisory Letter provides critical guidance for financial institutions managing exposures to volatile markets. It emphasizes that banks must maintain robust internal controls and comprehensive risk management frameworks to mitigate potential losses. Supervisors expect boards to oversee effective hedging strategies and conduct regular stress testing to evaluate market fluctuations. Proper governance and accurate reporting are essential to ensure that commodity-related activities do not compromise an institution's overall safety and soundness. Understanding these regulatory expectations is vital for maintaining compliance during periods of extreme price instability.

Market Risk Stress Testing Supervisory Letter

The Market Risk Stress Testing Supervisory Letter, often associated with SR 11-7 and SR 15-18, outlines regulatory expectations for financial institutions to assess vulnerability under extreme scenarios. It emphasizes the need for robust governance, sound conceptual frameworks, and rigorous model validation. Banks must utilize diverse stress scenarios to capture non-linear risks and potential liquidity shocks. This supervisory guidance ensures that capital adequacy is maintained during volatile periods, requiring continuous compliance and comprehensive reporting to demonstrate resilience against adverse market movements and systemic threats.

Market Risk Governance Assessment Letter

A Market Risk Governance Assessment Letter is a formal regulatory document evaluating an institution's oversight frameworks. It validates that the board of directors and senior management effectively monitor financial exposure arising from market fluctuations. The letter focuses on the adequacy of risk appetite statements, internal controls, and limit structures. By addressing compliance gaps, it ensures the firm maintains robust policies to mitigate potential losses. This assessment is critical for demonstrating regulatory transparency and ensuring that systemic stability is maintained through disciplined risk management practices and independent validation protocols.

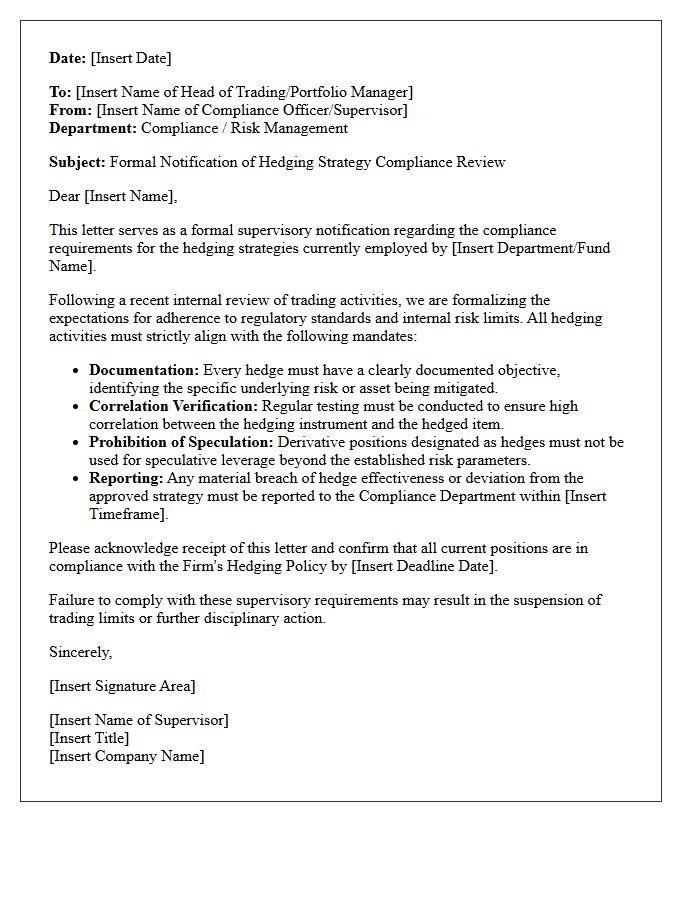

Hedging Strategy Compliance Supervisory Letter

The Hedging Strategy Compliance Supervisory Letter outlines critical regulatory expectations for financial institutions managing risk. It emphasizes that hedging activities must align with internal policies and risk management frameworks to prevent speculative trading. Supervisors focus on the effectiveness of internal controls, accurate reporting, and governance protocols. Compliance requires demonstrating that hedges are intended to mitigate specific exposures rather than generate independent profit. Ensuring proper documentation and regular audits is essential to satisfy regulatory oversight and maintain institutional stability under current financial standards.

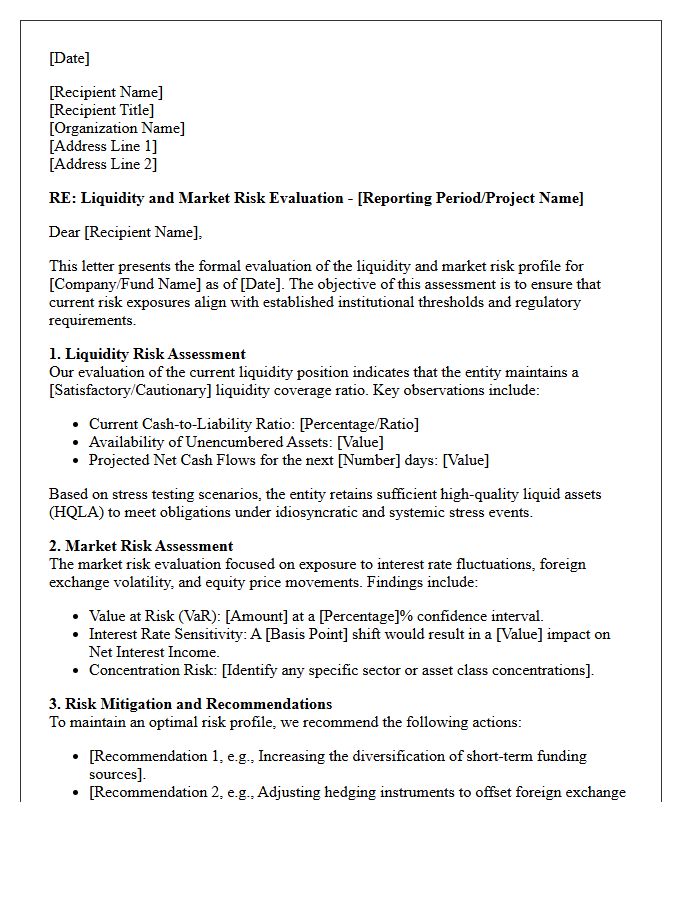

Liquidity And Market Risk Evaluation Letter

The Liquidity and Market Risk Evaluation Letter is a formal document used by financial institutions to assess a portfolio's ability to meet obligations. It identifies potential liquidity mismatches and measures sensitivity to fluctuating market variables like interest rates. This letter ensures regulatory compliance and verifies that an entity maintains sufficient cash reserves to withstand periods of high volatility. By evaluating these risks, organizations can implement effective mitigation strategies, protecting their financial stability against sudden asset devaluations or unexpected capital outflows during stressed market conditions.

What is a Market Risk Supervisory Letter?

A Market Risk Supervisory Letter is an official communication issued by financial regulators to banking institutions, outlining specific expectations, deficiencies, or updates regarding the management and measurement of market-related financial risks.

What are the primary objectives of Market Risk Supervisory guidance?

The primary objectives are to ensure that institutions maintain sufficient capital against potential losses, implement robust internal controls, and adhere to standardized risk measurement frameworks like Value at Risk (VaR) or Fundamental Review of the Trading Book (FRTB).

Which financial institutions are subject to Market Risk Supervisory oversight?

Oversight typically applies to large banking organizations and financial institutions with significant trading activity or those that meet specific asset thresholds defined by regulatory bodies such as the Federal Reserve, OCC, or FDIC.

What are common deficiencies highlighted in Market Risk Supervisory Letters?

Common deficiencies often include inadequate stress testing scenarios, weaknesses in model risk management, insufficient data governance, and failure to align internal risk appetite statements with actual trading floor activities.

How should an institution respond to a Supervisory Letter regarding market risk?

Institutions should provide a formal written response that includes a detailed remediation plan, specific timelines for addressing regulatory concerns, and evidence of senior management oversight to ensure ongoing compliance with safety and soundness standards.

Comments