Banks issue a Warning Letter for Excessive Regulation D Violations when savings account transfer limits are repeatedly exceeded. Federal rules restrict certain withdrawals, and non-compliance can lead to account reclassification or closure. Understanding these notifications helps maintain your financial standing and avoid unnecessary penalties. To help you draft a professional notice, below are some ready to use template.

Image cover: Official Notice: Excessive Regulation D Violations and Account Restrictions templates

Letter Samples List

- Initial Warning Letter for Regulation D Transfer Violations

- Second Warning Letter for Excessive Savings Account Transactions

- Final Warning Letter Prior to Account Conversion

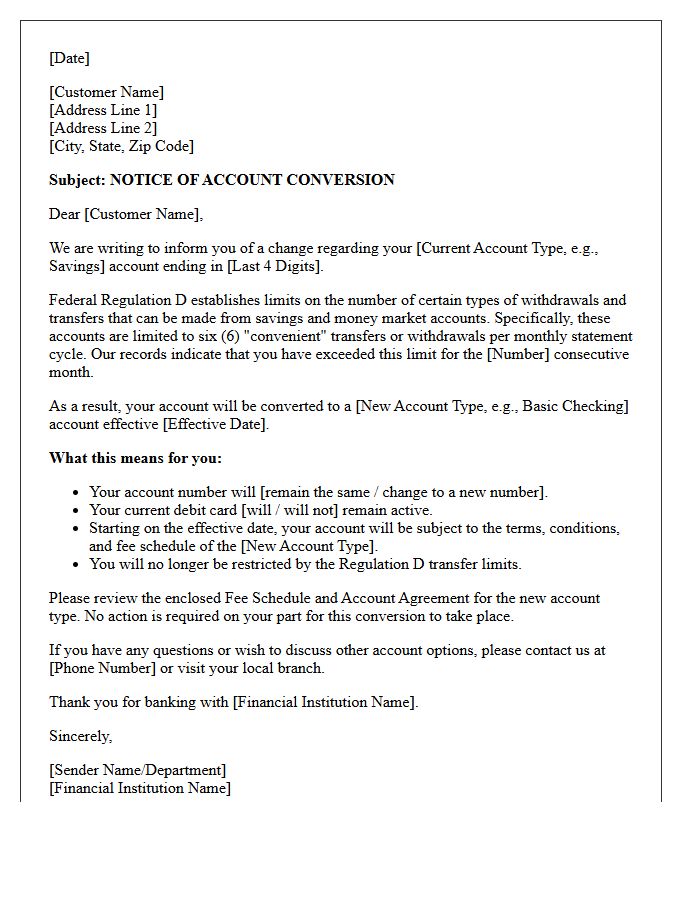

- Account Conversion Notification Letter Due to Regulation D Limits

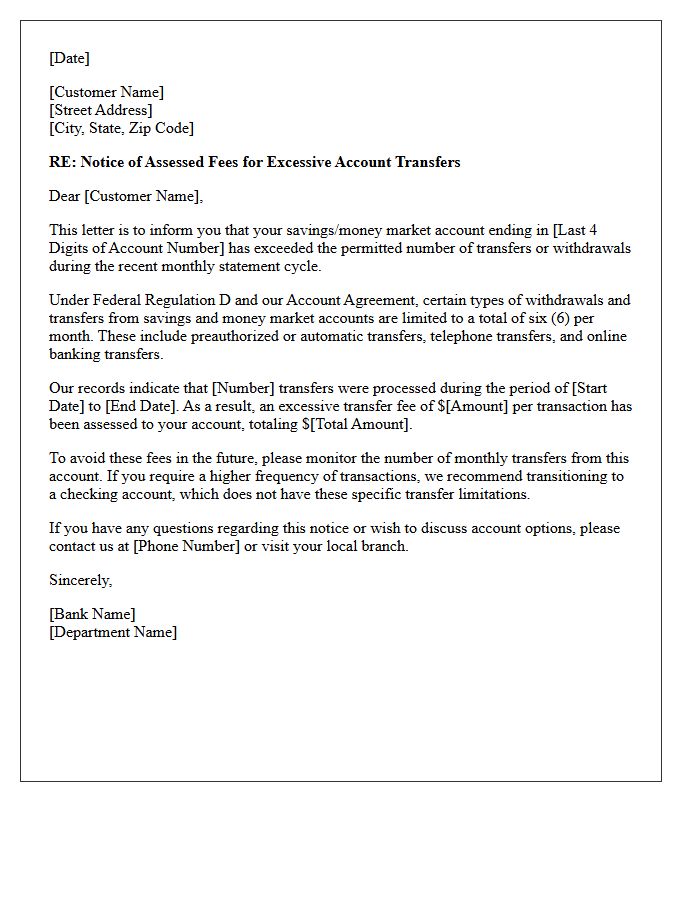

- Notice Letter of Assessed Fees for Excessive Regulation D Transfers

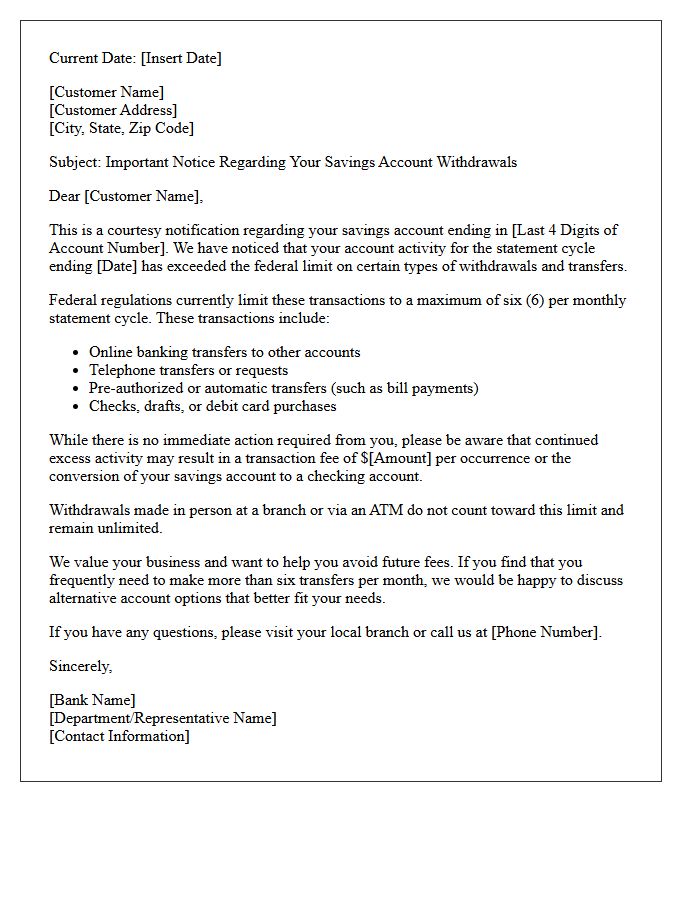

- First Courtesy Letter for Exceeding Federal Withdrawal Limits

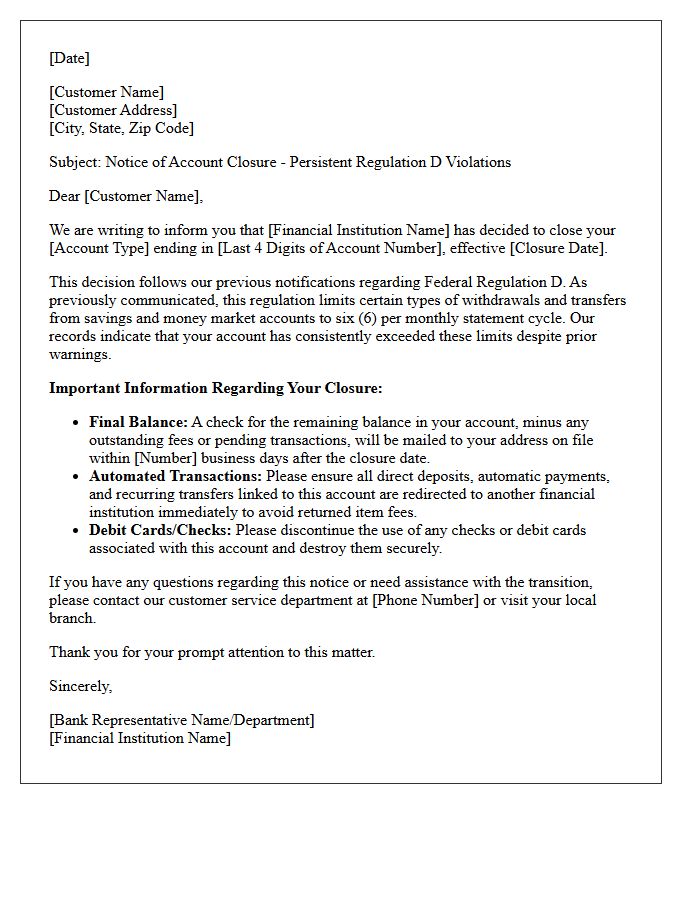

- Account Closure Letter for Persistent Regulation D Violations

- Acknowledgment Letter of Regulation D Compliance Requirements

- Restrictive Action Letter for Money Market Account Violations

- Federal Regulation D Policy Reminder Letter

- Imminent Account Reclassification Letter for Excessive Withdrawals

- Compliance Violation Letter Regarding Savings Account Transfers

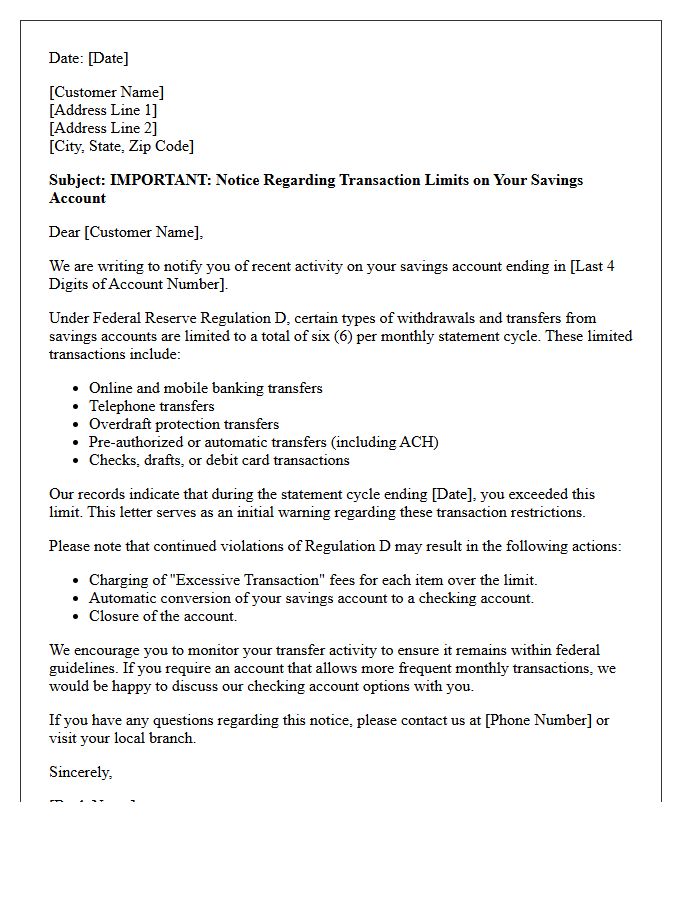

Initial Warning Letter for Regulation D Transfer Violations

An initial warning letter for Regulation D transfer violations notifies account holders about exceeding the monthly limit on specific savings withdrawals. While the Federal Reserve suspended the mandatory six-transfer cap under Regulation D, many financial institutions still enforce internal policies to maintain liquidity. Receiving this notice serves as a formal alert that continued excessive transfers may lead to account reclassification, conversion into a checking account, or potential closure. It is essential to monitor automated transfers to ensure compliance with your bank's specific transactional limits and avoid associated penalty fees.

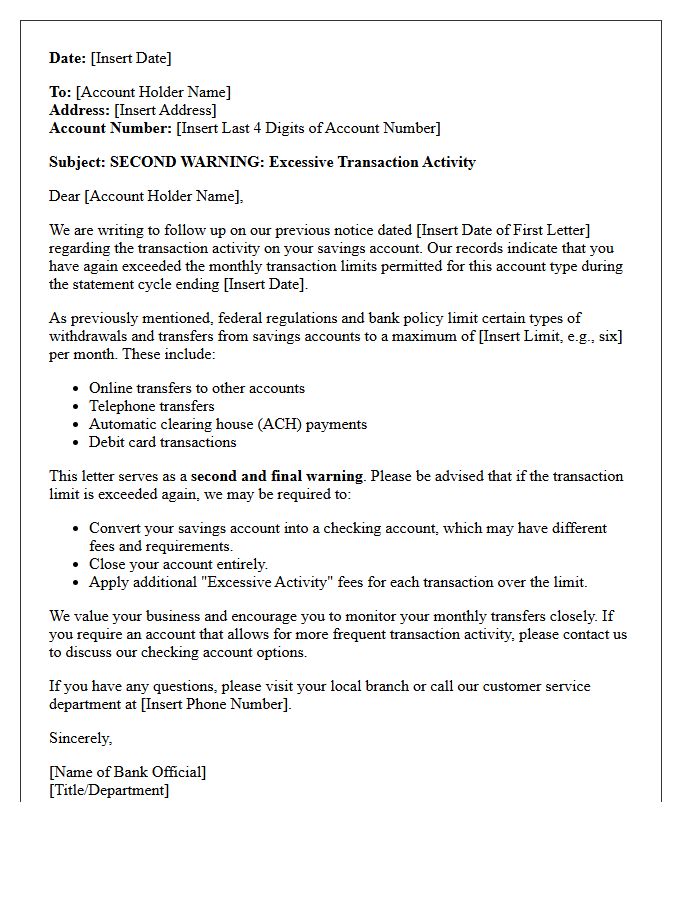

Second Warning Letter for Excessive Savings Account Transactions

A second warning letter for excessive savings account transactions indicates a repeated violation of federal or bank-specific limits. Most institutions restrict convenient withdrawals to six per month. Exceeding this threshold again may lead to your account being reclassified as a checking account or permanent closure. It is crucial to monitor your monthly transfers and automate your finances to avoid additional penalties. To maintain your banking compliance, consider moving excess funds to a checking account to manage frequent spending and prevent further regulatory interventions.

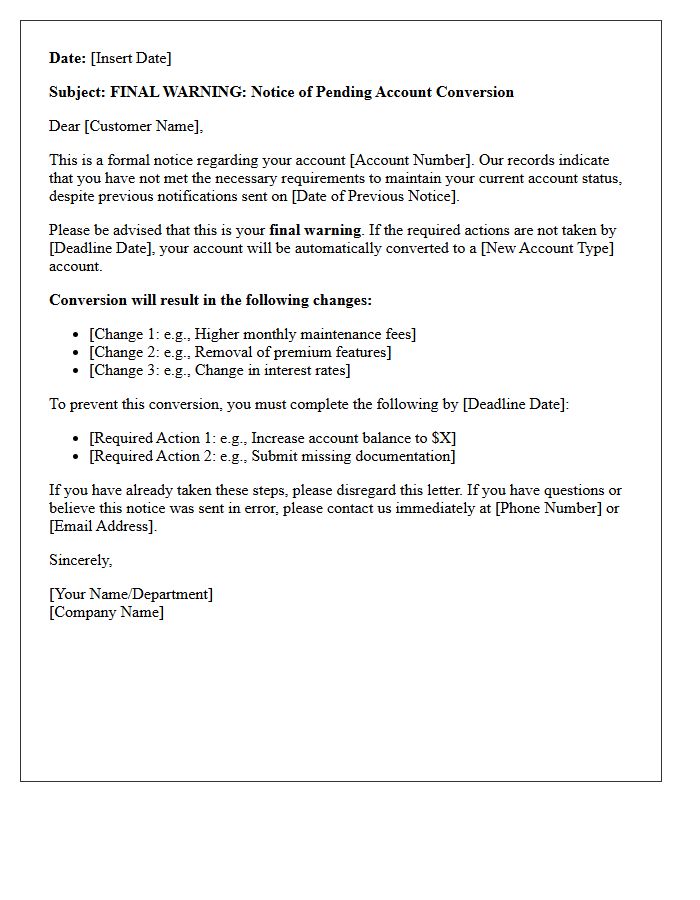

Final Warning Letter Prior to Account Conversion

A final warning letter serves as a critical notice regarding an imminent account conversion. This document specifies that failure to settle outstanding balances or meet compliance requirements will result in your account status being permanently changed. It often involves a shift from active to collections or a downgrade in service tier. To prevent this transition, you must take immediate action by the deadline stated in the letter. Addressing these issues promptly is essential to protect your credit standing and maintain uninterrupted access to your professional financial or service-based agreements.

Account Conversion Notification Letter Due to Regulation D Limits

Your bank sends an Account Conversion Notification Letter when you exceed federal transaction limits. While Regulation D restrictions on savings transfers were technically suspended, many institutions still enforce monthly caps to maintain account classification. If you repeatedly surpass these limits, the bank is legally permitted to convert your savings into a checking account. This change may result in lower interest rates or new monthly service fees. To avoid automatic conversion, monitor your withdrawal frequency and ensure your banking habits align with current account terms and federal guidelines.

Notice Letter of Assessed Fees for Excessive Regulation D Transfers

A Notice Letter of Assessed Fees for Excessive Regulation D Transfers informs account holders that they exceeded the monthly limit of six convenient withdrawals from a savings or money market account. Under federal rules, exceeding these limits triggers per-transaction penalties or potential account conversion to checking. While the Federal Reserve recently suspended the mandatory enforcement of these limits, many banks still maintain internal policies to manage liquidity. Monitoring your automated transfers and third-party payments is essential to avoid unexpected costs and ensure your account remains in good standing with the financial institution.

First Courtesy Letter for Exceeding Federal Withdrawal Limits

A First Courtesy Letter is a formal notification from your bank regarding Regulation D compliance. This notice warns that you have surpassed the six-transaction limit for certain withdrawals or transfers from your savings account within a monthly statement cycle. While federal restrictions were recently relaxed, many institutions still enforce these caps. Receiving this letter serves as an initial warning to adjust your banking habits; continued violations may result in your savings account being converted into a checking account or incurring excessive usage fees per transaction.

Account Closure Letter for Persistent Regulation D Violations

An account closure letter is a formal notice sent by financial institutions when a customer repeatedly exceeds the six-transaction limit on savings or money market accounts. Under Regulation D, banks must monitor and restrict certain types of convenient withdrawals. If persistent violations occur after initial warnings, the bank is legally permitted to terminate the banking relationship. This letter outlines the effective closing date, the reason for termination, and instructions for receiving remaining funds via check, ensuring the institution maintains compliance with federal reserve requirements.

Acknowledgment Letter of Regulation D Compliance Requirements

An acknowledgment letter confirms that an investor understands and meets the specific Regulation D compliance requirements. This document is essential for private placements, ensuring participants qualify as accredited investors under SEC guidelines. By signing, investors verify they have received necessary disclosures and acknowledge the restricted nature of the securities. This process protects the issuer by maintaining the registration exemption and documenting due diligence. It serves as a legal safeguard, confirming that all parties adhere to federal securities laws during the private capital raising process.

Restrictive Action Letter for Money Market Account Violations

A Restrictive Action Letter is a formal notification issued by financial institutions when a customer exceeds the federal limit of six monthly withdrawals from a Money Market Account. Under Regulation D, frequent transfers or check payments trigger this warning. Failure to comply can result in the bank closing your account or converting it into a standard checking account with lower interest rates. To avoid penalties, monitor your transaction volume and use linked accounts for high-frequency spending. Understanding these transaction limits is essential for maintaining your account's status and financial benefits.

Federal Regulation D Policy Reminder Letter

A Federal Regulation D Policy Reminder Letter informs customers about the six-transfer limit previously imposed on savings and money market accounts. Although the Federal Reserve suspended these enforcement requirements under Regulation D, many financial institutions still monitor transaction frequency. This letter serves as a formal notice regarding potential excessive withdrawal fees or account reclassification if monthly limits are surpassed. It is essential to review your bank's specific terms, as they maintain the right to restrict transfers to ensure account stability and regulatory compliance.

Imminent Account Reclassification Letter for Excessive Withdrawals

An Imminent Account Reclassification Letter is a formal notice sent when a savings account exceeds the federal limit of six monthly transfers. Under Regulation D guidelines, banks monitor these excessive withdrawals to maintain the account's status. If non-compliance continues, the financial institution is legally required to convert your savings into a checking account, which may lack interest benefits or carry higher fees. To avoid this permanent reclassification, ensure you limit outgoing transactions and monitor your monthly statement cycle closely.

Compliance Violation Letter Regarding Savings Account Transfers

A compliance violation letter regarding savings accounts typically refers to exceeding the Regulation D limit on convenient transfers. Federal rules previously restricted users to six "convenient" withdrawals per month. If you surpass this threshold, your bank may send a warning notice, charge excessive activity fees, or convert your account into a checking sub-type. To maintain regulatory compliance, monitor your monthly automated transfers and bill payments. While some banks have relaxed these limits following policy updates, many still enforce internal restrictions to manage liquidity and ensure account status integrity.

What is a Regulation D violation warning letter?

A Regulation D violation warning letter is a formal notice sent by a financial institution to a customer who has exceeded the federal limit of six "convenient" withdrawals or transfers from a savings or money market account within a single monthly statement cycle.

What happens if I continue to violate Regulation D limits?

If you continue to exceed the monthly transaction limit after receiving a warning, the bank is required by federal guidelines to take corrective action, which may include charging excessive usage fees, converting your savings account into a checking account, or closing the account entirely.

Which types of transactions count toward the Regulation D limit?

Transactions that count toward the limit include online banking transfers, mobile app transfers, overdraft protection transfers, phone transfers, and payments made to third parties via check, debit card, or ACH. In-person withdrawals at a branch or ATM typically do not count toward this limit.

Can I dispute a Warning Letter for Excessive Regulation D Violations?

While you can contact your bank to clarify specific transactions, Regulation D is a federal oversight requirement. If the transactions were initiated by you or your authorized billers, the bank is legally obligated to issue the warning and enforce the transaction limits as defined by the Federal Reserve.

How can I avoid receiving future Regulation D violation notices?

To avoid violations, you should plan larger, less frequent transfers, use a checking account for primary bill payments and high-volume transactions, and utilize ATMs or in-branch tellers for withdrawals, as these methods generally do not count toward the six-transfer monthly limit.

Comments