Missing a payment can lead to a lapse in protection against water damage. A Flood Insurance Reinstatement Letter is a formal request to restore your policy and maintain continuous coverage for your property. Timely submission is crucial to avoid waiting periods and financial risk. To help you draft this document quickly, below are some ready to use template.

Image cover: Restoring Your Coverage: Flood Insurance Reinstatement Letter Templates and Guide

Letter Samples List

- Flood Insurance Reinstatement Request Letter

- Flood Insurance Reinstatement Approval Letter

- Flood Insurance Reinstatement Denial Letter

- Flood Insurance Reinstatement Appeal Letter

- Flood Insurance Policy Cancellation Notice Letter

- Flood Insurance Premium Past Due Warning Letter

- Flood Insurance Grace Period Expiration Letter

- Flood Insurance Reinstatement Application Letter

- Flood Insurance Missing Documentation Request Letter

- Flood Insurance Reinstatement Conditions Letter

- Flood Insurance Coverage Reinstatement Confirmation Letter

- Flood Insurance Declaration Of Reinstatement Letter

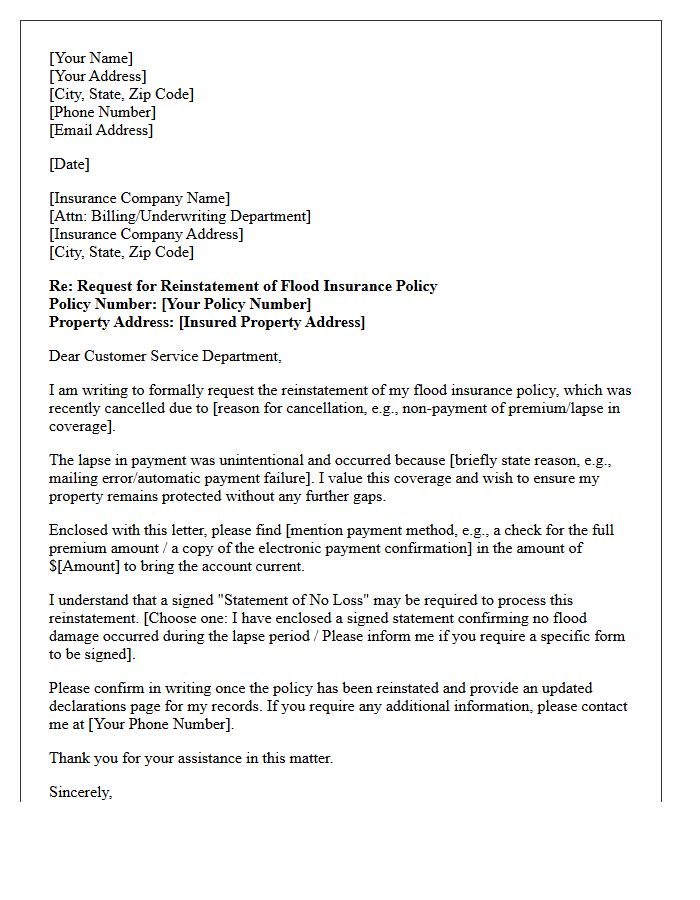

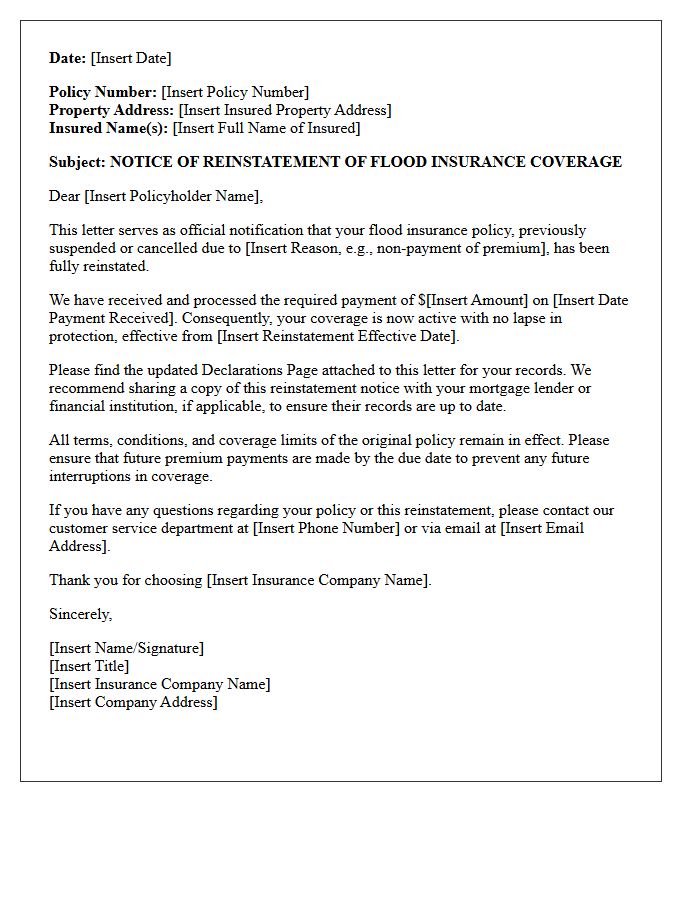

Flood Insurance Reinstatement Request Letter

A Flood Insurance Reinstatement Request Letter is a formal document sent to an insurer to restore a policy that has lapsed due to non-payment or missed deadlines. It is crucial to submit this request promptly to maintain continuous coverage and protect your property from financial loss. The letter must clearly state the policy number, the reason for the lapse, and be accompanied by the full premium payment. Timely reinstatement is essential to avoid a new 30-day waiting period and ensure your assets remain protected under the National Flood Insurance Program standards.

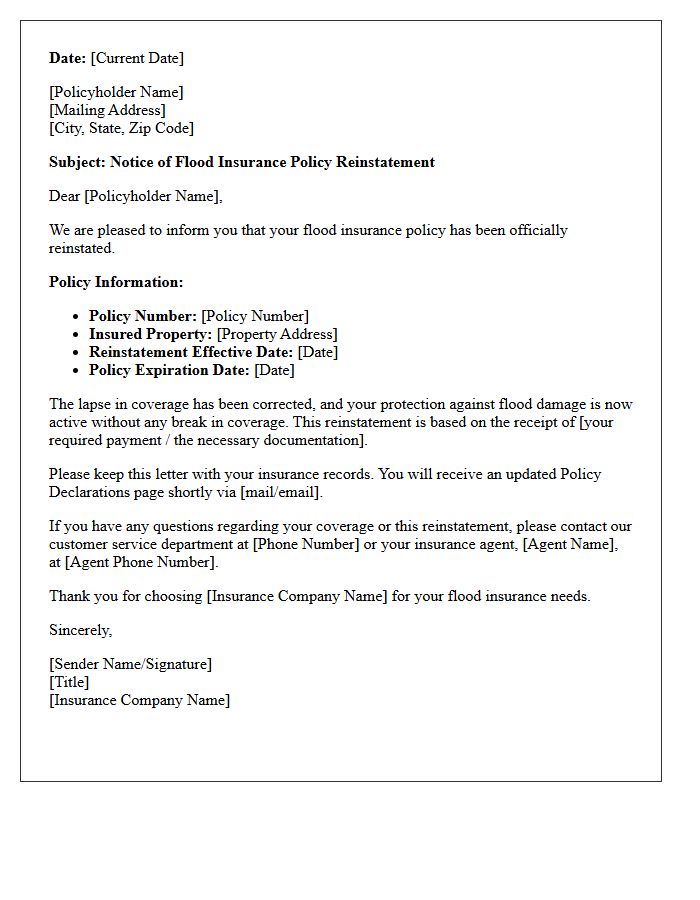

Flood Insurance Reinstatement Approval Letter

A Flood Insurance Reinstatement Approval Letter is a formal document from your provider confirming that a lapsed policy is active again. It typically requires the payment of overdue premiums and adherence to waiting periods. This letter is crucial for homeowners because it proves continuous coverage to mortgage lenders, ensuring compliance with loan requirements. Receiving this approval means your property is once again protected against rising water damage, restoring financial security after a temporary gap in protection. Always keep this document for your permanent insurance records.

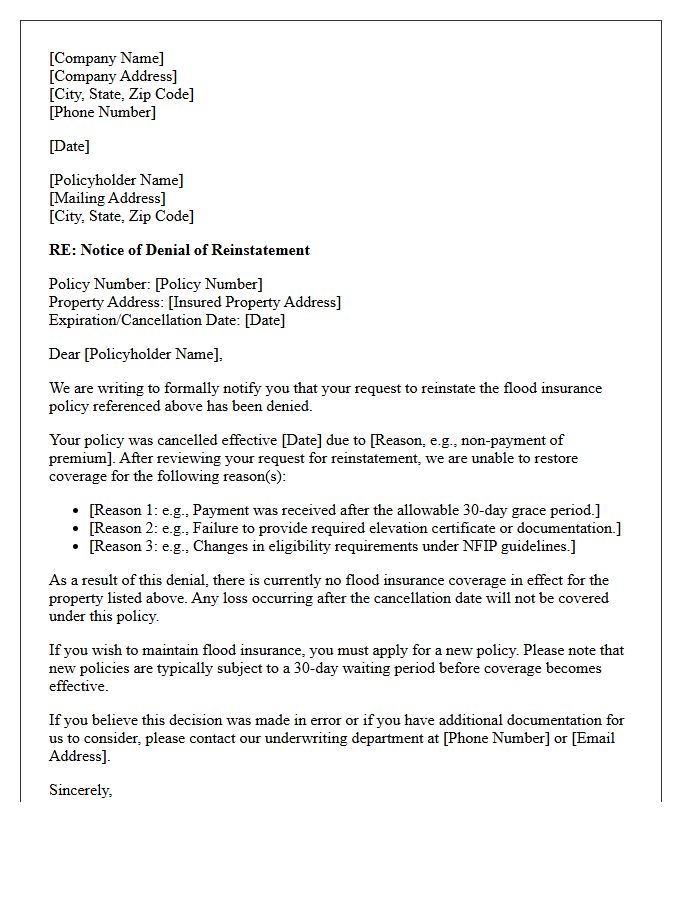

Flood Insurance Reinstatement Denial Letter

A Flood Insurance Reinstatement Denial Letter notifies policyholders that their request to restore a lapsed policy has been rejected. This typically occurs due to missed payment deadlines or failure to meet specific underwriting requirements during the grace period. Receiving this notice means your property currently lacks financial protection against rising water damage. To contest a denial, you must act quickly by providing proof of payment or correcting documentation errors. Failure to reinstate coverage may lead to a permanent policy cancellation and a potential lapse in mandatory lender requirements.

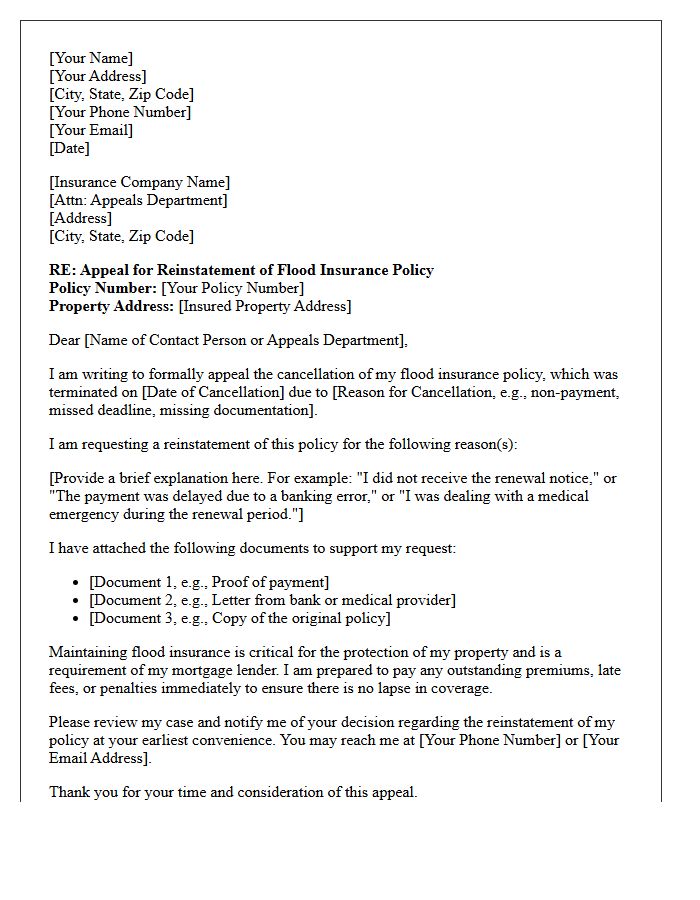

Flood Insurance Reinstatement Appeal Letter

A Flood Insurance Reinstatement Appeal Letter is a formal request sent to FEMA or a private insurer to restore a canceled policy. To be effective, the letter must clearly state your policy number and provide compelling evidence, such as proof of timely payment or a bank error. Clearly explain the reasons for the lapse and request a waiver for any late fees or missed deadlines. Including supporting documentation is essential for a successful outcome. Act quickly, as most reinstatement appeals have strict deadlines to maintain continuous coverage and protect your property assets.

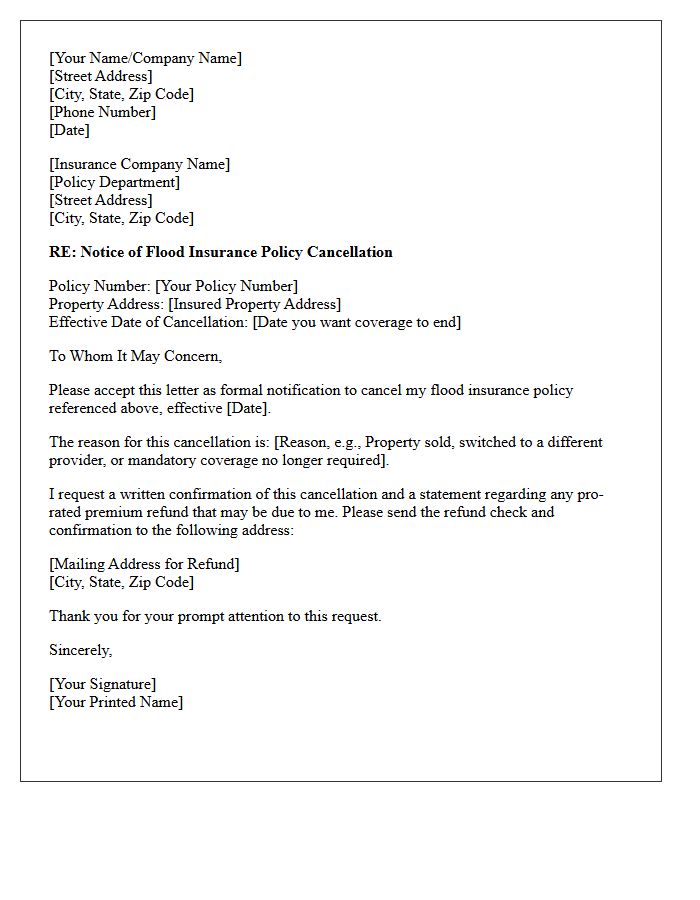

Flood Insurance Policy Cancellation Notice Letter

Receiving a Flood Insurance Policy Cancellation Notice Letter is a critical warning that your property coverage is terminating. This document typically outlines the specific reason for termination, such as non-payment of premiums, misrepresentation, or an increase in property risk. It is essential to act immediately to avoid a coverage lapse, which can lead to severe financial vulnerability and mortgage complications. Always verify the effective date of cancellation and contact your provider to discuss potential reinstatement options or to secure a new policy through the NFIP or private insurers.

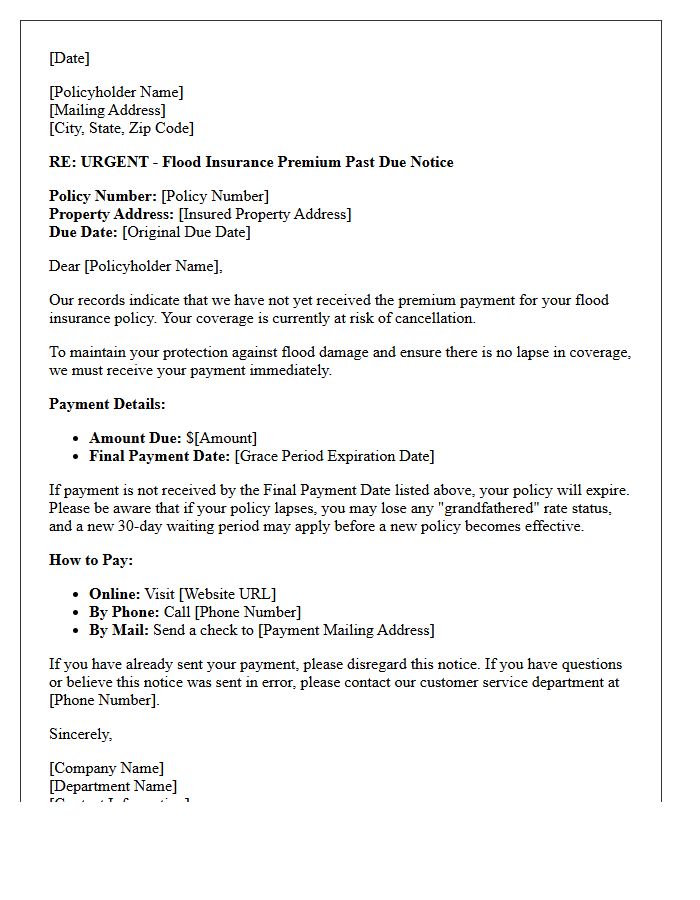

Flood Insurance Premium Past Due Warning Letter

Receiving a Flood Insurance Premium Past Due Warning Letter is a critical notice that your coverage is at risk of expiration. To maintain financial protection against water damage, you must submit payment before the grace period ends. Failure to pay will result in a lapse of coverage, meaning subsequent flood events will not be covered. Additionally, if you have a mortgage, your lender may force-place a more expensive policy to protect their interest. Always verify the payment deadline and policy number immediately to ensure continuous property protection.

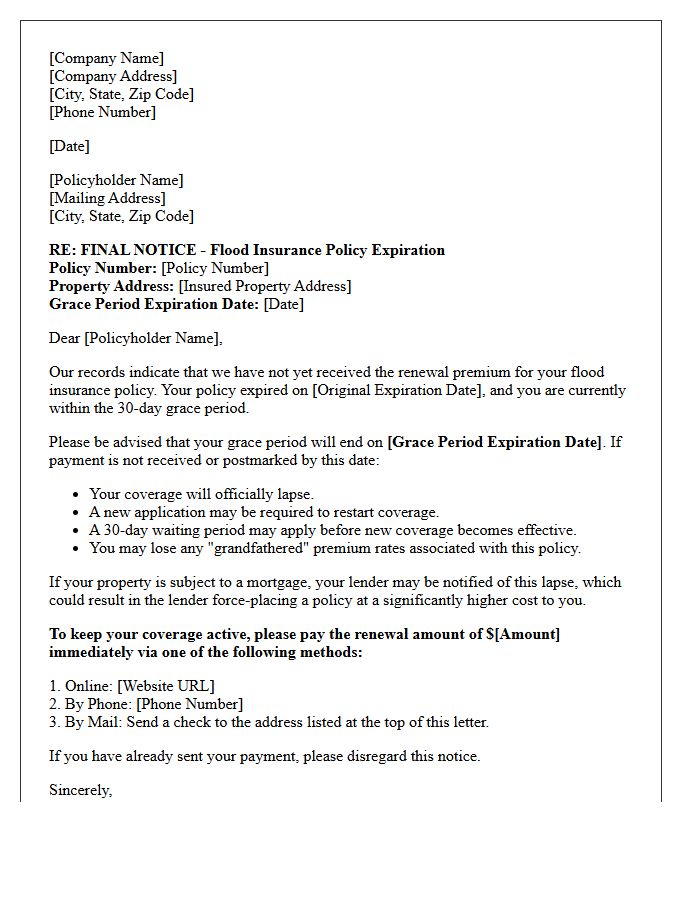

Flood Insurance Grace Period Expiration Letter

A Flood Insurance Grace Period Expiration Letter serves as a critical final notice that your policy has lapsed due to non-payment. Typically, NFIP policies offer a 30-day grace period to renew coverage. If payment is not received before this window closes, you lose protection against water damage and may face a waiting period for new coverage to take effect. Receiving this letter means your property is currently uninsured, which could also trigger a force-placed insurance requirement from your mortgage lender to protect their financial interest.

Flood Insurance Reinstatement Application Letter

A Flood Insurance Reinstatement Application Letter is a formal request to restore a lapsed policy. It must include your policy number, property address, and the specific reason for the payment gap. To ensure continuous coverage, homeowners must submit this letter alongside the full premium owed. Most carriers require a Statement of No Loss, certifying that no flood damage occurred during the inactive period. Timely submission is critical to avoid new waiting periods and maintain financial protection against water damage risks under National Flood Insurance Program guidelines.

Flood Insurance Missing Documentation Request Letter

A Flood Insurance Missing Documentation Request Letter is a formal notice sent by insurers to policyholders when specific compliance records are absent. To maintain active coverage and ensure eligibility for claims, you must provide requested items such as elevation certificates or photos promptly. Failure to submit these documents can lead to policy cancellation or higher premiums. Always verify the deadline mentioned in the letter to prevent a lapse in protection. Organizing your property records beforehand ensures a swift response and secures your financial safety against water damage risks.

Flood Insurance Reinstatement Conditions Letter

A Flood Insurance Reinstatement Conditions Letter is a formal notice sent by the NFIP or private carriers when a policy has lapsed due to non-payment. This document outlines the specific eligibility requirements and necessary actions, such as paying the full premium and submitting a signed "no loss" statement, to restore coverage. It is critical to respond within the specified grace period to avoid a permanent gap in protection. Reinstatement ensures your property remains continuously insured against water damage while maintaining compliance with mandatory mortgage lender requirements.

Flood Insurance Coverage Reinstatement Confirmation Letter

A Flood Insurance Coverage Reinstatement Confirmation Letter is a formal document verifying that a lapsed or cancelled policy is once again active. This letter confirms that the policyholder has successfully met all reinstatement requirements, such as paying overdue premiums or submitting required documentation. It serves as legal proof of protection against water damage risks. Homeowners should present this confirmation to their mortgage lender to ensure compliance with loan terms and avoid force-placed insurance. Always verify the effective date to ensure there are no remaining gaps in your property coverage.

Flood Insurance Declaration Of Reinstatement Letter

A Flood Insurance Declaration of Reinstatement Letter is a formal document confirming that a lapsed policy is once again active. This official notification is issued by the insurer after the policyholder pays the outstanding premium or resolves eligibility issues. It is crucial for homeowners to provide this letter to their mortgage lender to prove continuous coverage and avoid force-placed insurance. The document specifies the effective date of coverage restoration, ensuring the property is protected against future water damage claims without a gap in protection.

What is a Flood Insurance Reinstatement Letter?

A Flood Insurance Reinstatement Letter is an official document sent by an insurance provider confirming that a lapsed or cancelled policy has been restored to active status, typically after a missed premium payment has been received and processed.

What is the deadline to submit a payment for flood insurance reinstatement?

Under the National Flood Insurance Program (NFIP), you generally have a 30-day grace period from the policy expiration date to pay your premium. If payment is made after 30 days but within 90 days, a reinstatement letter may be issued, but a 30-day waiting period for coverage usually applies.

Will my coverage be continuous after receiving a reinstatement letter?

Coverage is only continuous if the full premium is paid within the 30-day grace period. If the reinstatement occurs after this window, there is typically a lapse in coverage, meaning any flood damage sustained during the inactive period will not be covered.

What information is included in a Flood Insurance Reinstatement Letter?

The letter includes the policy number, the effective dates of the reinstated coverage, the total premium amount received, and clear notification of whether there was a lapse in coverage or if the policy remains continuous.

Why did I receive a notice of reinstatement instead of a new policy?

A reinstatement letter is used when an existing policy is revived under the same terms and policy number. This is common when a payment is received late but within the underwriting guidelines, allowing the homeowner to maintain their previous rating status without starting a new application.

Comments