A High-Value Home Policy Renewal Adjustment Letter is an essential communication sent to policyholders when coverage terms or premiums change. This formal notice explains adjustments reflecting current property valuations and updated risk assessments for luxury estates. Ensuring clarity helps maintain client trust during the renewal process. To assist your communication efforts, below are some ready to use template.

Image cover: Effective High-Value Home Policy Renewal Adjustment Letter Templates

Letter Samples List

- High-Value Home Policy Renewal Adjustment Letter

- Premium Adjustment Notification Letter for Luxury Home Renewal

- Replacement Cost Valuation Adjustment Letter for Estate Policy Renewal

- Scheduled Property Limit Adjustment Letter for High-Value Home

- Inflation Guard Coverage Adjustment Letter for Luxury Property Renewal

- Deductible Modification Letter for High-Net-Worth Homeowner Renewal

- Appraisal Requirement Adjustment Letter for High-Value Home Policy

- Coverage Reassessment Letter for Premium Home Policy Renewal

- Catastrophe Risk Premium Adjustment Letter for Luxury Home Renewal

- Fine Art and Jewelry Schedule Adjustment Letter for Policy Renewal

- Security System Requirement Adjustment Letter for High-Value Home

- Comprehensive Renewal Terms Adjustment Letter for Luxury Estate

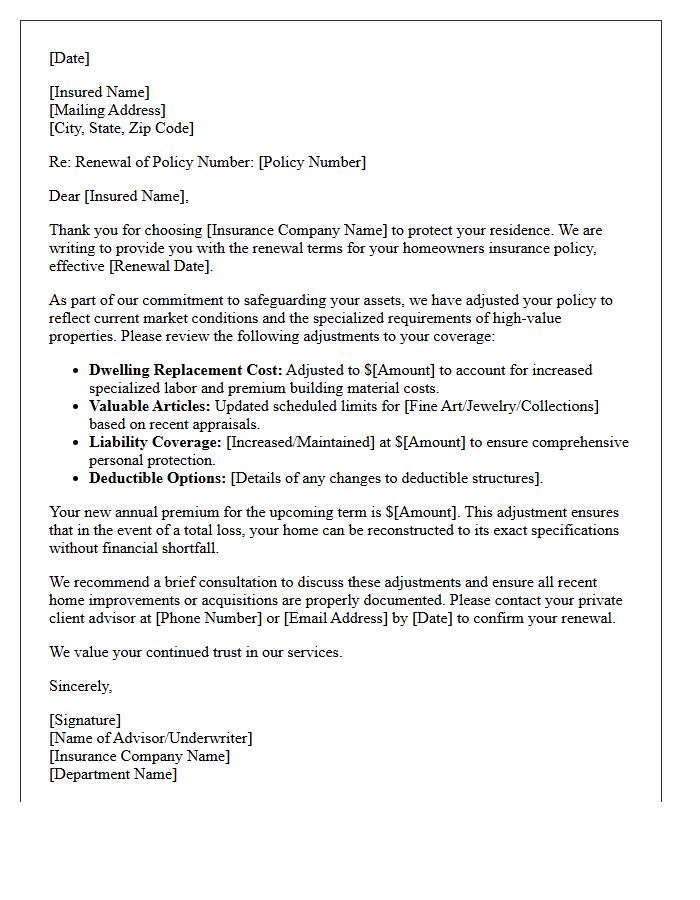

High-Value Home Policy Renewal Adjustment Letter

A High-Value Home Policy Renewal Adjustment Letter notifies policyholders of changes to their coverage, often reflecting inflationary trends and increased replacement costs. It is crucial to review the dwelling limit to ensure it aligns with current construction expenses. These adjustments prevent underinsurance, protecting your significant investment against total loss. Carefully examine any changes to deductibles or premium rates mentioned in the document. If your property has undergone recent renovations or upgrades, contact your insurer immediately to adjust your policy and maintain comprehensive protection for your luxury assets.

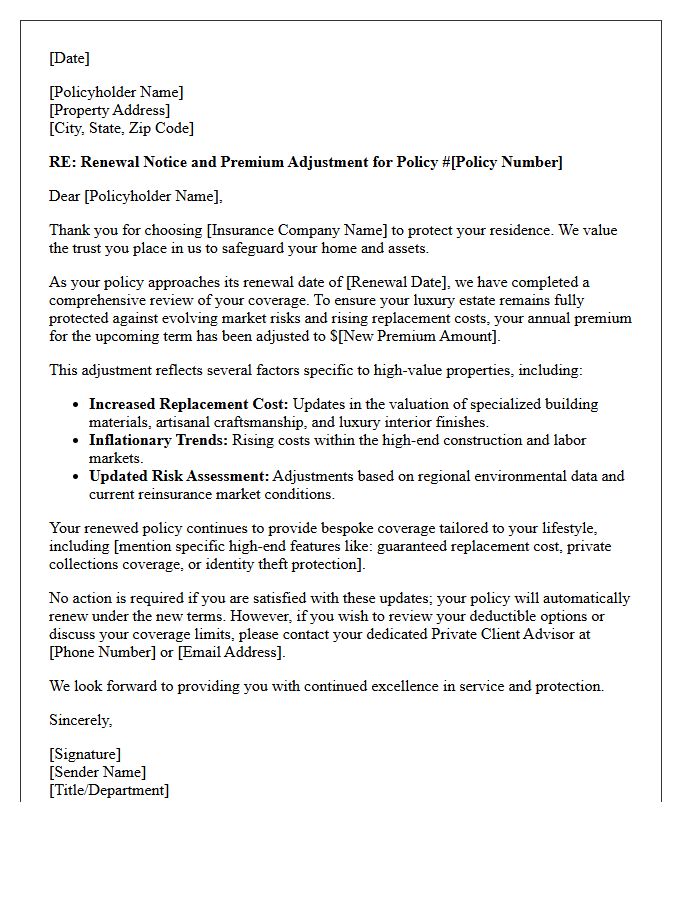

Premium Adjustment Notification Letter for Luxury Home Renewal

A Premium Adjustment Notification Letter informs policyholders of changes to their Luxury Home Insurance rates during the renewal period. This document outlines updated coverage terms, adjusted property valuations, and revised annual premiums based on current market risks. It is essential to review the policy schedule carefully to ensure your high-value assets remain fully protected. Homeowners should compare the new premium costs against previous terms and contact their broker to discuss potential discounts or coverage enhancements before the expiration date to maintain continuous protection for their estate.

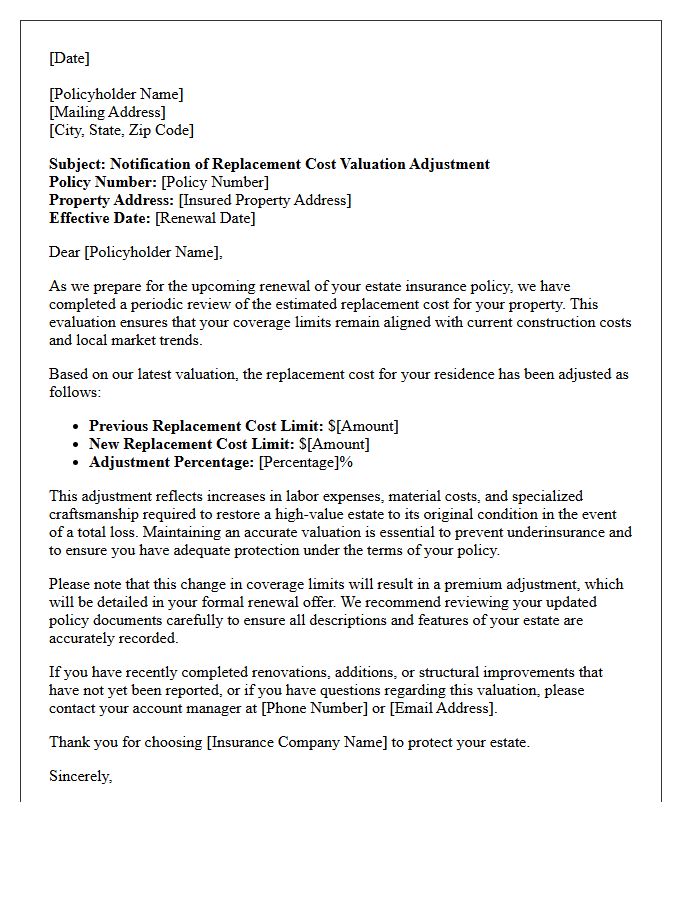

Replacement Cost Valuation Adjustment Letter for Estate Policy Renewal

A Replacement Cost Valuation Adjustment Letter is a critical notice during estate policy renewal. It informs policyholders that coverage limits have been updated to reflect current rebuilding costs rather than market value. Factors like inflation, material prices, and labor shortages often necessitate these increases. Reviewing this letter ensures your property remains fully protected against underinsurance risks. It is essential to verify that all structural improvements are accurately documented to maintain adequate financial security for the estate's assets under prevailing economic conditions.

Scheduled Property Limit Adjustment Letter for High-Value Home

A Scheduled Property Limit Adjustment Letter informs homeowners that the coverage limits for high-value assets like jewelry or fine art have been updated. Due to market fluctuations or recent appraisals, your current insurance may no longer reflect the actual replacement value of these items. Reviewing this document is essential to ensure your most precious belongings are fully protected against loss or theft. Adjusting these limits prevents potential out-of-pocket expenses, maintaining financial security for your high-value home and its contents through accurate, up-to-date valuations.

Inflation Guard Coverage Adjustment Letter for Luxury Property Renewal

An Inflation Guard Coverage Adjustment letter notifies luxury property owners of mandatory increases to their dwelling limits. This ensures policy values keep pace with the rising costs of specialized high-end construction materials and artisan labor. Without this automated adjustment, your residence may become underinsured, leading to significant financial gaps during a total loss. Reviewing this letter is essential to verify that your replacement cost accurately reflects current market trends, preserving the full value of your high-value assets and maintaining comprehensive financial protection for your estate.

Deductible Modification Letter for High-Net-Worth Homeowner Renewal

A Deductible Modification Letter is a critical formal notice sent during high-net-worth homeowner insurance renewals. It informs policyholders of mandatory increases to specific deductibles, often targeting risks like wind, hail, or water damage. These adjustments help carriers manage exposure in volatile markets while maintaining coverage limits for high-value estates. Reviewing this document is essential to understand your increased financial responsibility during a claim. If the new terms are unfavorable, you may need to negotiate higher premiums to buy back lower deductibles or explore alternative risk management strategies with your broker.

Appraisal Requirement Adjustment Letter for High-Value Home Policy

An Appraisal Requirement Adjustment Letter is a formal notification from insurers mandate updating a property valuation for high-value home coverage. As market costs fluctuate, your current replacement cost may no longer reflect accurate rebuilding expenses. This adjustment ensures your policy limits prevent underinsurance during a total loss. Homeowners must provide a certified appraisal to maintain guaranteed replacement cost endorsements. Failure to comply can result in coverage gaps or policy non-renewal. Keeping appraisals current protects your financial equity by aligning premium costs with the true upscale architectural value of your luxury residence.

Coverage Reassessment Letter for Premium Home Policy Renewal

A Coverage Reassessment Letter is a vital notice sent during your Premium Home Policy Renewal. It highlights necessary adjustments to your dwelling limits and protection levels based on current construction costs and inflation. Reviewing this document ensures you avoid underinsurance, confirming your property remains fully protected against total loss. Carefully compare these updates to your existing coverage to maintain adequate financial security and adjust your premiums accordingly for the upcoming term.

Catastrophe Risk Premium Adjustment Letter for Luxury Home Renewal

A Catastrophe Risk Premium Adjustment Letter notifies owners of high-value estates about changes in reinsurance costs driven by natural disasters. During a luxury home renewal, carriers issue this notice to explain why premiums rose despite a clean claims history. It highlights how regional hazard modeling and increased secondary perils, such as wildfires or storms, impact global risk pools. Understanding this document is vital for asset protection, as it justifies the higher rates required to maintain comprehensive coverage and solvency for complex, multi-million dollar properties in volatile climate zones.

Fine Art and Jewelry Schedule Adjustment Letter for Policy Renewal

A Fine Art and Jewelry Schedule Adjustment Letter is essential during policy renewal to ensure valuation accuracy. This document allows policyholders to update their itemized inventory, reflecting recent acquisitions or sales. Because high-value assets fluctuate in market price, providing current professional appraisals prevents underinsurance. Timely adjustments guarantee that your most precious collectibles and jewelry pieces are protected at their true replacement cost. Carefully review your scheduled items annually to maintain comprehensive coverage and avoid financial gaps in the event of a total loss.

Security System Requirement Adjustment Letter for High-Value Home

A Security System Requirement Adjustment Letter is a formal request to your insurer to modify specific protective device mandates for a high-value home. This document justifies deviations from standard policy requirements by highlighting alternative safety measures, such as 24/7 onsite guards or advanced perimeter sensors. Providing professional documentation and expert security assessments is essential to ensure continuous coverage. Successfully negotiating these terms prevents potential claim denials while maintaining customized protection tailored to your estate's unique architectural features and specific risk profile.

Comprehensive Renewal Terms Adjustment Letter for Luxury Estate

A Comprehensive Renewal Terms Adjustment Letter is a formal document used to renegotiate or extend the lease of a luxury estate. It outlines updated financial obligations, such as rental increases, security deposit adjustments, and maintenance responsibilities. Precision is vital to ensure compliance with local property laws while preserving the exclusive landlord-tenant relationship. Key components include revised lease dates, service level agreements, and amenity access. This letter serves as a legal foundation for contractual continuity, ensuring both parties agree to market-aligned terms before the current term expires.

Why has my high-value home insurance premium increased this year?

Premium adjustments typically reflect rising construction material costs, specialized labor rates for high-end finishes, and updated local property valuations to ensure your home remains fully protected at current replacement values.

What specific changes were made to my policy coverage in this renewal?

Your renewal adjustment may include updated limits for "extended replacement cost," increased sub-limits for high-value collections like art or jewelry, and adjustments to deductible options to better align with your current risk profile.

How does the "Replacement Cost Plus" feature work under the new adjustment?

This feature ensures that if the cost to rebuild your bespoke home exceeds your policy limit due to market surges, the insurer will pay a specified percentage above the limit-often up to 150% or more-to guarantee the home is restored to its original quality.

Do I need to schedule a new appraisal following this renewal letter?

If you have recently completed significant renovations, added high-value acquisitions, or if it has been over three years since your last professional inspection, we recommend scheduling a complimentary high-value home appraisal to verify your coverage accuracy.

How can I mitigate the premium increase on my high-value property?

You can often reduce your premium by leveraging multi-policy discounts, increasing your deductible, or demonstrating the installation of loss-prevention technology such as smart leak detection systems and UL-certified central station security.

Comments