A Reverse Mortgage Maturity and Acceleration Notice is a formal legal document issued when a loan becomes due, typically following a homeowner's death or property sale. It outlines the repayment requirements and deadlines to prevent foreclosure. Understanding this process is vital for heirs and borrowers to navigate property transitions smoothly. Below are some ready to use template options to assist you.

Image cover: Navigating Your Reverse Mortgage: Maturity and Acceleration Notice Templates

Letter Samples List

- Reverse Mortgage Maturity Notification Letter

- Notice of Acceleration and Demand for Payment Letter

- Borrower Passing Maturity Event Notice Letter

- Primary Residence Non-Occupancy Acceleration Letter

- Property Tax Default and Acceleration Letter

- Homeowner Insurance Lapse Maturity Letter

- Surviving Heir Options and Payoff Demand Letter

- Notice of Intent to Foreclose Maturity Letter

- Deed in Lieu of Foreclosure Option Letter

- Reverse Mortgage Short Sale Resolution Letter

- Final Notice of Reverse Mortgage Maturity Letter

- Estate Settlement and Debt Repayment Letter

- Repayment Extension Request Decision Letter

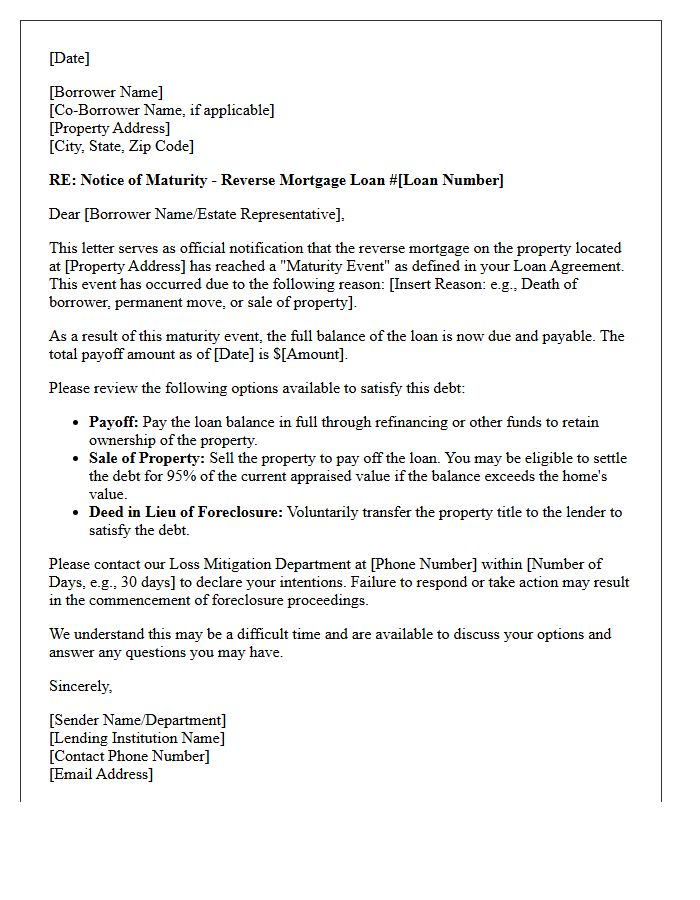

Reverse Mortgage Maturity Notification Letter

A Reverse Mortgage Maturity Notification Letter is a critical legal notice informing heirs or homeowners that the loan has become due and payable. This typically occurs after the last surviving borrower passes away or permanently vacates the property. The letter outlines specific repayment options, such as selling the home, refinancing, or providing a deed in lieu of foreclosure. Recipients must respond promptly, usually within 30 days, to initiate a grace period and prevent immediate legal action while settling the estate's obligations with the lender.

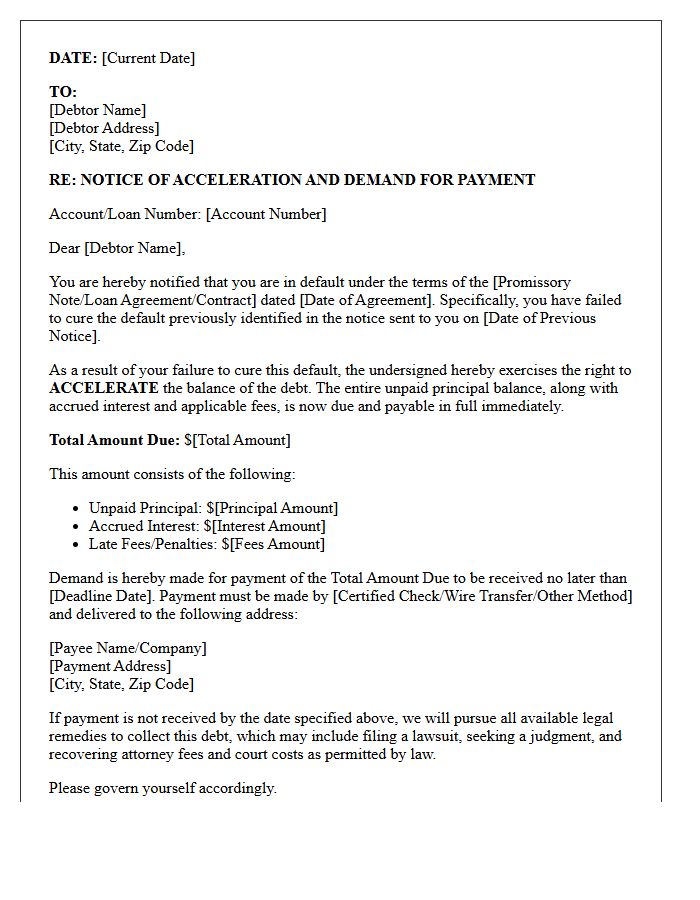

Notice of Acceleration and Demand for Payment Letter

A Notice of Acceleration is a formal legal warning issued when a borrower defaults on a loan. This letter signifies that the lender has exercised their right to demand the full remaining balance immediately, rather than following the original installment schedule. Receiving this document is critical because it usually serves as the final step before the lender initiates foreclosure or legal action. To prevent further escalation, the recipient must either pay the total debt or negotiate a reinstatement plan within the strictly specified timeframe mentioned in the notice.

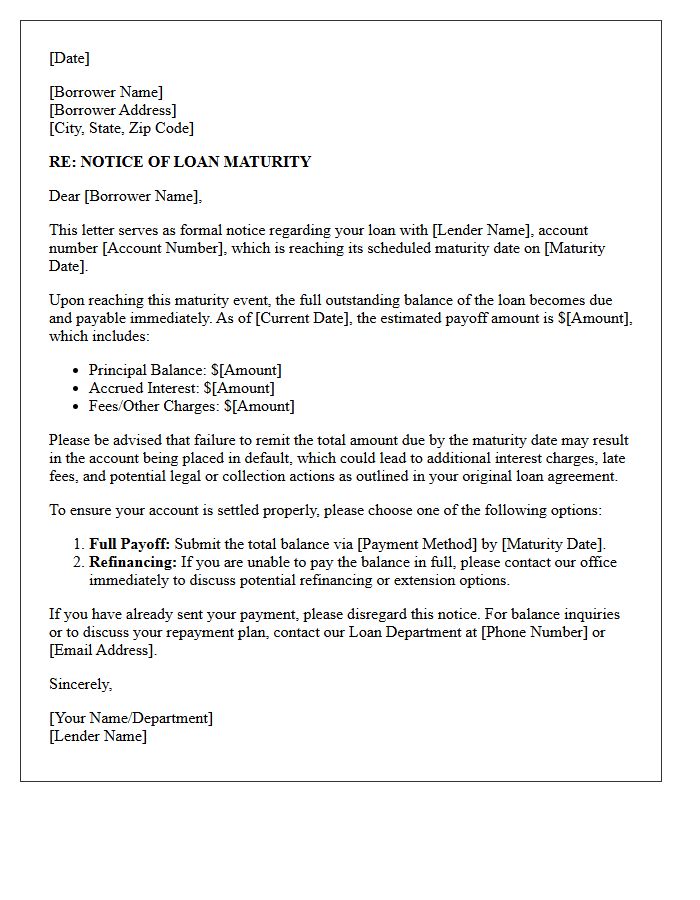

Borrower Passing Maturity Event Notice Letter

A Borrower Passing Maturity Event Notice Letter is a formal legal communication issued when a loan reaches its final maturity date without full repayment. This critical document notifies the borrower that the default event has occurred, potentially triggering immediate acceleration of the total debt. It serves as a formal demand for payment and outlines the lender's intent to exercise remedies, such as foreclosure or litigation. Understanding this notice is essential for initiating debt restructuring or workout negotiations to avoid severe financial penalties and collateral loss.

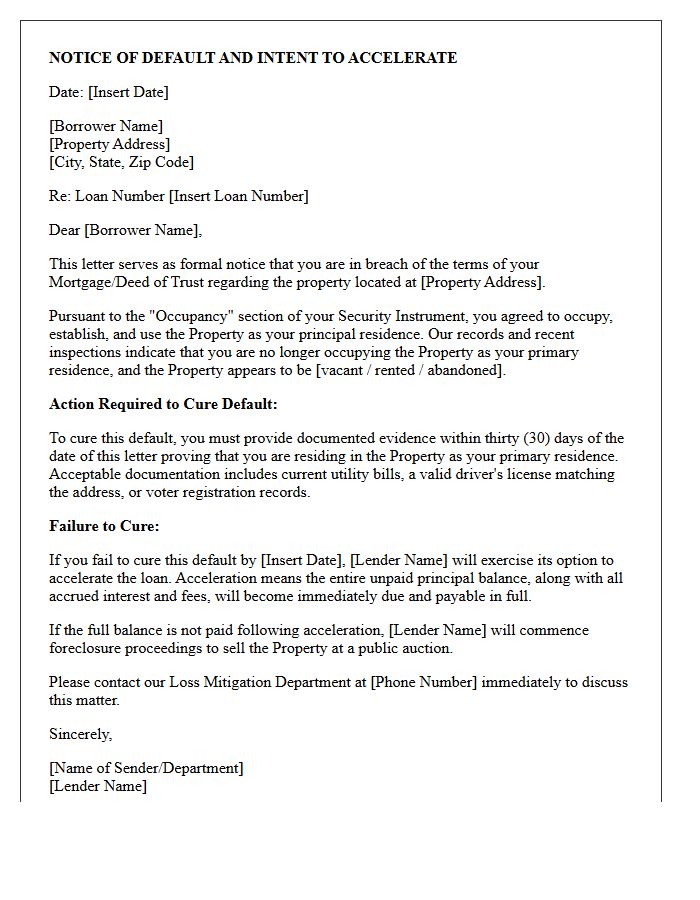

Primary Residence Non-Occupancy Acceleration Letter

A Primary Residence Non-Occupancy Acceleration Letter is a formal legal notice issued by a lender when a borrower violates the occupancy clause of their mortgage contract. If a homeowner moves out without permission, the lender may accelerate the loan, demanding immediate repayment of the full balance. This occurs because non-owner-occupied properties present higher financial risks. To avoid foreclosure, borrowers must promptly provide proof of residency or negotiate a loan modification to reflect the property's status as a rental or secondary home.

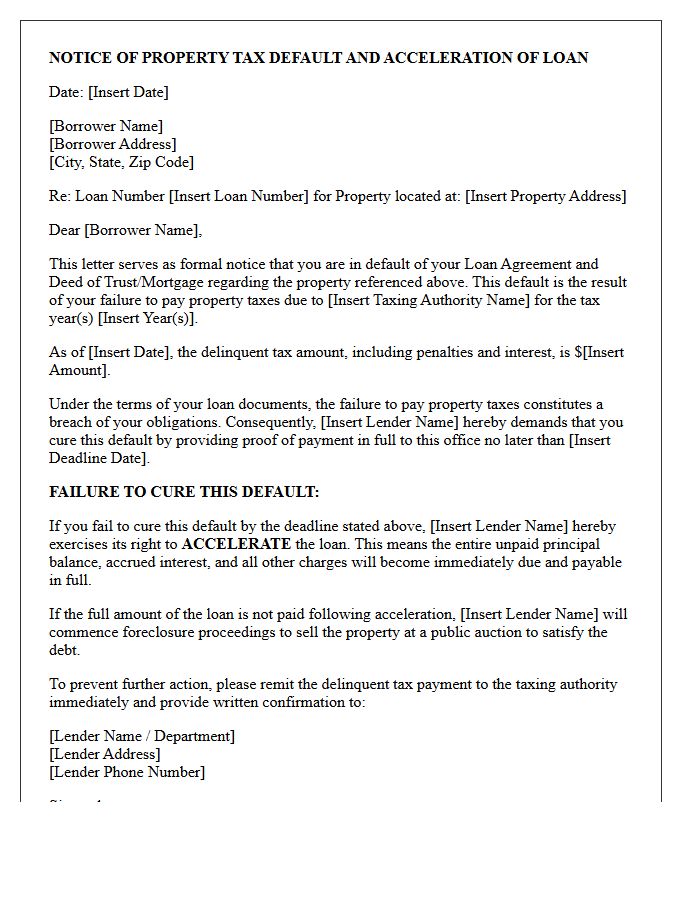

Property Tax Default and Acceleration Letter

Receiving a Notice of Default is a critical warning that you have fallen behind on property taxes. If unpaid, the taxing authority may issue an acceleration letter, demanding the full remaining balance immediately rather than installments. Failure to resolve this debt can lead to tax foreclosure, where the government seizes and sells your home to recover owed funds. To protect your ownership, you must explore repayment plans or redemption options before the final deadline to prevent the permanent loss of your property and home equity.

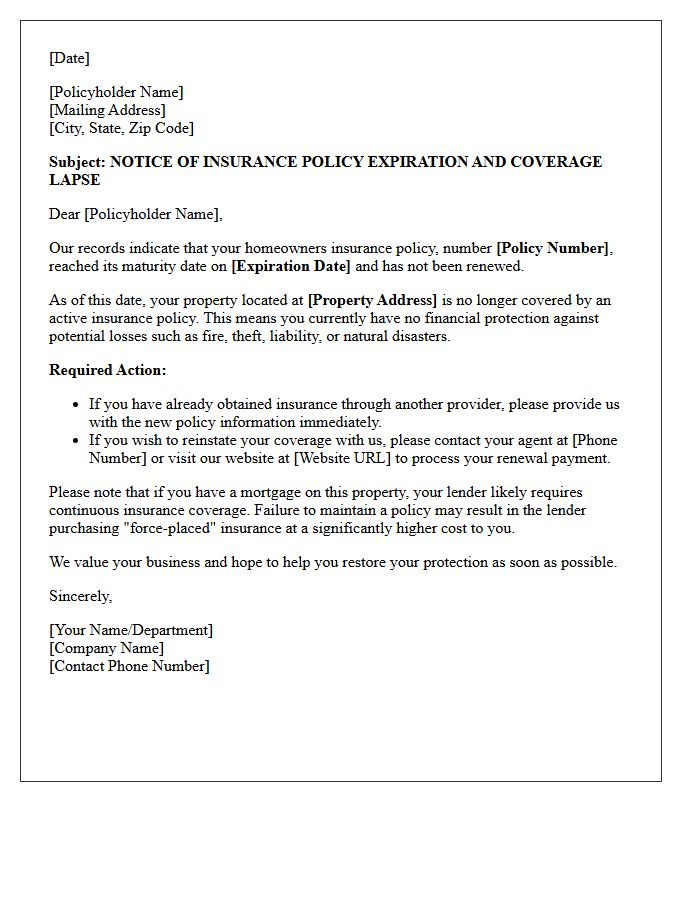

Homeowner Insurance Lapse Maturity Letter

A Homeowner Insurance Lapse Maturity Letter is a critical notice from your mortgage lender indicating that your property insurance has expired. This document signifies that you have reached a coverage gap, putting your home and loan agreement at risk. If you do not provide proof of a new policy immediately, the lender will likely implement force-placed insurance. This substitute coverage is typically much more expensive and offers limited protection for your personal belongings, making it essential to reinstate your private insurance quickly to avoid financial loss and higher premiums.

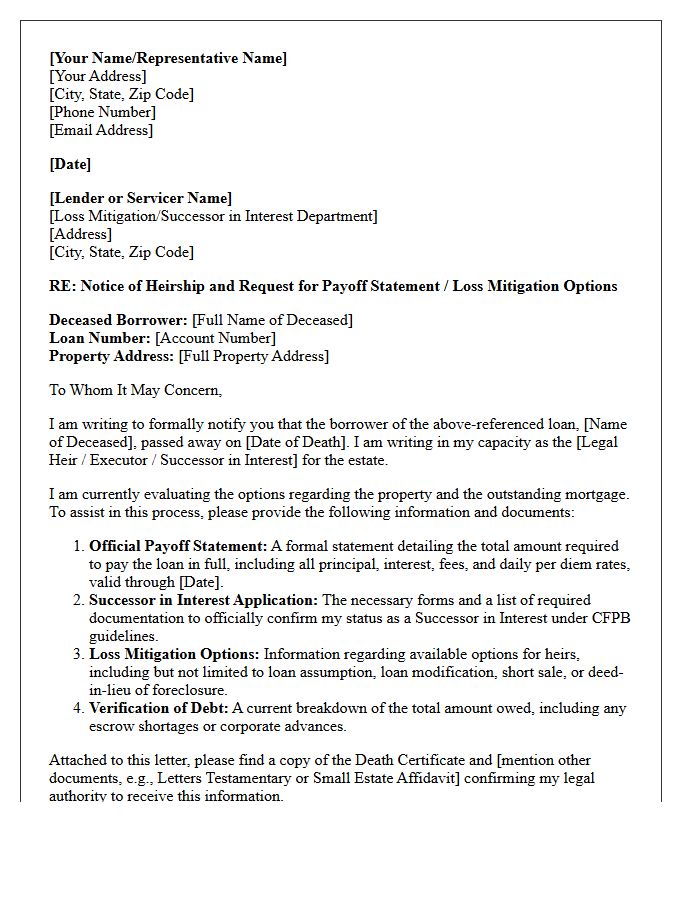

Surviving Heir Options and Payoff Demand Letter

A surviving heir must understand their legal succession rights to manage a deceased relative's mortgage. To prevent foreclosure, heirs can pursue options like loan assumption, refinancing, or a deed-in-lieu. To determine the exact debt, requesting a payoff demand letter is essential. This document provides the total outstanding balance, including interest and fees, required to satisfy the lien completely. Acting quickly ensures the property title is protected while allowing the heir to settle the estate efficiently and avoid unnecessary legal complications with the lender.

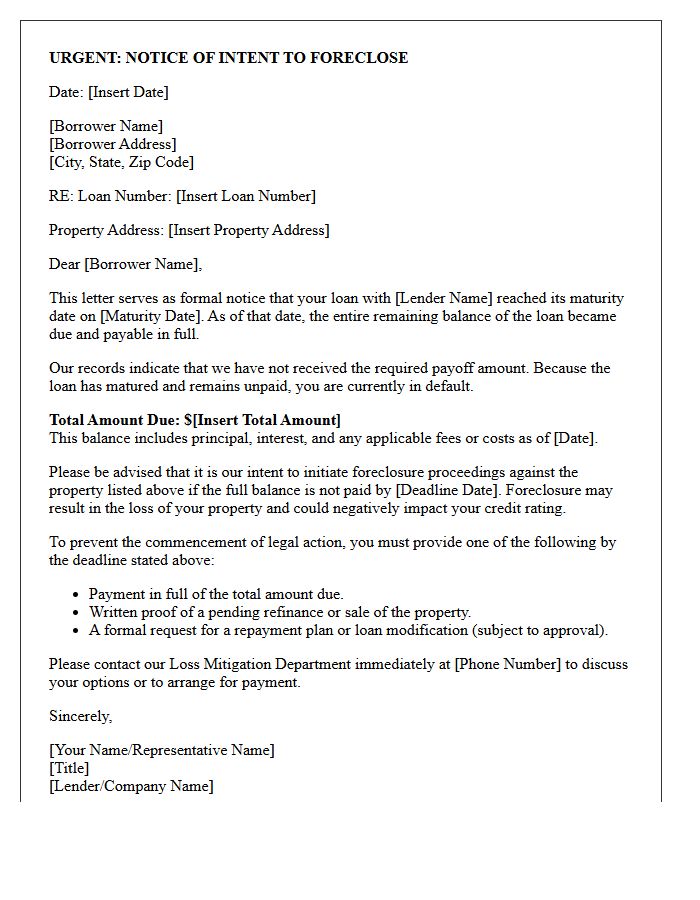

Notice of Intent to Foreclose Maturity Letter

A Notice of Intent to Foreclose is a formal warning issued when a borrower defaults on mortgage payments. It serves as a final legal precursor to legal action, detailing the total amount due to cure the default. Conversely, a Maturity Letter is sent when the full loan balance becomes due immediately, typically because the loan term has ended. Both documents are critical indicators of financial urgency, requiring immediate communication with lenders to explore loss mitigation, loan modifications, or repayment plans to prevent the loss of property ownership through foreclosure proceedings.

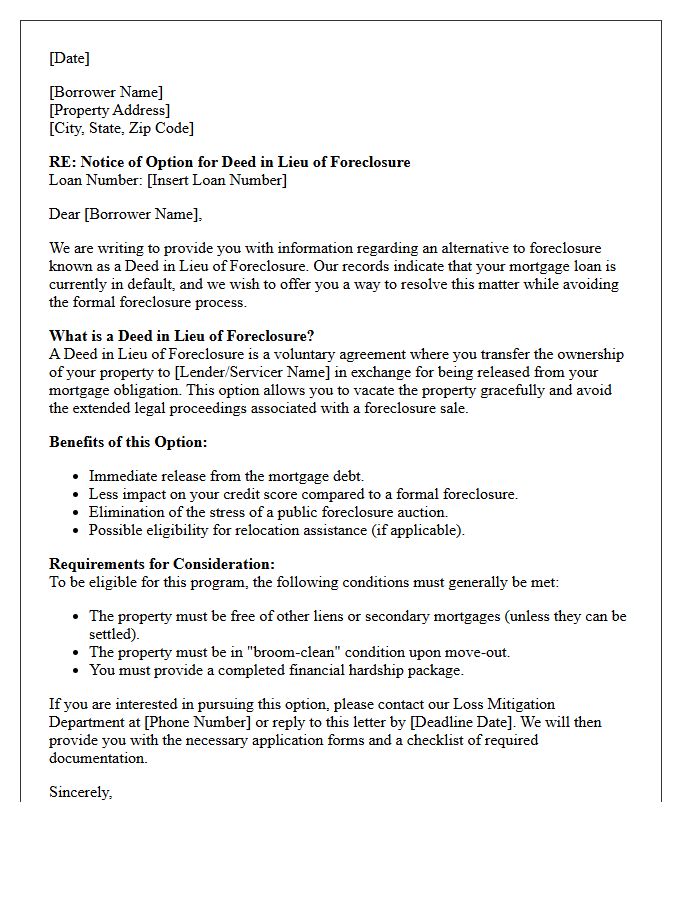

Deed in Lieu of Foreclosure Option Letter

A Deed in Lieu of Foreclosure Option Letter is a formal notification from a mortgage lender offering to accept the voluntary transfer of property ownership to satisfy a defaulted loan. This legal alternative allows homeowners to avoid a public foreclosure sale, potentially mitigating severe credit damage. The letter outlines specific terms, including the release of personal liability for the debt. It is a critical loss mitigation tool that requires the property to be free of secondary liens and often includes a move-out timeline in exchange for deficiency waiver protections.

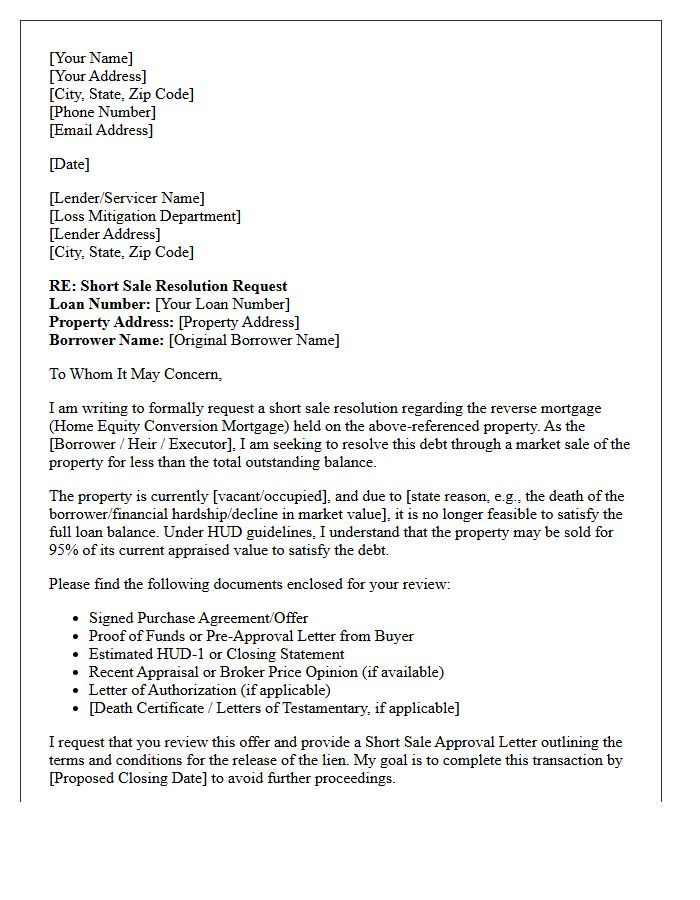

Reverse Mortgage Short Sale Resolution Letter

A Reverse Mortgage Short Sale Resolution Letter is a critical document issued by a loan servicer during the HUD non-recourse process. It confirms that the lender accepts the current market value of the property as full satisfaction of the debt, even if the balance exceeds the home's worth. This letter protects heirs from personal liability for the deficiency. To secure this resolution, an appraisal must verify the home's value, allowing the estate to settle the HECM loan legally without being burdened by negative equity or unpaid mortgage balances after the sale.

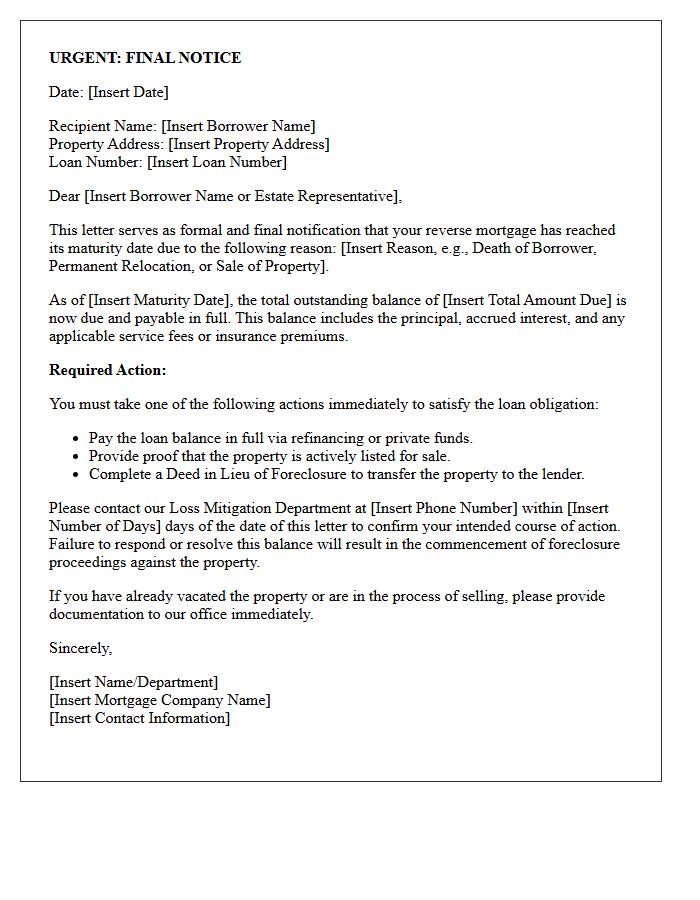

Final Notice of Reverse Mortgage Maturity Letter

A Final Notice of Reverse Mortgage Maturity Letter is a critical legal document informing heirs or homeowners that the loan has become due. This typically occurs after the death of the last borrower or a permanent move. The repayment must be addressed promptly to avoid foreclosure. Recipients have specific timelines to pay the balance, sell the property, or provide a deed-in-lieu. Understanding your options immediately is essential to protecting equity and managing the estate transition effectively within the required HUD guidelines.

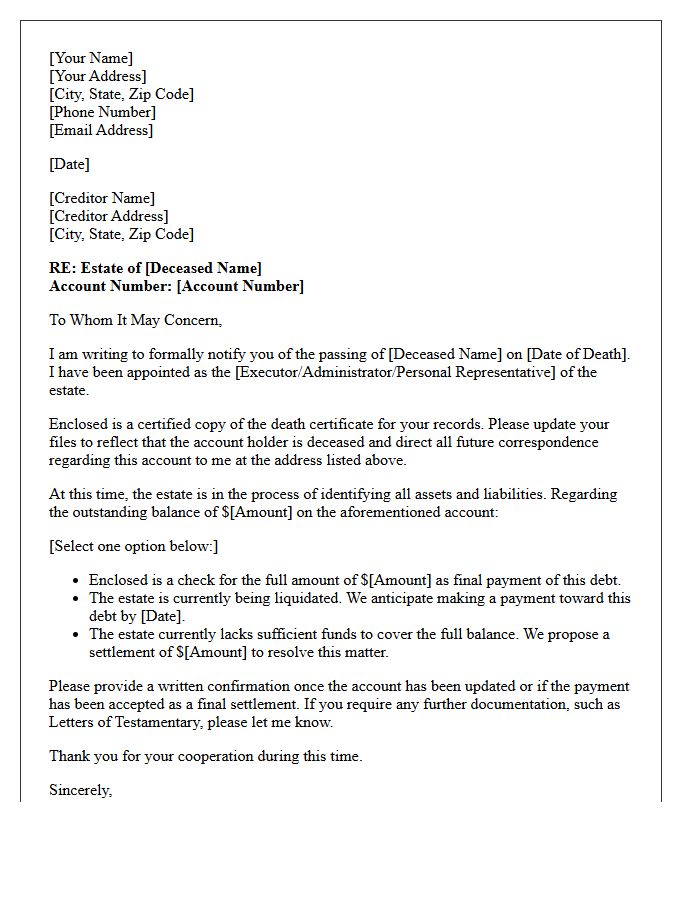

Estate Settlement and Debt Repayment Letter

An Estate Settlement and Debt Repayment Letter is a formal notice sent by an executor to inform creditors of a person's passing. This document initiates the legal process of probate, ensuring all outstanding liabilities are identified and verified. It protects the estate from late fees and establishes a structured timeline for resolving claims. Properly notifying creditors is vital to ensure that assets are distributed to beneficiaries only after all valid debts are settled, shielding the executor from personal liability during the final distribution of the deceased's assets.

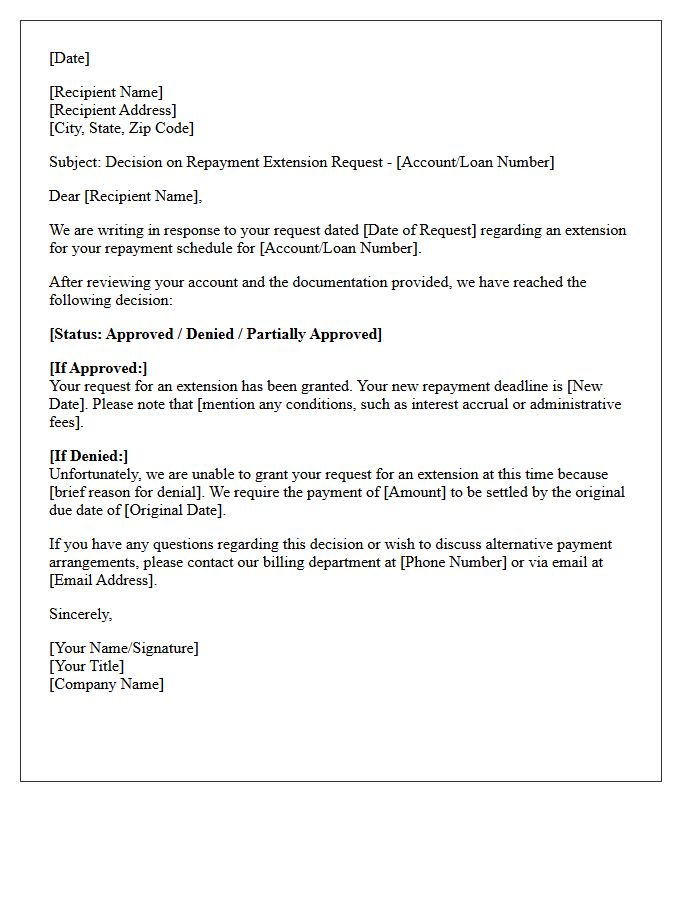

Repayment Extension Request Decision Letter

A Repayment Extension Request Decision Letter is the formal response from a creditor regarding your application to delay loan installments. This document specifies whether your request is approved or denied, outlining new deadlines or required next steps. It is crucial to review the revised payment schedule and any potential accrued interest or fees incurred during the extension period. Retaining this letter is essential for your financial records to ensure compliance with the modified agreement and to avoid accidental default or negative impacts on your credit score.

What is a Reverse Mortgage Maturity and Acceleration Notice?

A Maturity and Acceleration Notice is a formal legal notification sent by a loan servicer informing the homeowner or their heirs that the HECM (Home Equity Conversion Mortgage) has become due and payable in full. This occurs when a "triggering event" happens, such as the death of the last surviving borrower or the permanent vacancy of the principal residence.

What common events trigger a Reverse Mortgage Maturity Notice?

The most frequent triggers for loan acceleration include the death of all titled borrowers, the sale or transfer of the property, or the borrower moving out for more than 12 consecutive months (often due to assisted living). Failure to pay property taxes, homeowner's insurance, or maintain the home's condition can also lead to a notice of default and maturity.

How long do I have to respond to an Acceleration Notice?

Typically, borrowers or their estates have 30 days from the date of the notice to respond with a letter of intent. This letter must outline how they plan to satisfy the debt, whether through a deed-in-lieu of foreclosure, selling the home, or refinancing the balance to keep the property.

Can heirs keep the home after receiving a Maturity Notice?

Yes, heirs have the right to keep the property by paying the lesser of the full loan balance or 95% of the current appraised value. This is a protected feature of FHA-insured HECMs, allowing the estate to satisfy the debt even if the home is "underwater" (worth less than the loan balance).

What are the options to satisfy a Reverse Mortgage once it is called due?

There are four primary ways to satisfy the debt: pay the balance in full via cash or refinancing, sell the home and use the proceeds to pay the debt (retaining any remaining equity), execute a deed-in-lieu of foreclosure to return the property to the lender, or allow the lender to proceed with a foreclosure sale.

Comments