An FHA Conditional Loan Approval letter signifies that a lender is willing to finance your home, provided specific underwriting requirements are met. This document outlines the remaining steps, such as property appraisals or income verification, needed to secure final funding. Understanding these conditions is crucial for a smooth closing process. To help you get started, below are some ready to use template.

Image cover: Your Federal Housing Administration Conditional Loan Approval: Key Templates and Professional Samples

Letter Samples List

- Federal Housing Administration Conditional Loan Approval Letter

- Mortgage Lender Pre-Approval Commitment Letter

- Federal Housing Administration Final Loan Approval Letter

- Mortgage Loan Underwriting Conditions Letter

- Federal Housing Administration Clear To Close Letter

- Mortgage Lender Adverse Action Denial Letter

- Federal Housing Administration Notice Of Incomplete Application Letter

- Mortgage Loan Rate Lock Confirmation Letter

- Federal Housing Administration Gift Funds Explanation Letter

- Mortgage Lender Appraisal Contingency Notice Letter

- Federal Housing Administration Escrow Holdback Agreement Letter

- Mortgage Loan Post-Closing Review Letter

- Federal Housing Administration Loan Funding Confirmation Letter

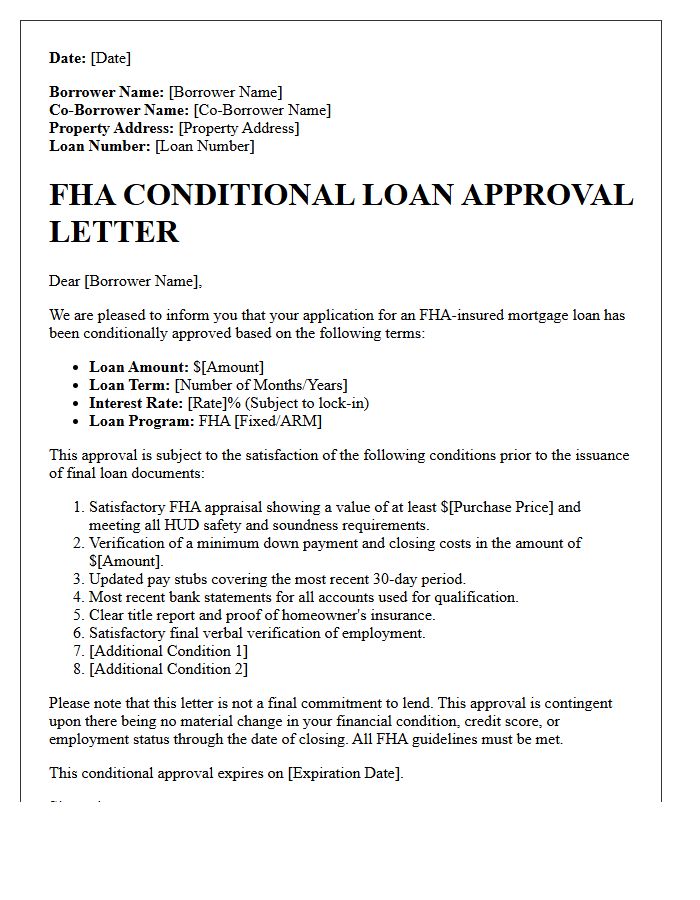

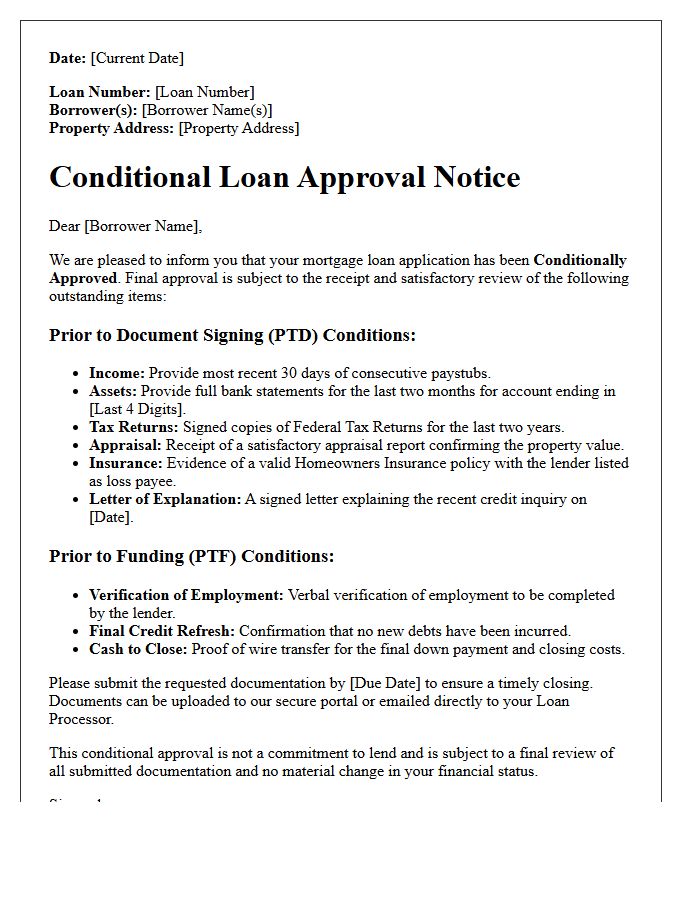

Federal Housing Administration Conditional Loan Approval Letter

A Federal Housing Administration (FHA) Conditional Loan Approval Letter signifies that a lender is willing to finance your home purchase provided specific requirements are met. It is not a final guarantee but a critical milestone indicating your application has passed initial underwriting. To receive a full "clear to close," borrowers must satisfy outstanding conditions, such as providing additional tax returns, verifying employment, or resolving credit inquiries. Timely submission of these documents is essential to ensure your mortgage meets FHA guidelines and moves toward a successful final closing.

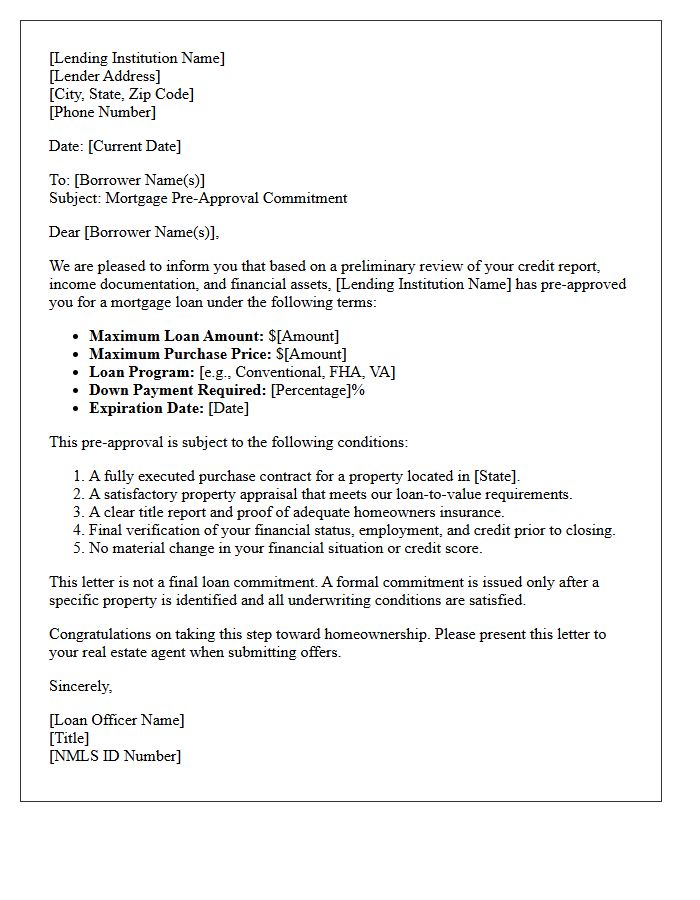

Mortgage Lender Pre-Approval Commitment Letter

A Mortgage Lender Pre-Approval Commitment Letter is a formal document verifying a buyer's financial ability to secure a home loan. Unlike a basic pre-qualification, this conditional approval involves a rigorous underwriting review of your income, credit score, and assets. It signals to sellers that you are a serious, qualified candidate with verified financing, providing a significant competitive advantage during negotiations. While it demonstrates strong borrowing power, final funding remains subject to a satisfactory property appraisal and no negative changes to your financial status before closing.

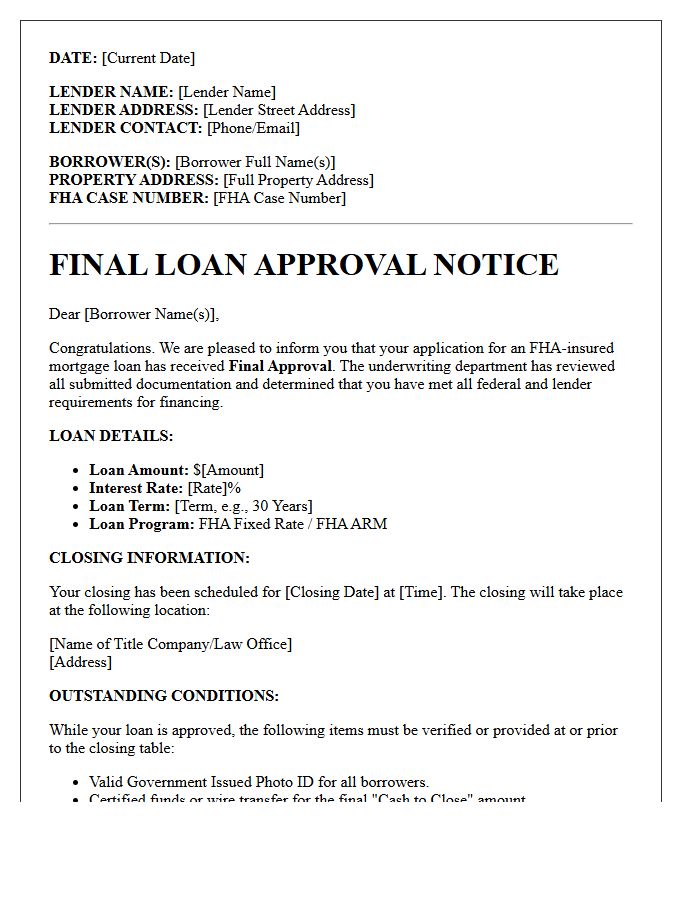

Federal Housing Administration Final Loan Approval Letter

The Federal Housing Administration Final Loan Approval Letter confirms that a borrower has met all underwriting requirements and is cleared to close. Unlike a pre-approval, this document signifies that the lender has verified income, assets, and the property's FHA compliance. It represents the final step before signing legal documents, ensuring the loan is ready for funding. Receiving this letter means all contingencies are cleared, providing the green light to complete your home purchase with confidence.

Mortgage Loan Underwriting Conditions Letter

A mortgage loan underwriting conditions letter is a formal document issued after initial review, stating that your application is approved conditionally. It outlines specific requirements you must fulfill, such as providing additional tax returns, proof of assets, or debt explanations, before achieving final approval. Timely responses are critical to maintain your interest rate and closing timeline. Always review this letter carefully, as satisfying every stipulation is the final hurdle to securing your home loan and receiving the official clear to close status from the lender.

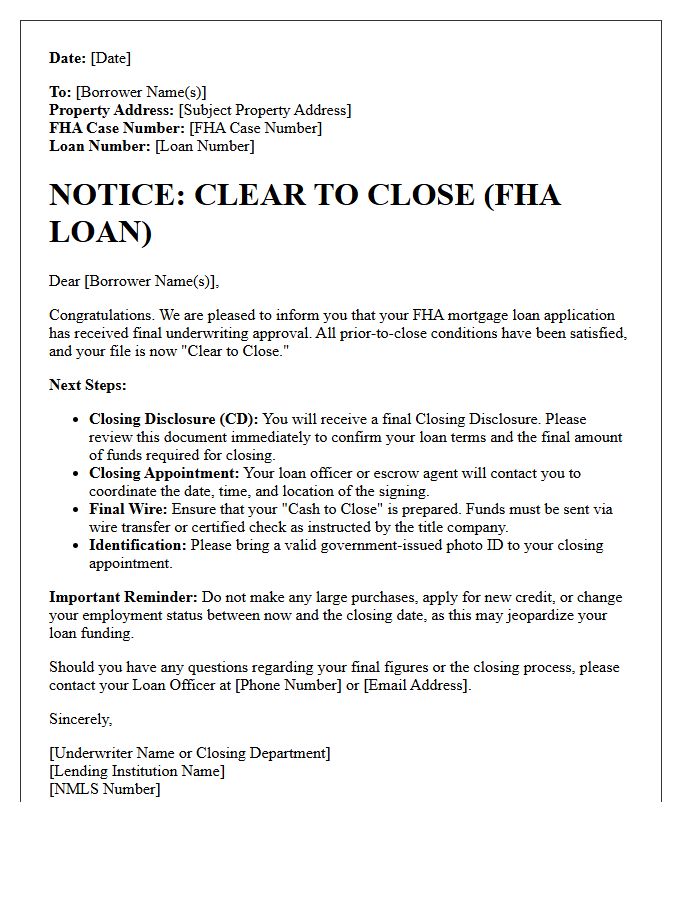

Federal Housing Administration Clear To Close Letter

Receiving an FHA Clear to Close letter signifies that the underwriter has reviewed all documentation and satisfied every mortgage condition. This final milestone confirms that your loan is fully approved and the lender is ready to fund the transaction. Before signing at the closing table, ensure your financial status remains stable by avoiding new debts or employment changes. This official notification is the last step before you receive your final closing disclosure and secure the keys to your new home.

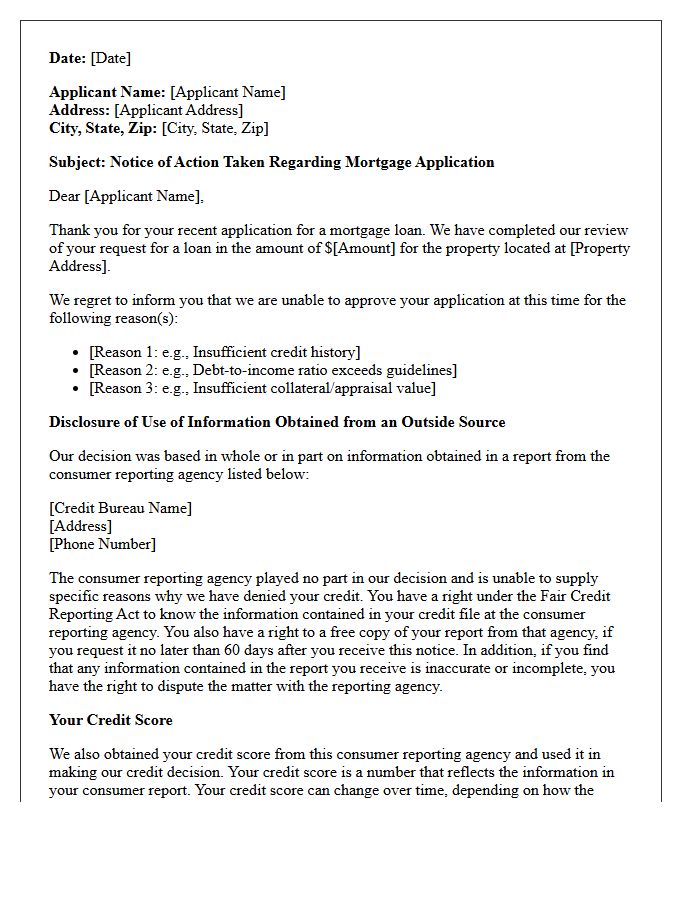

Mortgage Lender Adverse Action Denial Letter

A mortgage lender adverse action denial letter is a formal notice explaining why your loan application was rejected. Required by the Equal Credit Opportunity Act, it must provide specific reasons, such as low credit scores or insufficient income. This document is crucial because it allows you to identify financial weaknesses and check your credit report for errors. If the denial was based on credit data, you are entitled to a free report copy to dispute inaccuracies and improve your eligibility for future home financing.

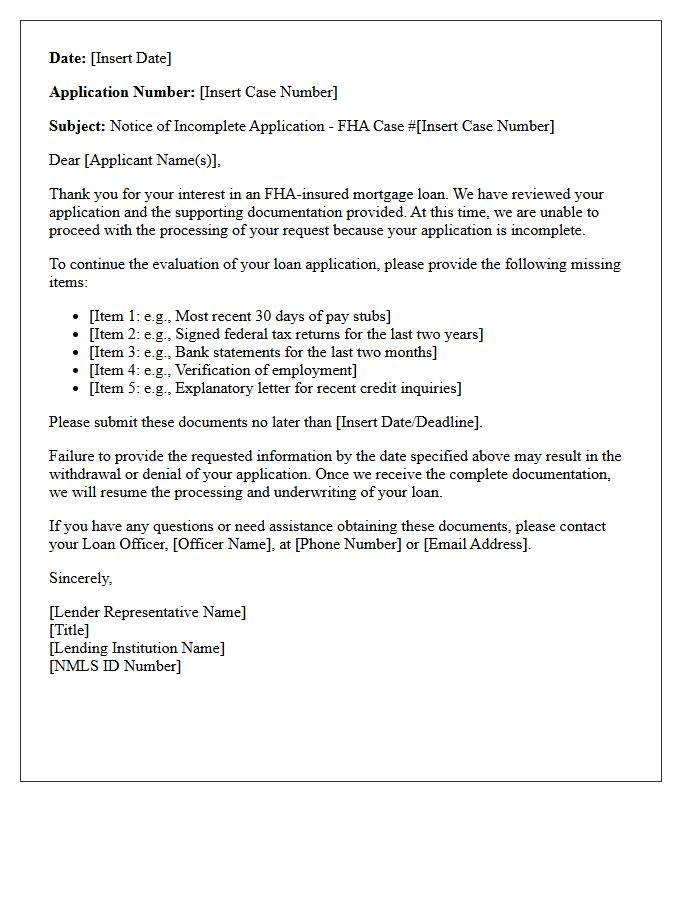

Federal Housing Administration Notice Of Incomplete Application Letter

The FHA Notice of Incomplete Application is a formal document issued when a mortgage file lacks essential information required for underwriting. Receiving this letter means the regulatory clock has paused, and you must provide missing documentation-such as pay stubs, tax returns, or bank statements-within a specific timeframe. Failing to respond promptly can result in a denial of your loan request. Review the listed deficiencies carefully to ensure your FHA loan processing resumes and you maintain your eligibility for government-backed financing.

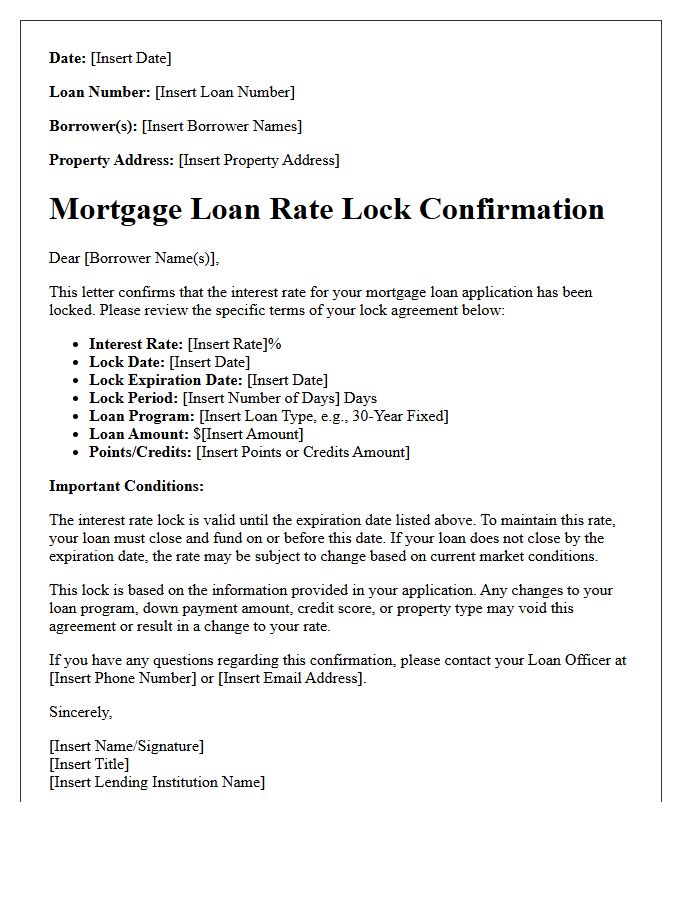

Mortgage Loan Rate Lock Confirmation Letter

A mortgage loan rate lock confirmation letter is a vital document guaranteeing your specific interest rate for a set timeframe. It protects you from market volatility while your application is processed. Carefully review the expiration date and potential fees to ensure the lock remains valid until closing. This written agreement provides financial security by fixing your monthly payment costs, shielding you from rising rates during the underwriting phase. Always verify that the terms, including points and loan duration, accurately reflect your verbal agreement with the lender.

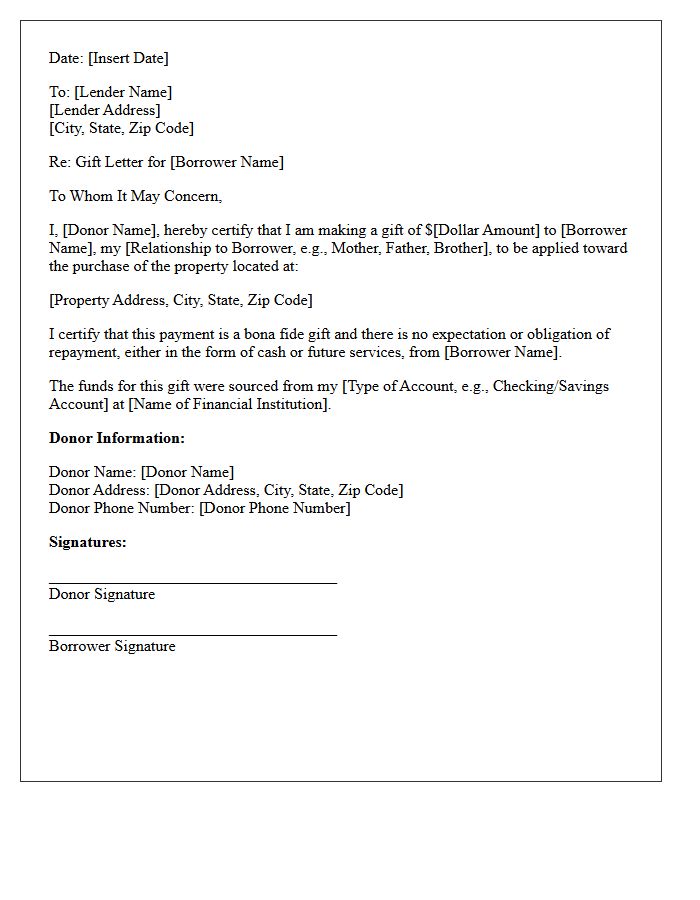

Federal Housing Administration Gift Funds Explanation Letter

A Federal Housing Administration (FHA) gift funds explanation letter is a mandatory document verifying that down payment assistance is a bona fide gift rather than a loan. The donor must clearly state their relationship to the borrower and confirm that no repayment is expected. This letter ensures compliance with HUD guidelines by documenting the source of funds and the transfer process. Both the donor and borrower must sign the document to maintain transparency during the mortgage underwriting process, protecting the loan's integrity and the borrower's debt-to-income ratio.

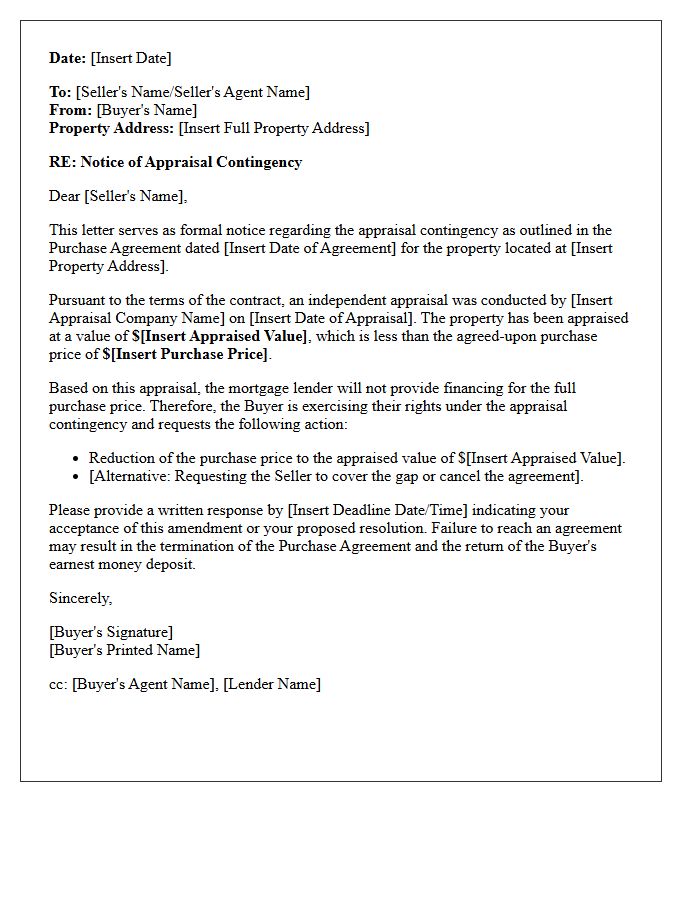

Mortgage Lender Appraisal Contingency Notice Letter

A Mortgage Lender Appraisal Contingency Notice Letter is a formal document notifying the seller that the property's appraised value is lower than the agreed purchase price. This triggers the appraisal contingency clause, allowing the buyer to request a price reduction, cover the gap with cash, or legally terminate the contract without penalty. It protects the lender from financing an overpriced asset and safeguards the buyer's earnest money. Timely delivery is critical to ensure the financing condition remains valid and the transaction stays within legal compliance under the sales agreement.

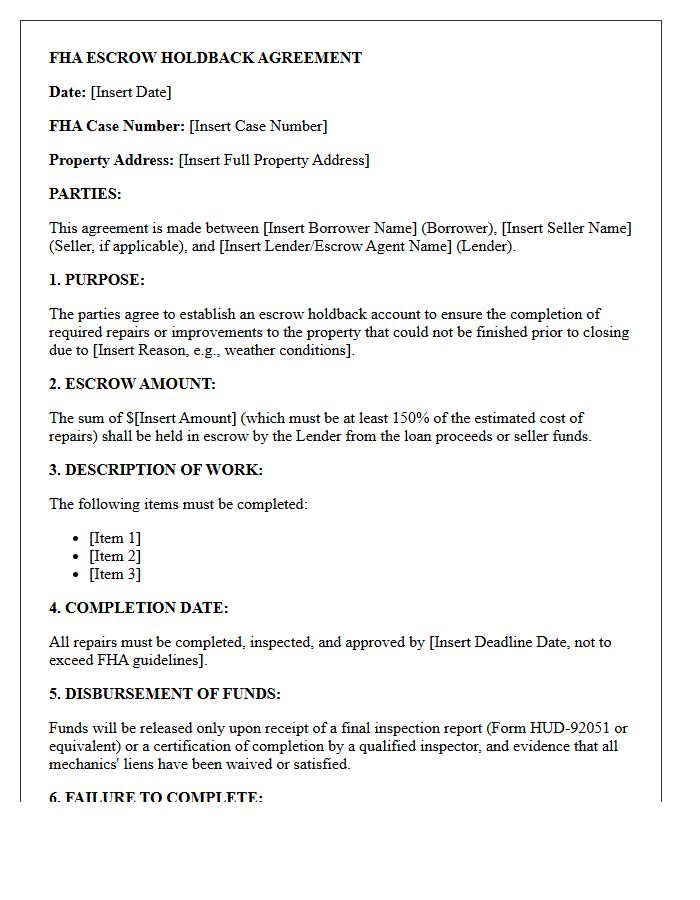

Federal Housing Administration Escrow Holdback Agreement Letter

A Federal Housing Administration (FHA) Escrow Holdback Agreement Letter is a legal contract allowing a home sale to close before specific repairs are finished. It ensures the lender withholds a portion of the seller's proceeds-typically 150% of the estimated cost-in a dedicated account. This document outlines the required renovations, completion deadlines, and inspection terms. Once a professional confirms the work meets FHA safety standards, the funds are released. This agreement is essential for bypassing minor property deficiencies that would otherwise delay or prevent traditional financing approval.

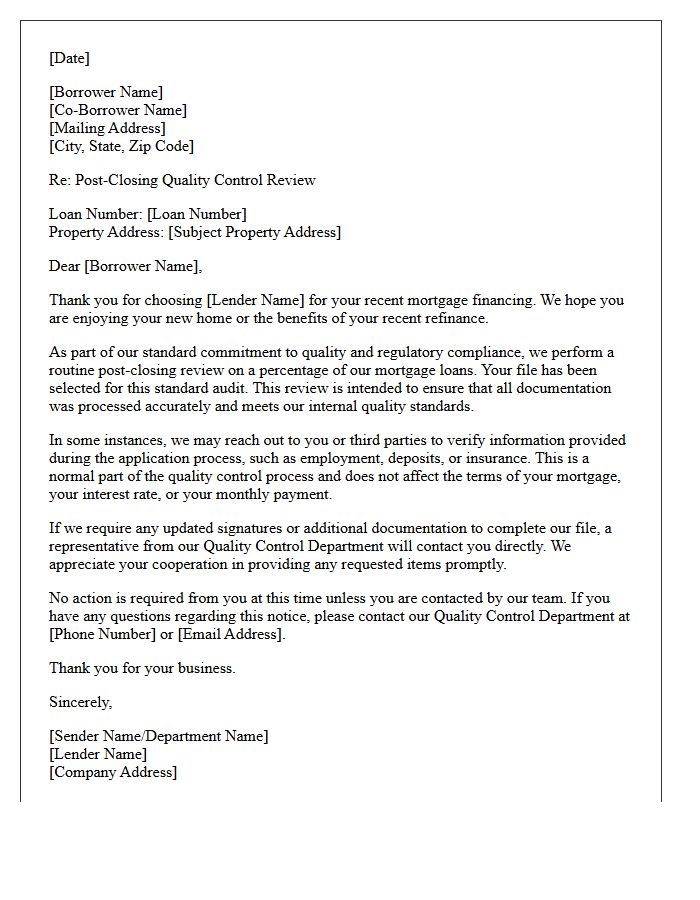

Mortgage Loan Post-Closing Review Letter

A mortgage loan post-closing review letter is a critical document sent by lenders after a real estate transaction. Its primary purpose is to confirm that the loan file complies with all federal regulations and internal underwriting standards. During this quality control phase, auditors verify the accuracy of legal documents, financial disclosures, and signatures. Receiving this letter may sometimes involve requests for missing information or clarification. Ensuring a clean review is essential for the lender to successfully sell the mortgage on the secondary market or to government-sponsored entities like Fannie Mae.

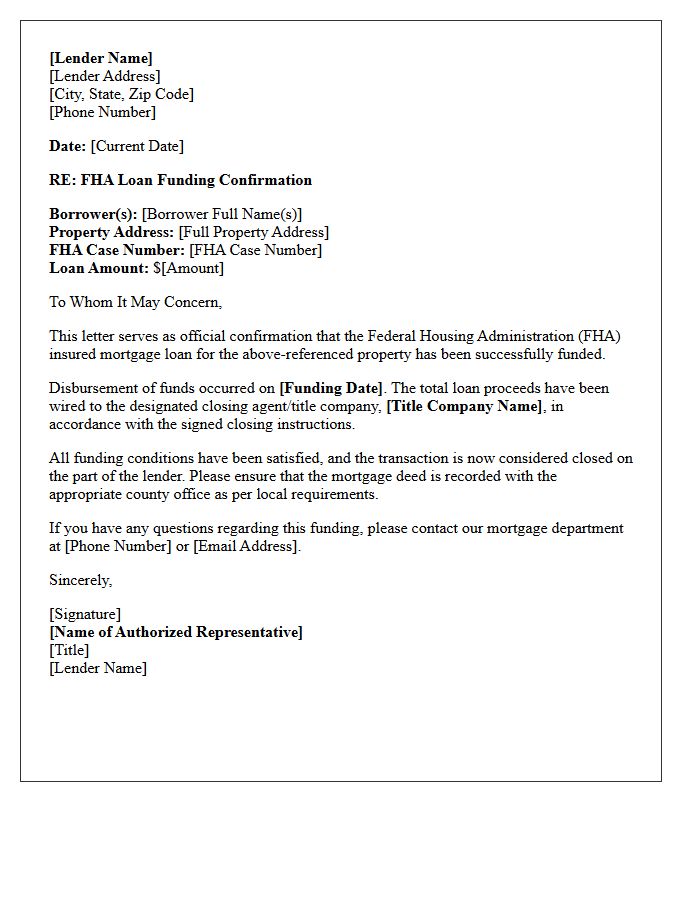

Federal Housing Administration Loan Funding Confirmation Letter

A Federal Housing Administration Loan Funding Confirmation Letter is an official document verifying that a mortgage lender has received final approval to release funds for a real estate transaction. This letter confirms that all underwriting conditions have been met and the government insurance is secured. For homebuyers, this serves as the definitive proof that the loan is fully funded, allowing for the legal transfer of property title. It marks the successful completion of the FHA financing process, ensuring that the seller receives payment and the buyer can finalize their purchase.

What is an FHA conditional loan approval letter?

An FHA conditional loan approval letter is a document issued by a mortgage underwriter indicating that a borrower's loan application is approved, provided specific requirements or "conditions" are met before closing.

What are common conditions listed in an FHA conditional approval?

Common conditions typically include providing updated pay stubs, clarifying bank statement deposits, submitting proof of homeowners insurance, and completing a satisfactory FHA-compliant property appraisal.

How long does it take to get a conditional approval letter for an FHA loan?

The timeline generally ranges from 3 to 7 business days after the initial application and document submission, depending on the lender's current processing volume and the complexity of the borrower's file.

Does a conditional approval mean my FHA loan is guaranteed to close?

No, a conditional approval is not a final guarantee. The loan only moves to "clear to close" status once the underwriter reviews and approves all requested documentation and verifies that the borrower's financial status has not changed.

What is the difference between FHA pre-approval and conditional approval?

An FHA pre-approval is an initial estimate of borrowing power based on unverified data, whereas a conditional approval is a formal commitment issued after a professional underwriter has reviewed the borrower's credit, income, and assets.

Comments