Securing an Escrow Waiver Request allows homeowners to manage their own property taxes and insurance payments directly. This process requires lender approval based on specific equity levels and credit criteria. Understanding the requirements is essential for financial flexibility and avoiding monthly impound accounts. To help you draft a formal application, below are some ready to use template.

Image cover: Official Approval Templates for Escrow Waiver Requests

Letter Samples List

- Approval Letter for Escrow Waiver Request

- Escrow Waiver Approval Letter

- Mortgage Escrow Account Waiver Approval Letter

- Official Letter of Escrow Waiver Approval

- Letter of Approval for Property Tax Escrow Waiver

- Confirmation Letter for Escrow Waiver Approval

- Escrow Requirement Waiver Approval Letter

- Letter Approving Mortgage Escrow Waiver Request

- Property Insurance Escrow Waiver Approval Letter

- Approval Letter for Voluntary Escrow Account Waiver

- Home Loan Escrow Waiver Approval Letter

- Letter of Authorization for Escrow Account Waiver

- Notice and Approval Letter for Escrow Waiver Request

Approval Letter for Escrow Waiver Request

An Escrow Waiver Approval Letter is a formal document from your lender granting permission to manage your own property taxes and insurance. To qualify, homeowners typically need a minimum 20% equity stake and a strong payment history. Once approved, your monthly mortgage payment decreases, but you become legally responsible for making large, lump-sum tax and insurance payments on time. Failure to pay these obligations can result in the lender revoking the waiver or placing expensive force-placed insurance on the property to protect their financial interest.

Escrow Waiver Approval Letter

An Escrow Waiver Approval Letter is a formal document issued by a mortgage lender granting a borrower permission to pay property taxes and homeowners insurance directly. By obtaining this waiver, the homeowner avoids monthly impound payments, gaining greater control over their cash flow. However, lenders typically require a minimum equity position or a specific loan-to-value ratio to mitigate risk. It is crucial to remember that the homeowner assumes full legal responsibility for timely payments to avoid tax liens or policy lapses that could jeopardize the property title.

Mortgage Escrow Account Waiver Approval Letter

A Mortgage Escrow Account Waiver Approval Letter is a formal document from your lender granting permission to manage your own property taxes and homeowners insurance payments directly. To secure this waiver, homeowners typically must maintain a specific loan-to-value ratio and a history of on-time payments. Once approved, the lender will no longer collect monthly escrow deposits, reducing your total monthly mortgage statement. However, you assume full responsibility for meeting tax deadlines and maintaining continuous insurance coverage to avoid potential penalties or loan default.

Official Letter of Escrow Waiver Approval

An Official Letter of Escrow Waiver Approval is a formal document issued by a mortgage lender granting a homeowner permission to manage their own property taxes and insurance payments. To qualify, borrowers typically must meet specific loan-to-value ratios and maintain a strong payment history. Once approved, the lender removes the monthly escrow requirement from the mortgage payment. However, the homeowner assumes full responsibility for making timely disbursements to local tax authorities and insurance providers to avoid penalties or loan default risks.

Letter of Approval for Property Tax Escrow Waiver

A Letter of Approval for a Property Tax Escrow Waiver allows homeowners to manage their own property tax payments rather than using a lender-managed account. To qualify, lenders typically require a minimum equity of 20% and a history of timely payments. Once approved, the monthly mortgage payment decreases, but the homeowner assumes full responsibility for paying lump-sum tax bills directly to the municipality. Failing to pay on time can result in penalties or the lender revoking the waiver to protect their lien interest.

Confirmation Letter for Escrow Waiver Approval

A confirmation letter for an escrow waiver approval is a formal document verifying that a lender has granted permission for a homeowner to pay their property taxes and insurance premiums directly instead of through an impound account. To qualify, borrowers typically must maintain a specific loan-to-value ratio and a history of timely payments. This letter serves as critical proof that the lender's servicing requirements have changed, shifting the responsibility for managing annual housing-related liabilities and financial compliance solely to the property owner.

Escrow Requirement Waiver Approval Letter

An Escrow Requirement Waiver Approval Letter is a formal document from a lender granting a borrower permission to pay property taxes and insurance directly. To qualify, homeowners typically must maintain a specific loan-to-value ratio and demonstrate a consistent history of on-time payments. Once approved, the borrower assumes full responsibility for these financial obligations, removing them from the monthly mortgage installment. It is crucial to manage these funds independently to avoid tax liens or lender-placed insurance, which can occur if self-managed payments are missed or delayed.

Letter Approving Mortgage Escrow Waiver Request

A letter approving a mortgage escrow waiver confirms you are now responsible for paying property taxes and homeowner's insurance directly. This approval typically requires a loan-to-value ratio below 80% and a record of on-time payments. Once granted, your monthly mortgage installment decreases, but you must manage large annual expenses independently. Failure to provide proof of payment to your lender can result in the waiver being revoked or the imposition of costly force-placed insurance. Carefully review the effective date to ensure a smooth transition from servicer-managed payments to self-management.

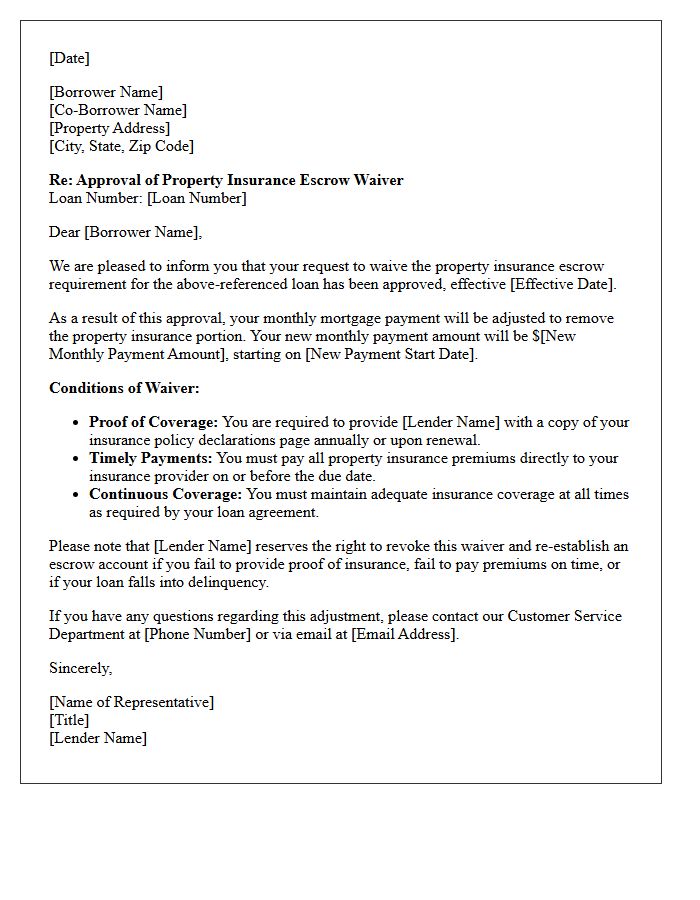

Property Insurance Escrow Waiver Approval Letter

A Property Insurance Escrow Waiver Approval Letter is a formal document from your lender granting permission to pay homeowners insurance premiums directly instead of through an impound account. This waiver confirms that the borrower assumes full responsibility for timely payments and policy renewals. Lenders typically require a strong loan-to-value ratio and a proven credit history before approving this request. It is crucial to provide the lender with annual proof of coverage to avoid force-placed insurance, which is significantly more expensive and provides less protection for the homeowner.

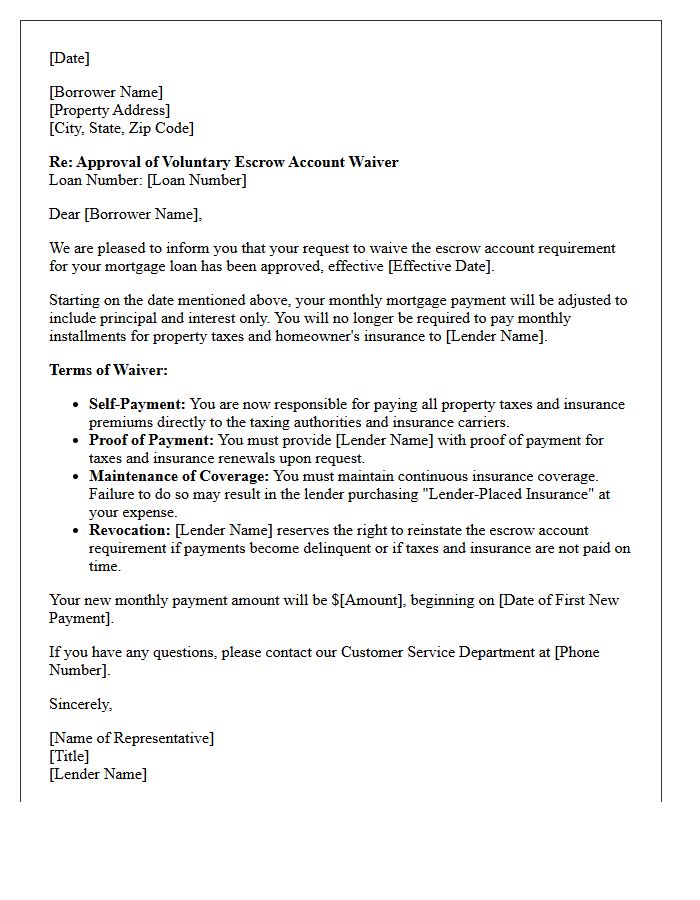

Approval Letter for Voluntary Escrow Account Waiver

An Approval Letter for Voluntary Escrow Account Waiver is a formal document issued by a mortgage lender granting a borrower permission to manage their own property taxes and insurance. This waiver eliminates the need for a lender-managed impound account, providing homeowners with increased liquidity and direct control over payment schedules. To qualify, lenders typically require a specific loan-to-value ratio and a proven history of on-time payments. It is essential to remember that even with a waiver, homeowners remain legally responsible for maintaining continuous coverage and settling tax liabilities promptly.

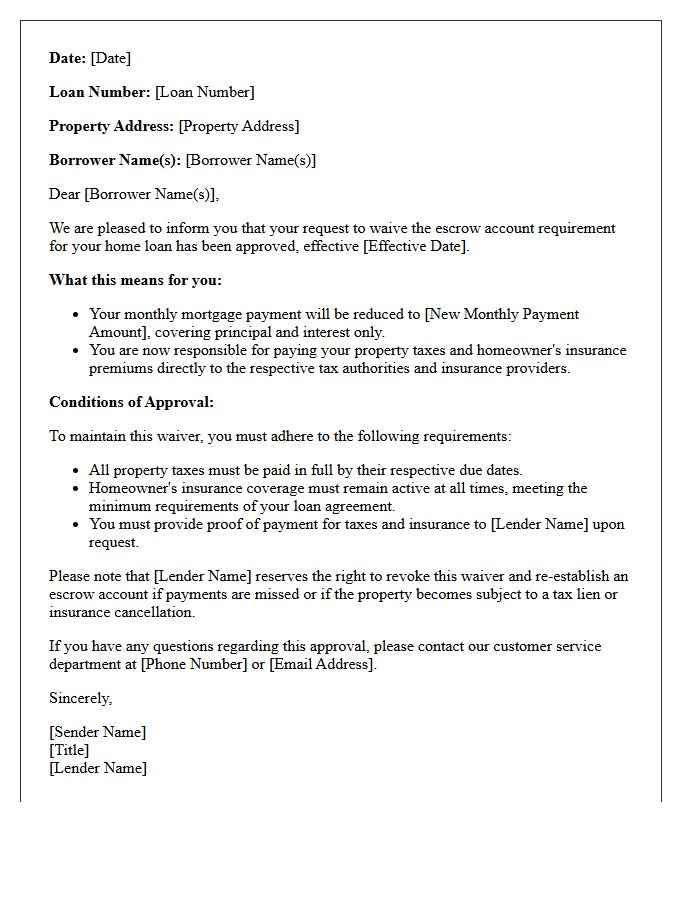

Home Loan Escrow Waiver Approval Letter

A Home Loan Escrow Waiver Approval Letter is an official document from your lender granting permission to manage your own property taxes and homeowners insurance. To qualify, homeowners typically need a minimum 20% equity stake and a strong credit history. Once approved, you are responsible for making large lump-sum payments directly to tax authorities and insurers instead of including them in your monthly mortgage. This letter confirms the removal of the lender's impound account requirement, providing more control over your cash flow and potential interest earnings on those funds.

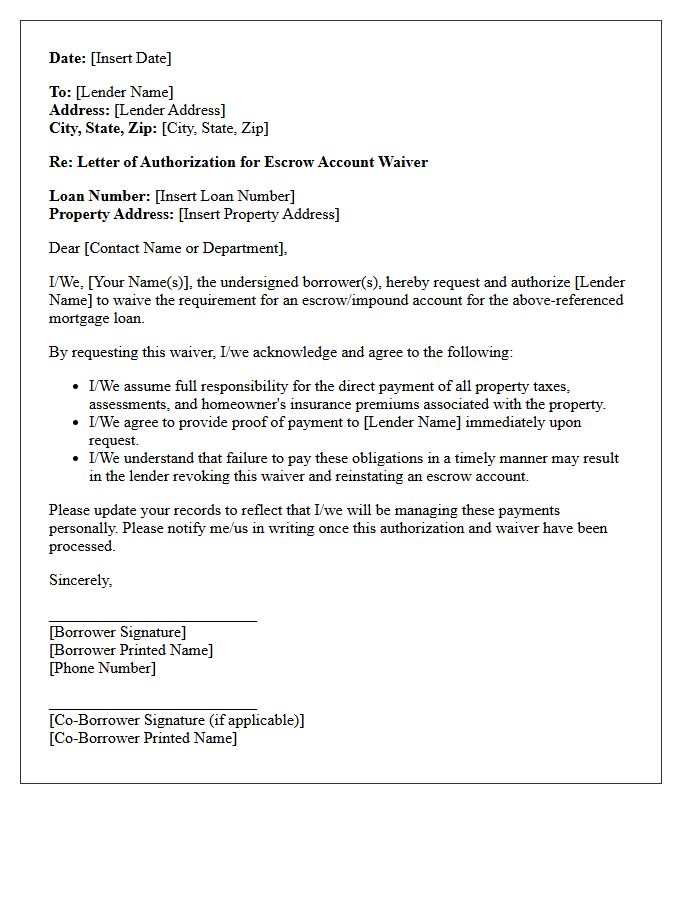

Letter of Authorization for Escrow Account Waiver

A Letter of Authorization for Escrow Account Waiver is a formal request allowing a borrower to manage their own property taxes and insurance payments. By submitting this document, you ask the lender to remove the escrow requirement, providing greater control over personal cash flow. To qualify, homeowners typically must maintain a specific loan-to-value ratio and demonstrate a consistent history of on-time payments. Once approved, the borrower assumes full responsibility for meeting all tax obligations and insurance premiums independently to avoid potential loan default or lender-placed coverage.

Notice and Approval Letter for Escrow Waiver Request

A Notice and Approval Letter for Escrow Waiver Request confirms that a lender has granted permission for a homeowner to manage their own property taxes and insurance payments. To receive this official authorization, borrowers typically must meet specific loan-to-value ratios and maintain a clean payment history. Once approved, you are responsible for paying these liabilities directly and on time. Failure to settle these obligations can result in the lender revoking the waiver and reinstating a mandatory escrow account to protect their financial interest in the property.

What is an escrow waiver request?

An escrow waiver request is a formal application made by a borrower to their mortgage lender asking to manage their own property taxes and homeowners insurance payments instead of having them collected and paid through an escrow account.

What are the requirements for approval of an escrow waiver?

Most lenders require a minimum loan-to-value (LTV) ratio of 80% or lower, a history of on-time mortgage payments, and a conventional loan. Some lenders may also require a specific credit score or a one-time waiver fee to process the request.

How long does it take to get an escrow waiver approved?

The review process typically takes between 15 to 30 business days. During this time, the lender evaluates your payment history, current equity, and loan type to ensure you meet all secondary market and internal guidelines.

Will my monthly mortgage payment change after an escrow waiver approval?

Yes, your monthly mortgage payment will decrease because the lender will no longer collect funds for taxes and insurance. However, you become fully responsible for paying these large annual or semi-annual bills directly to the tax authority and insurance provider.

Can an approved escrow waiver be revoked by the lender?

Yes, lenders reserve the right to revoke an escrow waiver and reinstate an escrow account if the borrower fails to pay property taxes on time, allows insurance coverage to lapse, or becomes delinquent on mortgage payments.

Comments