Receiving a Notice of Deficiency Judgment Intent means a creditor plans to collect the remaining balance owed after a foreclosure or repossession sale. This formal legal notification outlines your liability for the shortfall and initiates the recovery process. Understanding your rights is essential to protecting your financial future. To help you respond effectively, below are some ready to use template.

Image cover: Formal Notice of Intent to Seek a Deficiency Judgment: Templates and Essential Guidance

Letter Samples List

- Notice of Intent to Pursue Deficiency Judgment Letter

- Post-Foreclosure Deficiency Judgment Intent Letter

- Automobile Repossession Deficiency Judgment Warning Letter

- Commercial Loan Deficiency Judgment Demand Letter

- Mortgage Shortfall Deficiency Judgment Intent Letter

- Outstanding Balance Deficiency Judgment Notice Letter

- Final Demand and Deficiency Judgment Intent Letter

- Secured Asset Liquidation Deficiency Judgment Letter

- Unpaid Promissory Note Deficiency Judgment Intent Letter

- Defaulted Debt Deficiency Judgment Action Letter

- Bank Collateral Shortage Deficiency Judgment Letter

- Pre-Litigation Deficiency Judgment Intent Letter

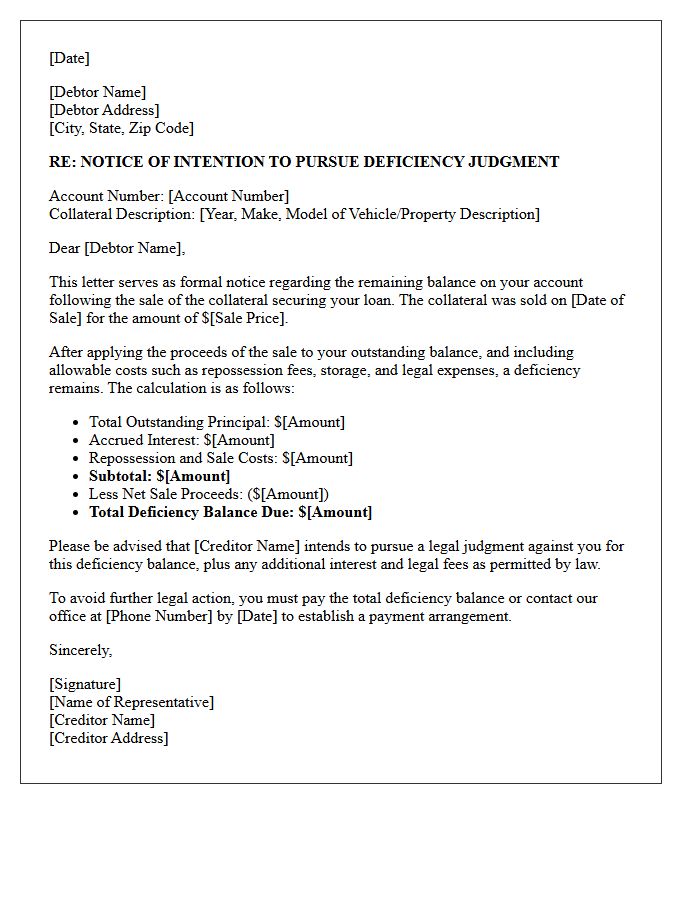

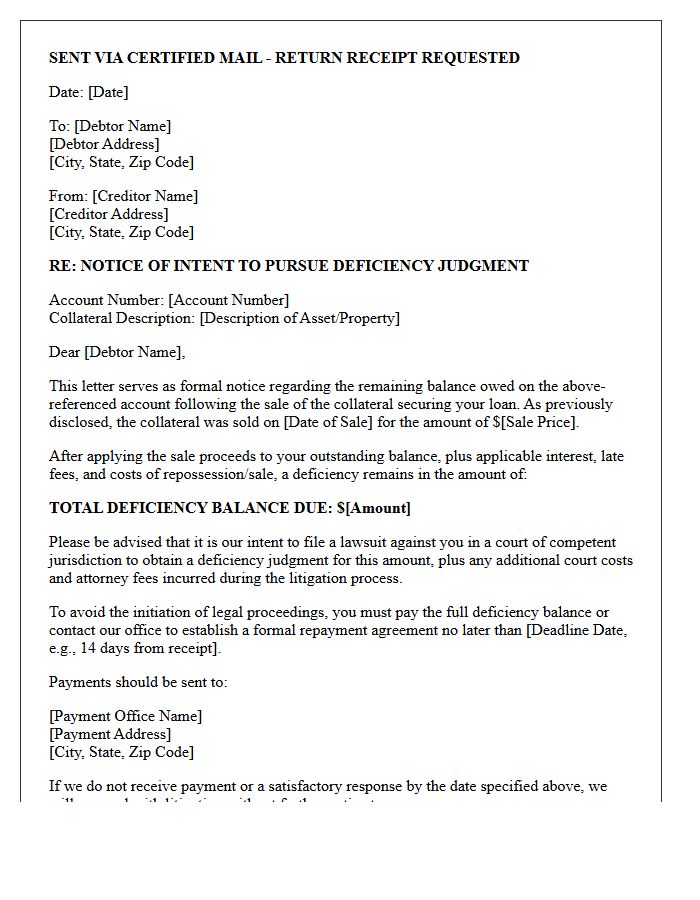

Notice of Intent to Pursue Deficiency Judgment Letter

A Notice of Intent to Pursue Deficiency Judgment is a critical legal warning sent after a foreclosure or repossession. It informs the debtor that the sale proceeds failed to cover the total loan balance. Receiving this letter means the lender plans to sue for the remaining debt. To protect your rights, you must respond within the specified statutory timeframe. Failure to act can lead to wage garnishment or bank levies. Always verify the deficiency amount and check local state laws, as some jurisdictions limit or prohibit these secondary recovery actions.

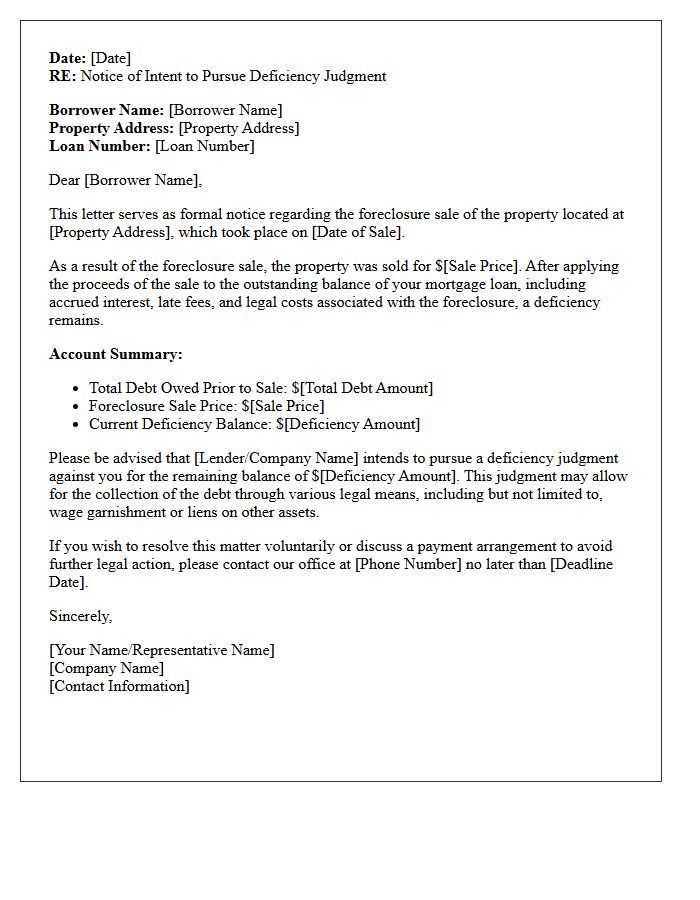

Post-Foreclosure Deficiency Judgment Intent Letter

A Post-Foreclosure Deficiency Judgment Intent Letter is a formal notice sent by a lender to a borrower after a home sale fails to cover the total loan balance. This document signals the creditor's legal intent to recover the remaining debt, known as a deficiency. It is a critical stage where borrowers should seek legal advice to explore debt settlement options or contest the amount claimed. Timely response is essential to prevent further litigation, wage garnishments, or bank levies resulting from a court-ordered judgment following the foreclosure process.

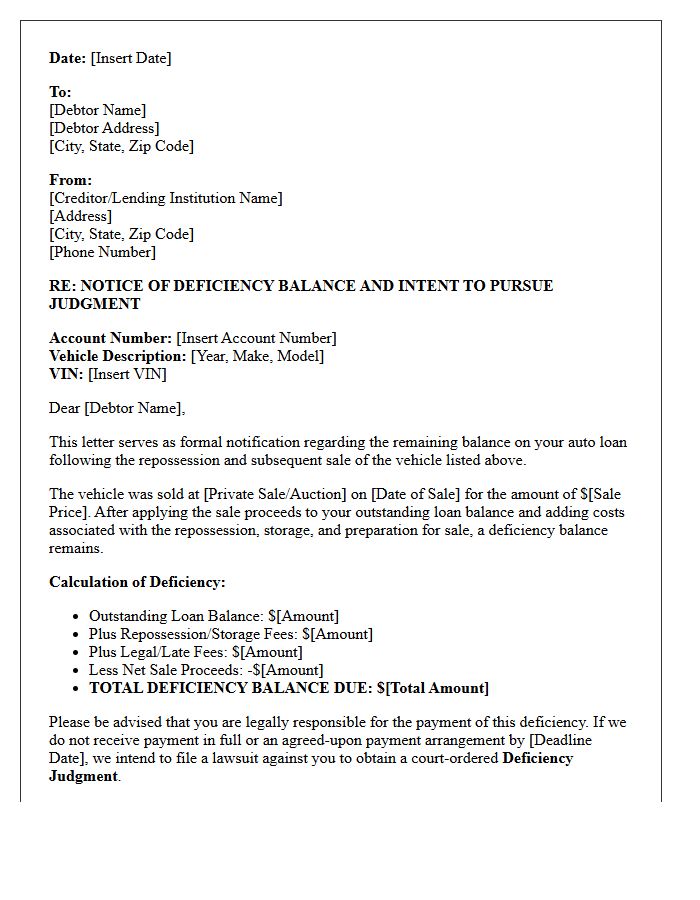

Automobile Repossession Deficiency Judgment Warning Letter

An automobile repossession deficiency judgment warning letter notifies you that selling your seized vehicle didn't cover your full loan balance. This legal notice serves as a final opportunity to pay the remaining "deficiency" before the lender pursues a court judgment against you. Ignoring this letter can lead to severe consequences, including wage garnishment, bank levies, or further damage to your credit score. It is critical to verify the auction math and state laws to ensure the lender followed proper notification procedures before they file a formal lawsuit.

Commercial Loan Deficiency Judgment Demand Letter

A Commercial Loan Deficiency Judgment Demand Letter is a formal legal notice issued after a foreclosure sale. When the property's auction price fails to cover the total outstanding debt, the lender sends this document to demand the remaining balance from the borrower or guarantors. It serves as a final warning before a deficiency judgment is pursued in court. Understanding the statute of limitations and specific state laws is critical, as they dictate the timeframe and legality of collecting the shortfall. Timely legal review is essential to mitigate personal financial liability.

Mortgage Shortfall Deficiency Judgment Intent Letter

A Mortgage Shortfall Deficiency Judgment Intent Letter is a formal notice from a lender stating their intent to collect the remaining balance after a foreclosure or short sale. It notifies the borrower that the sale proceeds did not cover the total debt, resulting in a deficiency. This legal step warns of potential litigation or wage garnishment to recover the outstanding funds. Understanding this letter is crucial for assessing financial liability and negotiating a settlement or exploring legal defenses to prevent further collection actions against your personal assets.

Outstanding Balance Deficiency Judgment Notice Letter

An Outstanding Balance Deficiency Judgment Notice Letter is a legal notification sent after a foreclosure or repossession. It informs the debtor that the sale proceeds failed to cover the total debt owed. This formal document demands payment for the remaining deficiency balance, including interest and legal fees. Receiving this letter indicates that the lender may pursue further debt collection actions, such as wage garnishment or bank levies, through a court order. Understanding your state's specific statutes of limitations and consumer rights is essential for disputing the amount or negotiating a settlement.

Final Demand and Deficiency Judgment Intent Letter

A Final Demand and Deficiency Judgment Intent Letter is a formal legal notice issued after a foreclosure or vehicle repossession. Its primary purpose is to inform the debtor that the sale of the asset did not cover the full loan balance, creating a deficiency balance. The document serves as a final warning before the creditor pursues a deficiency judgment through the court system to garnish wages or seize assets. It outlines the specific amount owed, including interest and fees, providing a final opportunity for settlement before aggressive legal action commences.

Secured Asset Liquidation Deficiency Judgment Letter

A Secured Asset Liquidation Deficiency Judgment Letter is a formal notice sent after a lender sells collateral for less than the total debt owed. It informs the borrower of the remaining balance, known as the deficiency, following the sale. This document outlines the legal obligation to pay the difference and serves as a precursor to potential collection actions or wage garnishment. Understanding your rights regarding the fair market value of the sold asset is critical to potentially challenging the amount claimed by the creditor.

Unpaid Promissory Note Deficiency Judgment Intent Letter

An Unpaid Promissory Note Deficiency Judgment Intent Letter is a formal legal notice issued by a creditor to a borrower. It signals the lender's legal intent to sue for the remaining balance if collateral liquidation fails to cover the total debt. This document serves as a final opportunity to resolve the deficiency balance before a court-ordered judgment is sought. Understanding this letter is critical, as it precedes wage garnishments or asset seizures. Timely negotiation or legal counsel is essential to mitigate long-term financial consequences and potential litigation costs.

Defaulted Debt Deficiency Judgment Action Letter

A Defaulted Debt Deficiency Judgment Action Letter is a formal legal notice indicating that a creditor is seeking a court-ordered judgment to collect the remaining balance after collateral liquidation. This deficiency balance occurs when an asset's sale price fails to cover the total loan amount. Recipients must respond promptly to avoid automatic wage garnishment or bank levies. Understanding your rights regarding statutes of limitations and verifying the debt's accuracy are critical steps in defending against such legal actions to protect your financial future.

Bank Collateral Shortage Deficiency Judgment Letter

A Bank Collateral Shortage Deficiency Judgment Letter is a formal notice sent after a foreclosure or repossession sale fails to cover the outstanding loan balance. This deficiency represents the remaining debt you legally owe the lender. Receiving this letter signifies the bank's intent to pursue a judgment through the court system to collect the funds. It is critical to review the deficiency balance for accuracy, as this legal action can lead to wage garnishment or asset seizures. Seeking legal counsel immediately is vital to negotiate a settlement or contest the claim.

Pre-Litigation Deficiency Judgment Intent Letter

A Pre-Litigation Deficiency Judgment Intent Letter is a formal legal notice sent by a lender following a foreclosure or repossession. It notifies the borrower that the sale of the asset did not cover the outstanding loan balance. This document serves as a final warning, declaring the creditor's legal intent to sue for the remaining shortfall. Receiving this letter is critical because it marks the transition from property loss to personal financial liability, often requiring immediate legal counsel to negotiate a settlement or contest the claimed deficiency amount before a formal lawsuit begins.

What is a Notice of Intent to Seek a Deficiency Judgment?

A Notice of Intent to Seek a Deficiency Judgment is a formal legal notification sent by a lender informing a borrower that the proceeds from a foreclosure sale were insufficient to cover the total mortgage debt. It signals the lender's legal objective to collect the remaining balance through a court order.

When will I receive a Notice of Deficiency Judgment Intent?

In most jurisdictions, this notice is issued shortly after the foreclosure auction or short sale is finalized. State laws typically require lenders to serve this notice within a specific timeframe-often 30 to 90 days-to preserve their right to sue for the remaining debt balance.

Can I contest a Notice of Intent to Seek a Deficiency Judgment?

Yes, borrowers can contest the notice by challenging the "fair market value" of the property at the time of sale. If the lender sold the home for significantly less than its worth, a judge may reduce or eliminate the deficiency amount based on the property's actual appraisal value rather than the auction price.

What happens if I ignore a Notice of Deficiency Judgment Intent?

Ignoring this notice allows the lender to obtain a default judgment against you. Once a judgment is granted, the lender can exercise aggressive collection methods, including wage garnishment, placing liens on other owned assets, or freezing funds in your bank accounts.

Are there ways to avoid a deficiency judgment after receiving a notice?

Common strategies to resolve a deficiency intent include negotiating a settlement for a smaller lump sum, entering a structured repayment plan, or filing for bankruptcy, which may discharge the unsecured debt. Some states also have "non-recourse" laws that prohibit deficiency judgments on primary residences.

Comments