This memorandum outlines critical updates to the Know Your Customer protocol, focusing on enhanced due diligence and regulatory compliance standards. These improvements streamline identity verification processes to better mitigate financial risk and prevent fraud within your organization. Understanding these structural changes ensures operational integrity and alignment with modern security mandates. Below are some ready to use template.

Image cover: Standardizing Compliance: Modern KYC Protocol Enhancements and Implementation Templates

Letter Samples List

- Letter of Memorandum on Know Your Customer Protocol Enhancements

- Executive Letter Regarding Enhanced Customer Due Diligence Standards

- Letter of Directive for Banking Institution Identity Verification Updates

- Internal Compliance Letter on Know Your Customer Policy Revisions

- Letter of Notification for Advanced Client Screening Procedures

- Advisory Letter on Know Your Customer Risk Assessment Frameworks

- Letter of Guidance for Biometric Authentication Protocol Integration

- Management Letter Detailing Anti-Money Laundering Protocol Enhancements

- Letter of Instruction on Ultimate Beneficial Ownership Verification

- Regulatory Alignment Letter for Know Your Customer Procedure Upgrades

- Letter of Implementation for Continuous Customer Monitoring Systems

- Departmental Letter on Enhanced Know Your Customer Audit Requirements

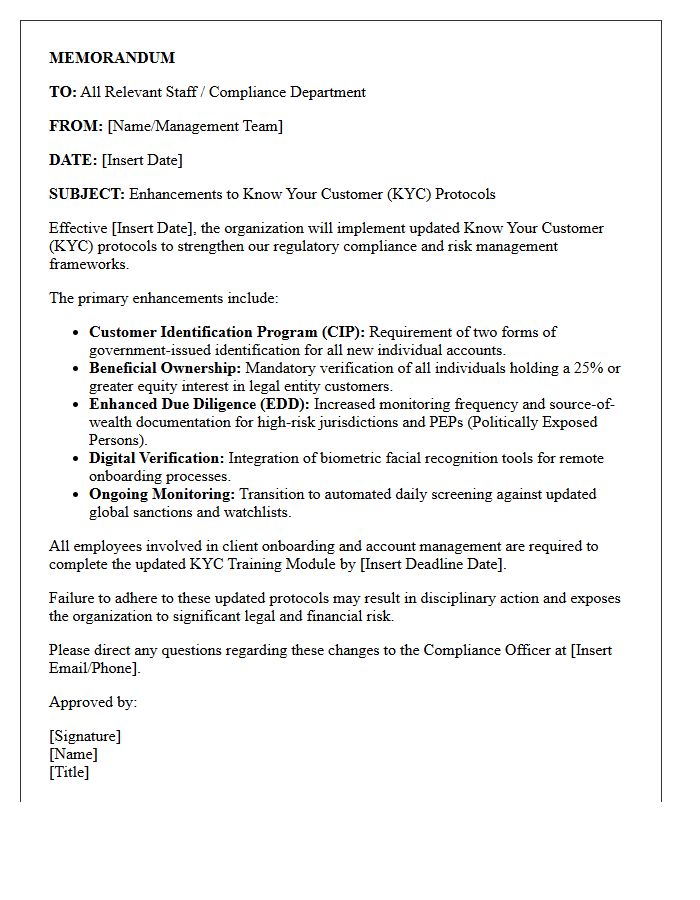

Letter of Memorandum on Know Your Customer Protocol Enhancements

A Letter of Memorandum on Know Your Customer (KYC) Protocol Enhancements outlines critical updates to identity verification standards. These modifications aim to strengthen regulatory compliance by integrating advanced risk assessment tools and automated screening processes. Financial institutions utilize these memorandums to document improved due diligence procedures, ensuring more effective prevention of money laundering and fraud. Understanding these enhancements is vital for maintaining legal transparency and protecting the integrity of global financial transactions through more rigorous customer identification and monitoring systems.

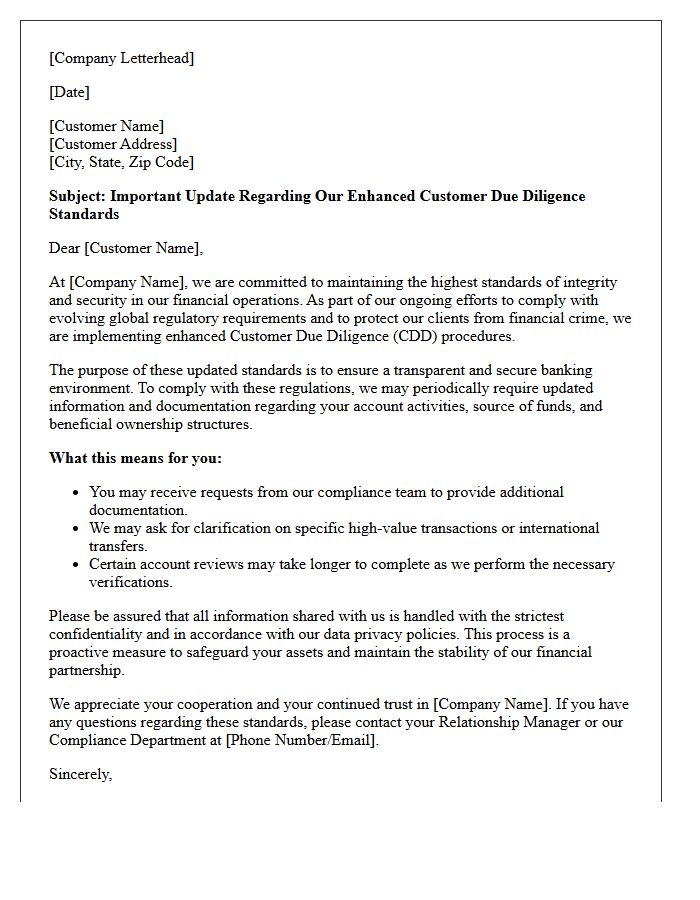

Executive Letter Regarding Enhanced Customer Due Diligence Standards

Financial institutions must implement an Executive Letter to formalize Enhanced Customer Due Diligence (ECDD) standards for high-risk profiles. This document establishes mandatory protocols for verifying the source of wealth and beneficial ownership. It ensures senior management oversight while aligning internal policies with global AML/CFT regulations. By defining clear risk appetite and investigative requirements, the letter mitigates legal exposure and prevents financial crimes. Adherence to these standards is critical for maintaining regulatory compliance and ensuring the integrity of the banking system during onboarding and ongoing monitoring of complex client entities.

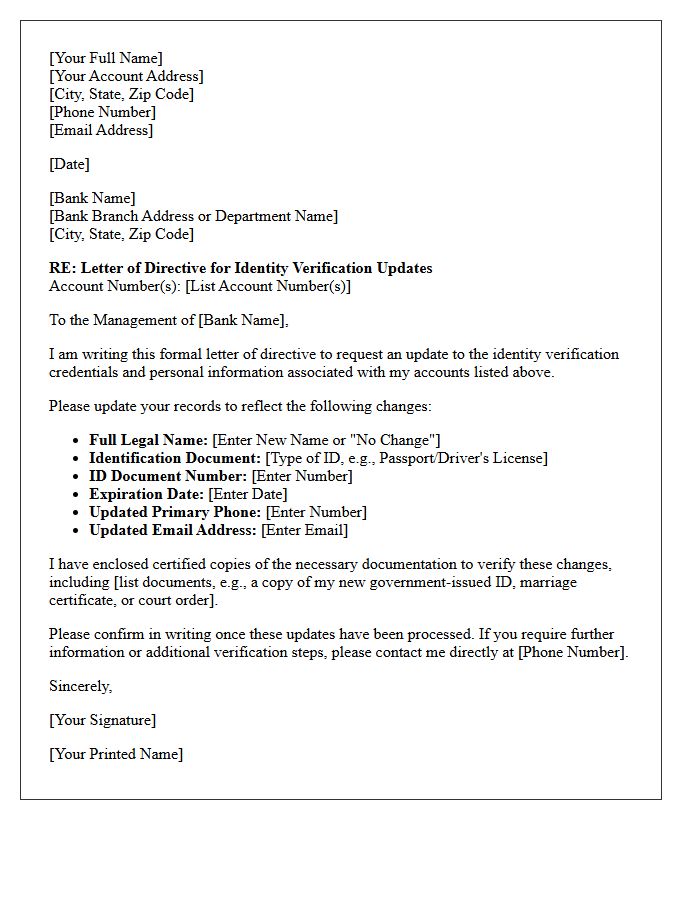

Letter of Directive for Banking Institution Identity Verification Updates

A Letter of Directive is a formal instruction used to update identity verification protocols within a banking institution. This document ensures compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. It mandates the submission of valid government-issued identification and proof of address to maintain account security. Timely adherence to these directives is crucial to prevent service interruptions or account freezes. Always verify the authenticity of the request through official channels to protect against identity theft and ensure your financial records remain accurate and secure.

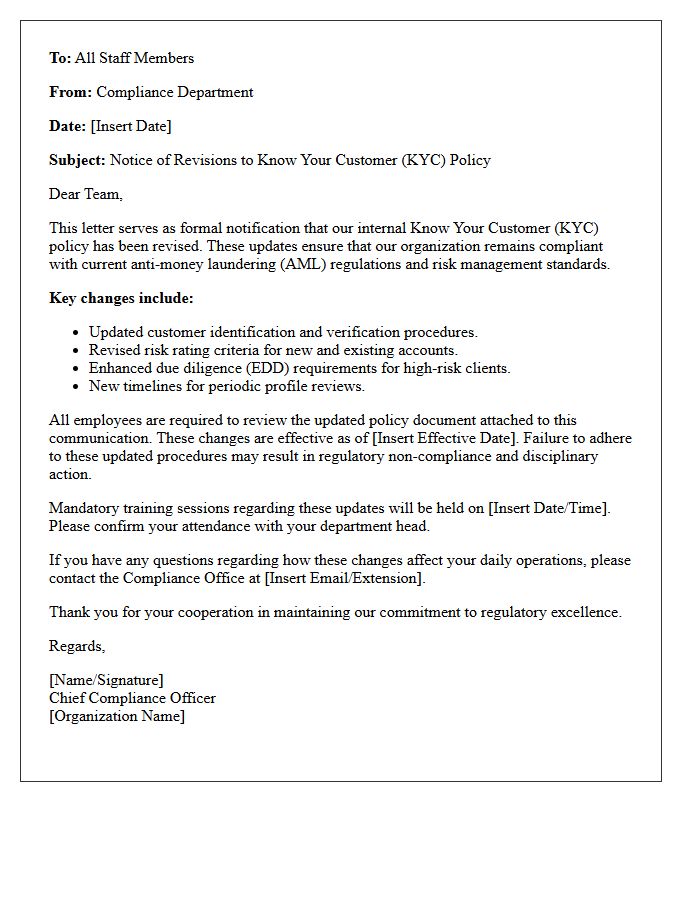

Internal Compliance Letter on Know Your Customer Policy Revisions

An internal compliance letter regarding Know Your Customer (KYC) policy revisions serves as a formal notification to staff about updated due diligence protocols. It outlines essential changes to identity verification, risk assessment, and monitoring procedures required to prevent financial crimes. Employees must acknowledge these updates to ensure regulatory alignment and mitigate operational risks. Adhering to these revised standards is mandatory to maintain AML compliance and protect the institution from legal penalties. Clear communication of these policy shifts ensures a unified approach to client onboarding and ongoing oversight within the organization.

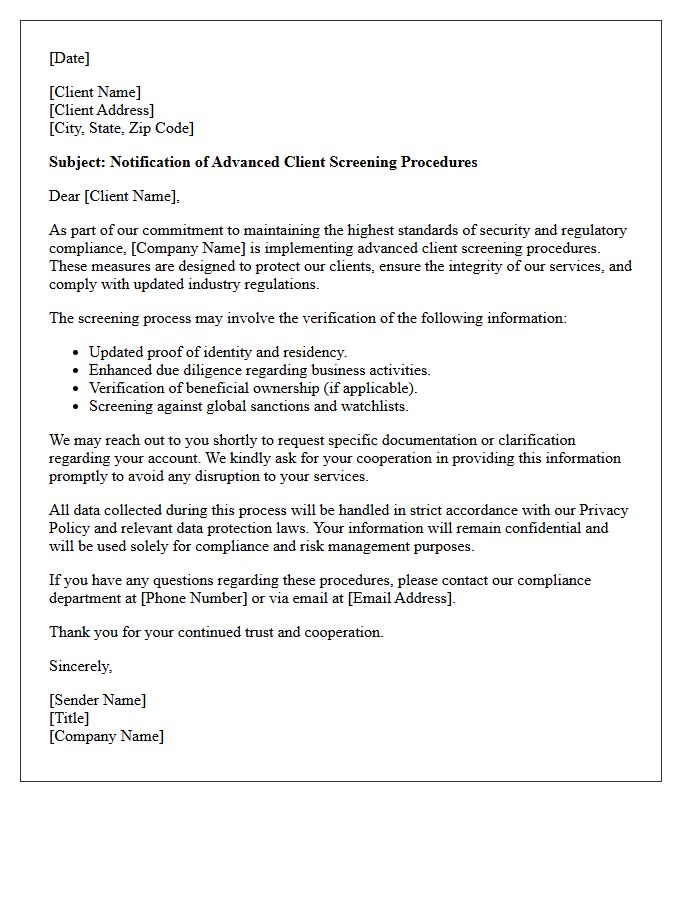

Letter of Notification for Advanced Client Screening Procedures

A Letter of Notification informs businesses that they must undergo Advanced Client Screening to comply with legal regulations. This process involves a rigorous verification of identity, financial history, and risk profiles to prevent fraud or money laundering. It is an essential step in modern due diligence, ensuring transparency between service providers and their clients. Recipients must provide accurate documentation promptly to maintain operational compliance and avoid potential service interruptions or legal complications during the onboarding phase.

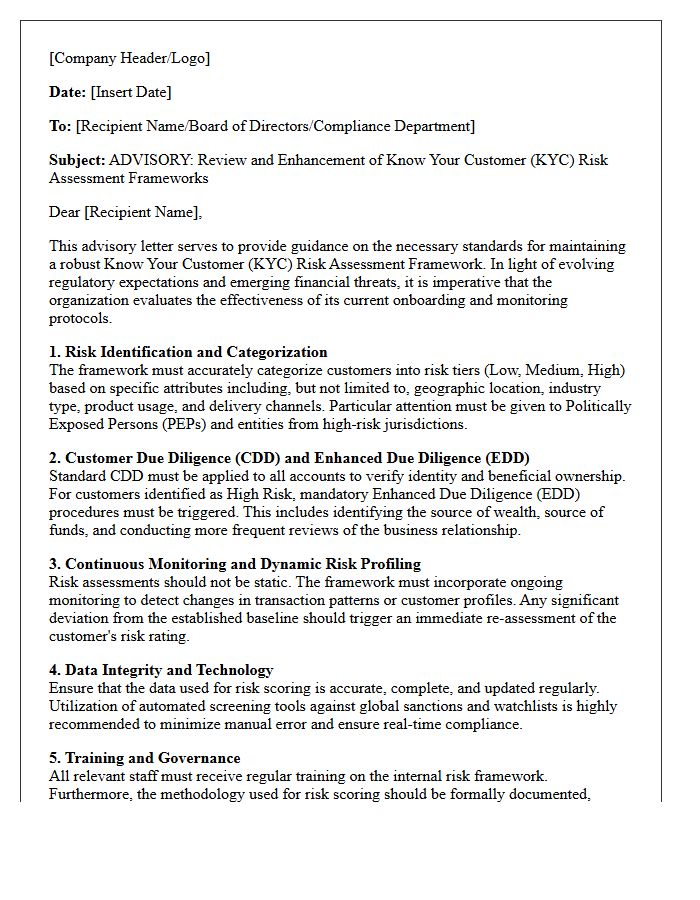

Advisory Letter on Know Your Customer Risk Assessment Frameworks

The Advisory Letter on Know Your Customer Risk Assessment Frameworks emphasizes the critical need for financial institutions to maintain robust Customer Risk Rating (CRR) models. It highlights that static systems often fail to capture evolving financial crime threats. Institutions must ensure their methodologies incorporate dynamic data, objective risk factors, and regular model validation to prevent illicit activity. Effective governance requires aligning risk appetites with actual customer profiles to mitigate money laundering and terrorism financing risks effectively within the global regulatory landscape.

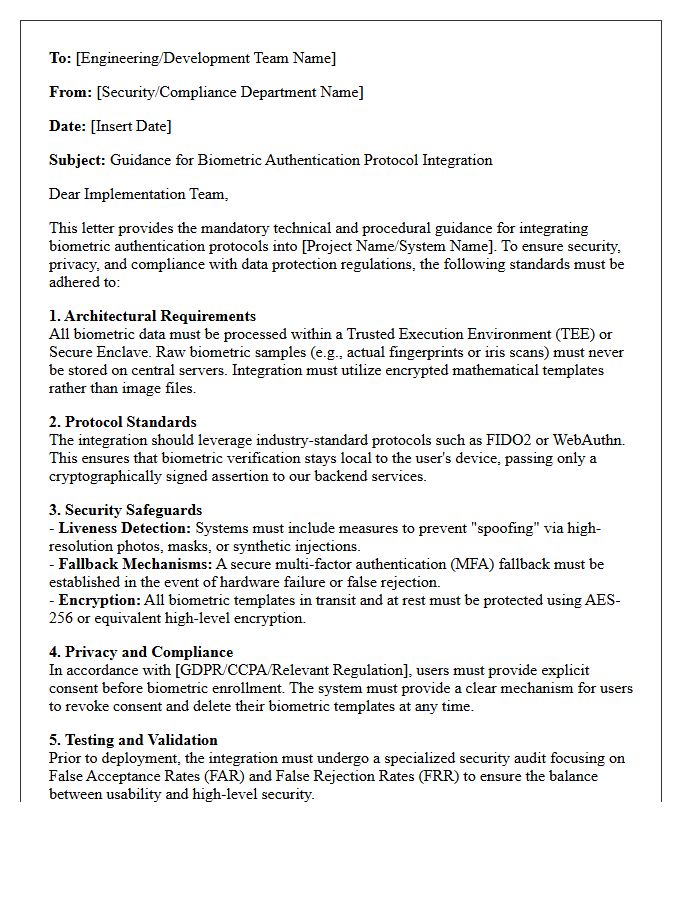

Letter of Guidance for Biometric Authentication Protocol Integration

A Letter of Guidance outlines the essential technical requirements and compliance standards for integrating a biometric authentication protocol. It serves as a formal roadmap, ensuring that identity verification systems align with security frameworks and interoperability mandates. Organizations must follow these instructions to guarantee data privacy, cryptographic integrity, and seamless user enrollment. Adhering to this guidance minimizes authentication failures and mitigates risks associated with unauthorized access. Understanding these protocols is vital for developers and stakeholders to achieve regulatory compliance while maintaining a robust digital security infrastructure during system deployment.

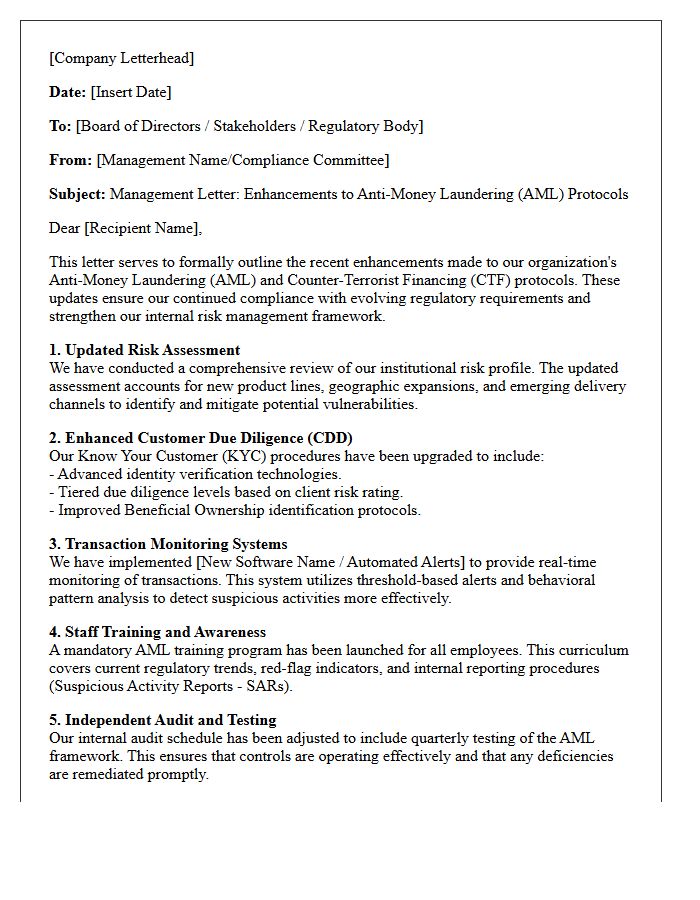

Management Letter Detailing Anti-Money Laundering Protocol Enhancements

A management letter detailing AML protocol enhancements provides a strategic roadmap for strengthening financial defenses. It outlines critical remediation steps necessary to address identified vulnerabilities in monitoring and reporting systems. This document ensures regulatory compliance by formalizing improvements to customer due diligence and risk assessment frameworks. By implementing these tailored recommendations, organizations effectively mitigate financial crime risks, improve operational transparency, and demonstrate a proactive commitment to maintaining institutional integrity and legal standards in an evolving global landscape.

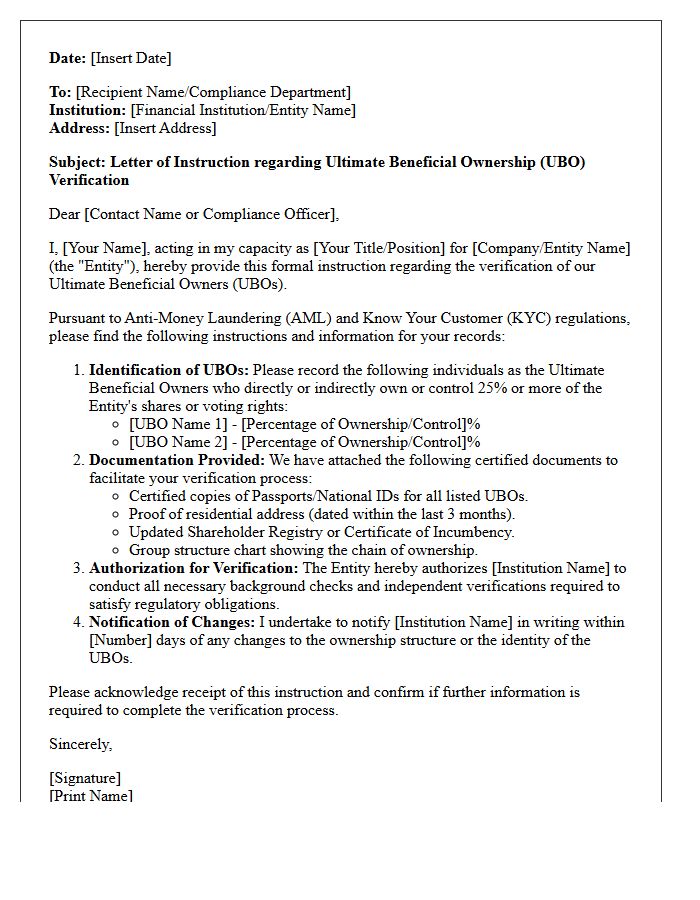

Letter of Instruction on Ultimate Beneficial Ownership Verification

The Letter of Instruction provides mandatory guidelines for the Ultimate Beneficial Ownership verification process. It ensures transparency by identifying individuals who exercise effective control or own at least 25% of a legal entity. Financial institutions use this document to comply with Anti-Money Laundering and Know Your Customer regulations. Providing accurate documentation prevents financial crimes and ensures regulatory adherence. Organizations must submit updated information to maintain legal standing and mitigate risks associated with transparency and hidden corporate structures.

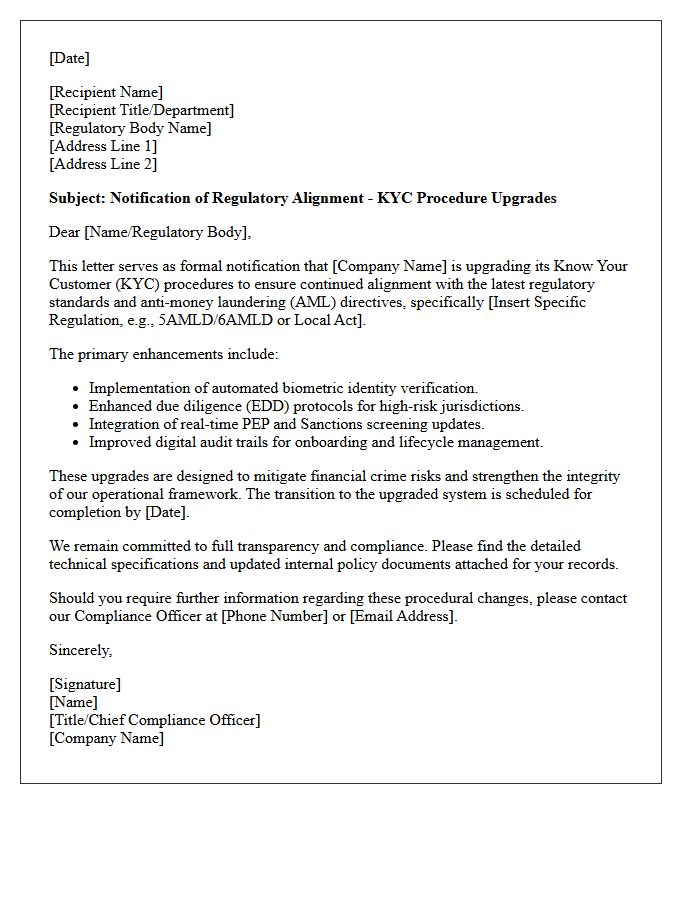

Regulatory Alignment Letter for Know Your Customer Procedure Upgrades

A Regulatory Alignment Letter is a formal document ensuring KYC procedure upgrades comply with evolving financial mandates. It serves as a compliance roadmap, bridging the gap between current verification protocols and new legal standards. This letter demonstrates proactive transparency to auditors and regulators, outlining specific enhancements in risk assessment and identity validation. By utilizing this document, institutions mitigate legal risks, prevent financial penalties, and ensure that internal systems remain aligned with global anti-money laundering (AML) frameworks during technical or operational transitions.

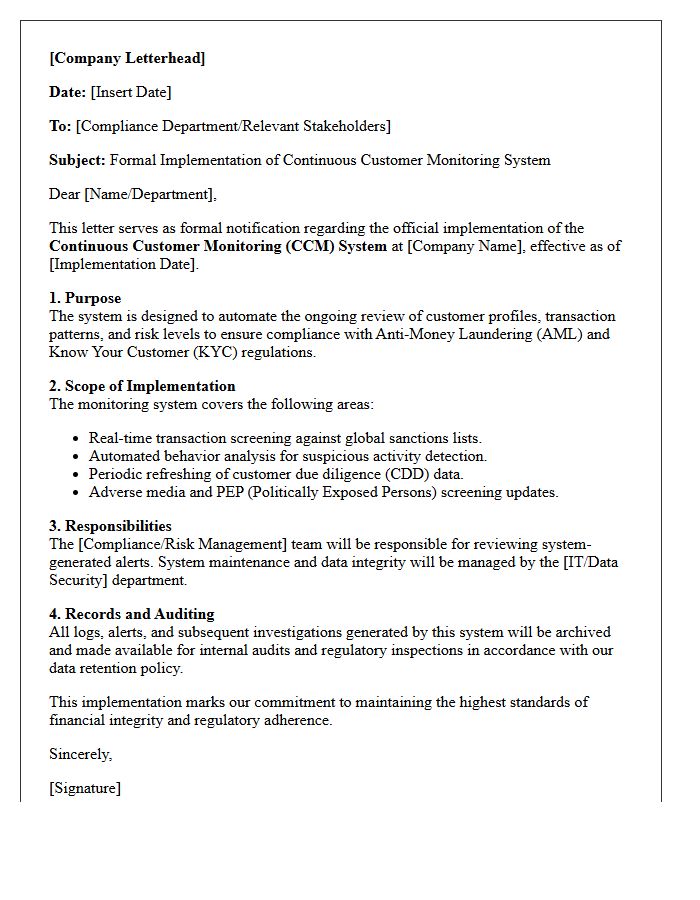

Letter of Implementation for Continuous Customer Monitoring Systems

A Letter of Implementation (LoI) serves as a formal commitment by financial institutions to deploy Continuous Customer Monitoring Systems. This document outlines the technical integration and strategic timeline for real-time surveillance tools. Its primary purpose is to ensure ongoing compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. By formalizing this process, organizations proactively mitigate risks associated with financial crime, providing regulators with documented proof that automated oversight mechanisms are active, effective, and capable of identifying suspicious behavioral patterns across the entire customer lifecycle.

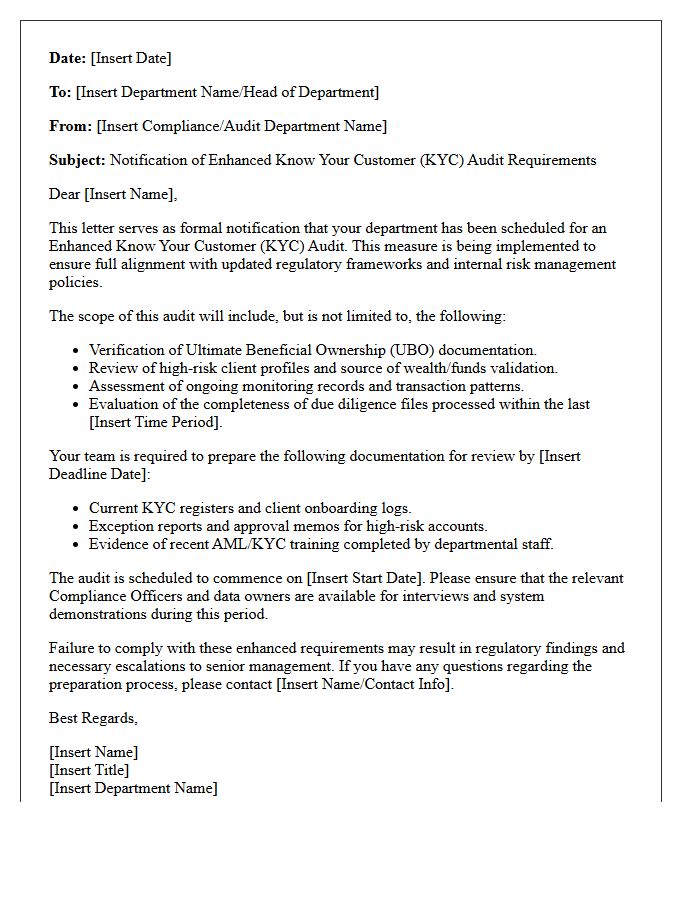

Departmental Letter on Enhanced Know Your Customer Audit Requirements

The Departmental Letter mandates strictly Enhanced Know Your Customer (EKC) audit standards to combat financial crimes. Financial institutions must implement rigorous verification processes to identify high-risk clients and beneficial owners. This regulatory update emphasizes continuous monitoring and robust data validation to ensure compliance with anti-money laundering protocols. Failure to adhere to these heightened due diligence requirements can result in severe legal penalties and operational restrictions. Maintaining accurate, real-time documentation is essential for passing upcoming regulatory examinations and ensuring organizational transparency.

What is the primary objective of the Memorandum on Know Your Customer (KYC) Protocol Enhancements?

The primary objective is to strengthen anti-money laundering (AML) frameworks and improve the accuracy of risk assessments by implementing more rigorous identity verification standards and continuous monitoring procedures.

Which specific identity verification methods are mandated by the new KYC protocol enhancements?

The enhancements mandate a multi-factor approach, integrating biometric authentication, real-time document validation against government databases, and advanced digital footprint analysis to ensure the authenticity of customer data.

How does the enhanced KYC protocol impact the onboarding process for high-risk entities?

High-risk entities are now subject to Enhanced Due Diligence (EDD), which requires comprehensive disclosure of ultimate beneficial ownership (UBO), source of wealth verification, and more frequent periodic reviews compared to standard accounts.

What are the requirements for ongoing monitoring under the updated KYC memorandum?

The memorandum requires automated transaction monitoring systems that flag suspicious patterns in real-time, coupled with a dynamic risk-scoring model that updates customer profiles based on behavioral changes or updated sanctions lists.

What are the regulatory compliance deadlines for implementing these KYC protocol upgrades?

Financial institutions and regulated entities must achieve full integration of the enhanced protocols within the timeframe specified in the memorandum's transitional provisions, typically involving a phased rollout starting with new account acquisitions.

Comments