A Mortgage Backing Guarantee Letter is a formal document where a third party, often a parent or financial institution, pledges to cover loan payments if the borrower defaults. This letter provides lenders with additional security, helping applicants qualify for larger amounts or better interest rates. Explore our comprehensive guide and see below are some ready to use template.

Image cover: Securing Home Financing: Mortgage Backing Guarantee Letter Samples and Templates

Letter Samples List

- Mortgage Backing Guarantee Letter

- Conditional Mortgage Commitment Letter

- Irrevocable Credit Guarantee Letter

- Bank Underwriting Approval Letter

- Financial Indemnity Guarantee Letter

- Corporate Sponsorship Guarantee Letter

- Collateral Pledge Guarantee Letter

- Primary Lender Comfort Letter

- Certified Funds Verification Letter

- Surety Bond Guarantee Letter

- Mortgage Default Indemnity Letter

- Repayment Obligation Guarantee Letter

- Third Party Guarantor Letter

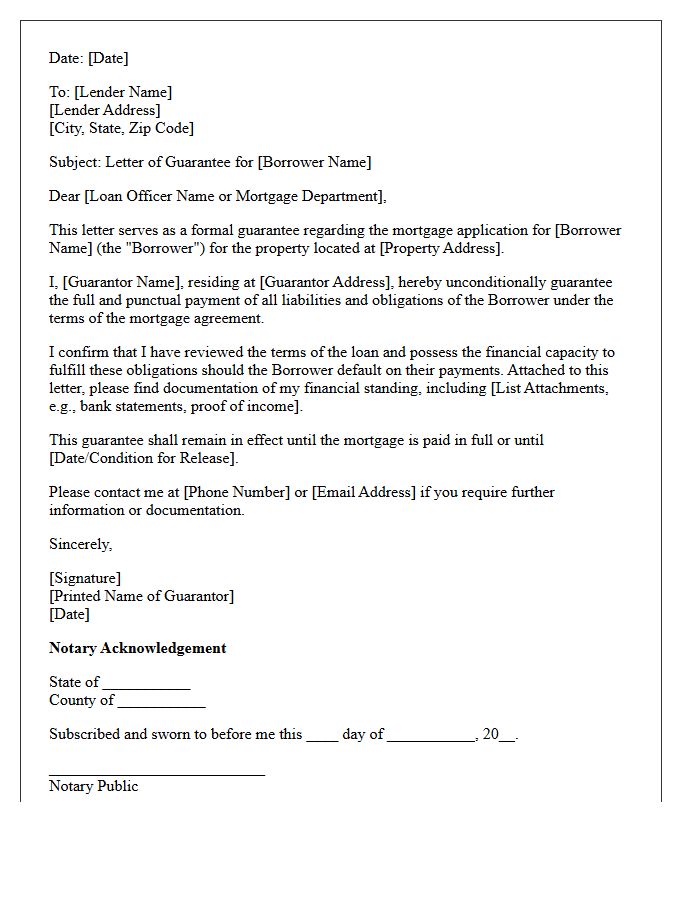

Mortgage Backing Guarantee Letter

A Mortgage Backing Guarantee Letter is a formal document issued by a financial institution to assure a seller that a buyer has secured the necessary funding for a property purchase. This letter acts as a financial safety net, confirming that the lender will cover the mortgage obligations if specific conditions are met. It enhances the buyer's credibility during negotiations by reducing the risk of transaction failure. Understanding this guarantee is essential for ensuring payment security and streamlining the closing process in competitive real estate markets.

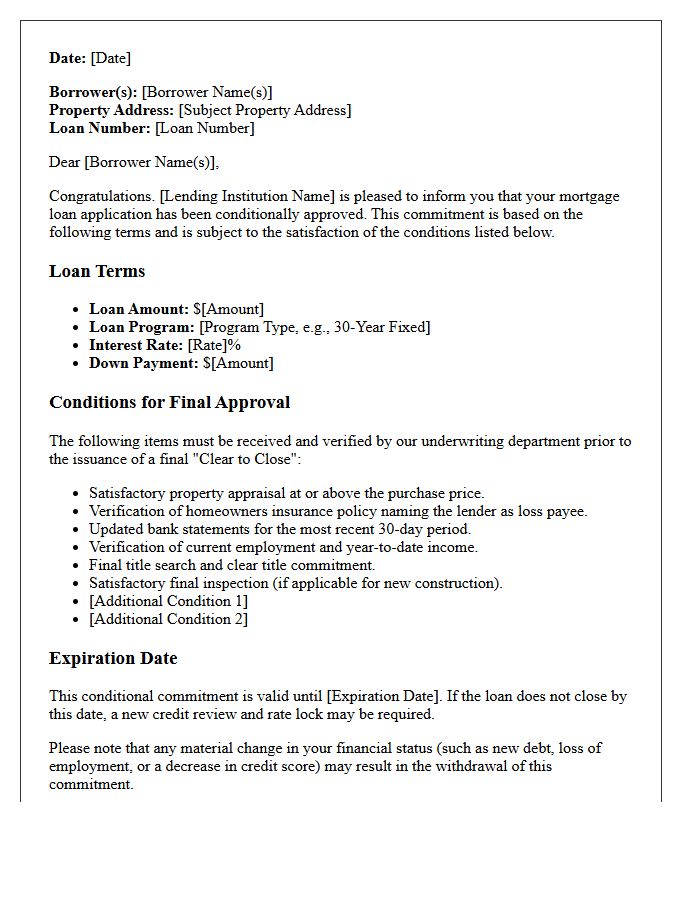

Conditional Mortgage Commitment Letter

A Conditional Mortgage Commitment Letter is a formal document from a lender indicating they are willing to fund your loan, provided you meet specific underwriting requirements. Unlike a pre-approval, this commitment is issued after a preliminary review of your credit and finances. To secure final approval, you must satisfy outstanding conditions such as property appraisals, employment verification, or additional financial documentation. Understanding these contingencies is essential, as the loan is not guaranteed until every requirement is met and the file is cleared to close.

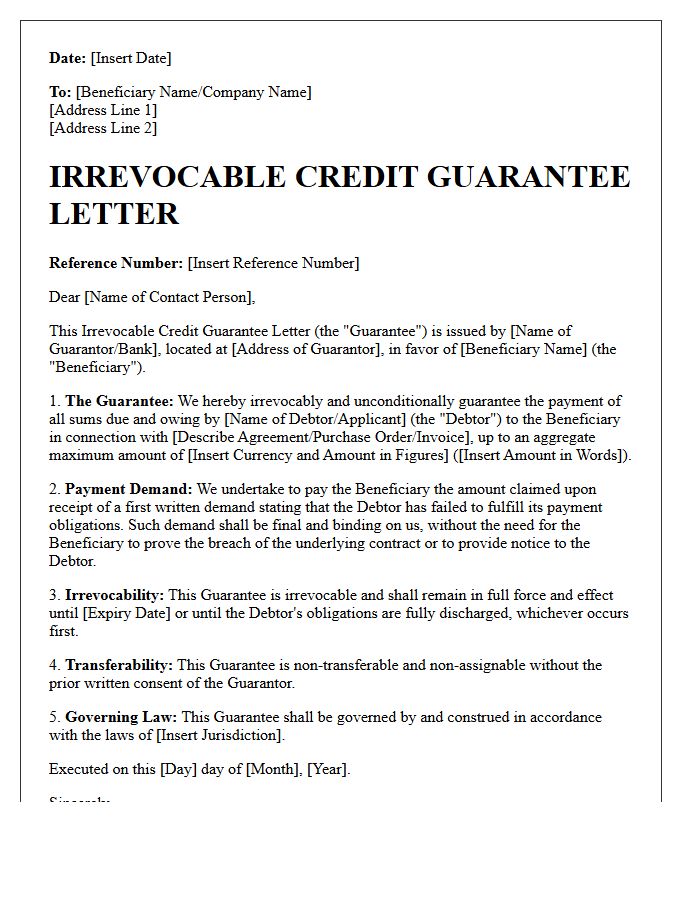

Irrevocable Credit Guarantee Letter

An Irrevocable Credit Guarantee Letter is a binding financial instrument issued by a bank to guarantee payment to a beneficiary. Unlike standard agreements, it cannot be cancelled or modified without the explicit consent of all involved parties. This document provides maximum security in international trade by ensuring the issuing bank assumes the payment obligation if the applicant defaults. It serves as a critical risk mitigation tool, building trust between exporters and importers by guaranteeing that financial commitments are honored regardless of changes in the buyer's circumstances.

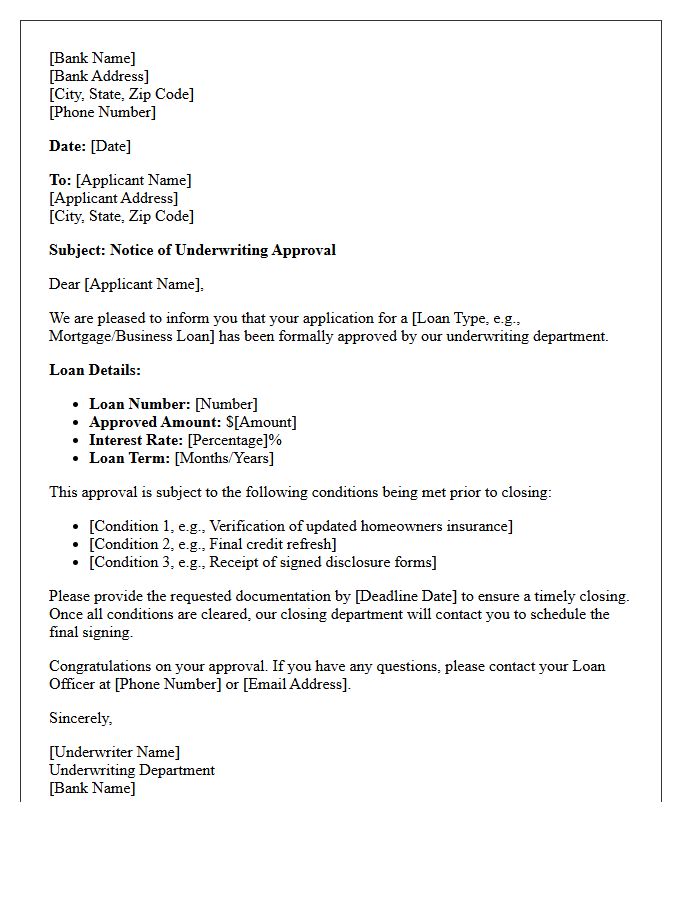

Bank Underwriting Approval Letter

A Bank Underwriting Approval Letter is the final commitment from a lender confirming your mortgage is fully authorized. Unlike a pre-approval, this document signifies that an underwriter has verified your financial documentation, including income, credit, and assets. It typically contains specific conditions that must be met before closing, such as updated paystubs or property inspections. Receiving this letter means the bank has formally agreed to fund your loan, moving you toward the final "clear to close" stage of the home-buying process.

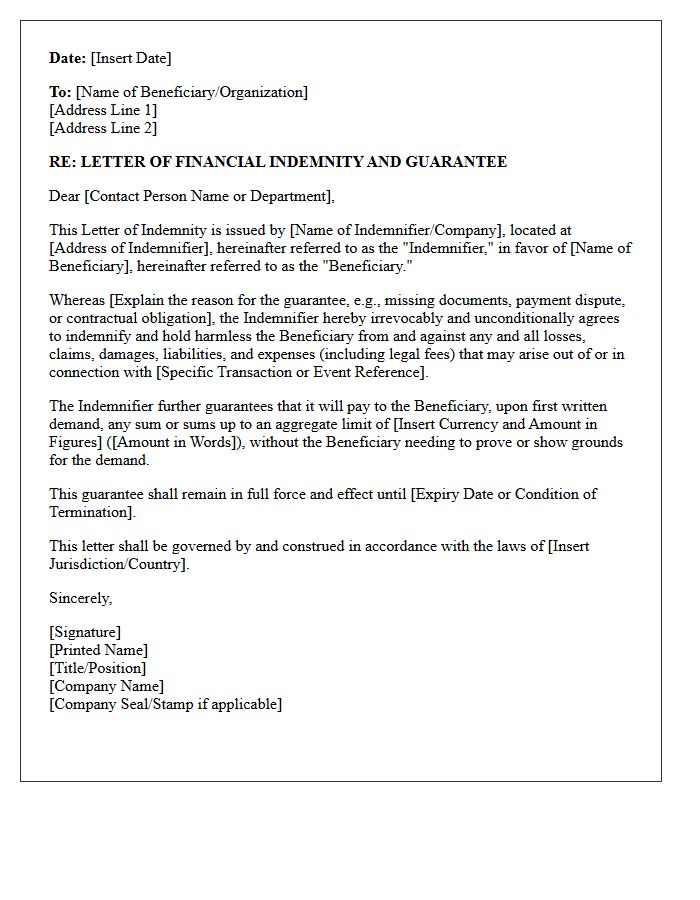

Financial Indemnity Guarantee Letter

A Financial Indemnity Guarantee Letter is a binding legal commitment issued by a bank or insurance company. It ensures that a specific financial obligation will be met if the principal party fails to perform. This document acts as a safeguard, protecting the beneficiary from monetary loss during high-stakes transactions. It is essential for securing international trade contracts and large-scale projects, providing creditors with the security that they will be compensated for damages or defaults, thereby mitigating risk and establishing trust between commercial partners.

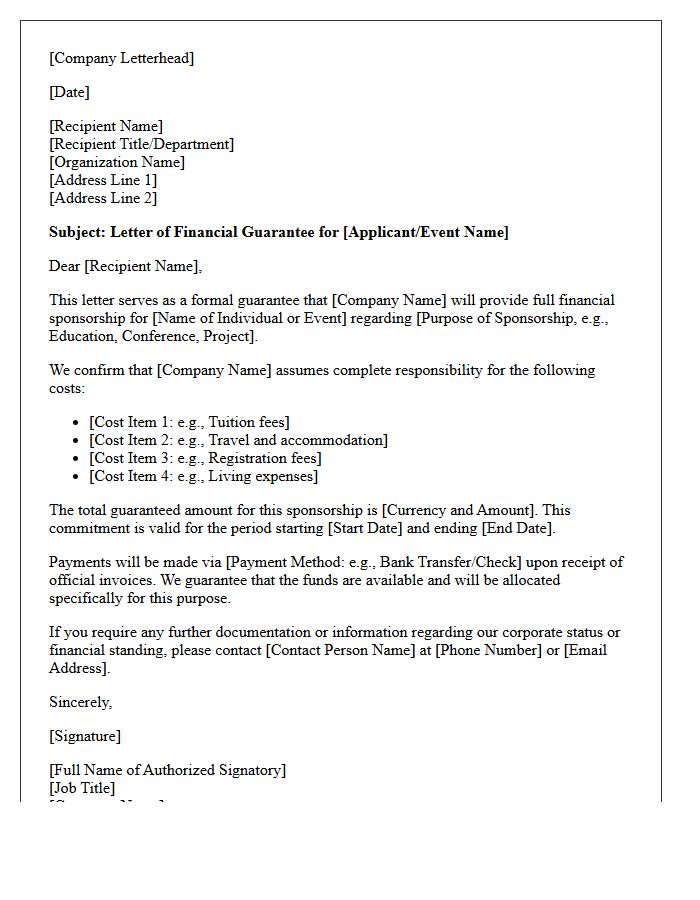

Corporate Sponsorship Guarantee Letter

A Corporate Sponsorship Guarantee Letter is a formal legal commitment where a business pledges to cover all financial costs for an individual, such as tuition fees, travel, or living expenses. This document acts as proof of funding for visa applications or university admissions. It must be issued on official company letterhead, clearly stating the sponsor's contact details, the specific funding duration, and the exact expenses included. Providing this verified assurance minimizes financial risk for institutions and demonstrates the organization's full financial accountability for the sponsored candidate.

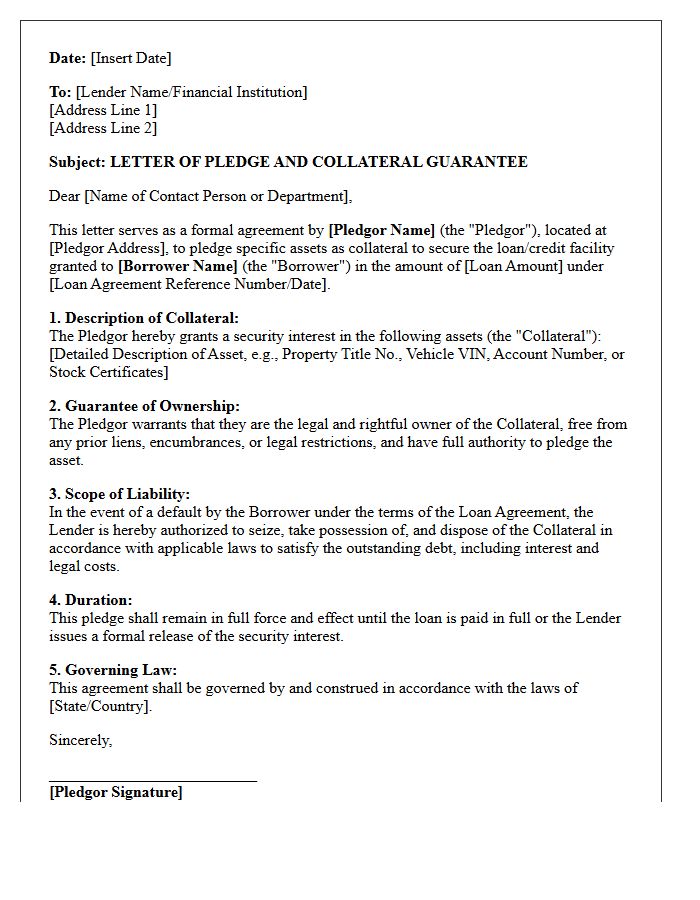

Collateral Pledge Guarantee Letter

A Collateral Pledge Guarantee Letter is a formal legal document where a promisor commits specific assets as security for a loan. This instrument ensures the lender can seize the pledged property if the borrower defaults on repayment obligations. Key elements include a detailed description of the assets, the scope of the debt, and terms of release. It serves as a binding assurance that minimizes financial risk for creditors while facilitating credit access for borrowers by leveraging existing equity to secure favorable financing terms.

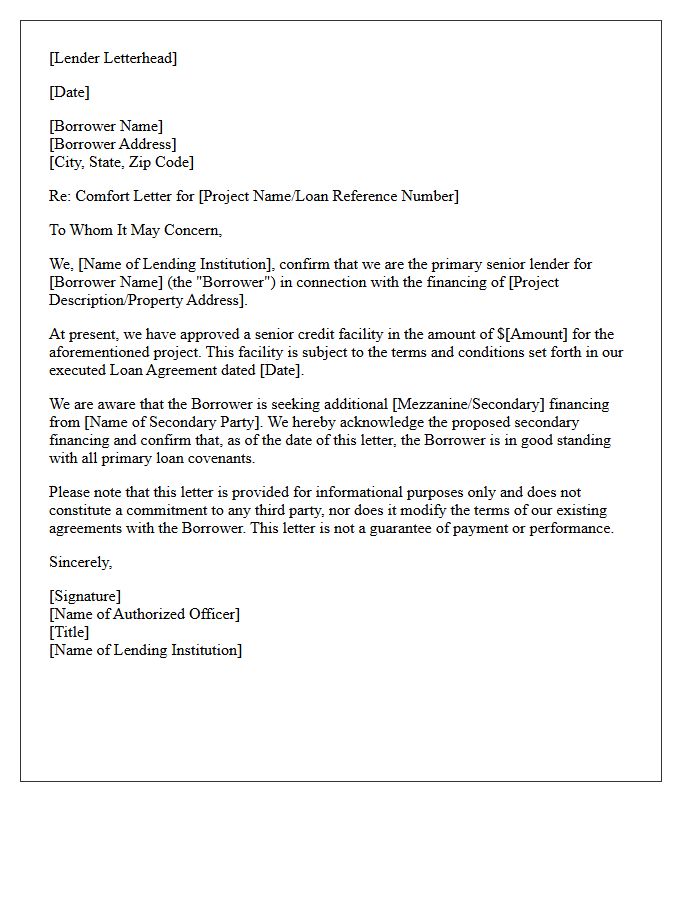

Primary Lender Comfort Letter

A Primary Lender Comfort Letter is a formal document issued by a senior mortgagee to a subordinate party, typically a ground lessor or secondary lender. It provides financial reassurance by outlining the primary lender's commitment to notify the recipient of any loan defaults. This letter establishes intercreditor communication protocols and may detail specific cure rights or foreclosure procedures. Understanding these terms is essential for protecting collateral interests and ensuring structural transparency within complex real estate financing agreements or commercial leasehold transactions.

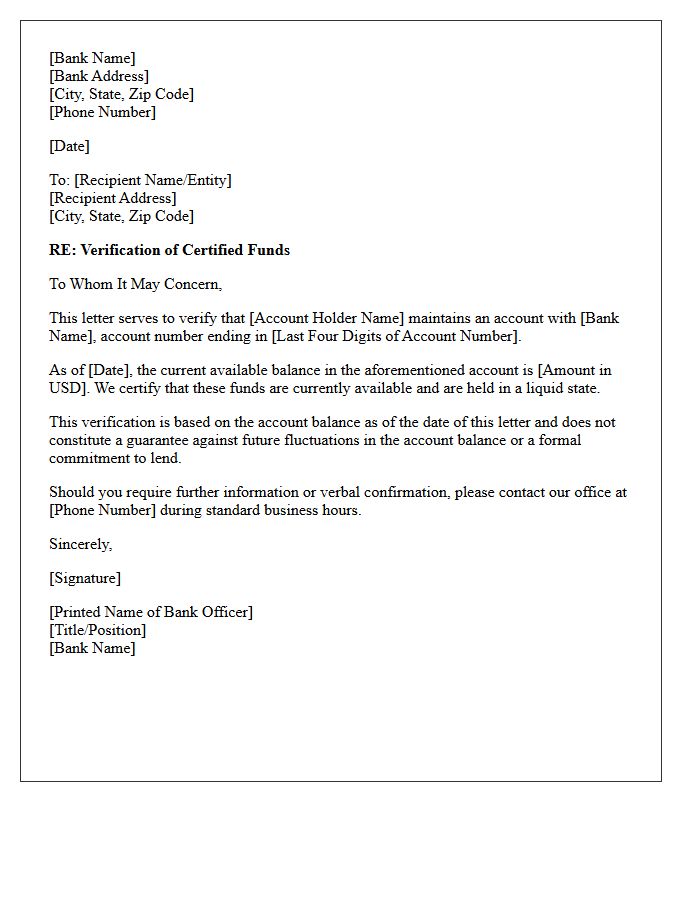

Certified Funds Verification Letter

A Certified Funds Verification Letter is a formal document issued by a financial institution to confirm that a client holds sufficient liquid assets for a specific transaction. This official statement reassures sellers or lenders that the necessary capital is readily available and cleared for use. Often required in high-value real estate or business acquisitions, it serves as a guarantee of financial capacity, reducing risk for all parties involved. Unlike a simple balance inquiry, it validates that funds are legitimate, accessible, and reserved for the intended purchase, ensuring a smoother closing process.

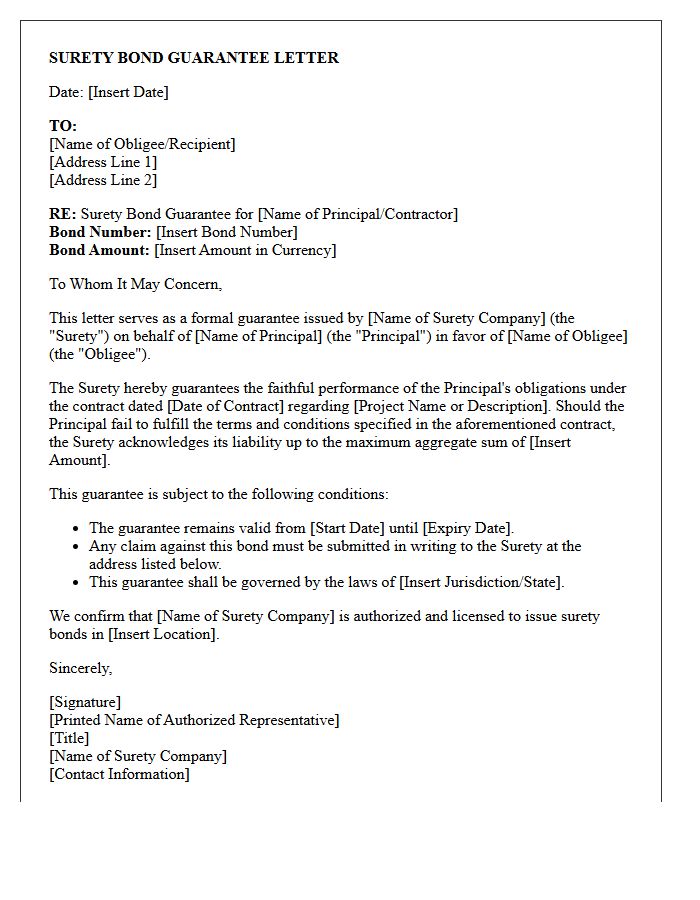

Surety Bond Guarantee Letter

A Surety Bond Guarantee Letter is a formal commitment issued by a bank or insurance provider to ensure contractual compliance. It acts as a financial safeguard, promising that a principal will fulfill their legal or professional obligations to an obligee. If the principal fails to perform, the issuer compensates the beneficiary for losses. This document is essential in construction and trade to mitigate financial risk, build trust, and verify that a business possesses the necessary liquidity and backing to complete specific projects or satisfy regulatory requirements effectively.

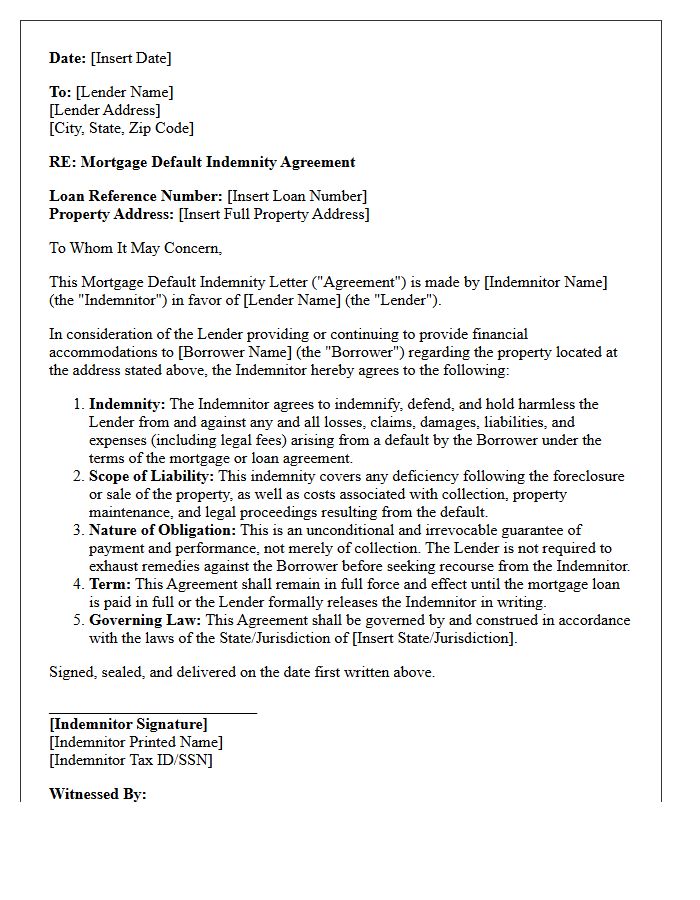

Mortgage Default Indemnity Letter

A Mortgage Default Indemnity Letter is a binding legal commitment where a third party guarantees to compensate a lender for financial losses resulting from a borrower's default. This document mitigates risk by providing an extra layer of security, often required for high-risk loans or complex corporate financing. It ensures the lender is "held harmless" against shortfalls in loan recovery. Understanding the specific indemnity triggers and the scope of liability is essential for guarantors to avoid unexpected financial obligations if the primary borrower fails to meet repayment terms.

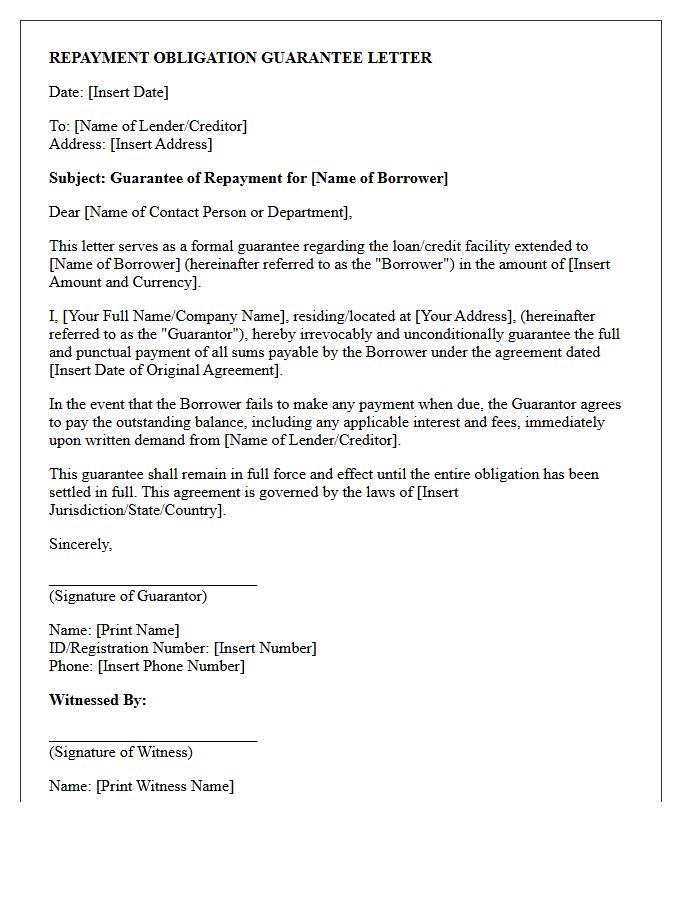

Repayment Obligation Guarantee Letter

A Repayment Obligation Guarantee Letter is a formal legal document where a third party, often a bank or parent company, commits to fulfilling a debt if the borrower defaults. This irrevocable commitment provides essential security to lenders, significantly reducing credit risk during financial transactions. It ensures that the principal amount and accrued interest are recovered, fostering trust in international trade and lending. Understanding the specific terms and conditions within the letter is vital, as it dictates the legal enforceability and the exact scope of the guarantor's financial liability.

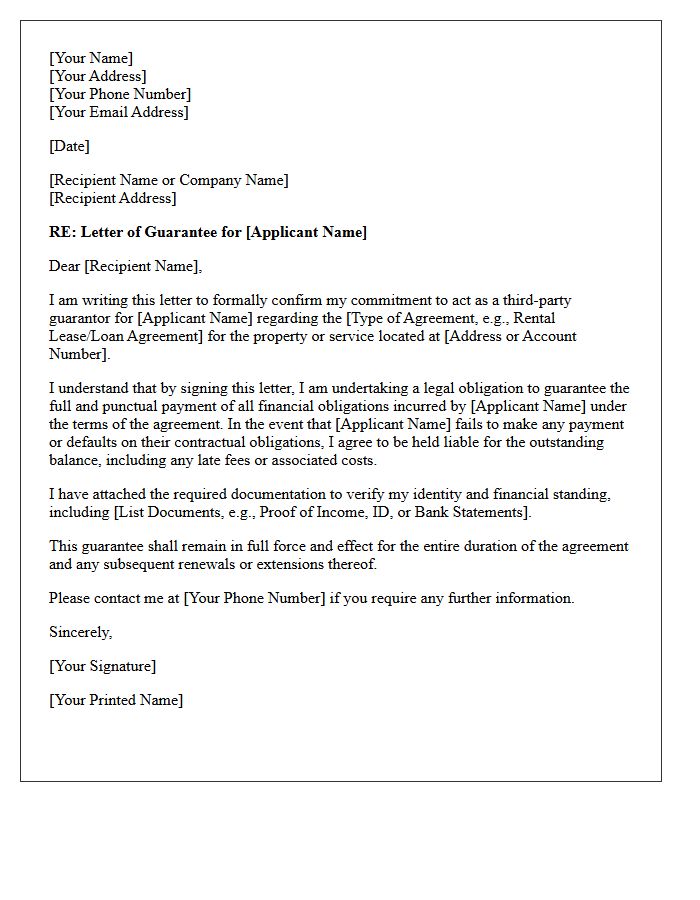

Third Party Guarantor Letter

A Third Party Guarantor Letter is a legally binding document where an individual or entity agrees to take financial responsibility for a tenant's or borrower's obligations. This is essential when an applicant lacks sufficient income or credit history. By signing, the guarantor promises to cover unpaid rent, damages, or loan defaults if the primary party fails to pay. Landlords and lenders use this to mitigate risk, ensuring financial security. It is vital to understand that the guarantor remains liable for the full duration of the contract terms.

What is a Mortgage Backing Guarantee Letter?

A Mortgage Backing Guarantee Letter is a formal document issued by a financial institution or a third-party guarantor that promises to cover the mortgage repayment obligations if the primary borrower defaults on the loan.

Who typically requires a Mortgage Backing Guarantee Letter?

Lenders often require this letter when a borrower has a limited credit history, insufficient income to meet debt-to-income ratios, or is applying for a high-value commercial mortgage that necessitates additional security.

What are the essential components of a Mortgage Backing Guarantee Letter?

The letter must include the guarantor's legal identity, the specific loan account details, the maximum guaranteed amount, the duration of the guarantee, and the specific conditions under which the guarantee can be invoked.

Is a Mortgage Backing Guarantee Letter legally binding?

Yes, it is a legally enforceable contract. By signing the letter, the guarantor assumes legal liability for the debt, allowing the lender to seek repayment directly from the guarantor in the event of a borrower default.

How does a Mortgage Backing Guarantee Letter affect loan approval?

It significantly reduces the risk for the lender, which can lead to higher chances of loan approval, more favorable interest rates, and the ability to secure a larger principal amount than the borrower would qualify for alone.

Comments