Securing your first property is easier with a First-Time Homebuyer Mortgage Discount Letter. This formal request helps eligible buyers negotiate lower interest rates or reduced closing costs by highlighting their qualifications and specific program eligibility. Using a professional format can significantly increase your chances of saving thousands over the life of your loan. Below are some ready to use templates.

Image cover: Winning the Best Rates: First-Time Homebuyer Mortgage Discount Letter Templates

Letter Samples List

- Promotional Offer Letter for First-Time Homebuyer Mortgage Discount

- Application Acknowledgment Letter for First-Time Homebuyer Mortgage Discount

- Pre-Approval Letter for First-Time Homebuyer Mortgage Discount

- Eligibility Confirmation Letter for First-Time Homebuyer Mortgage Discount

- Conditional Approval Letter for First-Time Homebuyer Mortgage Discount

- Interest Rate Reduction Letter for First-Time Homebuyer Mortgage Discount

- Closing Cost Waiver Letter for First-Time Homebuyer Mortgage Discount

- Rate Lock Agreement Letter for First-Time Homebuyer Mortgage Discount

- Missing Documentation Request Letter for First-Time Homebuyer Mortgage Discount

- Final Commitment Letter for First-Time Homebuyer Mortgage Discount

- Approval Letter for First-Time Homebuyer Mortgage Discount

- Closing Disclosure Letter for First-Time Homebuyer Mortgage Discount

- Post-Closing Welcome Letter for First-Time Homebuyer Mortgage Discount

- Adverse Action Letter for First-Time Homebuyer Mortgage Discount

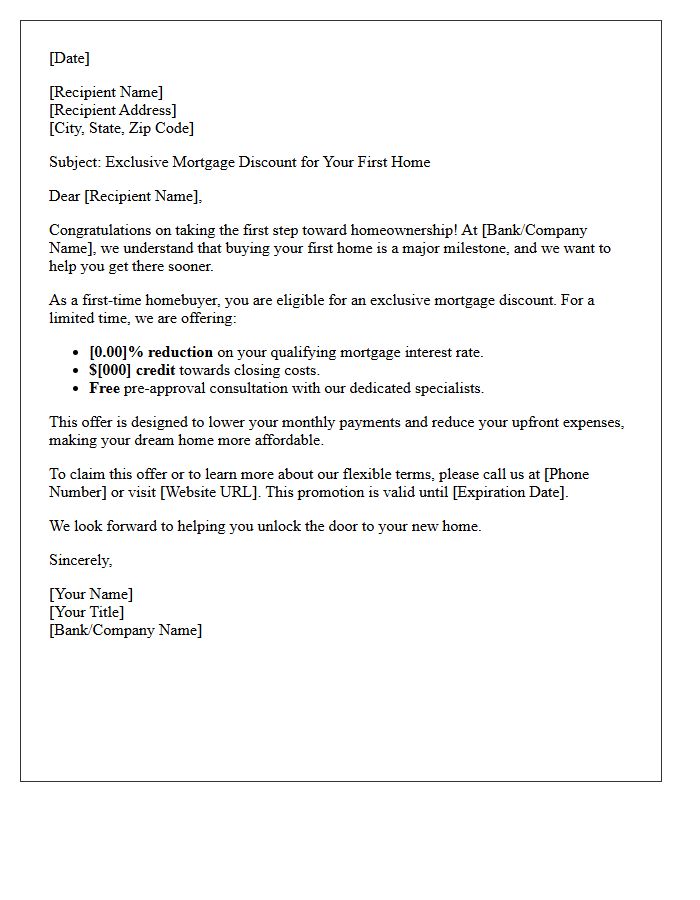

Promotional Offer Letter for First-Time Homebuyer Mortgage Discount

A promotional offer letter for a mortgage discount provides first-time buyers with reduced interest rates or credited closing costs. This document serves as a formal invitation to secure affordable financing by lowering the overall cost of homeownership. Key details typically include the specific percentage reduction, eligibility criteria, and a clear expiration date. Understanding these incentives is essential for maximizing savings during your initial property purchase. Always verify the terms and conditions to ensure the offer aligns with your long-term financial goals and credit profile.

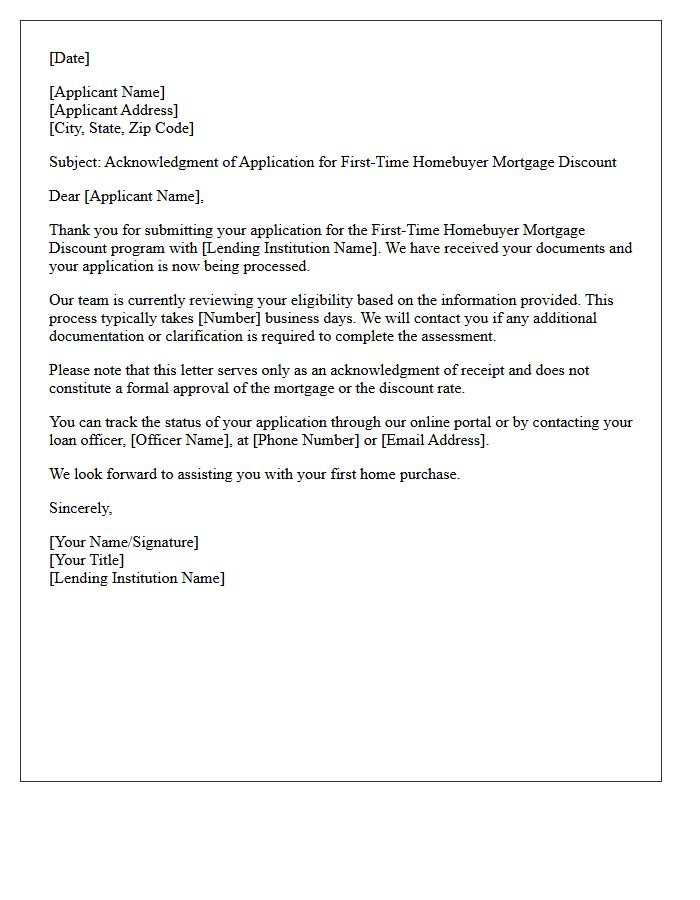

Application Acknowledgment Letter for First-Time Homebuyer Mortgage Discount

An Application Acknowledgment Letter confirms that your lender has received your request for a first-time homebuyer mortgage discount. This vital document serves as official proof of your application status and outlines the next steps in the verification process. It typically details the specific financial incentives or reduced interest rates you are applying for. Retaining this letter is essential for tracking your progress and ensuring you meet all eligibility requirements to secure lower closing costs or specialized down payment assistance during your home purchase journey.

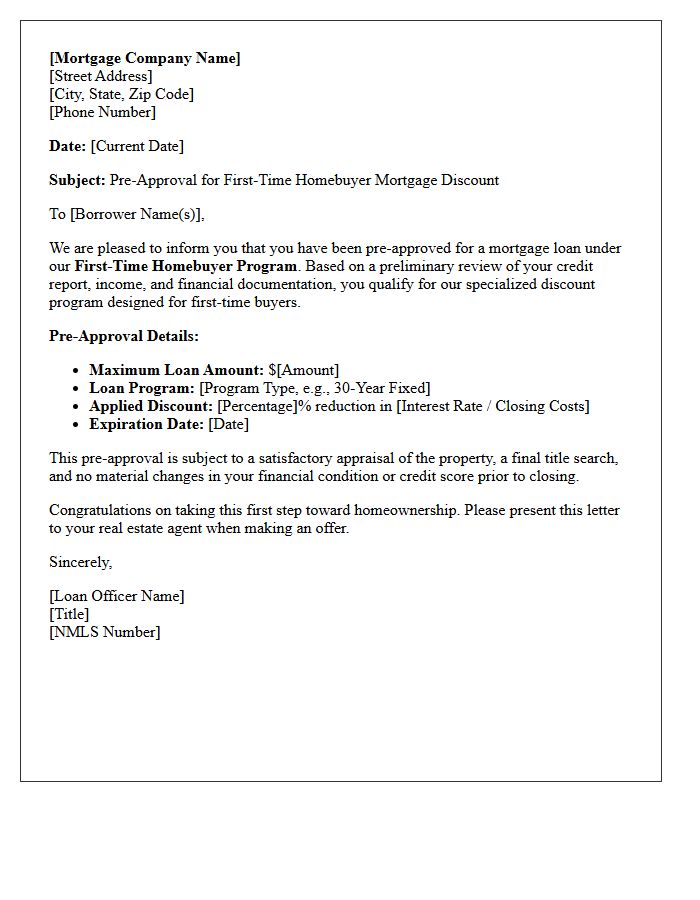

Pre-Approval Letter for First-Time Homebuyer Mortgage Discount

A Pre-Approval Letter is the most critical document for a first-time buyer, confirming your maximum loan amount and budget. It demonstrates financial credibility to sellers, making your offer competitive. For those seeking a mortgage discount, this letter often serves as the gateway to specialized programs like lower interest rates or reduced closing costs tailored for beginners. To secure these benefits, lenders evaluate your credit score and debt-to-income ratio. Obtaining this document early ensures you understand your purchasing power while locking in potential savings specifically designed for first-time homeowners.

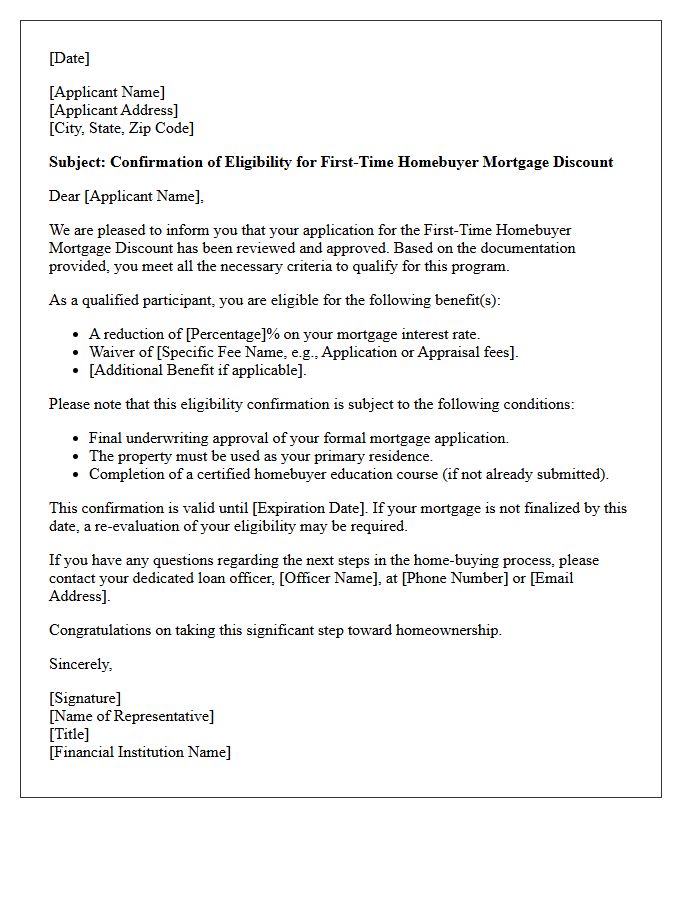

Eligibility Confirmation Letter for First-Time Homebuyer Mortgage Discount

An Eligibility Confirmation Letter serves as official proof that you qualify for a first-time homebuyer mortgage discount. Issued by government agencies or lenders, this document verifies you meet specific criteria, such as income limits and having not owned property in the last three years. Presenting this letter during the loan application process helps secure lower interest rates, reduced down payments, or tax credits. It is a vital tool for improving affordability and ensuring you receive the financial incentives reserved for new homeowners.

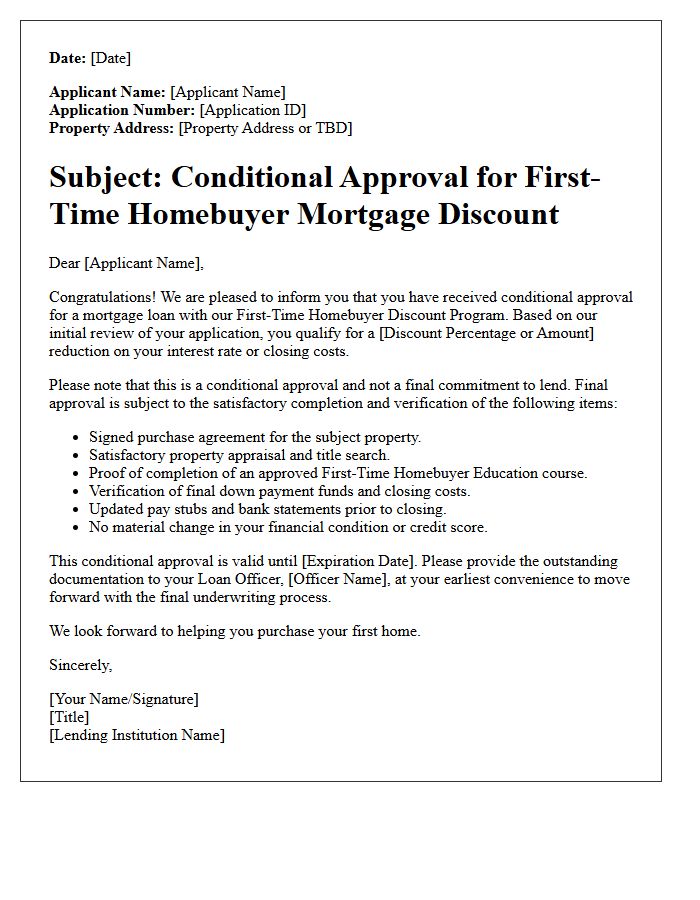

Conditional Approval Letter for First-Time Homebuyer Mortgage Discount

A Conditional Approval Letter is a critical document for first-time buyers seeking a mortgage discount. It signifies that a lender has verified your financial profile, including credit and income, pending specific final requirements like a home appraisal. Securing this pre-validation strengthens your bargaining power and confirms your eligibility for specialized interest rate reductions or down payment assistance. Obtaining this letter early ensures you meet the strict criteria for first-time homebuyer incentives while proving to sellers that your financing is robust and nearly finalized.

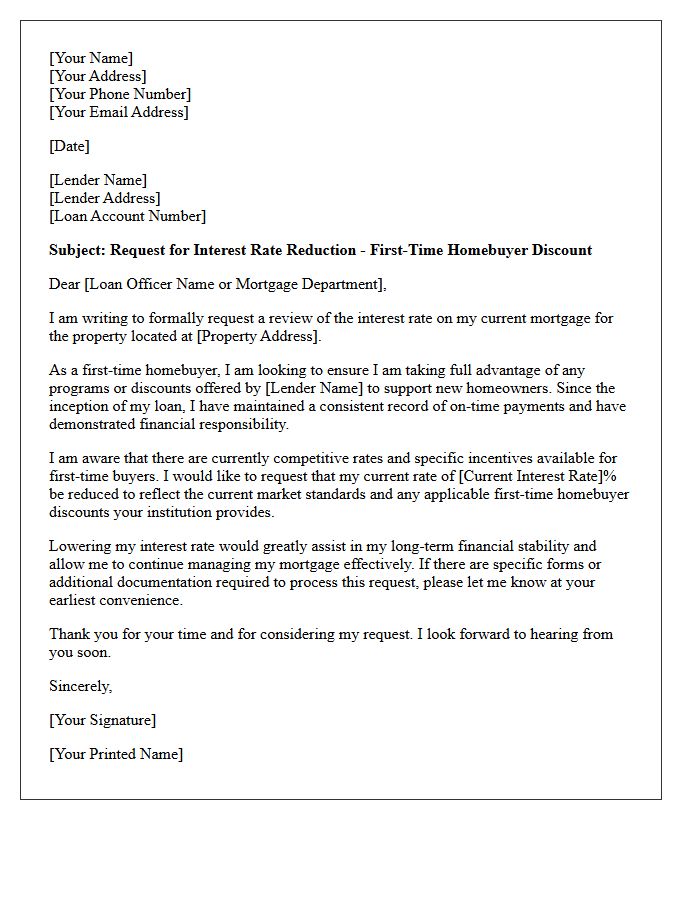

Interest Rate Reduction Letter for First-Time Homebuyer Mortgage Discount

A mortgage interest rate reduction letter is a formal request to your lender to lower your monthly payments. For first-time homebuyers, this document leverages market rate fluctuations or improved credit scores to secure a discount on an existing loan. To be effective, the letter should highlight your consistent payment history and current financial stability. Successfully negotiating a lower interest rate can save thousands of dollars over the life of the mortgage, making it an essential tool for long-term affordability and financial management for new homeowners.

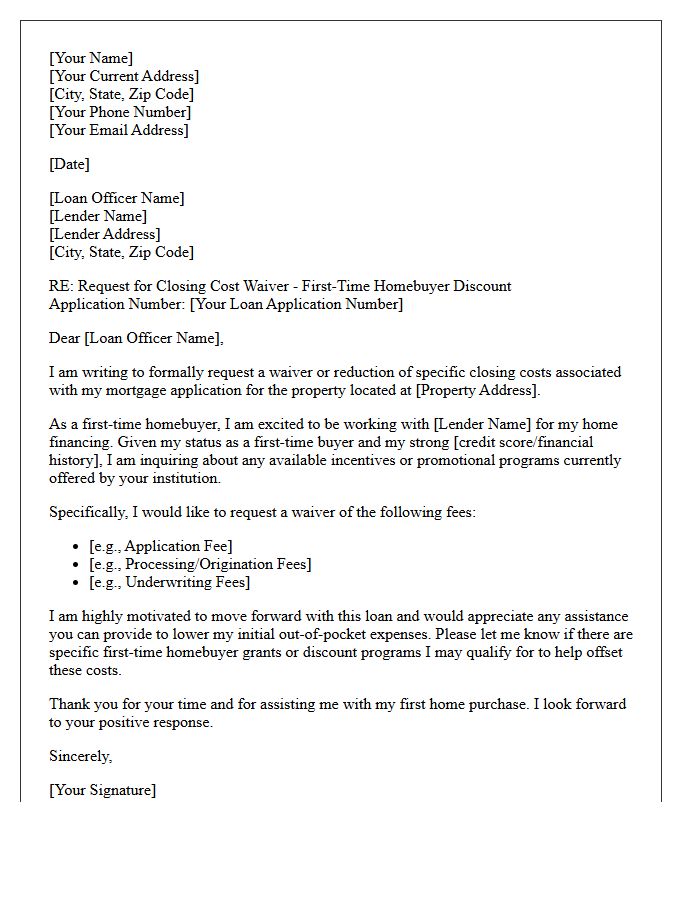

Closing Cost Waiver Letter for First-Time Homebuyer Mortgage Discount

A Closing Cost Waiver Letter is a formal request to a lender to reduce or eliminate upfront fees for a first-time homebuyer mortgage. This document highlights your eligibility based on creditworthiness, income limits, or specific government-backed programs. By successfully obtaining this discount, you significantly decrease your out-of-pocket expenses at settlement. Lenders may grant waivers to attract loyal borrowers or meet community reinvestment goals. Always ensure the letter clearly references the specific mortgage discount program you are applying for to maximize your potential savings during the home purchase process.

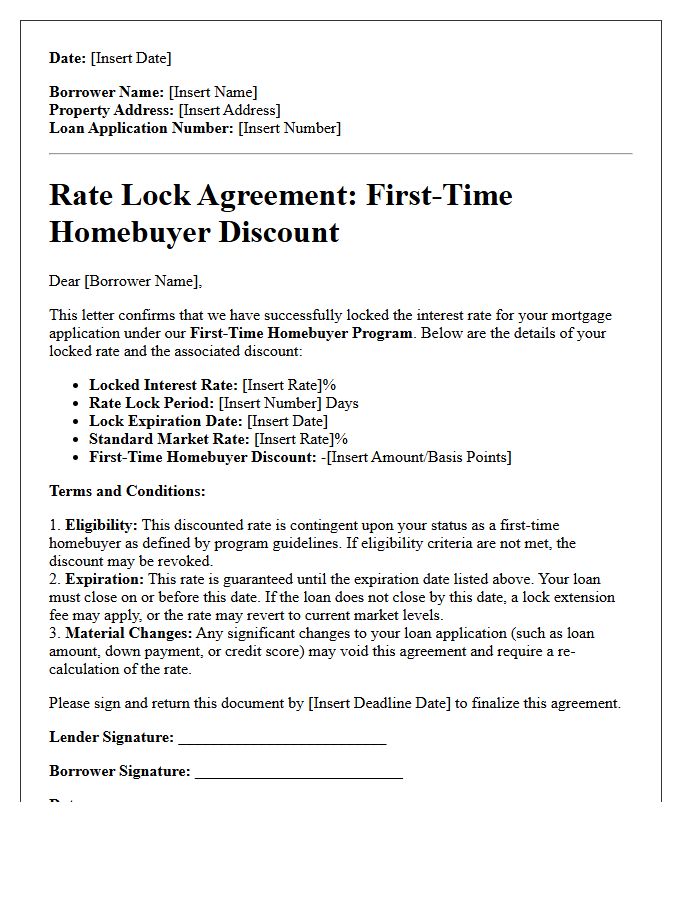

Rate Lock Agreement Letter for First-Time Homebuyer Mortgage Discount

A Rate Lock Agreement Letter is a vital document securing your mortgage interest rate for a specific period. For first-time homebuyers, this guarantees that market fluctuations will not increase your monthly payment before closing. It typically outlines the agreed rate, expiration date, and any applicable discount points or fees. Reviewing this letter ensures you receive the promised financial incentives and low-interest benefits tailored for new buyers. Always confirm the lock duration is sufficient to cover your entire underwriting process to avoid unexpected costs or losing your rate.

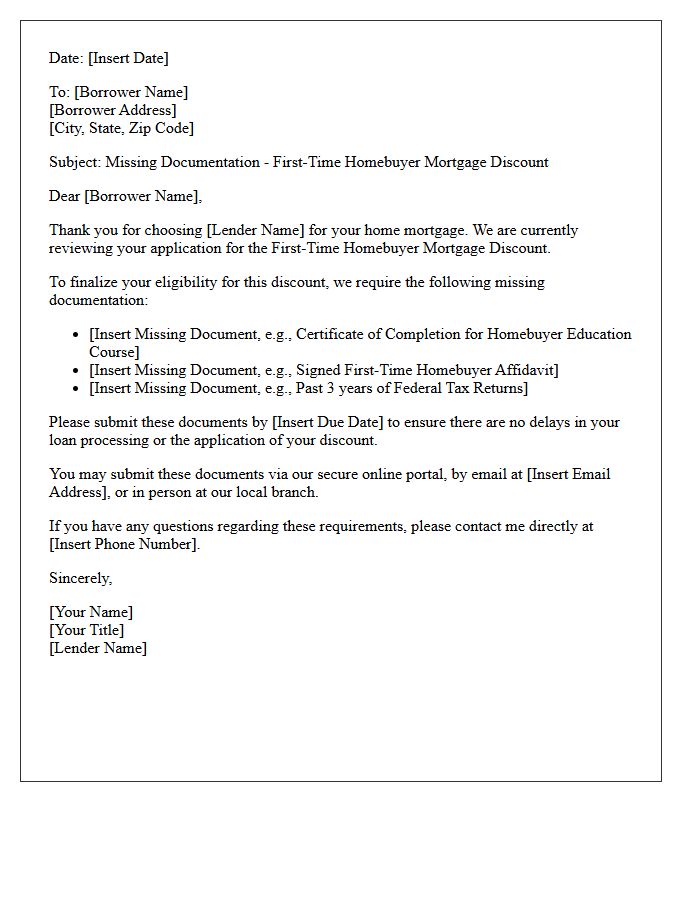

Missing Documentation Request Letter for First-Time Homebuyer Mortgage Discount

A missing documentation request letter is a formal notice sent by lenders to first-time homebuyers who have incomplete mortgage applications. To secure a mortgage discount or lower interest rate, you must promptly provide the requested financial records, such as tax returns or income statements. Failing to submit these documents within the specified deadline can delay your closing or lead to a loan denial. Always ensure your response is organized and includes your loan reference number to maintain eligibility for exclusive buyer incentives and favorable borrowing terms.

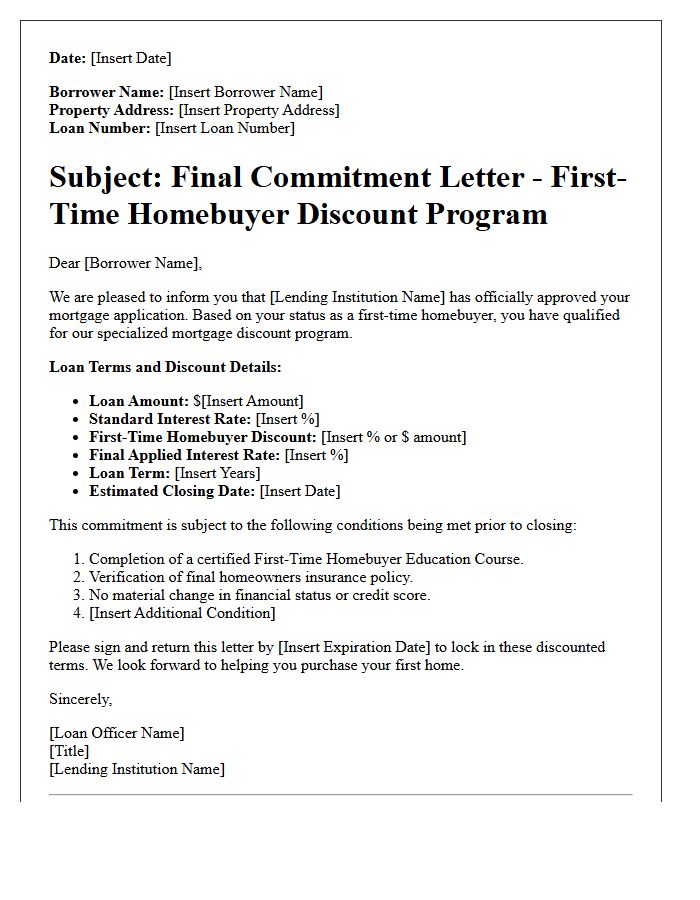

Final Commitment Letter for First-Time Homebuyer Mortgage Discount

A Final Commitment Letter is the formal approval from a lender confirming your mortgage is secured. For first-time buyers, this document is critical as it locks in your specific mortgage discount and interest rate. It outlines the final loan terms, monthly payments, and any remaining conditions to meet before closing. Receiving this letter signifies that your financial profile and the property appraisal have passed underwriting. Once signed, it serves as a legally binding agreement, ensuring you receive the financial incentives promised for your first home purchase.

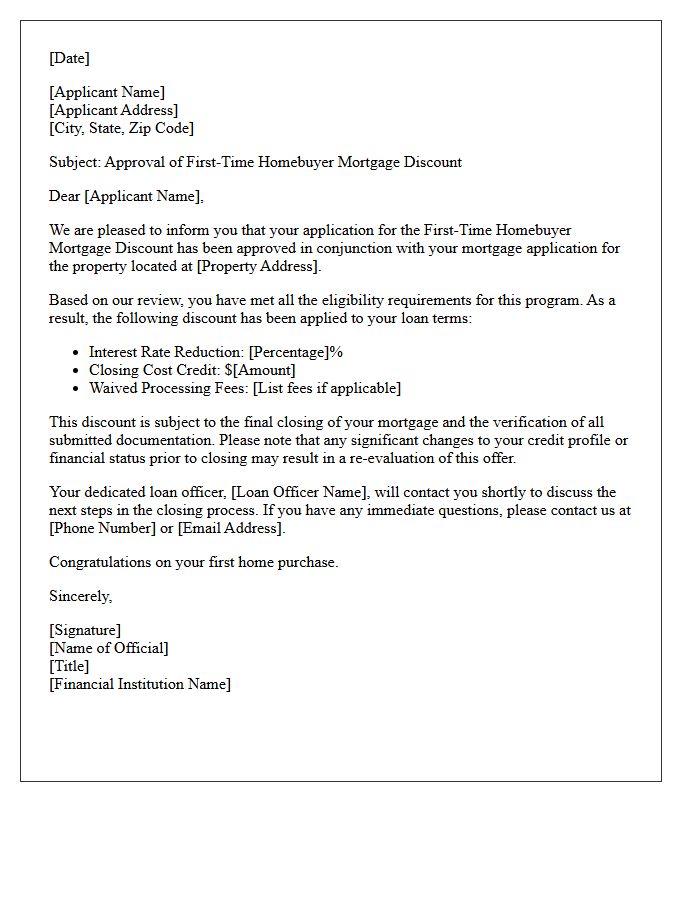

Approval Letter for First-Time Homebuyer Mortgage Discount

An Approval Letter serves as official confirmation that you qualify for a First-Time Homebuyer Mortgage Discount. This document verifies your eligibility for reduced interest rates, lower down payment requirements, or waived closing costs. Lenders issue this after evaluating your credit score and financial history to ensure you meet specific government or bank criteria. Having this letter in hand strengthens your purchasing power, proving to sellers that you are a serious, pre-qualified buyer capable of securing specialized financial incentives designed to make homeownership more affordable for beginners.

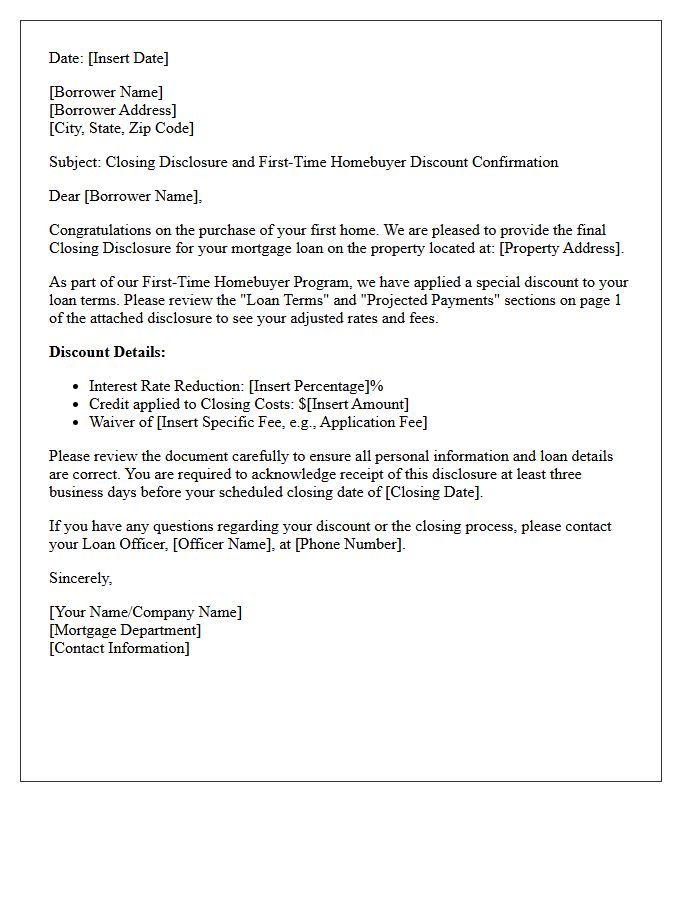

Closing Disclosure Letter for First-Time Homebuyer Mortgage Discount

A Closing Disclosure is a vital legal document issued three days before settlement, outlining your final loan terms and costs. For first-time buyers, it confirms eligibility for specific mortgage discounts, such as reduced interest rates or lender credits. It is essential to compare these figures against your initial Loan Estimate to ensure all promised financial incentives are accurately applied. Reviewing this letter carefully ensures you receive the full benefit of your first-time buyer status, preventing overpayment and ensuring a transparent, affordable transition into homeownership.

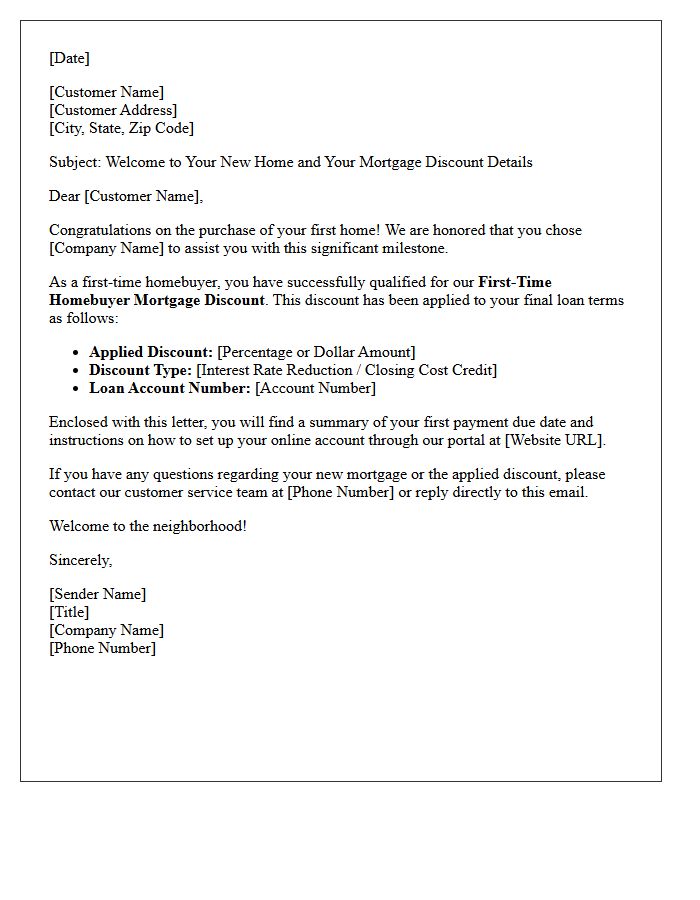

Post-Closing Welcome Letter for First-Time Homebuyer Mortgage Discount

The Post-Closing Welcome Letter is a vital document confirming your eligibility for a first-time homebuyer mortgage discount. This official notice outlines your finalized interest rate reduction, updated monthly payment schedule, and any applicable lender credits. It serves as formal verification that you have met all requirements for specialized affordability programs. Homeowners should retain this record to ensure their loan servicing reflects the promised savings accurately. Reviewing this letter promptly helps verify that your introductory financial benefits are correctly applied to your new mortgage account from the very first installment.

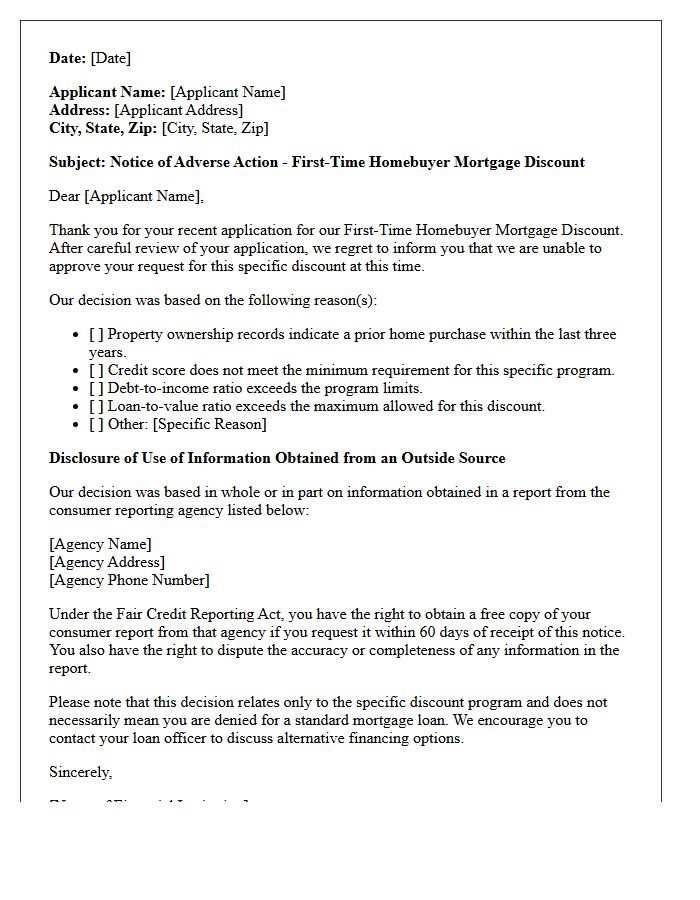

Adverse Action Letter for First-Time Homebuyer Mortgage Discount

When applying for a first-time homebuyer mortgage discount, an Adverse Action Letter is a formal notice explaining why your application was denied or why you were offered less favorable terms. It is crucial to review the specific reasons listed, such as credit score issues or debt-to-income ratios. Under the Equal Credit Opportunity Act, lenders must provide this document within 30 days. Use this information to correct errors in your credit report or improve your financial profile to qualify for better rates or specialized mortgage discounts in the future.

What is a First-Time Homebuyer Mortgage Discount Letter?

A First-Time Homebuyer Mortgage Discount Letter is an official document issued by a lender or housing authority confirming that a borrower qualifies for specific interest rate reductions, closing cost credits, or down payment assistance programs reserved for first-time buyers.

How do I qualify for a first-time homebuyer mortgage rate discount?

To qualify, you typically must not have owned a primary residence in the last three years, meet specific credit score requirements (usually 620 or higher), and fall within local household income limits. Some discounts also require the completion of a certified homebuyer education course.

What information should be included in a mortgage discount eligibility letter?

The letter should include the borrower's legal name, the specific loan program name (such as FHA, HomeReady, or a state-specific bond program), the discounted interest rate or credit amount, expiration date of the offer, and the lender's NMLS registration details.

Can a mortgage discount letter help lower my closing costs?

Yes, many mortgage discount letters specify "lender credits" or "grant awards" that are applied directly to your closing costs. These discounts can reduce the out-of-pocket cash needed at signing by several thousand dollars depending on the program.

Does a first-time homebuyer discount letter guarantee loan approval?

No, a discount letter confirms eligibility for a specific incentive or rate reduction but is not a final loan approval. Borrowers must still go through full underwriting, which includes verification of income, assets, employment, and a formal property appraisal.

Comments