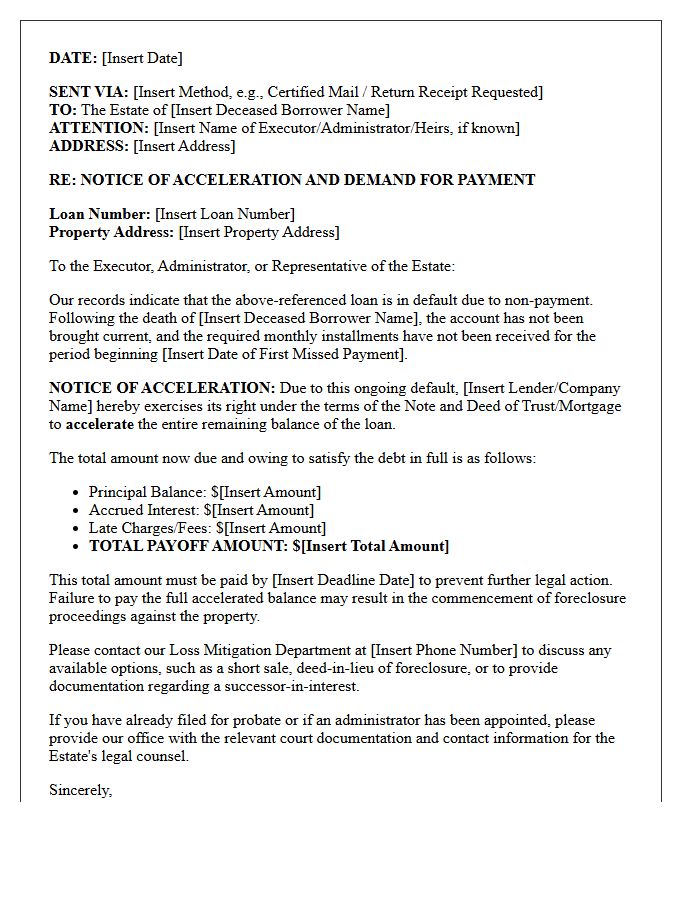

Managing debt after a loss is challenging. A Deceased Borrower Estate Acceleration Letter is a formal notice sent by lenders to demand full repayment from the decedent's assets. This legal step initiates the recovery process against the estate's remaining balance. Understanding your rights helps ensure proper handling of these sensitive financial claims. To assist you, below are some ready to use templates.

Image cover: Formal Estate Notification: Accelerated Debt Recovery Templates and Notice Samples

Letter Samples List

- Notice of Intent to Accelerate Deceased Borrower Estate Letter

- First Notice of Estate Mortgage Acceleration Letter

- Final Demand and Estate Loan Acceleration Letter

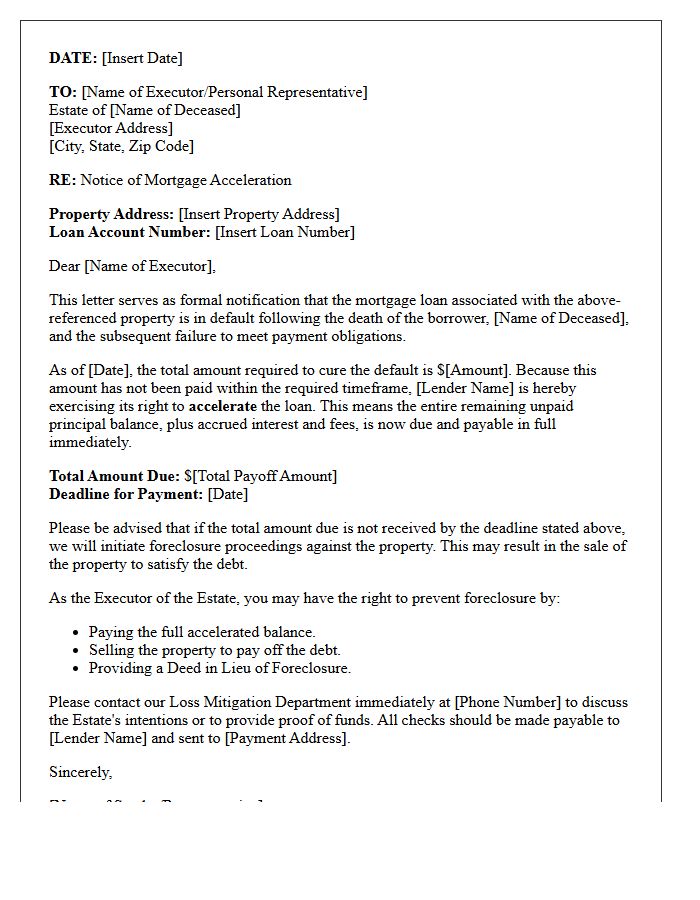

- Executor Notification of Mortgage Acceleration Letter

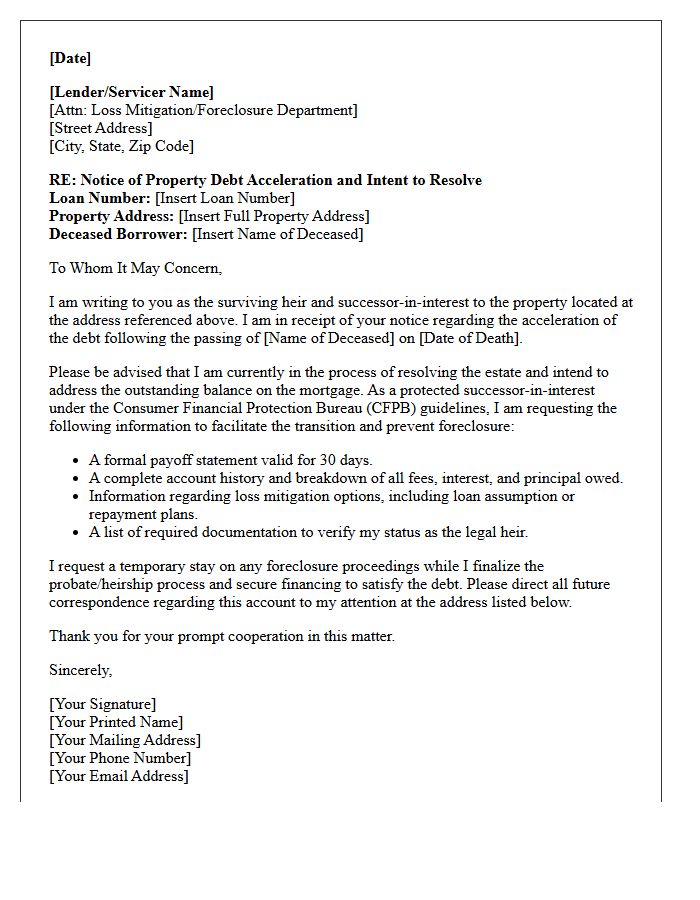

- Surviving Heir Property Debt Acceleration Letter

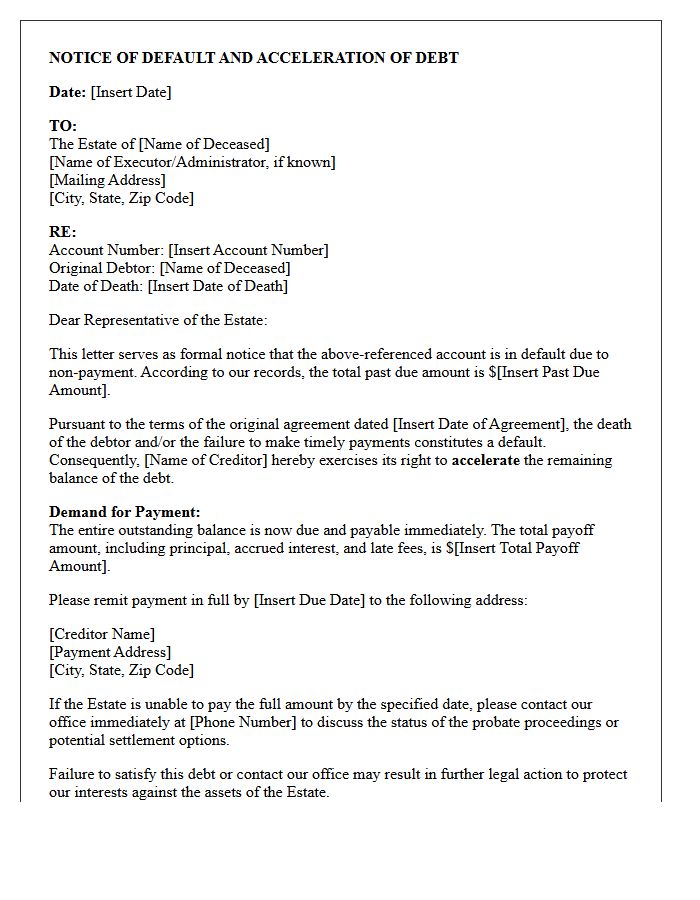

- Notice of Default and Estate Acceleration Letter

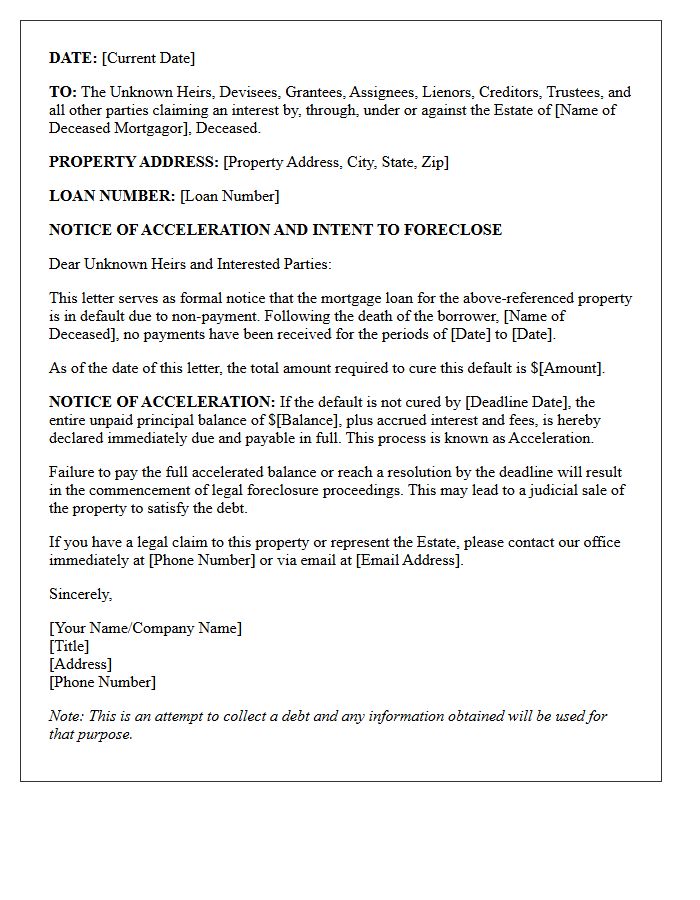

- Unknown Heirs Foreclosure Acceleration Letter

- Probate Claim and Mortgage Acceleration Letter

- Estate Administrator Loan Acceleration Demand Letter

- Successor in Interest Acceleration Warning Letter

- Post-Death Mortgage Balance Acceleration Letter

- Delinquent Deceased Borrower Estate Acceleration Letter

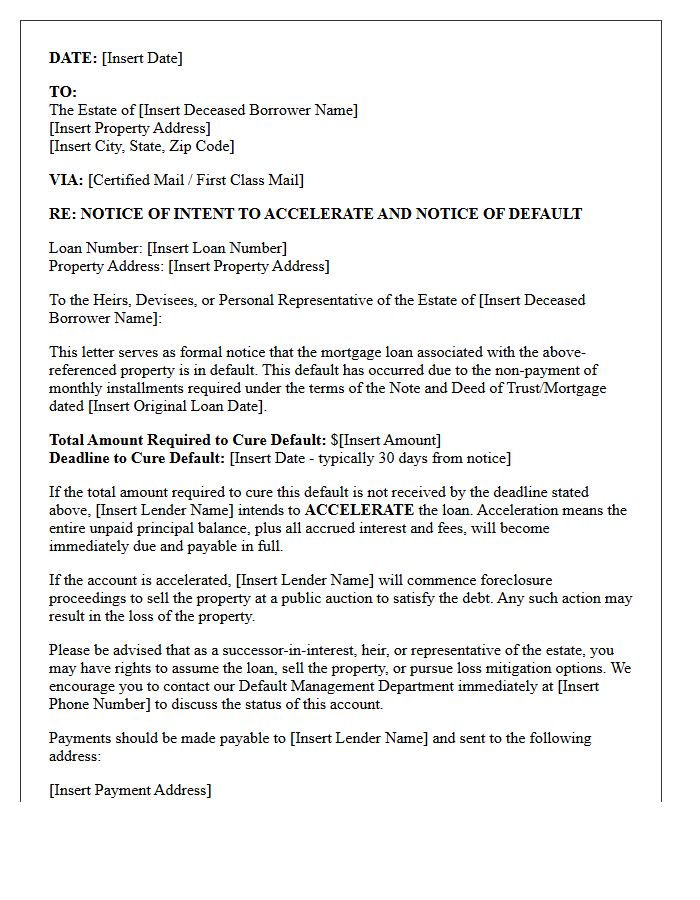

Notice of Intent to Accelerate Deceased Borrower Estate Letter

A Notice of Intent to Accelerate is a formal legal document sent to a deceased borrower's estate when mortgage payments lapse. This letter serves as a final warning that the lender plans to demand the full loan balance immediately unless the default is cured. It is a critical step before the foreclosure process begins. Beneficiaries or executors must act quickly to resolve the debt, pursue a loan assumption, or sell the property to prevent the loss of the home and protect any remaining equity within the estate.

First Notice of Estate Mortgage Acceleration Letter

A First Notice of Estate Mortgage Acceleration is a critical legal warning sent to heirs or executors when a deceased homeowner's loan payments lapse. This formal demand letter notifies the estate that the entire remaining loan balance must be paid immediately. Failure to resolve the default or negotiate a repayment plan typically triggers the foreclosure process. It is essential for representatives to contact the lender promptly to discuss loss mitigation options, such as a loan assumption or property sale, to protect the equity within the estate's real estate assets.

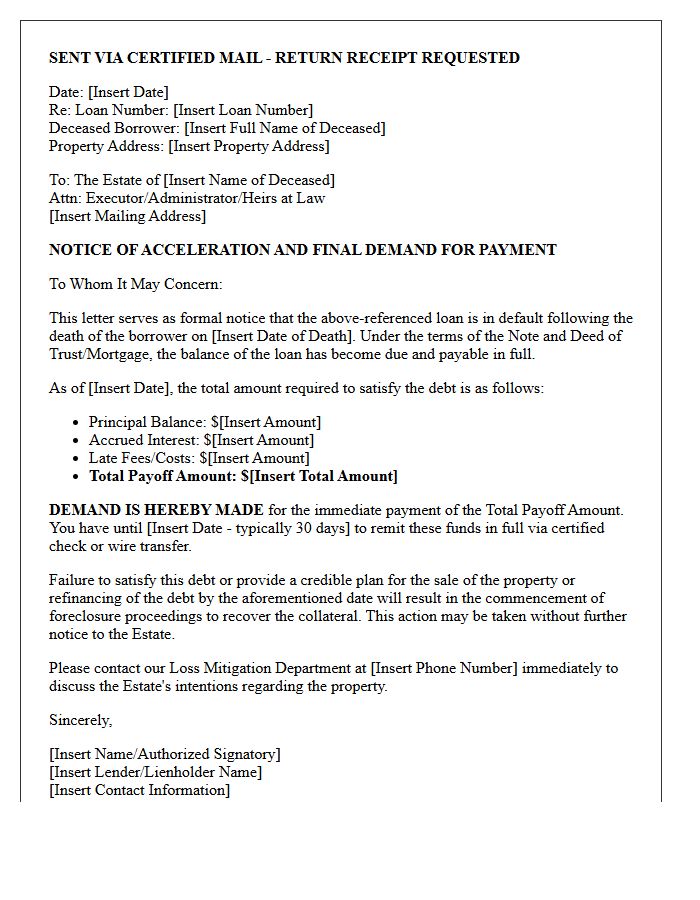

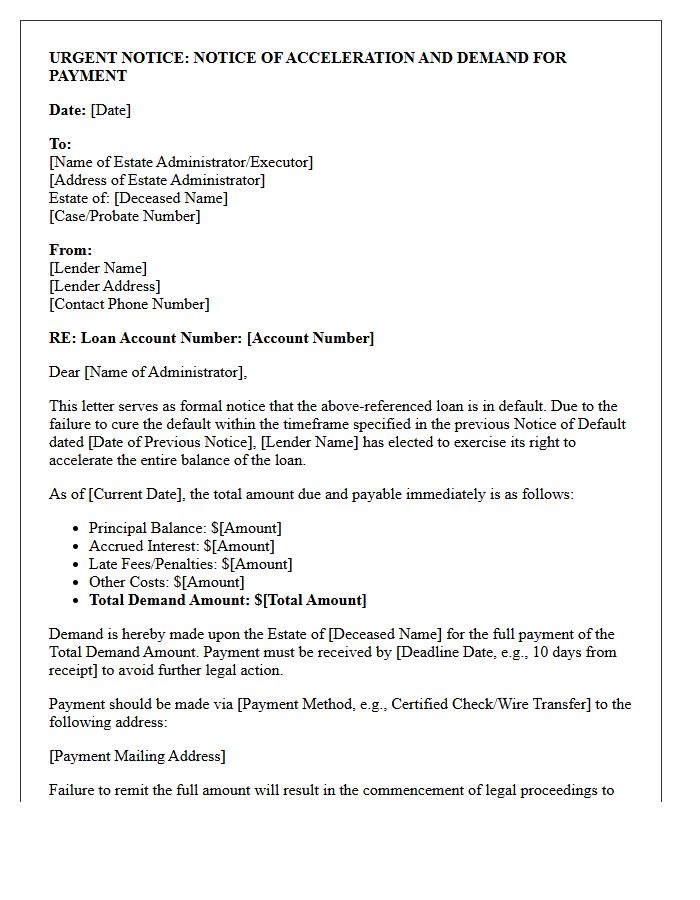

Final Demand and Estate Loan Acceleration Letter

A Final Demand and Estate Loan Acceleration Letter is a critical legal notice issued by lenders when a borrower passes away and payments cease. It officially declares the entire debt balance due immediately, terminating the original installment plan. For heirs and executors, the most important action is to communicate with the servicer to explore loss mitigation or probate settlements. Failure to respond to this formal warning typically triggers the foreclosure process, potentially leading to the loss of the property asset from the deceased person's estate.

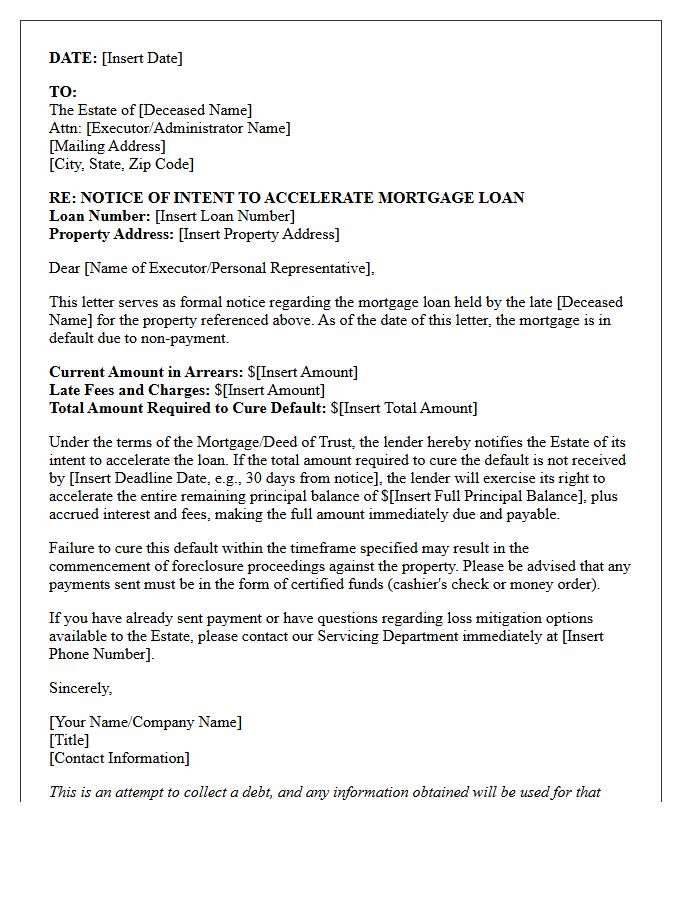

Executor Notification of Mortgage Acceleration Letter

An Executor Notification of Mortgage Acceleration Letter is a formal legal notice sent to an estate representative when mortgage payments remain unpaid after a homeowner's death. This critical document warns that the full loan balance is now due immediately, rather than just the missed installments. Receiving this letter indicates that the lender intends to initiate foreclosure proceedings. It is vital for executors to communicate with the servicer promptly to discuss loss mitigation options, loan assumption, or property sale to protect the estate's remaining equity and assets.

Surviving Heir Property Debt Acceleration Letter

A Surviving Heir Property Debt Acceleration Letter is a formal notice from a lender demanding immediate payment of the full mortgage balance. This usually occurs after a homeowner dies and the loan defaults or lacks a clear successor. To protect your home, you must provide proof of heirship quickly. Federal law often allows heirs to assume the mortgage or enter a loan modification without triggering the "due-on-sale" clause. Seeking legal counsel is vital to stop foreclosure, verify legal inheritance, and negotiate a manageable repayment plan with the servicer.

Notice of Default and Estate Acceleration Letter

A Notice of Default is a formal legal warning issued by a lender when a borrower breaches a mortgage contract, typically through non-payment. This document initiates the foreclosure process and provides a specific window to cure the delinquency. If the debt remains unpaid, the lender may issue an Estate Acceleration Letter, demanding immediate payment of the entire loan balance rather than just the missed installments. Understanding these documents is critical to protecting your property rights and exploring loss mitigation options before a public auction occurs.

Unknown Heirs Foreclosure Acceleration Letter

An Unknown Heirs Foreclosure Acceleration Letter is a formal legal notice issued when a property owner dies without a clear will or identified successors. This document notifies potential claimants that the lender is accelerating the loan balance, making the full debt due immediately to initiate foreclosure. It serves as a final warning to any unnamed beneficiaries to assert their legal interest or settle the debt. Failing to respond promptly typically results in the permanent loss of property rights through a judicial sale or auction process.

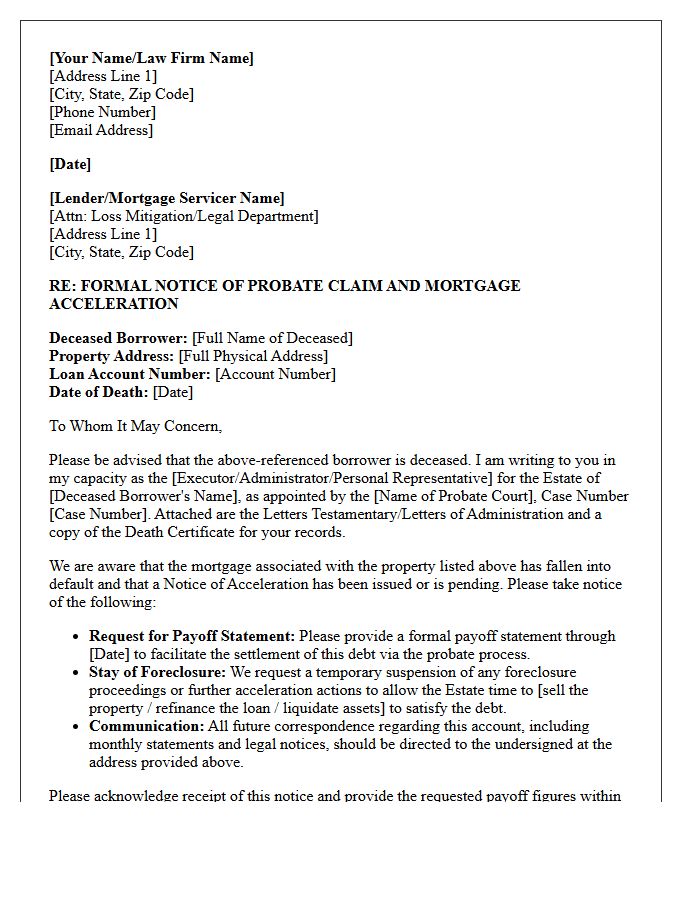

Probate Claim and Mortgage Acceleration Letter

A Probate Claim is a formal demand against a deceased person's estate to settle outstanding debts. If a homeowner dies, the lender may issue a Mortgage Acceleration Letter, demanding immediate payment of the entire loan balance. This often occurs if payments are missed during estate administration. Understanding these legal actions is crucial for heirs to prevent foreclosure and protect their inheritance. Timely communication with the lender and filing necessary court documents can help manage the debt and ensure the property title transfers smoothly without losing equity to a forced sale.

Estate Administrator Loan Acceleration Demand Letter

An Estate Administrator Loan Acceleration Demand Letter is a formal legal notice sent to a personal representative when a decedent's debt remains unpaid. This document triggers a mandatory repayment of the full loan balance immediately, rather than following the original installment schedule. It typically follows a breach of contract or default. Administrators must act quickly to resolve the claim to prevent foreclosure or legal action against the estate's assets. Timely communication with lenders is essential to protect the distributable inheritance and fulfill fiduciary duties effectively.

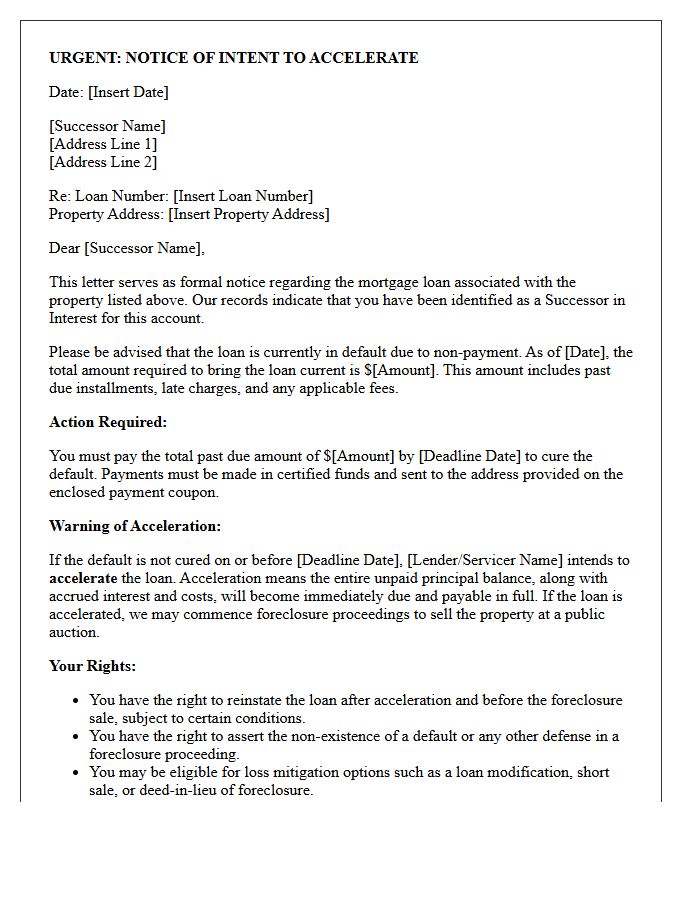

Successor in Interest Acceleration Warning Letter

A Successor in Interest Acceleration Warning Letter is a formal notice sent by mortgage servicers to individuals who have inherited property rights. It alerts the recipient that the loan is in default and the lender intends to accelerate the debt, making the full balance due immediately. To prevent foreclosure, the successor must quickly confirm their identity and legal status. This legal notification provides a final opportunity to cure the delinquency through payment or loan assumption before the property is referred to a foreclosure attorney for legal action.

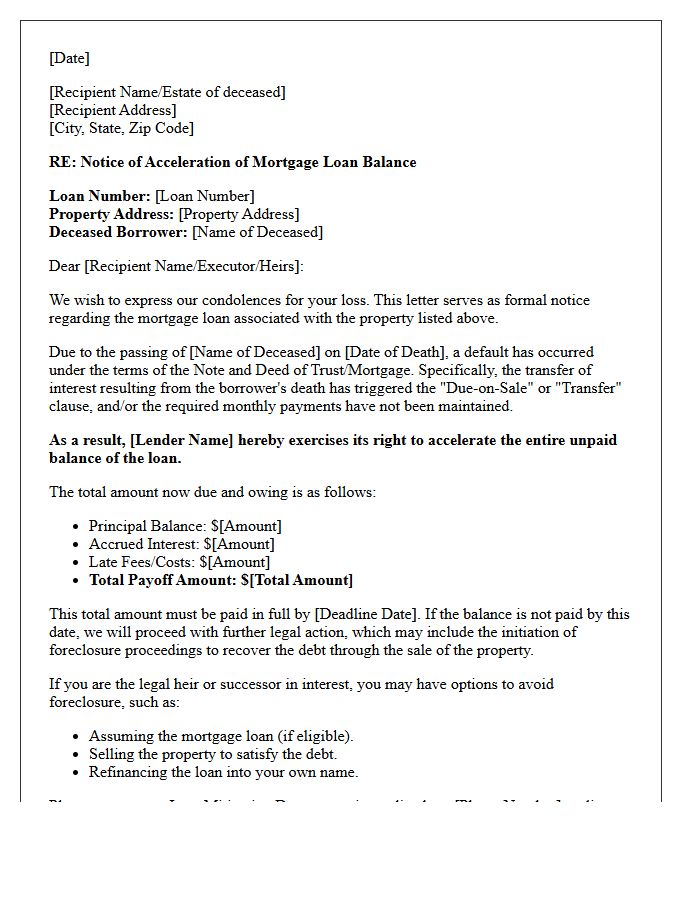

Post-Death Mortgage Balance Acceleration Letter

A Post-Death Mortgage Balance Acceleration Letter is a formal notice sent by lenders when a homeowner passes away. This document signifies the acceleration of the debt, demanding full repayment of the remaining loan balance. It typically triggers due to the Due-on-Sale clause, which treats the transfer of property after death as a technical sale. Heirs must act quickly to explore options like assuming the mortgage, refinancing, or selling the home to prevent foreclosure. Understanding your legal rights under federal protections is essential to maintaining homeownership during probate.

Delinquent Deceased Borrower Estate Acceleration Letter

A Delinquent Deceased Borrower Estate Acceleration Letter is a formal legal notice issued by lenders when a homeowner passes away with an outstanding mortgage. This document notifies the executor or heirs that the loan is in default. The most critical action is debt acceleration, which demands the entire remaining balance be paid immediately. This letter serves as a final warning before the lender initiates foreclosure proceedings against the property. It is essential for representatives to contact the servicer promptly to discuss repayment, sale, or loss mitigation options to protect estate assets.

What is a Deceased Borrower Estate Acceleration Letter?

A Deceased Borrower Estate Acceleration Letter is a formal legal notice sent by a mortgage lender notifying the heirs or the estate representative that the full remaining loan balance is now due. This typically occurs when a borrower passes away and the loan is not being paid or the lender is exercising a "due-on-sale" or "transfer" clause.

Why did I receive an acceleration notice after the homeowner passed away?

Lenders issue acceleration notices to protect their collateral when the primary borrower dies and the mortgage terms are breached. Common triggers include the cessation of monthly payments, failure to transfer the title to a qualified heir, or the estate's inability to maintain property taxes and insurance.

Can an heir stop the acceleration of a mortgage after death?

Yes, heirs can often stop acceleration by invoking the Garn-St. Germain Depository Institutions Act, which prevents lenders from enforcing due-on-sale clauses when a property is transferred to a relative. To stop the process, the heir must usually provide a death certificate, proof of heirship, and ensure monthly payments are brought current.

How long does the estate have to respond to an acceleration letter?

The timeframe is typically 30 days from the date of the letter, though this varies by state law and specific loan contracts. Failure to respond or pay the accelerated balance within this window usually results in the lender initiating formal foreclosure proceedings against the property.

What are the options for settling a mortgage after receiving an acceleration letter?

The estate or heirs generally have four options: pay the full loan balance through estate assets, refinance the mortgage into a new loan under the heir's name, sell the property to satisfy the debt, or apply for a loan assumption or modification if they intend to keep the home.

Comments