A VA Loan Commitment Letter is a crucial document issued by a lender, confirming that a veteran is officially approved for financing. It outlines specific loan terms, interest rates, and conditions required for closing. Securing this letter strengthens your position when making offers on a home. To help you finalize your application, below are some ready to use template.

Image cover: VA Loan Commitment Letter: Professional Samples and Templates

Letter Samples List

- Veterans Affairs Conditional Loan Commitment Letter

- Veterans Affairs Final Loan Commitment Letter

- Veterans Affairs Loan Commitment Extension Letter

- Veterans Affairs Revised Loan Commitment Letter

- Veterans Affairs Refinance Loan Commitment Letter

- Veterans Affairs Purchase Loan Commitment Letter

- Veterans Affairs Jumbo Loan Commitment Letter

- Veterans Affairs Construction Loan Commitment Letter

- Veterans Affairs Joint Loan Commitment Letter

- Veterans Affairs Pre-Approval Loan Commitment Letter

- Veterans Affairs Loan Commitment Reinstatement Letter

- Veterans Affairs Expired Loan Commitment Letter

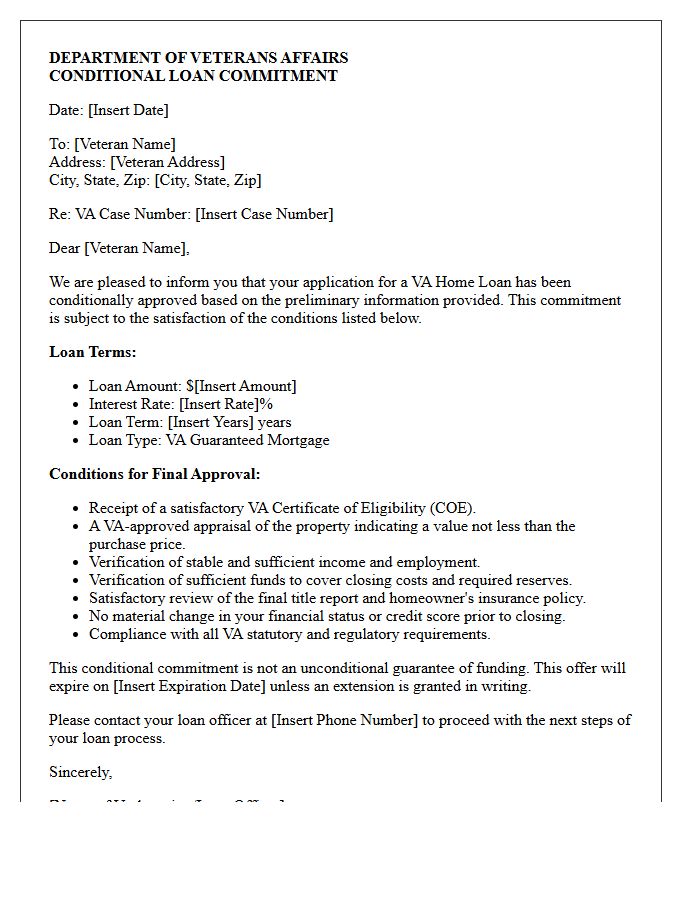

Veterans Affairs Conditional Loan Commitment Letter

A Veterans Affairs Conditional Loan Commitment Letter is a formal document issued by the VA indicating that a property meets specific eligibility requirements for a VA-backed mortgage. It outlines the maximum loan amount and necessary conditions, such as property appraisal and safety standards, that must be satisfied before final approval. This letter serves as a preliminary guarantee to lenders, ensuring the home provides safe, sanitary, and structurally sound housing for veterans. Understanding these conditions is vital for a smooth closing process and securing favorable financing terms.

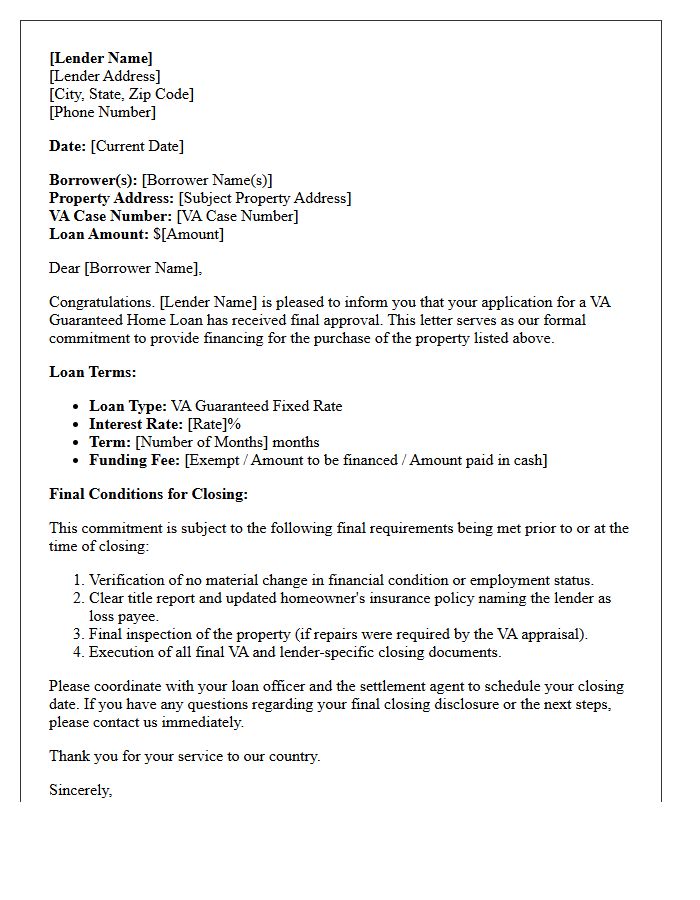

Veterans Affairs Final Loan Commitment Letter

A Veterans Affairs Final Loan Commitment Letter is the official approval issued by a lender once all underwriting conditions are met. This document confirms that the VA has verified the borrower's eligibility and the property's value, signifying the final stage before closing. It guarantees that funding is secured, provided no financial changes occur before signing. Receiving this letter means your home loan is cleared to close, transitioning the status from conditional pre-approval to a binding agreement for veteran financing.

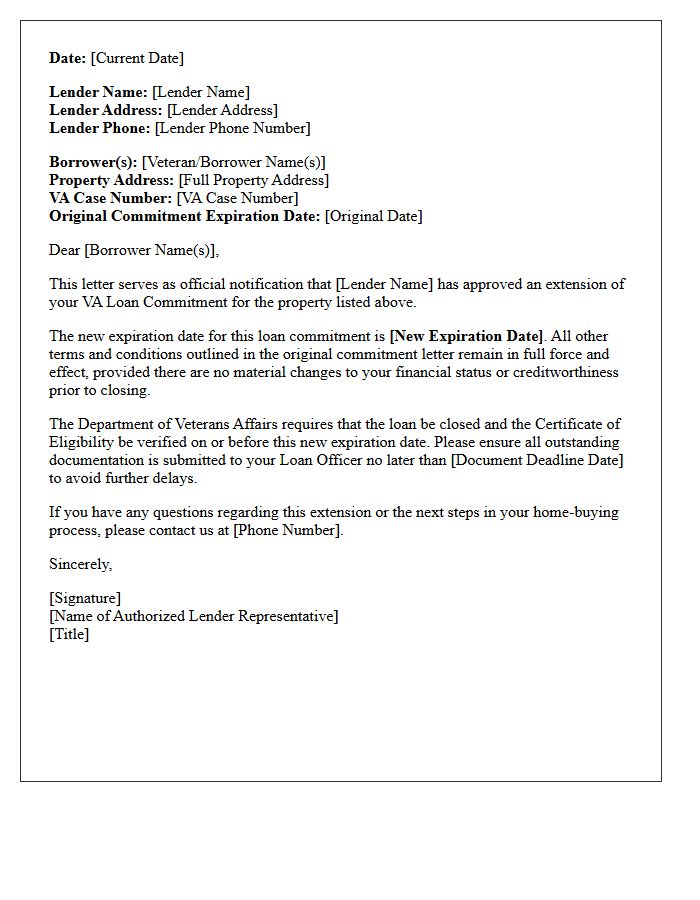

Veterans Affairs Loan Commitment Extension Letter

A Veterans Affairs Loan Commitment Extension Letter is a formal document that prolongs the validity of an initial loan approval. This extension is essential when construction delays or processing lags prevent a mortgage from closing before the original expiration date. To maintain eligibility, borrowers must ensure their credit profile and financial status remain unchanged during this period. Obtaining this letter prevents the need for a full re-application, ensuring the VA loan benefit remains active while finalizing the property purchase or construction project details.

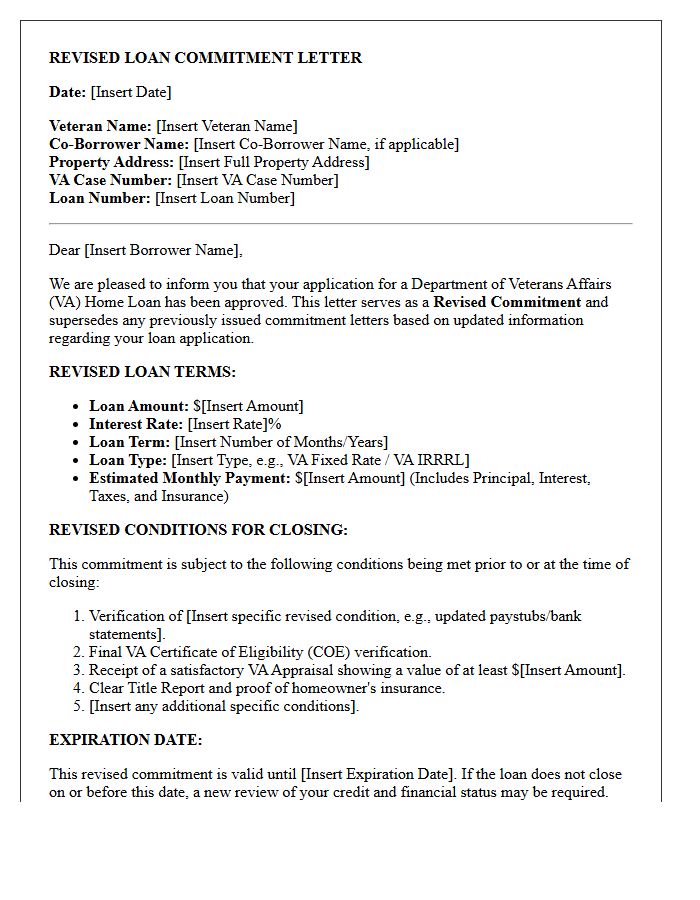

Veterans Affairs Revised Loan Commitment Letter

The VA Revised Loan Commitment Letter is a crucial document issued when significant changes occur after the initial approval. It confirms that the Department of Veterans Affairs has updated terms such as the loan amount, interest rate, or property value. Borrowers must review this letter carefully, as it outlines new conditions required for final closing. Ensuring all details match the current sales contract is essential to maintaining your guaranteed benefits and securing a successful home purchase without processing delays.

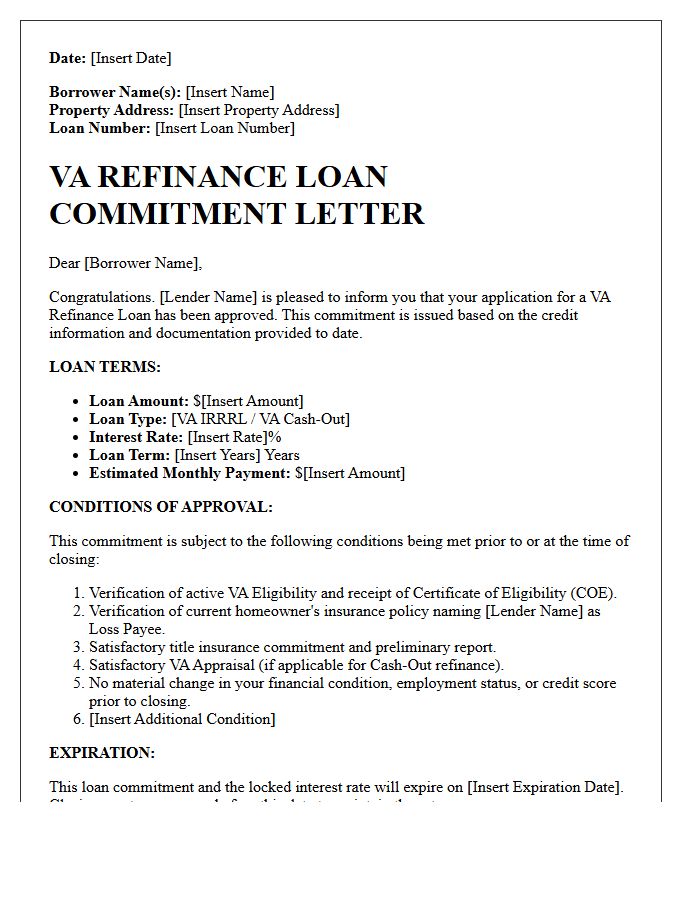

Veterans Affairs Refinance Loan Commitment Letter

A Veterans Affairs Refinance Loan Commitment Letter is a formal document issued by a lender confirming conditional approval for a VA interest rate reduction or cash-out loan. This legal pledge outlines the specific loan amount, interest rate, and required closing conditions the borrower must satisfy. Receiving this letter signifies that the underwriter has verified your eligibility and creditworthiness, moving you closer to final funding. It serves as essential proof to all parties that the financing is guaranteed, provided all listed contingencies are met before the expiration date.

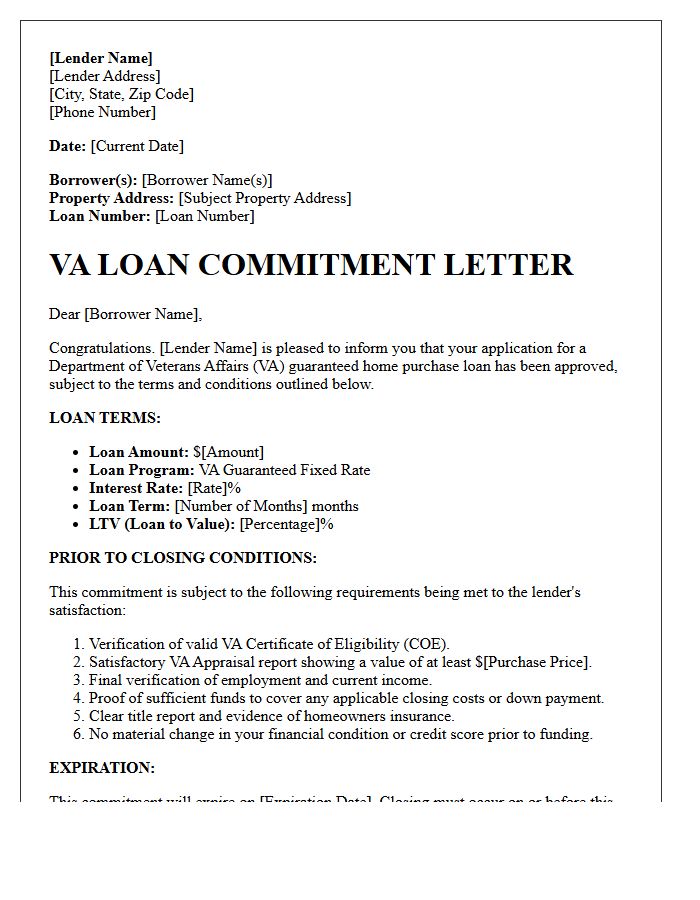

Veterans Affairs Purchase Loan Commitment Letter

A VA Loan Commitment Letter is a formal document issued by a lender confirming that a veteran is approved for financing. It signifies that the underwriting process is complete, contingent upon final conditions like a clear title or satisfactory appraisal. Unlike a pre-approval, this letter represents a binding agreement to fund the mortgage, providing financial credibility to sellers. It is an essential milestone in the home-buying journey, ensuring the borrower meets specific eligibility requirements for VA-backed benefits and competitive interest rates.

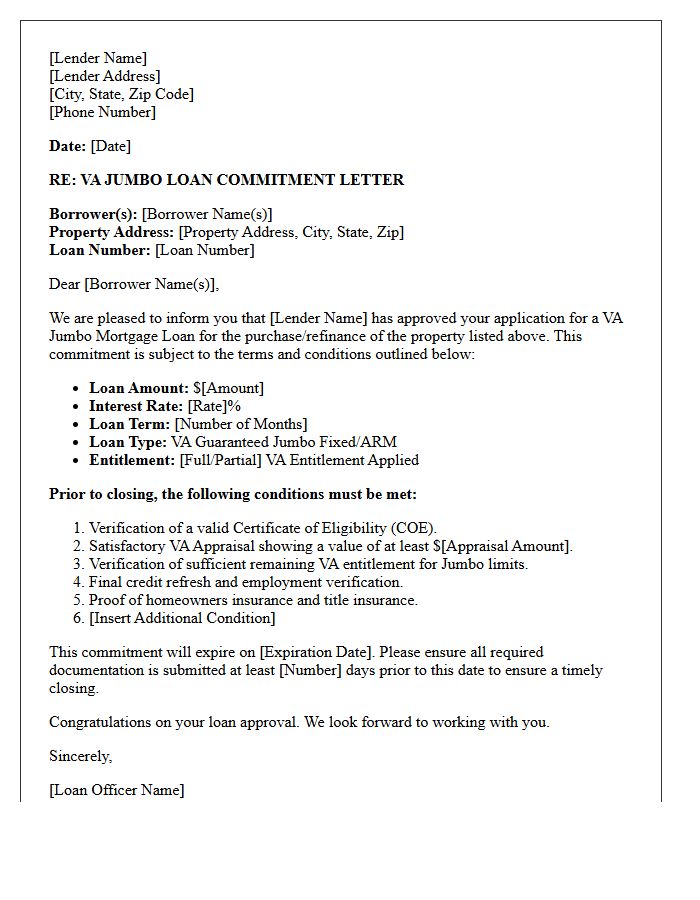

Veterans Affairs Jumbo Loan Commitment Letter

A Veterans Affairs Jumbo Loan Commitment Letter is a formal document confirming a lender's promise to finance a mortgage exceeding standard conforming limits. This legal approval signifies that a veteran has met rigorous credit, income, and service requirements. It is a critical milestone for high-value real estate transactions, providing sellers with assurance that the buyer's funding is secured. Unlike a pre-approval, this letter represents a verified financial guarantee, contingent only upon final property inspections and a clear title, ensuring the veteran can purchase a luxury home with earned benefits.

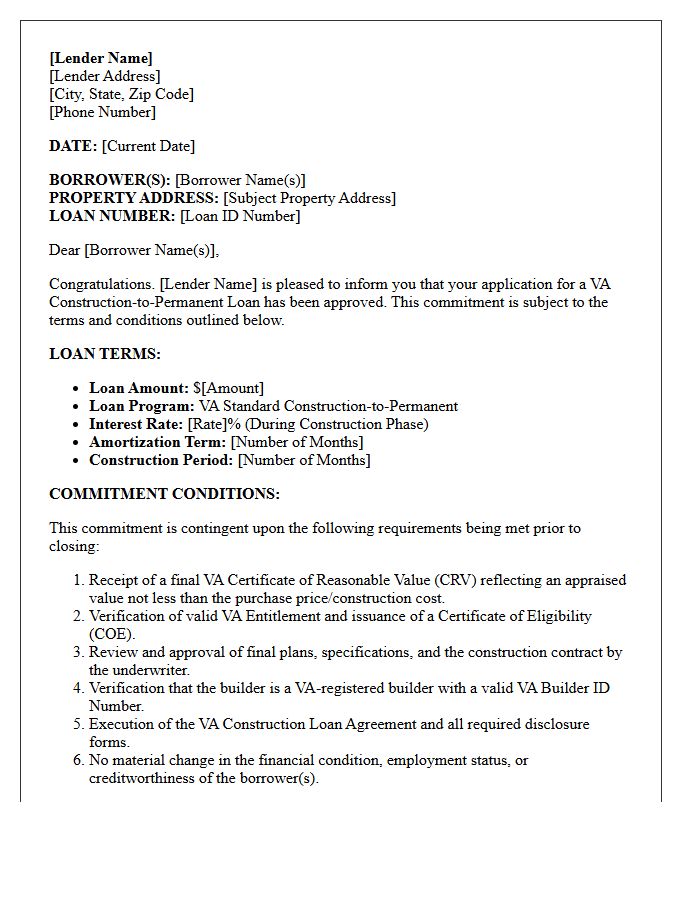

Veterans Affairs Construction Loan Commitment Letter

A Veterans Affairs Construction Loan Commitment Letter is a formal document from a lender guaranteeing financing for building a new home. This conditional approval outlines the specific terms, interest rates, and requirements a veteran must meet before construction begins. It serves as proof to builders that the borrower has secured the necessary VA entitlement and funding. For a successful closing, the project must comply with VA minimum property requirements and structural inspections, ensuring the veteran receives a safe, high-quality residence through their earned military benefits.

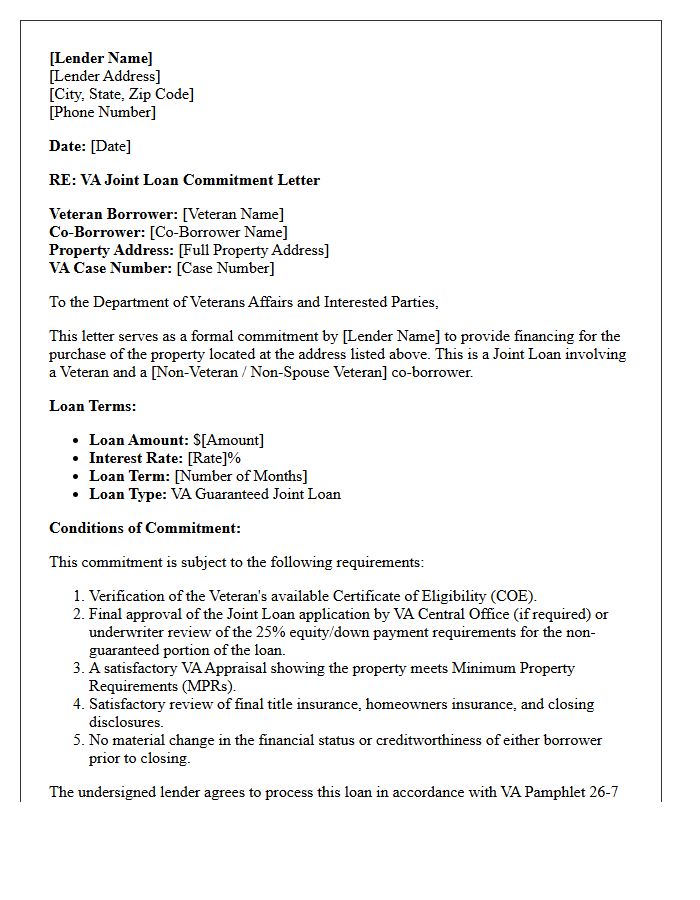

Veterans Affairs Joint Loan Commitment Letter

A Veterans Affairs Joint Loan Commitment Letter is a critical document issued when two or more individuals, often a veteran and a non-veteran, apply for a VA-backed mortgage together. This letter outlines the underwriting requirements and specific conditions mandated by the Department of Veterans Affairs to guarantee the loan. It ensures that the joint liability is clearly defined, protecting the government's interest while enabling eligible borrowers to secure favorable financing terms. Obtaining this commitment is a vital step in finalizing the home-buying process for multi-party veteran applications.

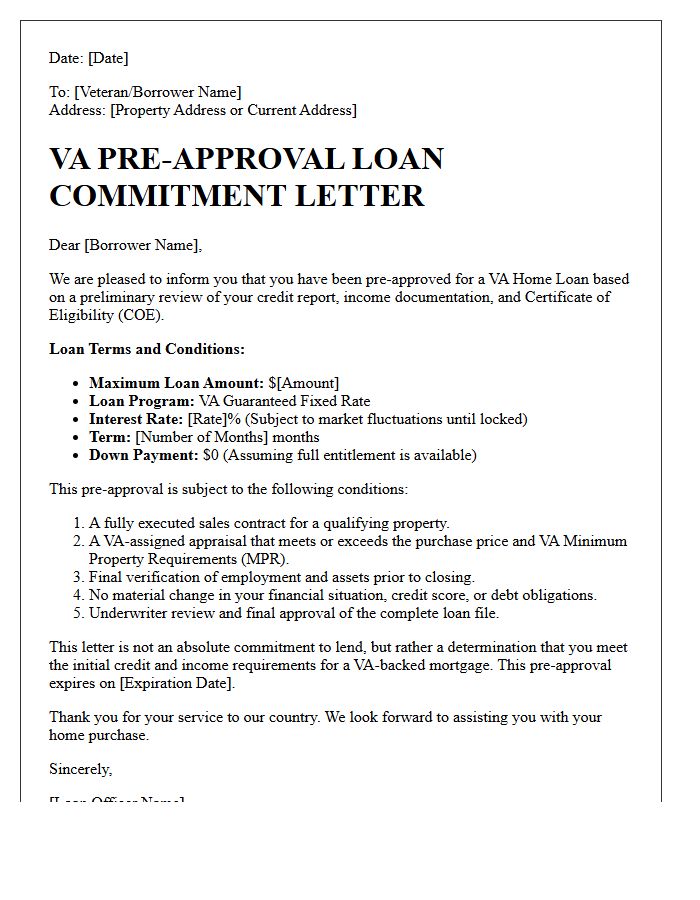

Veterans Affairs Pre-Approval Loan Commitment Letter

A Veterans Affairs Pre-Approval Loan Commitment Letter is a critical document proving a VA loan eligibility status to sellers. Unlike a basic pre-qualification, this formal assessment involves a comprehensive credit review and income verification by a lender. It demonstrates financial backing and intent to purchase, giving veterans a competitive edge in real estate negotiations. This letter confirms that you meet specific military service requirements and have the necessary borrowing power to secure a mortgage, ensuring a smoother closing process for your future home.

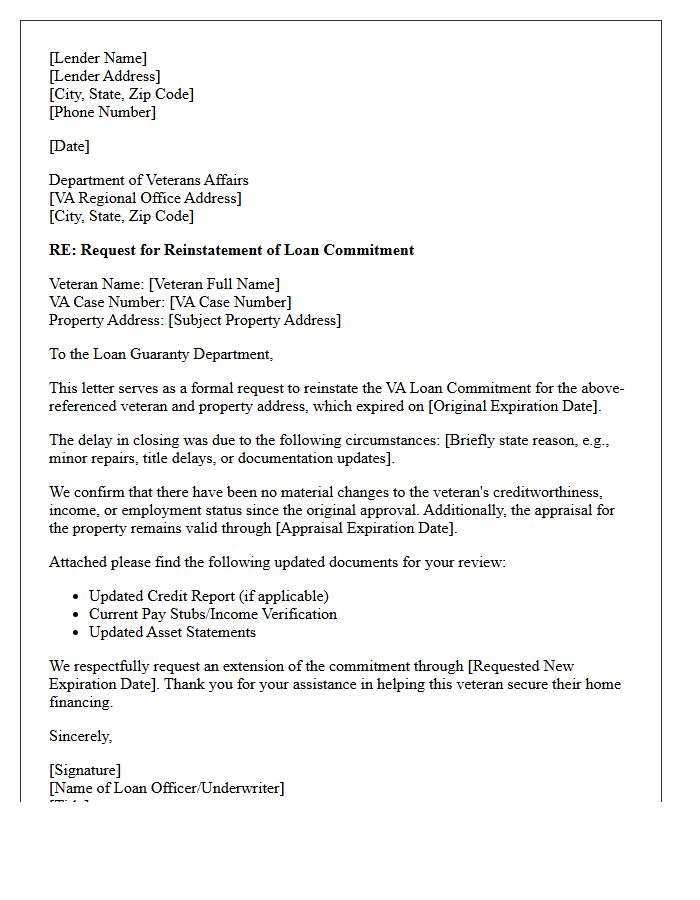

Veterans Affairs Loan Commitment Reinstatement Letter

A Veterans Affairs Loan Commitment Reinstatement Letter is a formal document issued by the VA to reactivate a previously expired or canceled financing guarantee. This reinstatement is essential when a loan closing is delayed beyond the original certificate's expiration date. It confirms that the government's guaranty remains valid, allowing the lender to proceed with funding. Borrowers must ensure all eligibility requirements and credit conditions are still met to receive this approval, ensuring the veteran maintains access to favorable mortgage terms and competitive interest rates.

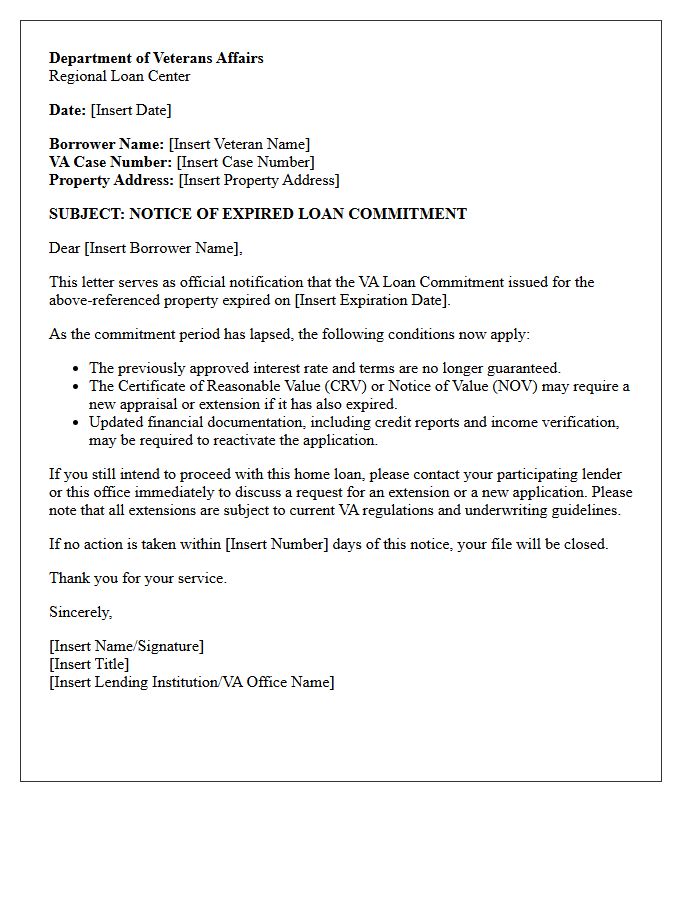

Veterans Affairs Expired Loan Commitment Letter

A Veterans Affairs (VA) loan commitment letter is a lender's formal promise to provide financing under specific terms. If you possess an expired loan commitment letter, the original interest rate and approval conditions are no longer guaranteed. To move forward, borrowers must undergo a re-verification of their credit, income, and assets. Because market rates fluctuate, an expiration often necessitates a new Certificate of Eligibility (COE) check or a full underwriting update. Staying in constant communication with your lender is essential to prevent costly delays in your home-buying process.

What is a VA Loan Commitment Letter?

A VA Loan Commitment Letter is a formal document issued by a mortgage lender stating that a veteran borrower has been approved for a home loan, pending specific conditions. Unlike a pre-approval, this letter signifies that the lender's underwriter has reviewed the veteran's financial profile and the property meets Department of Veterans Affairs requirements.

What is the difference between a VA pre-approval and a VA commitment letter?

A VA pre-approval is an initial estimate of borrowing power based on unverified data, whereas a VA Loan Commitment Letter is a binding agreement from the lender. The commitment letter is issued only after a full underwriting review of the borrower's income, credit, and the VA appraisal report, making it a much stronger signal to home sellers.

What are the common conditions found in a VA Loan Commitment Letter?

Common conditions include the "VA Amendatory Clause" signature, a clear termite inspection report (in required states), proof of homeowner's insurance, and a final verification of employment. The letter may also be contingent on the property's "Notice of Value" (NOV) matching or exceeding the agreed-upon purchase price.

How long does it take to receive a VA Loan Commitment Letter?

Typically, a VA Loan Commitment Letter is issued 20 to 30 days into the mortgage process. The timeline depends on how quickly the VA appraisal is completed and how fast the borrower provides necessary documentation to the underwriter for final approval.

Does a VA Loan Commitment Letter guarantee that the loan will close?

While a commitment letter is a very strong indicator of closing, it is not a final guarantee. The loan can still be denied if the borrower's financial situation changes significantly (such as taking on new debt), if the property title has unresolved issues, or if the borrower fails to meet the specific conditions outlined in the letter before the expiration date.

Comments