A Notice of Default on Forbearance Agreement is a formal legal notification issued when a borrower fails to meet the specific repayment terms established in a prior relief arrangement. This document officially terminates the temporary protection against foreclosure or collection actions, demanding immediate corrective measures. To help you navigate this process, below are some ready to use templates.

Image cover: Formal Notice of Default: Forbearance Agreement Non-Compliance Templates and Samples

Letter Samples List

- Notice of Default on Missed Forbearance Payment Letter

- Forbearance Agreement Cancellation Letter Due to Nonpayment

- Notice of Default and Reinstatement of Foreclosure Letter

- Failure to Resume Standard Mortgage Payments Default Letter

- Escrow Shortage Default During Forbearance Letter

- Failure to Provide Required Financial Documentation Default Letter

- Notice of Default on Forbearance Terms and Loan Acceleration Letter

- Property Abandonment Default During Forbearance Letter

- Unauthorized Property Transfer Forbearance Default Letter

- Final Demand Letter for Breached Forbearance Agreement

- Notice of Default on Balloon Payment Following Forbearance Letter

- Post-Forbearance Modification Denial and Default Letter

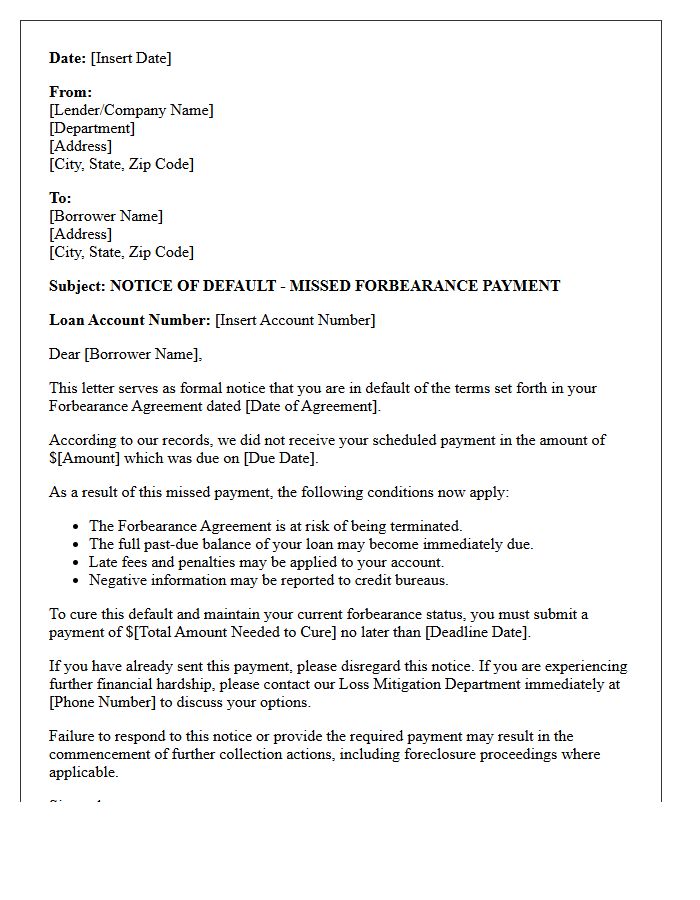

Notice of Default on Missed Forbearance Payment Letter

A Notice of Default on a missed forbearance payment is a critical legal warning that your mortgage foreclosure process may resume. This letter signifies that you failed to meet the agreed-upon repayment terms following a temporary pause. It is essential to contact your loan servicer immediately to discuss loss mitigation options or a loan modification. Ignoring this notice can lead to the acceleration of your debt, meaning the entire balance becomes due. Acting quickly is the best way to protect your home equity and prevent a formal trustee sale.

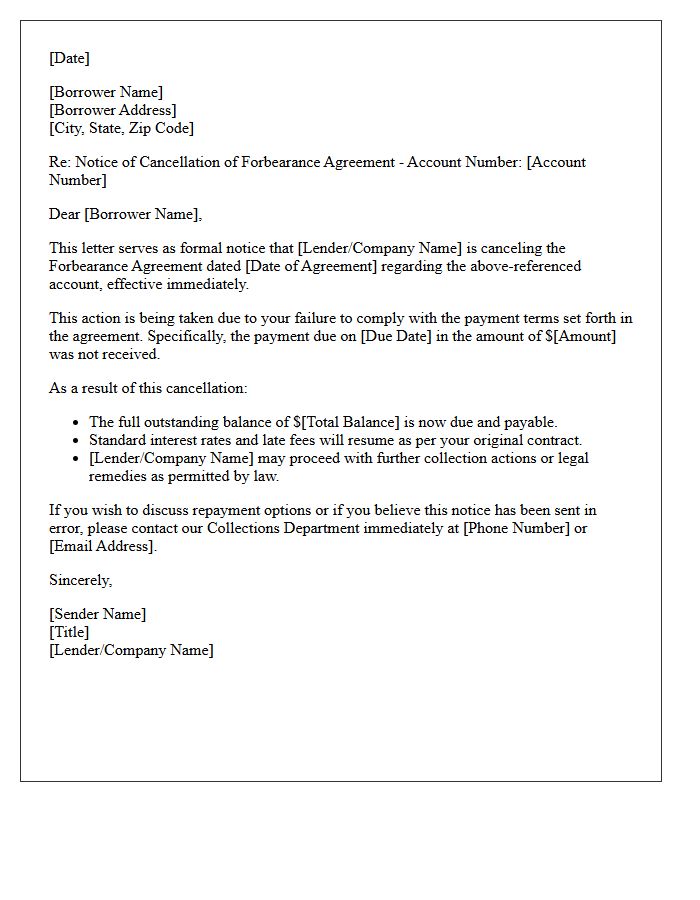

Forbearance Agreement Cancellation Letter Due to Nonpayment

A Forbearance Agreement Cancellation Letter Due to Nonpayment is a formal notice sent by a lender to a borrower when contractual installments are missed. This document officially terminates the temporary relief period, meaning the original loan terms and full payment obligations are reinstated immediately. It serves as a critical legal step before a lender initiates foreclosure or debt collection actions. To protect your rights, ensure the letter specifies the exact default date, the total outstanding balance, and any remaining reinstatement options available to avoid further legal consequences.

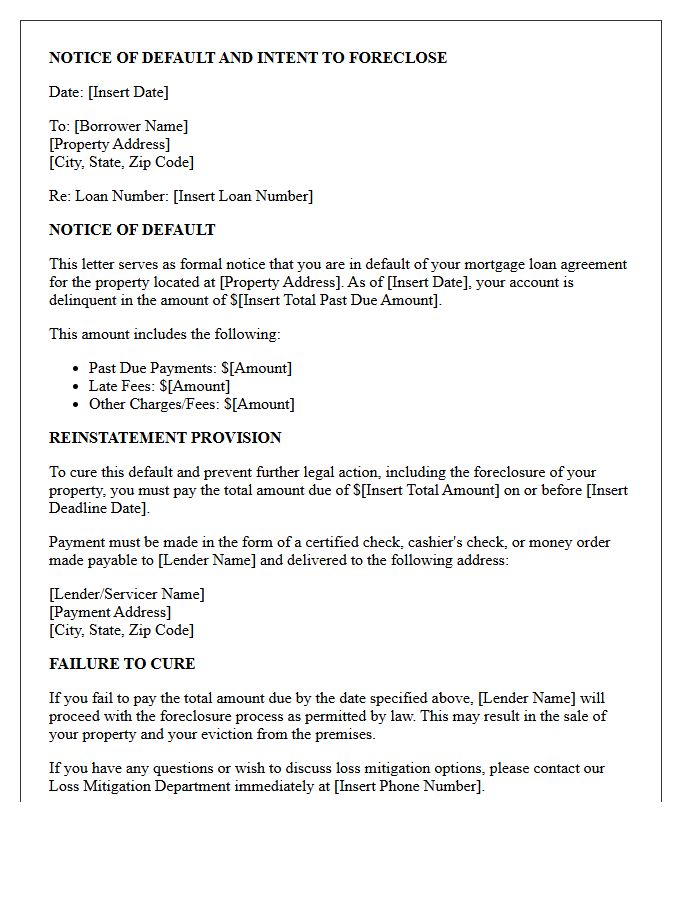

Notice of Default and Reinstatement of Foreclosure Letter

A Notice of Default is a formal legal document signaling the start of the foreclosure process because a borrower has failed to make payments. This letter serves as a final warning that the lender intends to seize the property unless the debt is resolved. To stop the proceedings, homeowners must exercise their right to reinstatement, which requires paying the total past-due balance, including late fees and legal costs, by a specific deadline. Acting quickly during this grace period is essential to avoid permanent loss of the home and severe credit damage.

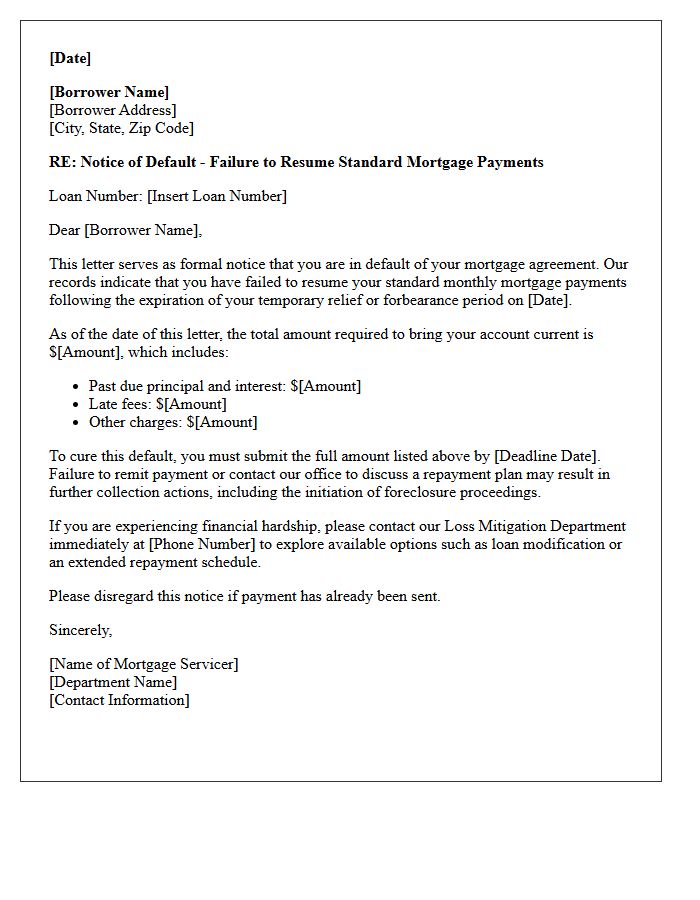

Failure to Resume Standard Mortgage Payments Default Letter

Receiving a Failure to Resume Standard Mortgage Payments Default Letter is a critical legal warning indicating you have breached your loan agreement. This formal notice signifies that your foreclosure process may soon begin if the outstanding arrears are not settled. It typically follows a temporary payment deferral or forbearance period. To protect your home, you must immediately contact your lender to discuss repayment options, loan modifications, or a formal reinstatement plan. Ignoring this document can lead to the loss of property rights and severe damage to your credit score.

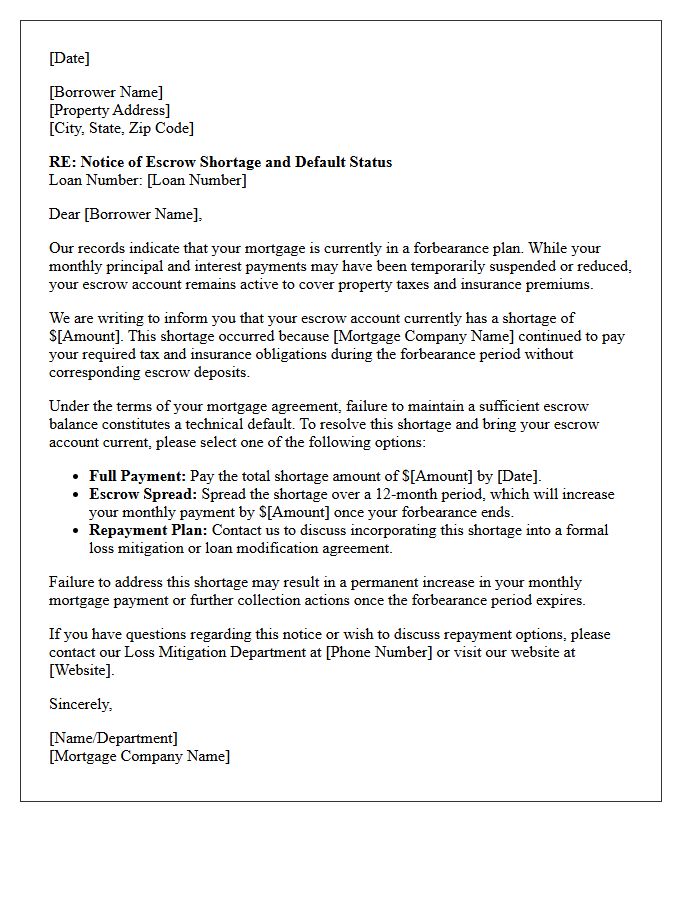

Escrow Shortage Default During Forbearance Letter

An Escrow Shortage Default During Forbearance Letter notifies homeowners that their property tax or insurance payments exceeded the funds available in their escrow account. While forbearance pauses principal and interest payments, the lender often continues advancing costs for escrowed items. This creates a deficiency that must be repaid. Recipients should contact their servicer immediately to discuss repayment options, such as spreading the shortage over twelve months or making a lump-sum payment, to ensure the loan remains in good standing once the protection period ends.

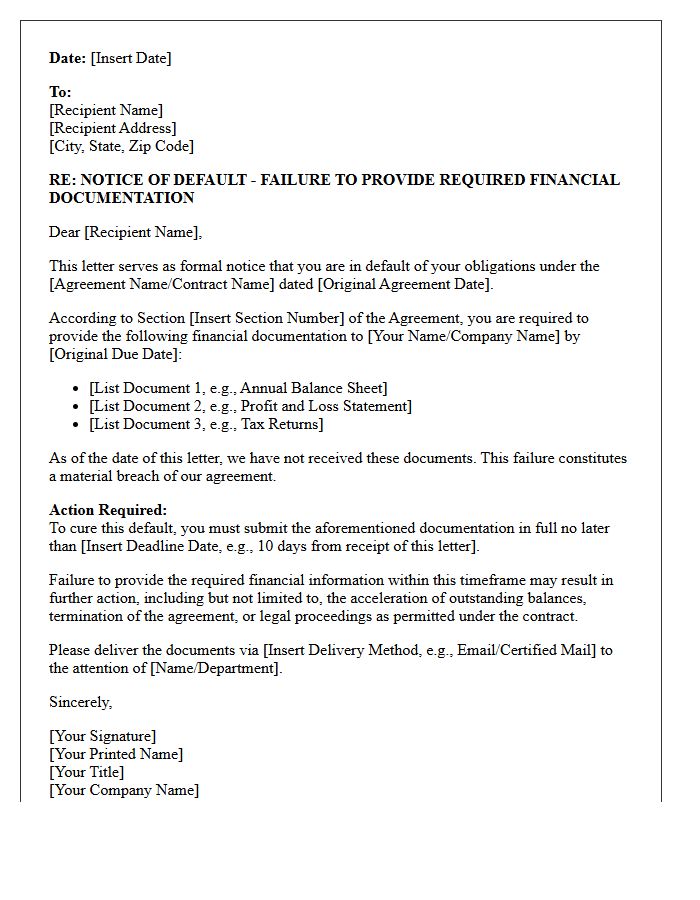

Failure to Provide Required Financial Documentation Default Letter

A Failure to Provide Required Financial Documentation Default Letter is a formal notice sent when a borrower or contractor fails to submit mandatory financial statements. This default notice serves as a legal warning that the recipient has breached their contractual reporting obligations. Failing to remedy this oversight within the specified cure period can lead to loan acceleration, termination of agreements, or legal action. It is critical to provide the requested verified documents immediately to maintain compliance and avoid severe financial penalties or loss of credit facilities.

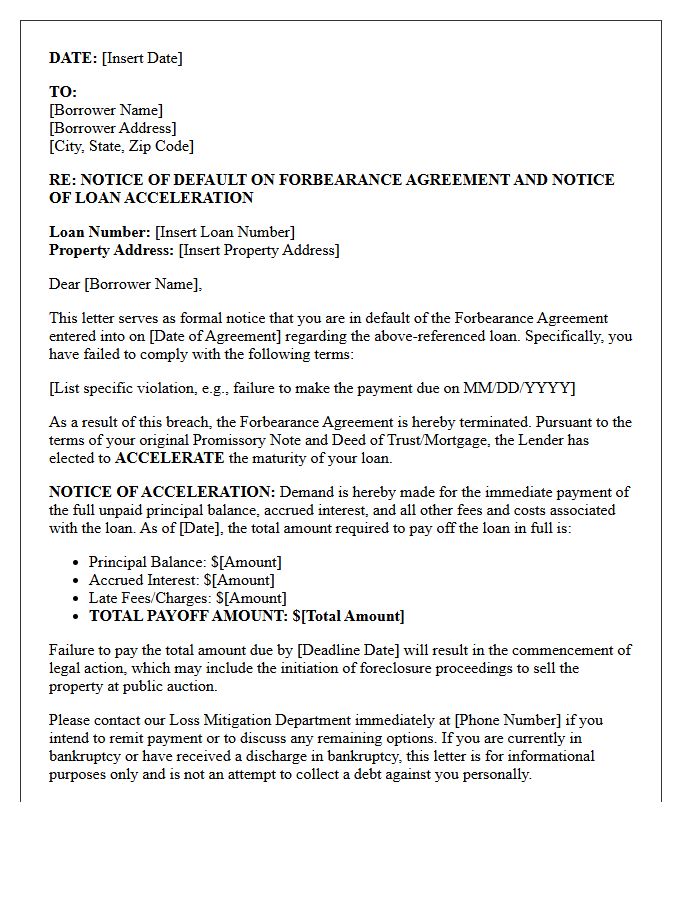

Notice of Default on Forbearance Terms and Loan Acceleration Letter

A Notice of Default and Loan Acceleration Letter signifies that a borrower has breached their forbearance agreement. This formal legal notice confirms the loss of payment relief and demands immediate repayment of the entire mortgage balance. Receiving this document means the lender is initiating the foreclosure process due to unresolved delinquency. To protect your property, you must act quickly by seeking legal counsel or contacting your servicer to explore workout options, as your right to pay in installments has been revoked following the default.

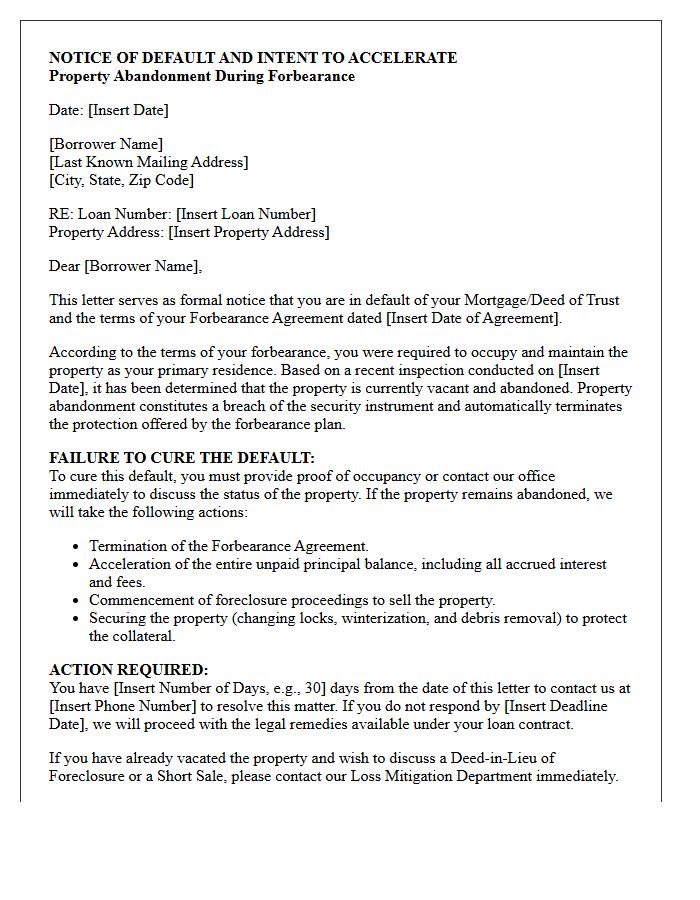

Property Abandonment Default During Forbearance Letter

A property abandonment default during forbearance letter is a formal notice sent by lenders when a borrower vacates their home while on a payment suspension plan. It warns that leaving the residence empty may violate loan terms, potentially triggering an acceleration of the debt. Borrowers must understand that occupancy is often a requirement for forbearance protection. If you receive this letter, you must provide proof of residence or risk immediate foreclosure proceedings, as abandonment typically voids the temporary relief agreement provided by the servicer.

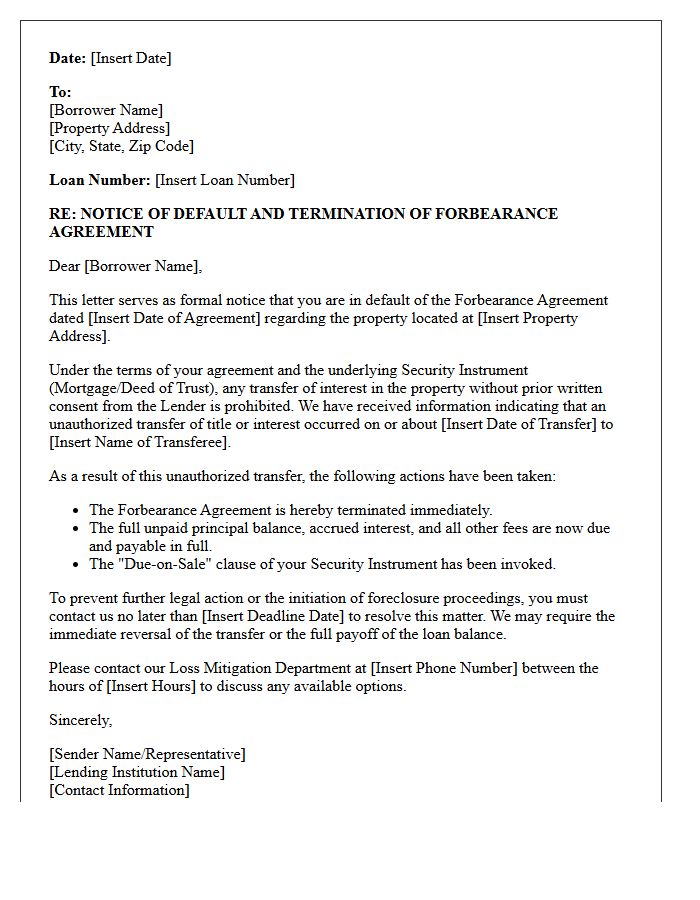

Unauthorized Property Transfer Forbearance Default Letter

An Unauthorized Property Transfer Forbearance Default Letter is a formal notice issued by a lender when a borrower transfers real estate ownership without prior consent. This action typically violates the due-on-sale clause, triggering a technical default. The letter serves as a warning that the existing forbearance agreement or mortgage terms have been breached. To avoid immediate foreclosure, the borrower must resolve the unauthorized transfer or pay the remaining loan balance in full. Prompt legal consultation is essential to navigate these serious contractual violations and preserve ownership rights.

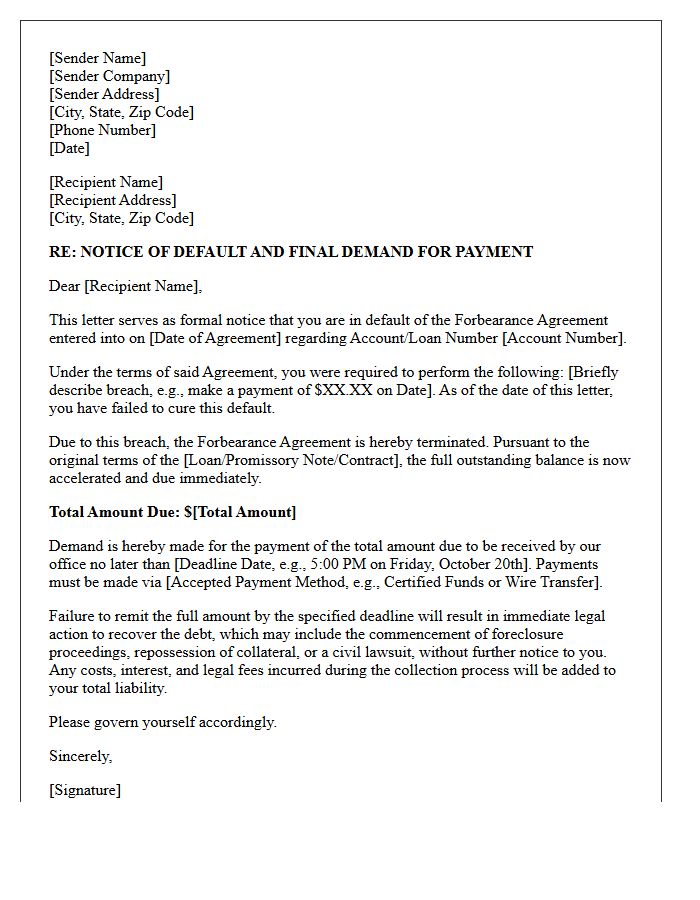

Final Demand Letter for Breached Forbearance Agreement

A final demand letter for a breached forbearance agreement is a formal legal notice issued when a borrower fails to meet the revised payment terms. This document officially terminates the temporary relief period and reinstates the lender's right to pursue foreclosure or legal action. It serves as a final warning, detailing the total amount due and providing a strictly limited timeframe to cure the default. Receiving this letter signifies that the acceleration clause has been triggered, making the entire loan balance immediately payable to avoid permanent loss of property or assets.

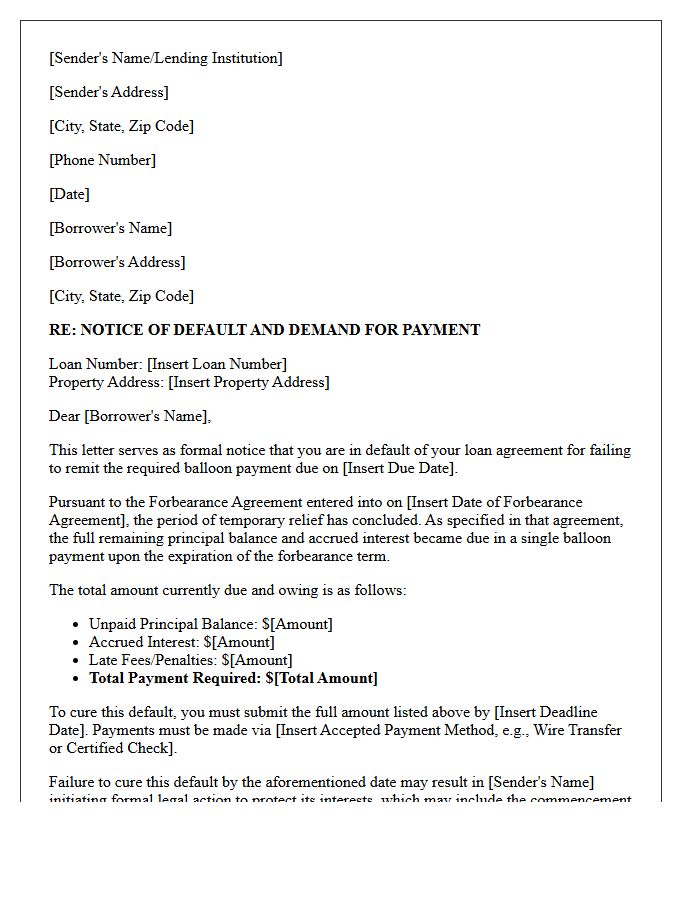

Notice of Default on Balloon Payment Following Forbearance Letter

Receiving a Notice of Default after a forbearance period indicates you failed to settle the remaining balance, specifically the balloon payment. This formal legal document warns that the lender is initiating the foreclosure process because the deferred amount was not paid by the new maturity date. It is critical to review your repayment options or seek a loan modification immediately to prevent property loss. Acting quickly allows you to negotiate a reinstatement or alternative settlement before the legal deadline expires and the home is auctioned.

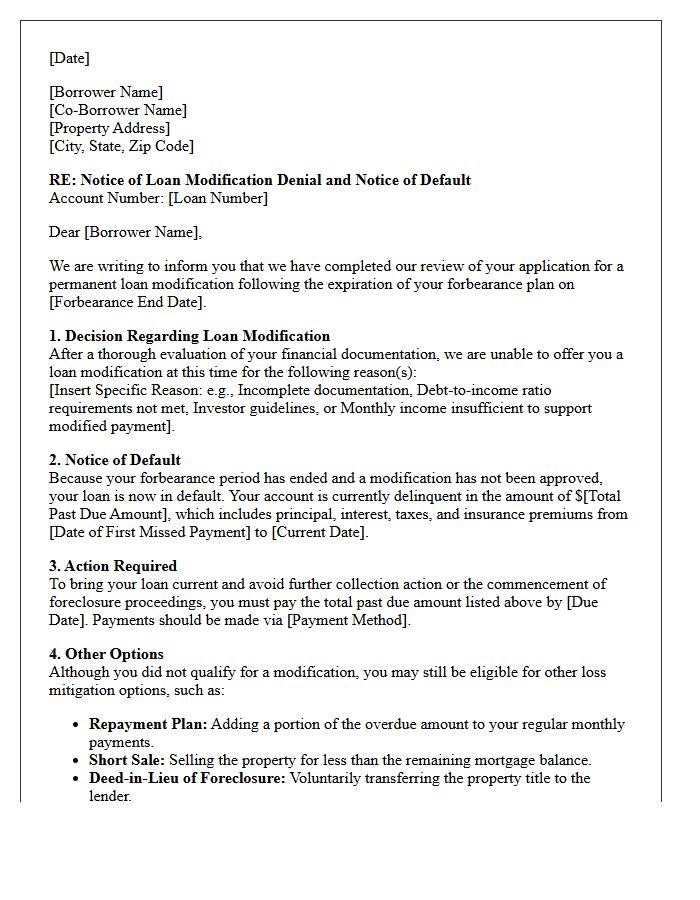

Post-Forbearance Modification Denial and Default Letter

A Post-Forbearance Modification Denial and Default Letter is a critical notice sent by lenders when a homeowner fails to qualify for a permanent loan workout. This document signifies the end of temporary relief and the start of formal foreclosure proceedings. Receiving this letter means your reinstatement options are limited, and you must act immediately to avoid losing your home. It often outlines the reasons for denial and provides a specific timeframe to appeal the decision or explore alternative solutions like a short sale or deed in lieu of foreclosure.

What is a Notice of Default on Forbearance Agreement terms?

A Notice of Default on Forbearance Agreement terms is a formal legal notification sent by a lender informing a borrower that they have failed to comply with the specific repayment conditions or obligations outlined in their existing forbearance plan.

What triggers a Notice of Default during a forbearance period?

Common triggers include missing a scheduled partial payment, failing to provide required financial documentation, or violating other contractual covenants such as maintaining property insurance or paying property taxes as agreed upon in the forbearance contract.

Can a lender start foreclosure after issuing a Notice of Default on a forbearance plan?

Yes. If the borrower fails to cure the default within the timeframe specified in the notice, the lender typically has the right to terminate the forbearance agreement and resume or initiate the formal foreclosure process to recover the debt.

How can I cure a default on my forbearance agreement?

To cure the default, you must typically pay the full past-due amount including any late fees, or rectify the specific breach of contract mentioned in the notice, before the expiration of the "right to cure" period stated in the document.

What are the alternatives if I cannot meet the terms of my forbearance agreement?

If you cannot adhere to the forbearance terms, you should immediately contact your loan servicer to discuss alternatives such as a formal loan modification, a repayment plan extension, a short sale, or a deed-in-lieu of foreclosure to avoid further legal action.

Comments