Securing an FHA loan pre-approval letter is a critical first step for homebuyers seeking government-backed financing with lower down payments. This document verifies your creditworthiness and estimated budget, showing sellers you are a serious, qualified buyer. Understanding the requirements helps streamline your path to homeownership. To simplify your application process, below are some ready to use template.

Image cover: FHA Loan Pre-Approval Letter: Professional Templates and Examples

Letter Samples List

- Federal Housing Administration Initial Loan Pre-Approval Letter

- Federal Housing Administration Conditional Loan Pre-Approval Letter

- Mortgage Lender Federal Housing Administration Pre-Approval Letter

- Federal Housing Administration Income Verified Pre-Approval Letter

- Federal Housing Administration Automated Underwriting Pre-Approval Letter

- Federal Housing Administration Manual Underwriting Pre-Approval Letter

- Federal Housing Administration Joint Applicant Pre-Approval Letter

- Federal Housing Administration Credit Assessed Pre-Approval Letter

- Federal Housing Administration Property Specific Pre-Approval Letter

- Federal Housing Administration Revised Loan Pre-Approval Letter

- Federal Housing Administration Extended Loan Pre-Approval Letter

- Federal Housing Administration Final Loan Pre-Approval Letter

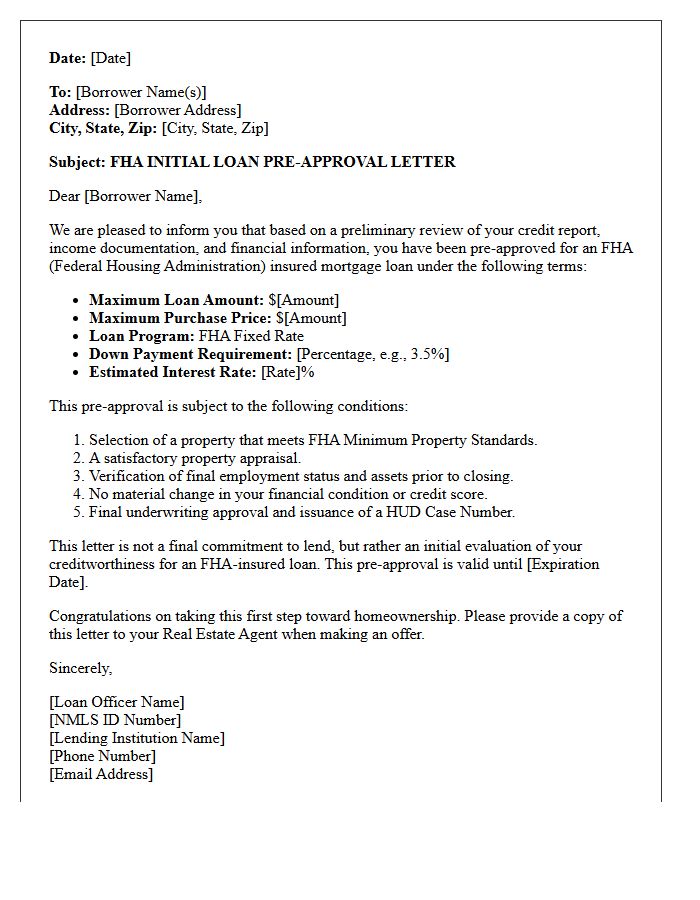

Federal Housing Administration Initial Loan Pre-Approval Letter

An FHA Initial Loan Pre-Approval Letter is a crucial document indicating a lender has preliminarily verified your creditworthiness and income. It establishes your borrowing capacity based on specific Federal Housing Administration guidelines, such as lower down payment requirements and flexible credit scores. This letter proves to sellers that you are a serious, qualified buyer capable of securing financing. To maintain its validity, avoid major financial changes like new debts or job switches, as the final approval depends on a rigorous underwriting process and a satisfactory property appraisal.

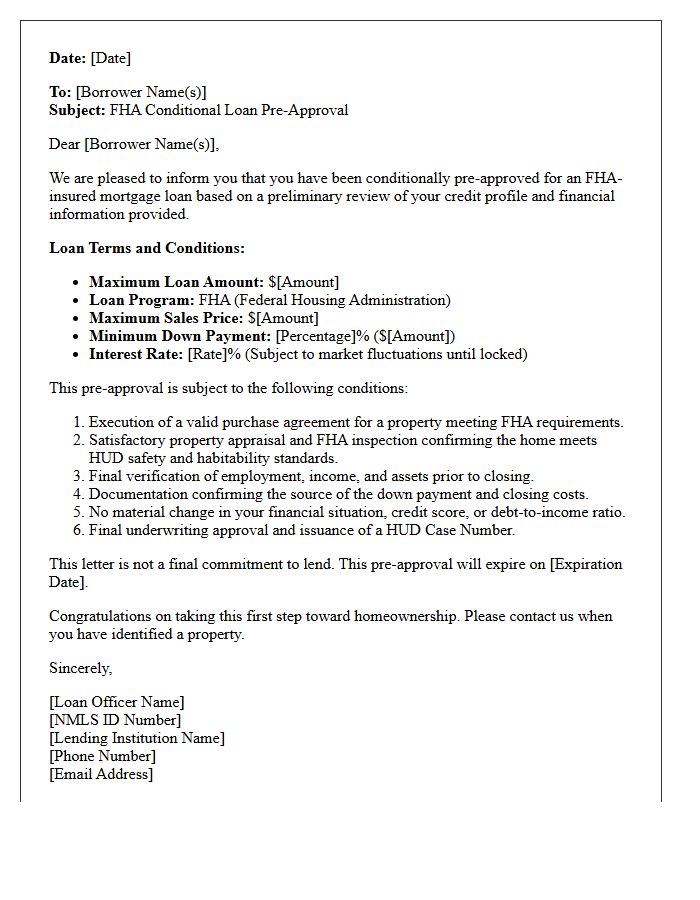

Federal Housing Administration Conditional Loan Pre-Approval Letter

A Federal Housing Administration (FHA) conditional loan pre-approval letter is a critical document indicating a lender has verified your financial data, such as credit and income. This conditional commitment signifies you are eligible for financing provided specific requirements, like a satisfactory home appraisal and final underwriting review, are met. It strengthens your position when making an offer by proving your borrowing capacity to sellers. Keep in mind that this is not a final guarantee; you must maintain your financial status until the closing date to secure the mortgage.

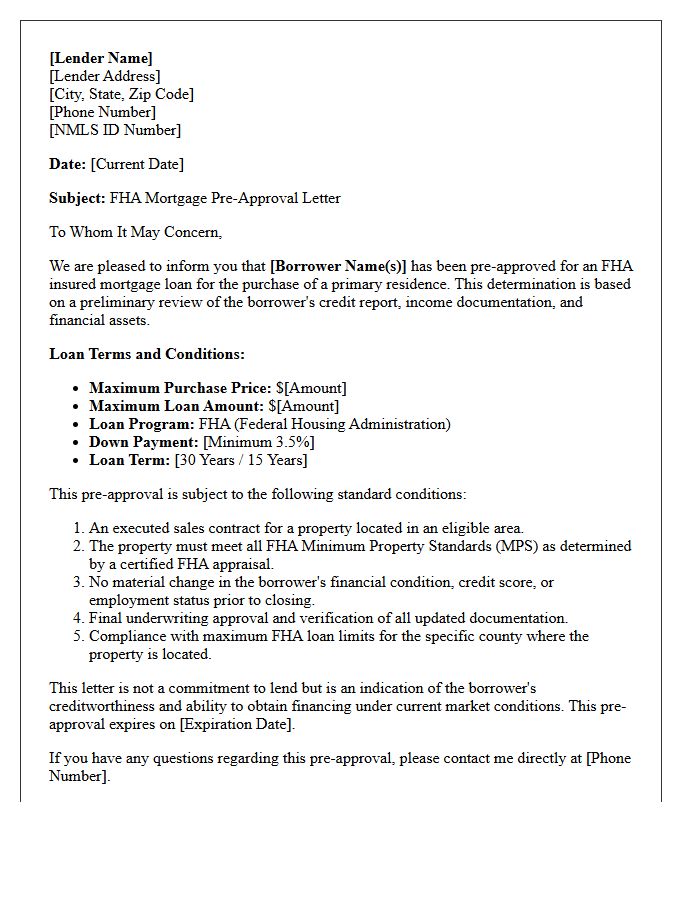

Mortgage Lender Federal Housing Administration Pre-Approval Letter

A Federal Housing Administration (FHA) pre-approval letter is a critical document issued by an FHA-approved mortgage lender. It confirms that a borrower meets specific credit and income requirements for a government-backed loan. Unlike a pre-qualification, this letter signifies a rigorous financial verification process, demonstrating to sellers that the buyer is qualified for financing with a low down payment. Obtaining this letter is the essential first step in the home-buying process, as it establishes a clear budget and strengthens the credibility of any purchase offer in a competitive real estate market.

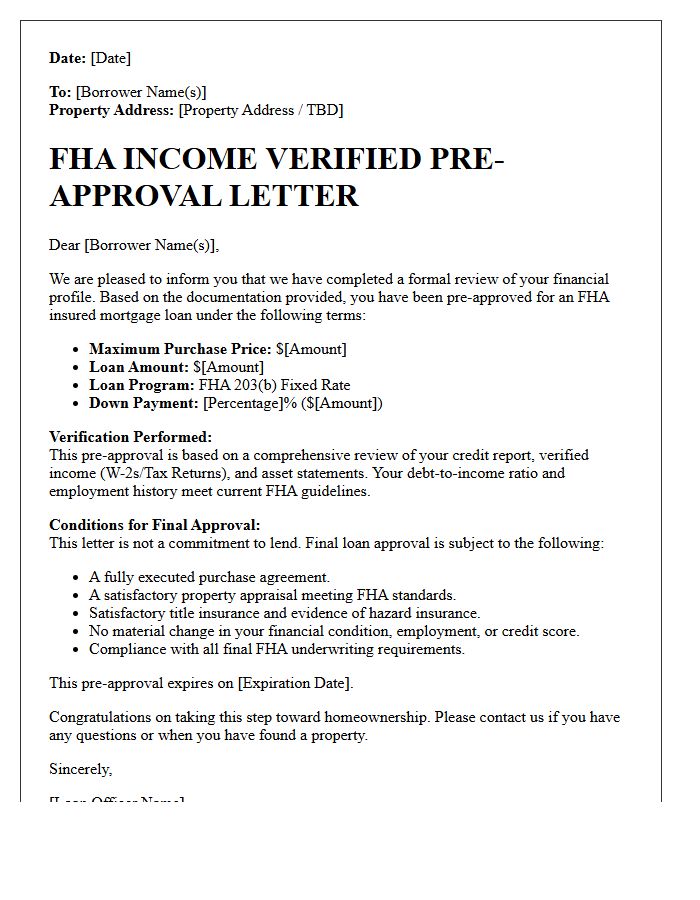

Federal Housing Administration Income Verified Pre-Approval Letter

A Federal Housing Administration (FHA) Income Verified Pre-Approval Letter is a critical document confirming a lender has vetted your financial data. Unlike a basic pre-qualification, this comprehensive evaluation involves a thorough review of tax returns, pay stubs, and bank statements. It strengthens your position with sellers by proving you meet specific FHA debt-to-income ratios and credit standards. Securing this letter ensures you are loan-ready, providing a realistic budget and a competitive edge in a crowded real estate market while guaranteeing your ability to secure government-backed financing.

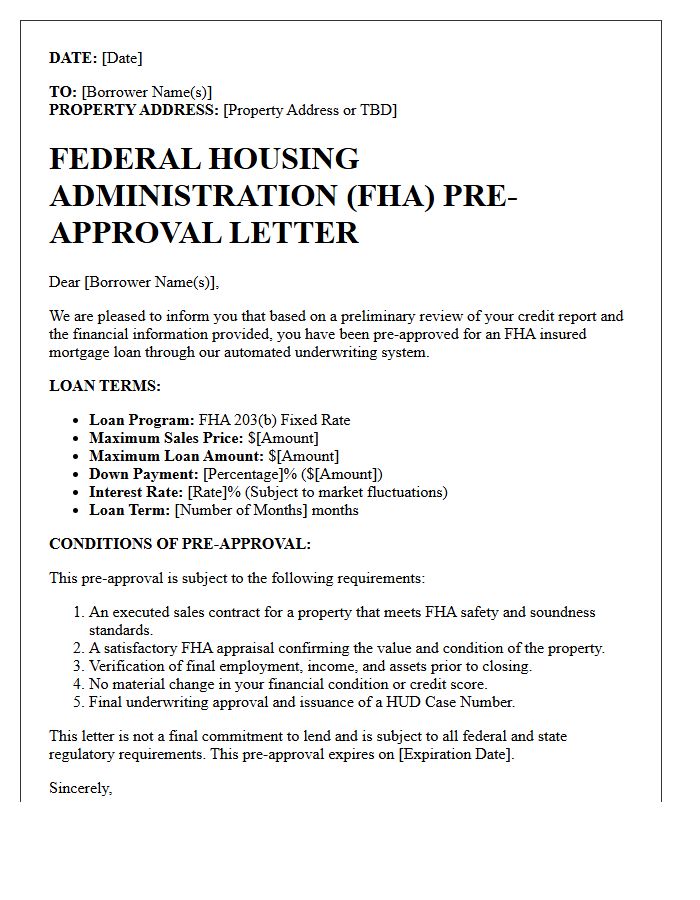

Federal Housing Administration Automated Underwriting Pre-Approval Letter

An FHA Automated Underwriting Pre-Approval Letter signifies that a mortgage lender has verified your financial data through an automated system. This document confirms you meet the eligibility requirements for a government-backed loan, including credit score and debt-to-income ratios. It provides a reliable estimate of your borrowing power, giving you a competitive advantage when making offers on a home. However, final approval remains subject to a manual underwriting review of your documentation and a satisfactory property appraisal to ensure the home meets safety standards.

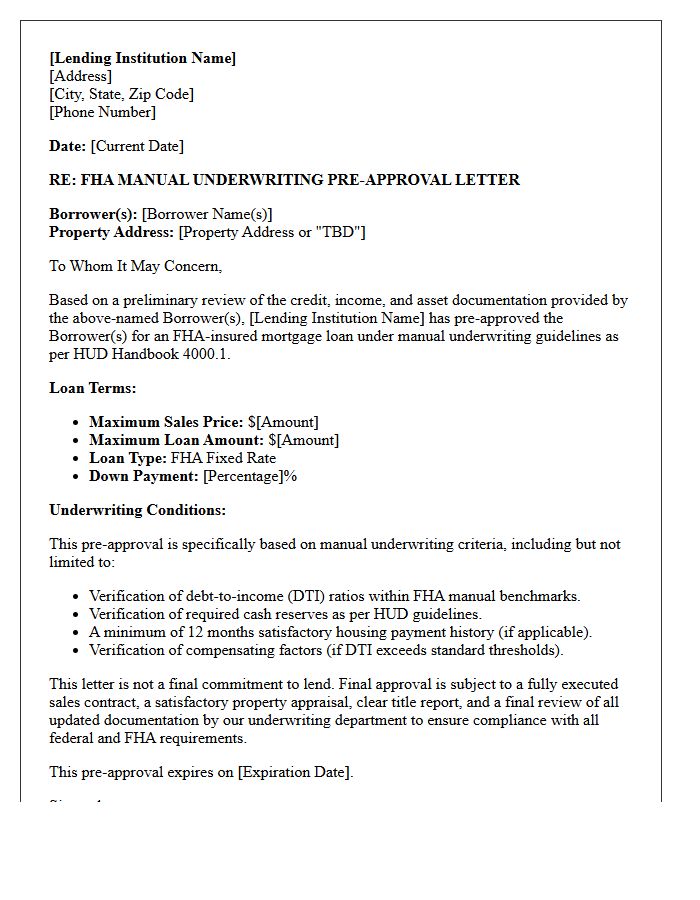

Federal Housing Administration Manual Underwriting Pre-Approval Letter

A manual underwriting pre-approval letter indicates that an FHA-approved lender has personally reviewed your financial file because automated systems could not provide an immediate decision. This manual underwriting process requires stricter documentation of your credit history, debt-to-income ratios, and cash reserves. Receiving this letter is a significant milestone, as it confirms you meet specific FHA compensating factors despite credit challenges. It provides sellers with assurance that your application has been human-verified and is likely to reach a successful loan approval once a property is selected.

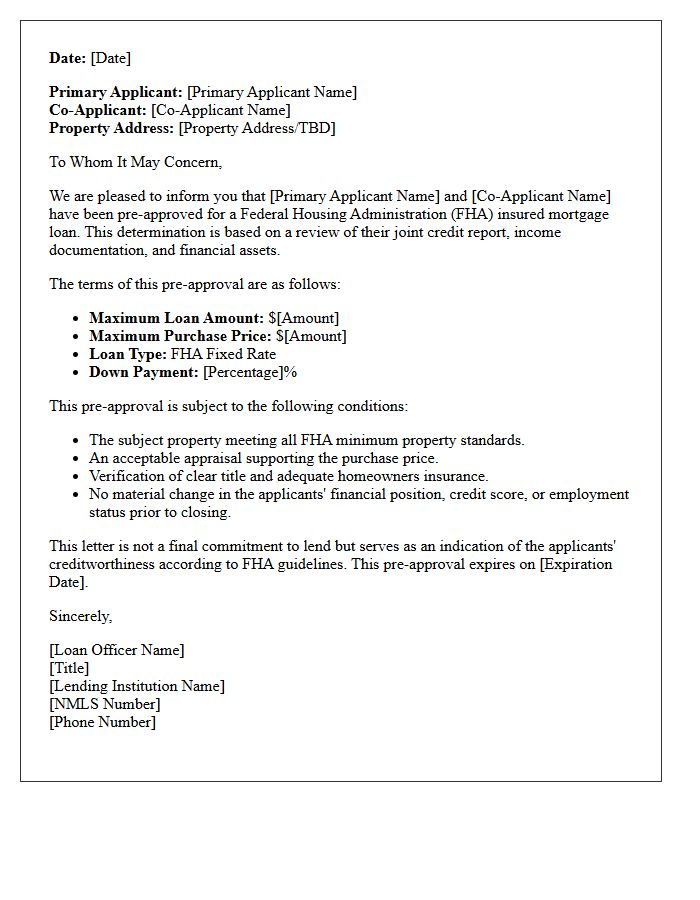

Federal Housing Administration Joint Applicant Pre-Approval Letter

An FHA Joint Applicant Pre-Approval Letter confirms that two or more borrowers have met the credit and income requirements for a government-backed mortgage. This document is essential for demonstrating financial readiness to sellers, as it combines the assets and debts of both parties to determine a maximum loan amount. For a successful application, both individuals must undergo a thorough credit evaluation and provide documentation for their shared debt-to-income ratio. This joint status can significantly increase purchasing power while ensuring both applicants are legally committed to the FHA loan terms.

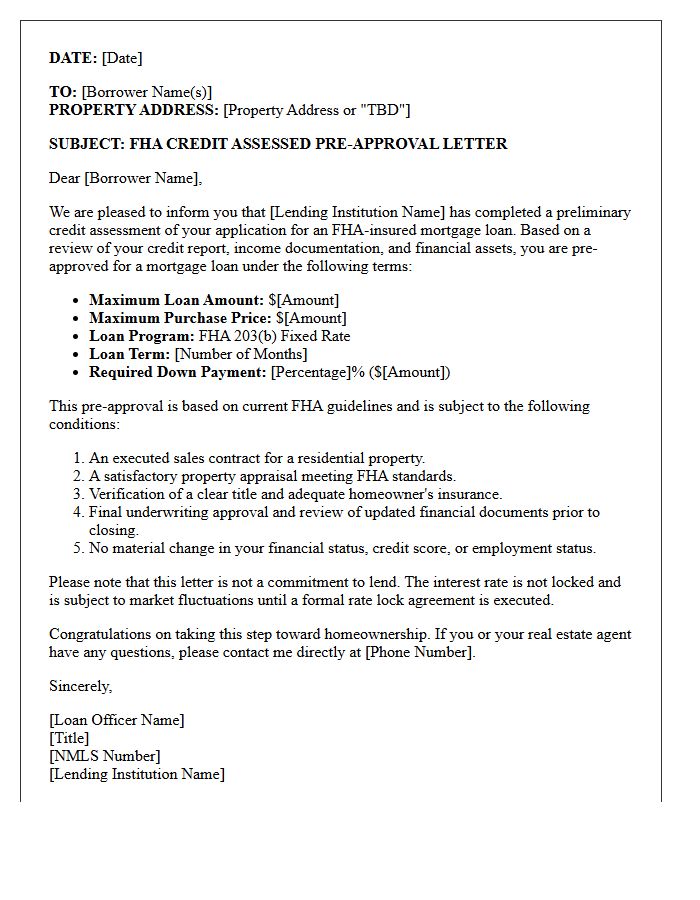

Federal Housing Administration Credit Assessed Pre-Approval Letter

A Federal Housing Administration (FHA) Credit Assessed Pre-Approval Letter is a critical document indicating a lender has verified your financial background. Unlike a basic pre-qualification, this assessment involves a comprehensive review of your credit report, income, and debt-to-income ratio. It signals to sellers that you are a serious buyer with verified financing potential. This letter strengthens your offer in competitive markets, ensuring your eligibility for government-backed loan benefits like lower down payments. Always ensure your lender performs a rigorous underwriting review to provide the most reliable pre-approval status possible.

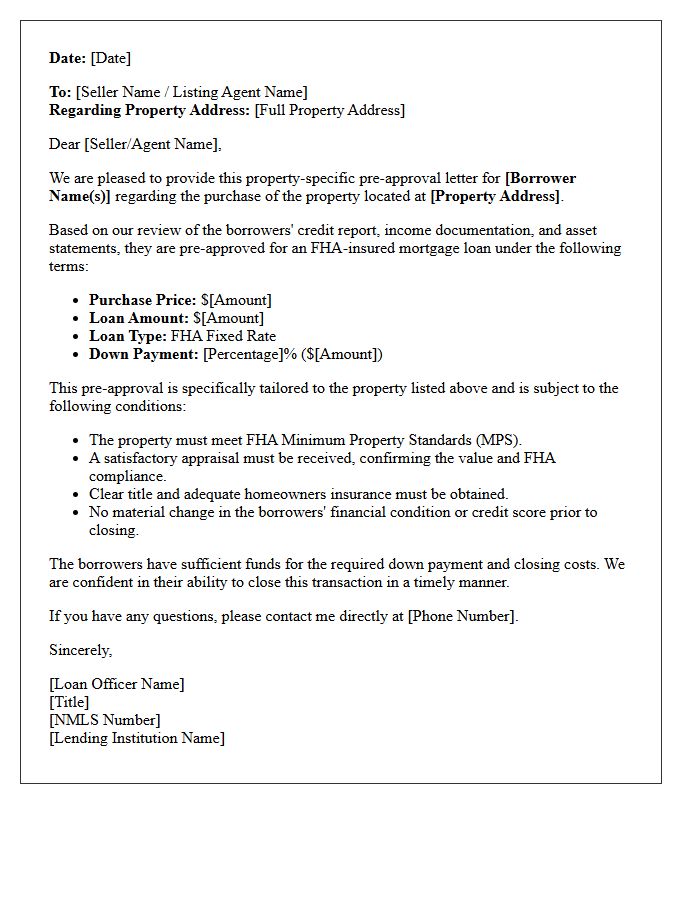

Federal Housing Administration Property Specific Pre-Approval Letter

A Federal Housing Administration (FHA) property-specific pre-approval letter is a formal document confirming a borrower's eligibility for a loan on a particular home. Unlike a general pre-approval, it includes the exact property address, estimated taxes, and insurance costs. This validates that the specific collateral meets FHA safety and habitability standards. Presenting this letter strengthens an offer by proving to sellers that the lender has already verified the financial details for their specific residence, significantly increasing the likelihood of a successful, timely closing in a competitive real estate market.

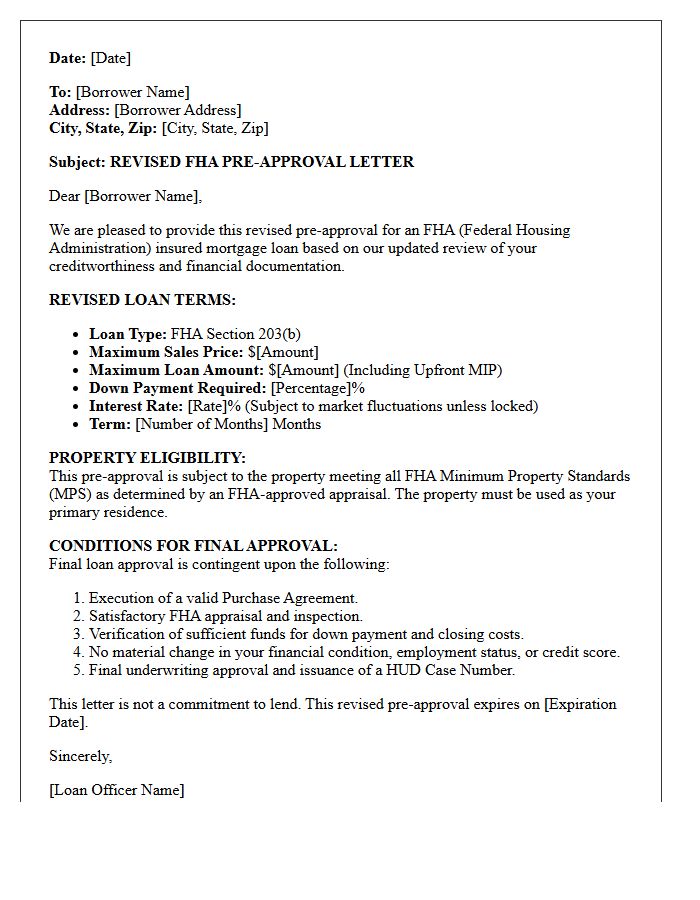

Federal Housing Administration Revised Loan Pre-Approval Letter

The Federal Housing Administration Revised Loan Pre-Approval Letter is a critical update in the homebuying process. It confirms a borrower's eligibility based on verified financial data, including income, credit score, and debt-to-income ratios. Unlike a basic pre-qualification, this Revised Pre-Approval reflects current interest rates and specific property costs. Sellers prioritize this document because it signifies a higher level of lender commitment and financial transparency, significantly strengthening a buyer's offer in competitive real estate markets. Always ensure your lender provides an updated version before submitting a formal bid on a property.

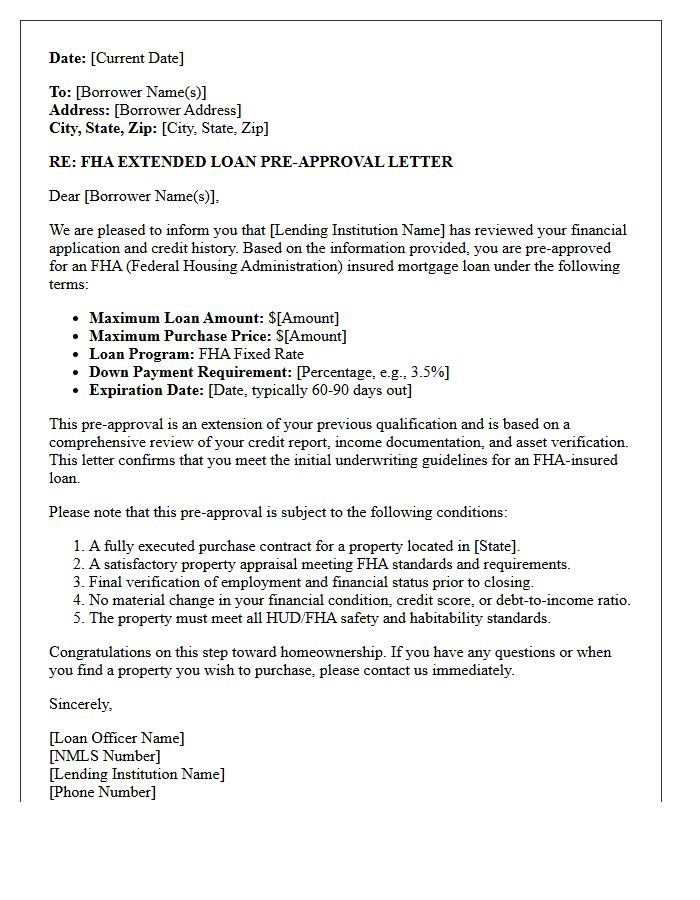

Federal Housing Administration Extended Loan Pre-Approval Letter

A Federal Housing Administration (FHA) Extended Loan Pre-Approval Letter provides potential homebuyers with a longer commitment period, typically lasting up to 120 days. This document signals to sellers that a borrower meets specific HUD guidelines regarding credit scores, debt-to-income ratios, and down payment requirements. It offers a competitive advantage in slow markets by locking in eligibility status. However, it remains subject to a final underwriting review and a satisfactory property appraisal to ensure the home meets FHA safety standards before the mortgage is officially funded.

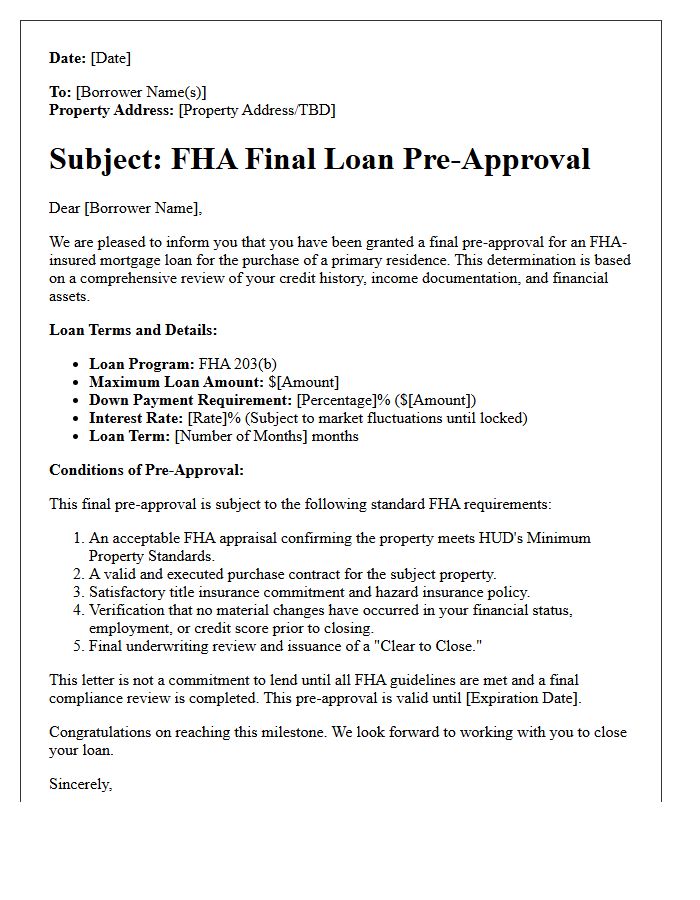

Federal Housing Administration Final Loan Pre-Approval Letter

A Federal Housing Administration (FHA) Final Loan Pre-Approval Letter is a critical document confirming that a lender has rigorously verified your financial data. Unlike a preliminary assessment, this stage involves a comprehensive underwriting review of your credit score, income, and debt-to-income ratio. Receiving this letter signals to sellers that you are a qualified buyer with secured financing, significantly strengthening your offer in a competitive real estate market. It represents the final milestone before the formal mortgage commitment and the closing process begins.

What is an FHA loan pre-approval letter?

An FHA loan pre-approval letter is an official document from a mortgage lender stating that a borrower tentatively qualifies for a Federal Housing Administration-backed loan up to a specific amount. This letter is issued after the lender evaluates the borrower's credit score, income, assets, and employment history.

How do I get a pre-approval letter for an FHA loan?

To obtain an FHA pre-approval, you must submit a formal application to an FHA-approved lender. You will need to provide documentation such as tax returns, W-2s, recent pay stubs, and bank statements for a comprehensive credit and financial review.

How long is an FHA loan pre-approval letter valid?

Most FHA loan pre-approval letters are valid for 60 to 90 days. Because credit reports and financial documents expire, lenders require periodic updates to the letter if the home search takes longer than the initial period.

What is the difference between FHA pre-qualification and FHA pre-approval?

FHA pre-qualification is a basic estimate of borrowing power based on unverified information provided by the borrower. In contrast, an FHA pre-approval is a conditional commitment from a lender based on verified financial data, making it a much stronger tool when making an offer on a home.

Does an FHA pre-approval letter guarantee that I will get the loan?

No, an FHA pre-approval letter is not a final loan guarantee. The final mortgage approval is subject to a satisfactory home appraisal, a clear title search, and no significant changes to the borrower's financial status or credit score before closing.

Comments