Secure financing by leveraging your substantial holdings with a High Net Worth Asset Depletion Pre-Approval Letter. This specialized document calculates monthly income based on total liquid assets rather than traditional employment earnings, streamlining the mortgage process for wealthy investors and retirees. It demonstrates your true purchasing power to lenders and sellers alike. Below are some ready to use templates.

Image cover: The Ultimate Asset Depletion Pre-Approval Guide for High Net Worth Borrowers: Custom Templates and Strategic Samples

Letter Samples List

- High Net Worth Asset Depletion Pre-Approval Letter

- Jumbo Mortgage Asset Depletion Pre-Approval Letter

- Liquid Asset Dissipation Loan Pre-Approval Letter

- Private Wealth Asset Depletion Pre-Approval Letter

- Investment Portfolio Depletion Mortgage Pre-Approval Letter

- Retirement Asset Qualification Pre-Approval Letter

- Wealth Management Asset Depletion Pre-Approval Letter

- Significant Asset Amortization Loan Pre-Approval Letter

- Trust Fund Asset Depletion Pre-Approval Letter

- Qualified Asset Based Income Pre-Approval Letter

- High Balance Asset Dissipation Pre-Approval Letter

- Comprehensive Wealth Asset Depletion Pre-Approval Letter

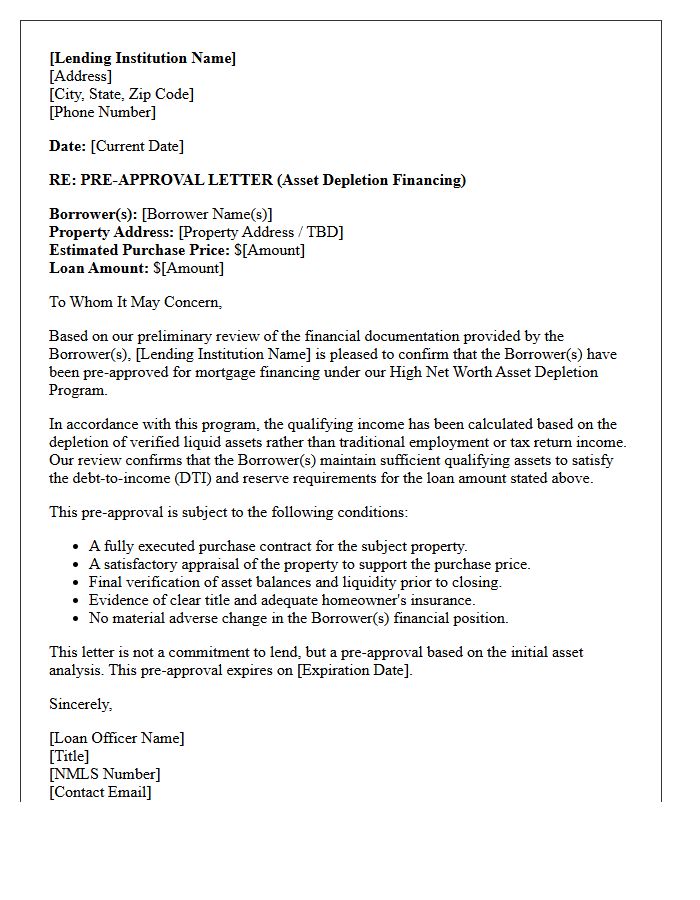

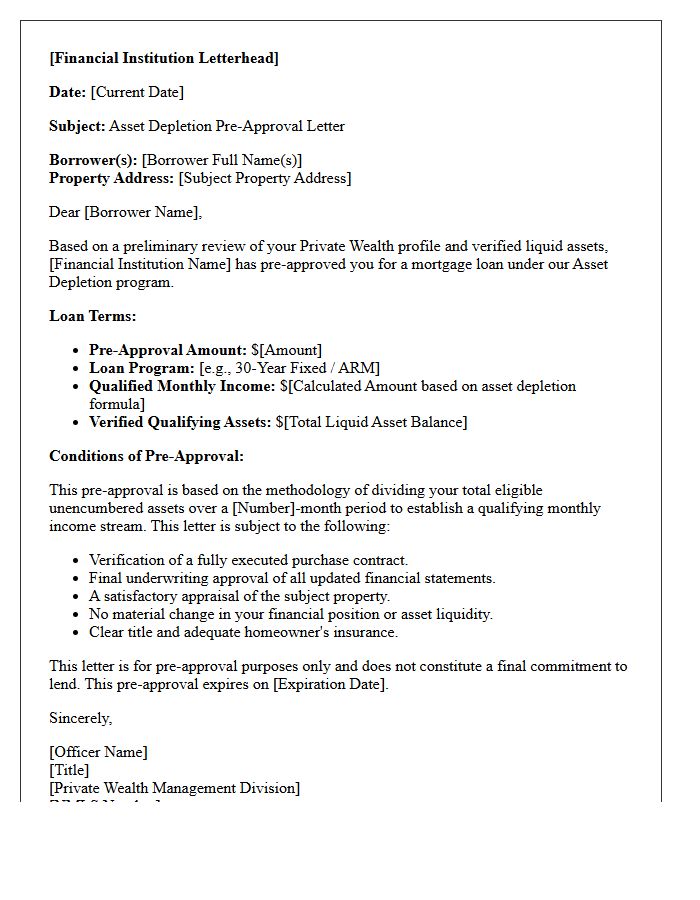

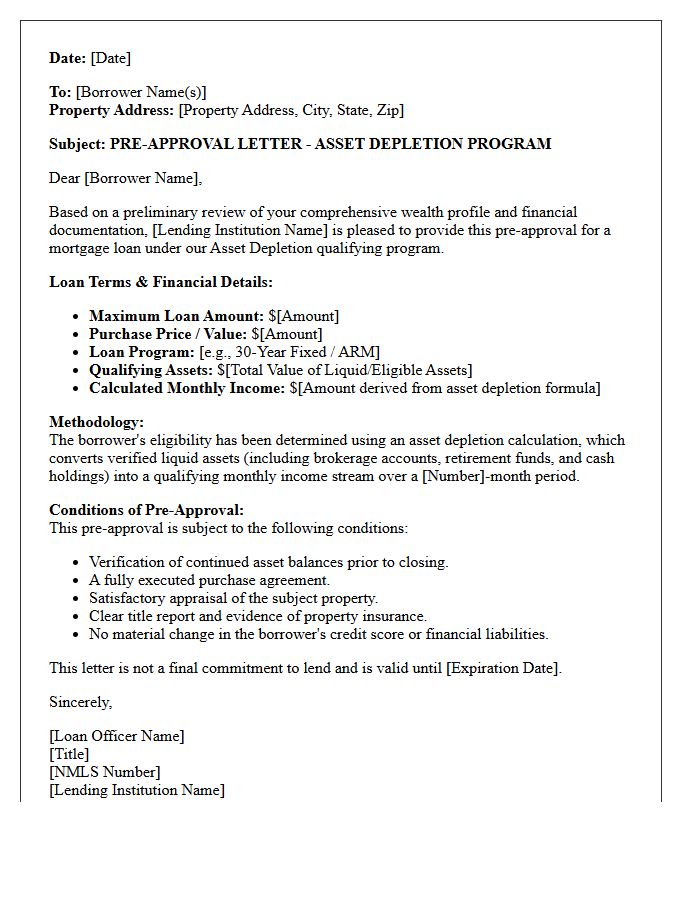

High Net Worth Asset Depletion Pre-Approval Letter

A High Net Worth Asset Depletion Pre-Approval Letter is a specialized financing document for affluent borrowers with significant liquid holdings but limited traditional income. Instead of using tax returns, lenders apply a formulaic calculation to divide total eligible assets by a set loan term to create a qualifying monthly income stream. This method allows wealthy investors to secure competitive mortgage rates based on their net worth rather than employment earnings. It is an essential tool for retirees or self-employed individuals seeking high-value real estate without liquidating their entire investment portfolio.

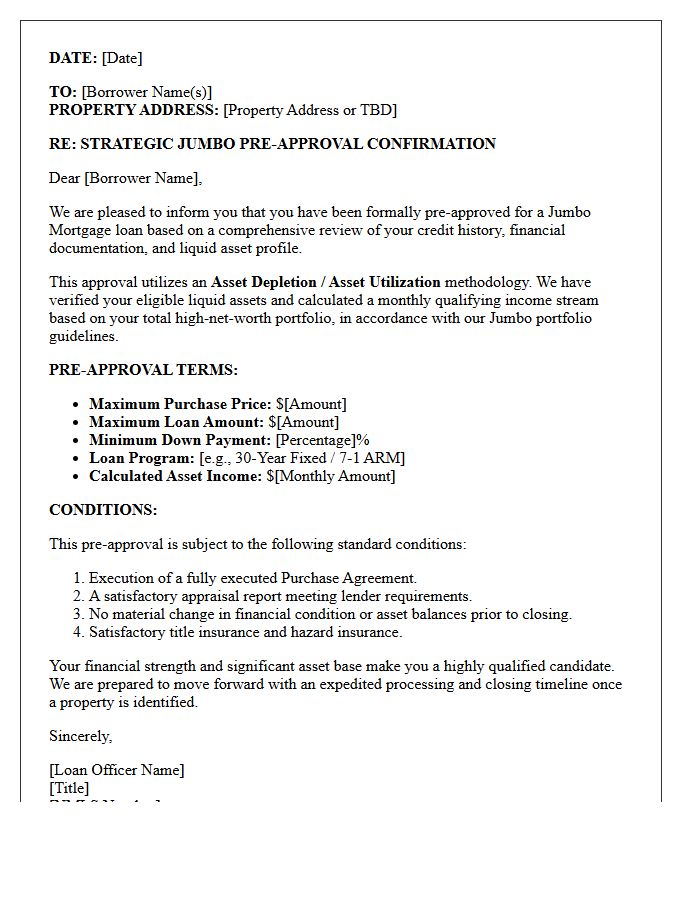

Jumbo Mortgage Asset Depletion Pre-Approval Letter

A Jumbo Mortgage Asset Depletion Pre-Approval Letter is a specialized financing document for high-net-worth borrowers. Instead of traditional income, lenders calculate qualifying income by dividing your total liquid assets over a specific loan term. This allows retirees or entrepreneurs with significant wealth but low monthly cash flow to secure luxury financing. To obtain this letter, you must provide verified statements of brokerage accounts or savings. It serves as proof of purchasing power, signaling to sellers that your substantial assets satisfy long-term debt obligations despite lacking standard payroll documentation.

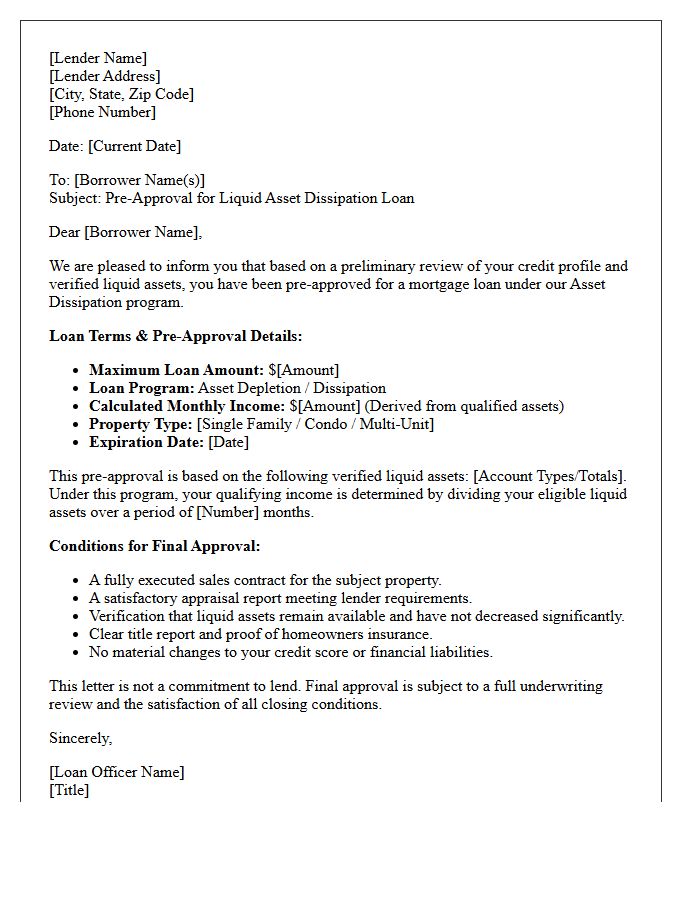

Liquid Asset Dissipation Loan Pre-Approval Letter

A Liquid Asset Dissipation pre-approval letter is a specialized financing document for high-net-worth borrowers. Instead of traditional employment income, lenders calculate a notional monthly income by dividing total qualifying assets by a set loan term. This allows retirees or self-employed individuals to secure a mortgage based on their liquidity rather than paystubs. To qualify, assets must be unencumbered and easily accessible. This letter proves to sellers that your significant cash reserves, stocks, or bonds are sufficient to guarantee long-term repayment, providing a competitive edge in luxury real estate markets.

Private Wealth Asset Depletion Pre-Approval Letter

A Private Wealth Asset Depletion Pre-Approval Letter is a specialized financing document for high-net-worth individuals. Instead of traditional income, lenders calculate qualifying monthly income by dividing total liquid assets by a specific loan term. This allows wealthy borrowers with significant liquidity but low taxable income to secure high-value mortgages. It confirms that the borrower's asset base is sufficient to cover debt obligations, providing a competitive advantage in luxury real estate markets by proving financial strength without standard paystubs or tax returns.

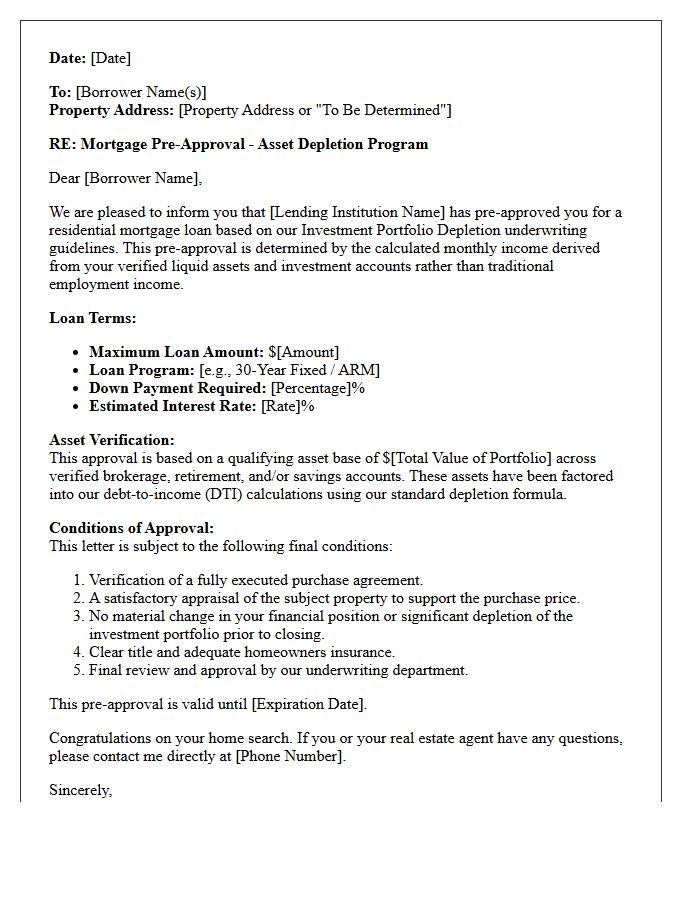

Investment Portfolio Depletion Mortgage Pre-Approval Letter

An Investment Portfolio Depletion mortgage pre-approval letter allows retirees or high-net-worth individuals to qualify for financing using liquid assets rather than traditional monthly income. Lenders calculate a notional income stream by dividing the total value of eligible brokerage accounts or retirement funds by a specific term, usually 360 months. This method is essential for borrowers with significant wealth but limited recurring salary. It provides a formal document verifying purchasing power, ensuring you can compete effectively in the real estate market by leveraging your existing investment capital as collateralized qualifying income.

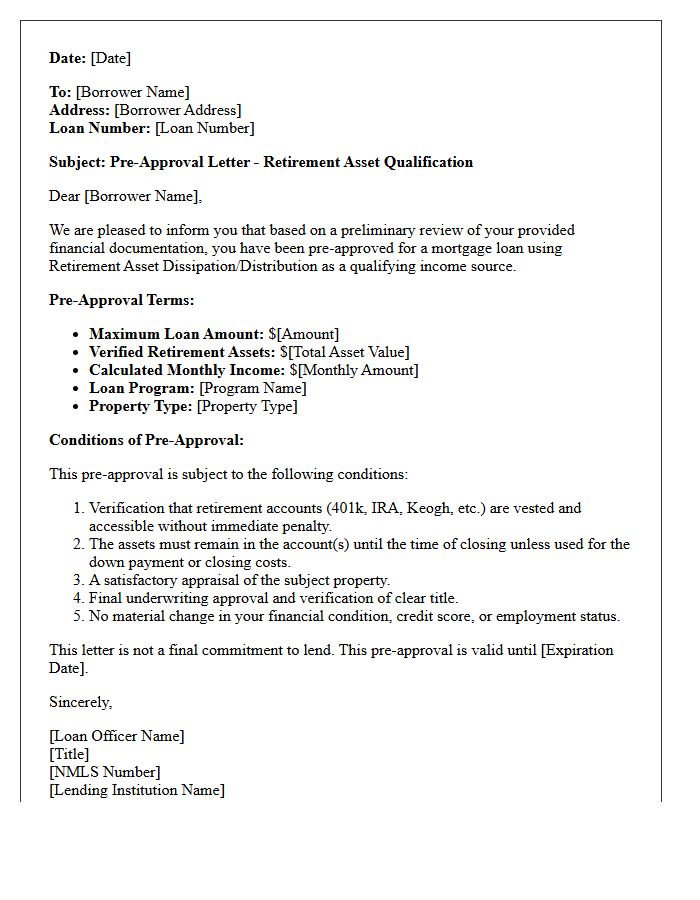

Retirement Asset Qualification Pre-Approval Letter

A retirement asset qualification pre-approval letter confirms that a lender has verified your 401(k), IRA, or pension accounts as valid sources for mortgage financing. This document is essential for asset-based lending, where your savings-rather than traditional monthly income-determine your borrowing power. It provides sellers with proof that your retirement funds are sufficiently liquid and accessible for down payments or monthly obligations. Obtaining this letter early streamlines the home-buying process for retirees or those with significant wealth tied to investment accounts.

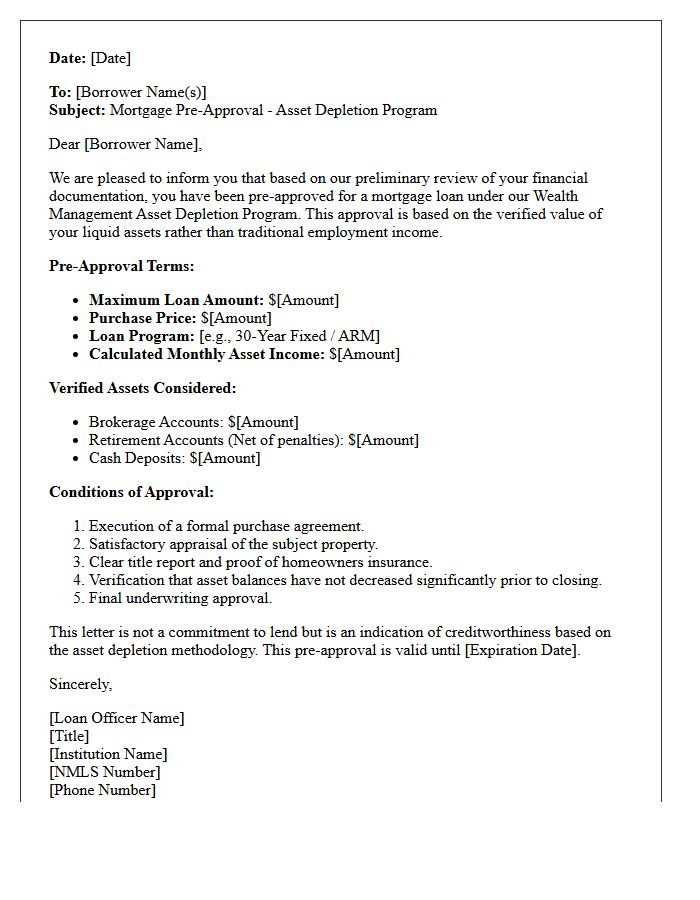

Wealth Management Asset Depletion Pre-Approval Letter

A Wealth Management Asset Depletion Pre-Approval Letter is a specialized financing document used for high-net-worth borrowers. Instead of traditional income, lenders calculate qualifying income by dividing total liquid assets over a specific loan term. This allows retirees or investors with significant wealth but low monthly cash flow to secure a mortgage. Obtaining this letter proves that your asset base provides sufficient liquidity to satisfy debt obligations. It is a critical tool for non-QM lending, ensuring competitive rates by demonstrating long-term financial stability through personal portfolios rather than standard paystubs.

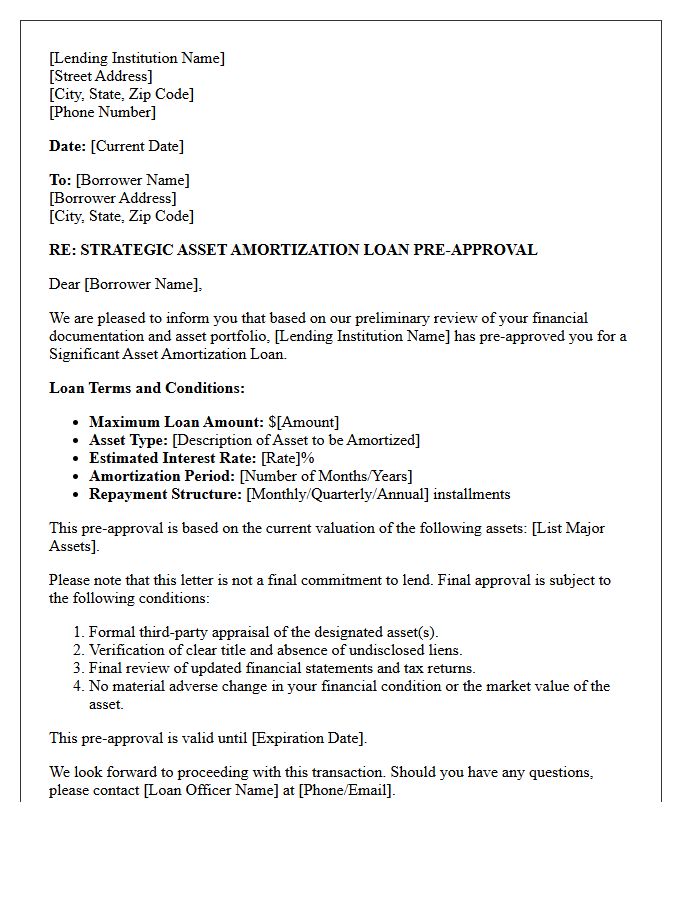

Significant Asset Amortization Loan Pre-Approval Letter

A Significant Asset Amortization Loan Pre-Approval Letter confirms a lender's preliminary commitment to finance high-value purchases. This document validates your financial credibility by accounting for the gradual repayment of principal and interest over time. It is crucial for high-net-worth borrowers because it highlights liquidity verification and asset stability. Sellers prioritize this letter as it proves the buyer has secured the necessary capital structure to complete complex, large-scale transactions efficiently while minimizing closing risks.

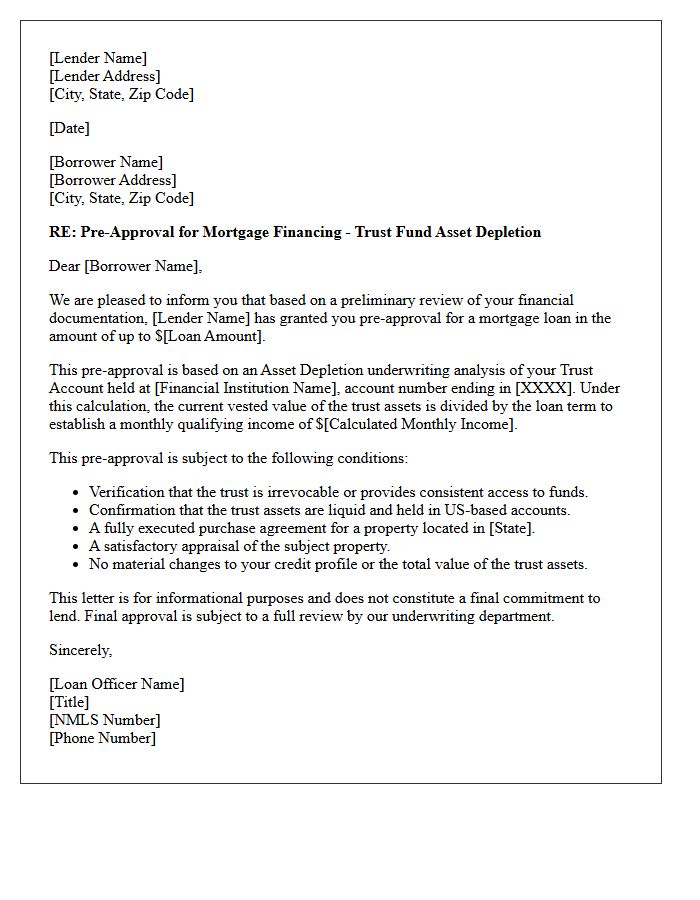

Trust Fund Asset Depletion Pre-Approval Letter

A Trust Fund Asset Depletion Pre-Approval Letter is a crucial document for borrowers using trust income to qualify for a mortgage. It verifies that the trust allows for regular monthly distributions and confirms the remaining assets are sufficient to sustain payments for at least three years. Lenders require this verification to ensure long-term repayment stability. Obtaining this letter early prevents financing delays by proving the trust is a reliable income source, making it an essential tool for securing loan approval when traditional employment income is insufficient.

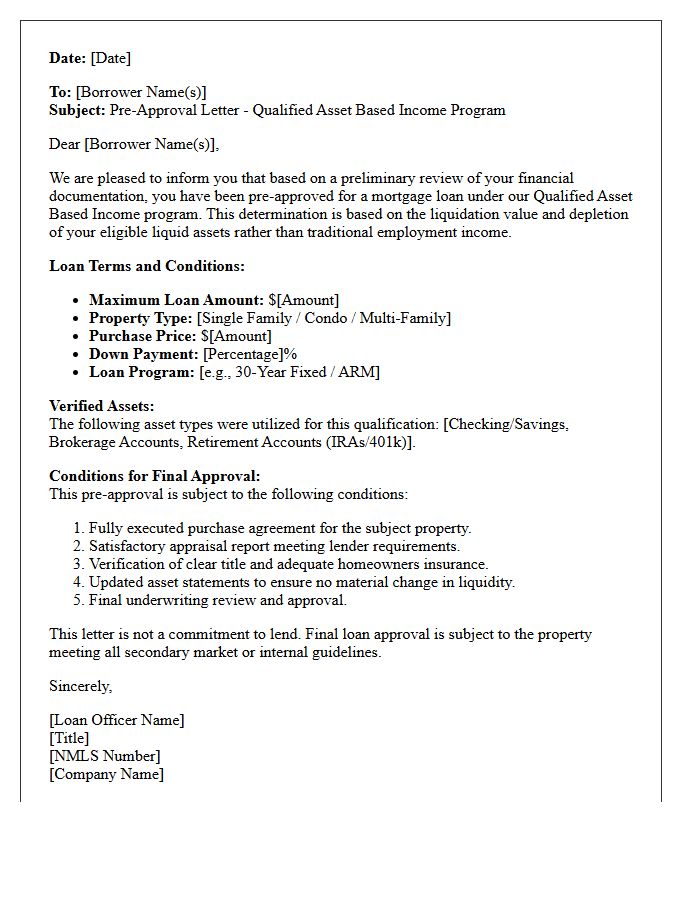

Qualified Asset Based Income Pre-Approval Letter

A Qualified Asset Based Income Pre-Approval Letter is a crucial document for high-net-worth borrowers or retirees seeking a mortgage without traditional employment. This specialized financing uses asset depletion formulas to convert liquid holdings into qualifying monthly income. Lenders verify liquid assets like stocks, bonds, and savings to determine debt-to-income ratios. Securing this letter proves your financial strength to sellers by demonstrating that your wealth reserves, rather than a monthly paycheck, are sufficient to satisfy long-term mortgage obligations and closing costs.

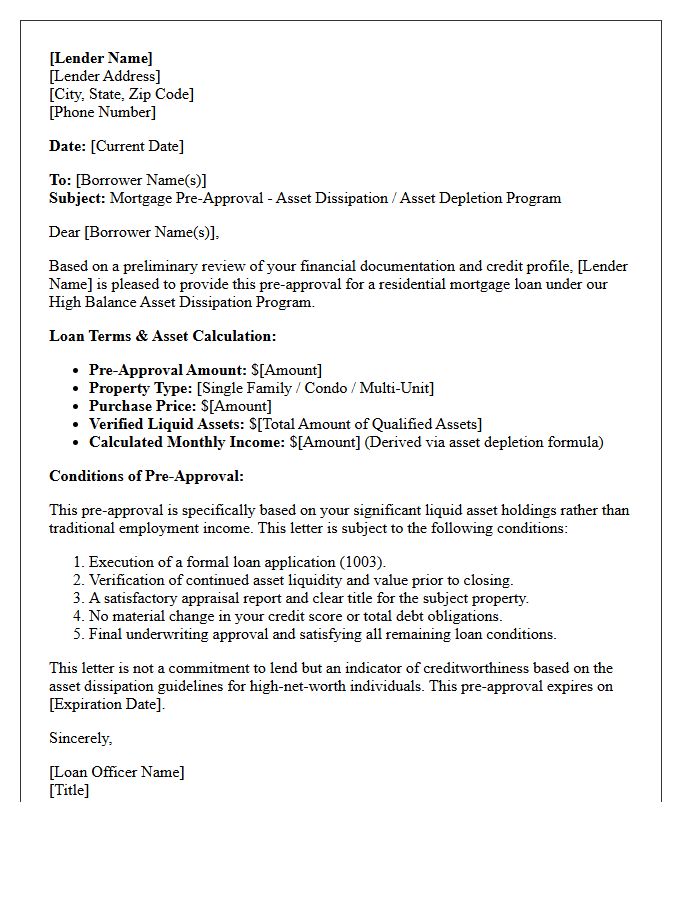

High Balance Asset Dissipation Pre-Approval Letter

A High Balance Asset Dissipation Pre-Approval Letter is a specialized financing document used by high-net-worth borrowers to qualify for a mortgage using liquid wealth rather than traditional employment income. Lenders calculate a monthly income stream based on the total value of eligible assets divided by a set term. This asset depletion strategy allows investors and retirees to secure luxury financing by proving substantial liquidity. It provides a competitive advantage in real estate markets by confirming purchasing power through verified capital reserves instead of monthly paystubs.

Comprehensive Wealth Asset Depletion Pre-Approval Letter

A Comprehensive Wealth Asset Depletion Pre-Approval Letter is a specialized document for high-net-worth borrowers. Instead of traditional employment income, lenders calculate a monthly qualifying income by dividing total liquid assets over a specific loan term. This allows retirees or investors to secure financing based on their portfolio value rather than a paycheck. This letter serves as essential proof to sellers that the borrower has sufficient liquid wealth to sustain mortgage payments, providing a competitive advantage in luxury real estate markets where standard tax returns may not reflect true purchasing power.

What is a High Net Worth Asset Depletion Pre-Approval Letter?

A High Net Worth Asset Depletion Pre-Approval Letter is a document issued by a lender that verifies a borrower's mortgage eligibility based on their total liquid assets rather than traditional employment income. It calculates a "monthly income stream" by dividing the borrower's qualifying assets by a specific term, usually 360 months, to meet debt-to-income requirements.

Which assets qualify for an asset depletion mortgage pre-approval?

To secure a pre-approval letter using this method, lenders typically look at liquid or semi-liquid assets including checking and savings accounts, certificates of deposit (CDs), money market accounts, publicly traded stocks, bonds, and mutual funds. Some lenders may also include a percentage of vested retirement accounts, such as a 401(k) or IRA, depending on the borrower's age.

How is the monthly income calculated for a high net worth pre-approval?

Lenders calculate qualifying income by taking the total value of eligible assets, subtracting the down payment and required closing reserves, and then dividing the remainder by a set period (typically 36 years or 432 months, though some use 30 years). This resulting figure is used as the borrower's monthly qualifying income on the pre-approval letter.

Do I need to be currently employed to get a pre-approval letter based on assets?

No, one of the primary benefits of a High Net Worth Asset Depletion Pre-Approval is that it allows retired individuals, self-employed borrowers with high write-offs, or those between careers to qualify for a luxury home loan without a traditional pay stub or W-2, provided their asset base is sufficient to cover the loan obligations.

Does an asset depletion pre-approval require me to liquidate my investments?

No, a pre-approval letter based on asset depletion does not require the borrower to actually spend or liquidate their assets to pay the mortgage. The "depletion" is a mathematical formula used solely for underwriting and risk assessment to prove the borrower has the financial capacity to repay the loan over time.

Comments