Receiving a Rate Lock Extension Denial Letter can jeopardize your mortgage terms and monthly payments. This formal notice indicates that your lender will not extend your original interest rate beyond the expiration date, often due to processing delays or market shifts. Understanding your options is crucial for securing your financing. To help you respond effectively, below are some ready to use template.

Image cover: Official Notice: Mortgage Rate Lock Extension Request Denial

Letter Samples List

- Mortgage Rate Lock Extension Denial Letter

- Notice of Rate Lock Extension Denial Letter

- Denial of Rate Lock Extension Request Letter

- Declined Mortgage Rate Lock Extension Letter

- Interest Rate Lock Extension Denial Letter

- Expired Rate Lock Period Denial Letter

- Ineligible Rate Lock Extension Denial Letter

- Unapproved Loan Rate Lock Extension Letter

- Final Decision Rate Lock Extension Denial Letter

- Borrower Interest Rate Lock Extension Denial Letter

- Adverse Action Rate Lock Extension Denial Letter

- Standard Rate Lock Extension Denial Letter

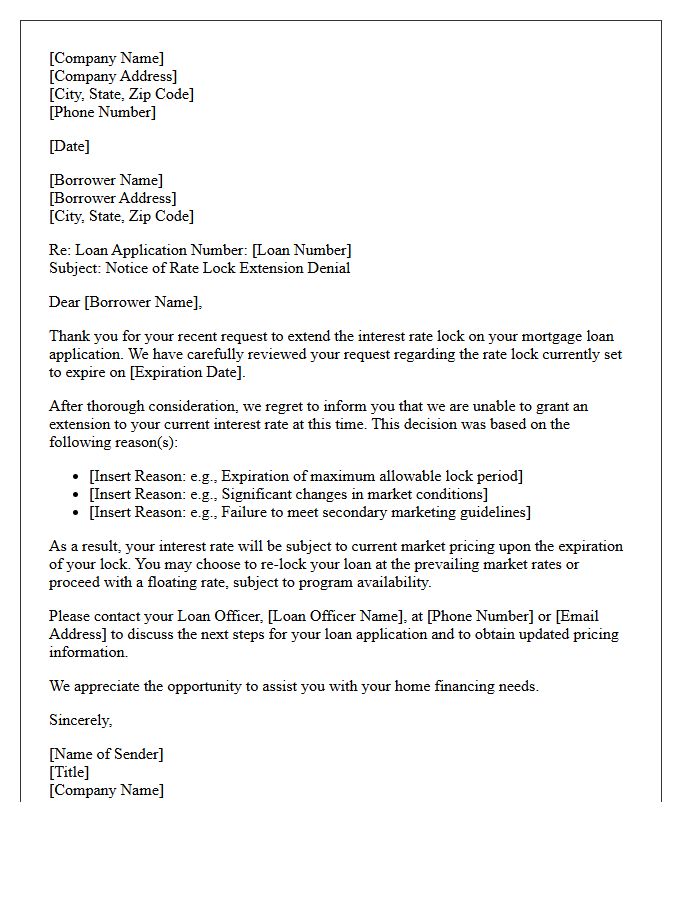

Mortgage Rate Lock Extension Denial Letter

A mortgage rate lock extension denial letter is a formal notice from a lender refusing to prolong your current interest rate. This typically occurs when the rate lock period expires due to processing delays or unmet underwriting conditions. Receiving this document means your loan will likely revert to prevailing market rates, which could increase your monthly payments. To mitigate financial impact, immediately contact your loan officer to discuss a relock agreement, potential fee waivers, or alternative financing options before your scheduled closing date.

Notice of Rate Lock Extension Denial Letter

A Notice of Rate Lock Extension Denial Letter informs a borrower that their request to prolong a guaranteed interest rate has been rejected. This typically occurs if the lock period expires before the loan closes and the lender determines the extension criteria were not met. Consequently, your mortgage rate may increase to reflect current market conditions. It is crucial to review the stated reasons for denial immediately to discuss alternative financing options or potential rate relock strategies with your loan officer to avoid unexpected closing costs.

Denial of Rate Lock Extension Request Letter

A Denial of Rate Lock Extension Request Letter is a formal notice from a lender rejecting a borrower's plea to prolong a guaranteed interest rate. This typically occurs if the lock-in period expires due to processing delays or missed deadlines. Understanding the specific reason for denial is crucial, as it may force the borrower to accept current, potentially higher market rates. To minimize financial impact, borrowers should immediately review their contract for contingency clauses or negotiate new terms to prevent a significant increase in monthly mortgage payments.

Declined Mortgage Rate Lock Extension Letter

A Declined Mortgage Rate Lock Extension Letter notifies a borrower that their request to prolong a specific interest rate has been rejected. This typically occurs due to expired deadlines, changes in financial qualifications, or non-compliance with lender policies. When an extension is denied, the loan may revert to current market pricing, potentially increasing monthly payments. It is crucial to review the denial reason immediately and consult with your loan officer to discuss alternative options, such as relocking the rate at new terms or expediting the closing process.

Interest Rate Lock Extension Denial Letter

An Interest Rate Lock Extension Denial Letter notifies a borrower that their request to maintain a specific mortgage rate beyond the original expiration date has been rejected. This typically occurs due to missed deadlines, lack of required documentation, or the lender's internal policies. Consequently, the loan may revert to current market rates, potentially increasing monthly payments. It is crucial to review the stated reasons for denial immediately and consult with your loan officer to discuss relock options or potential appeals to protect your financing terms before closing.

Expired Rate Lock Period Denial Letter

An Expired Rate Lock Period Denial Letter informs a borrower that their specific interest rate guarantee has lapsed before the loan closed. This typically occurs due to processing delays or missing documentation. When the lock expires, the lender is no longer obligated to honor the original terms, often requiring a market rate reset or a costly extension fee. To protect your financing, it is crucial to monitor lock-in expiration dates closely and maintain frequent communication with your loan officer to ensure all underwriting requirements are met before the deadline.

Ineligible Rate Lock Extension Denial Letter

An Ineligible Rate Lock Extension Denial Letter is a formal notification from a lender stating that a borrower's request to prolong a guaranteed interest rate has been rejected. This typically occurs because the loan file no longer meets specific secondary market guidelines or internal policy requirements. Common reasons for denial include missed deadlines, significant changes in credit profiles, or the expiration of the maximum allowable extension period. Receiving this letter means the current rate may expire, potentially leading to higher monthly payments or a market float during the final closing stages.

Unapproved Loan Rate Lock Extension Letter

An Unapproved Loan Rate Lock Extension Letter is a critical notification from a lender stating that a request to prolong a current interest rate has been denied. This document typically highlights that the lock expiration date remains unchanged, potentially exposing the borrower to higher market rates if the loan fails to close on time. Understanding the specific denial reason is essential, as it may stem from processing delays or missing documentation. Borrowers must act quickly to renegotiate terms or finalize their mortgage before the existing rate commitment officially expires.

Final Decision Rate Lock Extension Denial Letter

Receiving a Final Decision Rate Lock Extension Denial Letter means your request to keep a specific interest rate beyond its original expiry has been rejected. This formal notice typically occurs due to missed deadlines, lack of required documentation, or shifts in lender policy. Since your rate is no longer protected, your loan will likely revert to current market pricing, potentially increasing your monthly payments. It is crucial to immediately contact your loan officer to discuss alternative options, such as a new rate lock or re-locking at prevailing interest rates.

Borrower Interest Rate Lock Extension Denial Letter

A Borrower Interest Rate Lock Extension Denial Letter is a formal notice stating that a lender will not prolong a guaranteed interest rate beyond its original expiration date. This occurs when delays in the mortgage process exceed the lock period and the lender determines the borrower or market conditions do not meet extension criteria. Consequently, the loan may revert to current market rates, potentially increasing monthly payments. Reviewing the denial reasons is crucial, as you may need to renegotiate terms or explore new financing options to finalize your home purchase.

Adverse Action Rate Lock Extension Denial Letter

An Adverse Action Rate Lock Extension Denial Letter is a formal notice issued when a lender refuses to prolong a guaranteed interest rate. This typically occurs due to creditworthiness changes, property appraisal issues, or expired documentation. It is legally required under the ECOA to explain the specific reasons for the rejection. Borrowers must review this document carefully to understand if financial instability or market shifts caused the denial, as it directly impacts the final loan terms and monthly mortgage payments before closing.

Standard Rate Lock Extension Denial Letter

A Standard Rate Lock Extension Denial Letter informs borrowers that their request to maintain a specific interest rate beyond the original expiration date has been rejected. This formal notice typically cites reasons such as expired deadlines, failure to meet contractual conditions, or shifts in market volatility. Once denied, the loan may revert to current market pricing, potentially increasing monthly payments. It is crucial to review the denial reason immediately and consult your loan officer to discuss floating the rate or exploring new lock-in options before closing.

What is a Rate Lock Extension Denial Letter?

A Rate Lock Extension Denial Letter is a formal notification from a mortgage lender informing the borrower that their request to extend the current interest rate guarantee has been rejected. This typically occurs when the original lock period expires before the loan closes and the lender determines the file no longer meets extension eligibility criteria.

Why was my request for a mortgage rate lock extension denied?

Common reasons for denial include the expiration of the maximum allowable lock duration, failure to meet secondary market guidelines, or the borrower's inability to provide necessary documentation within a specific timeframe. Lenders may also deny extensions if the delay is attributed to borrower negligence rather than administrative or third-party processing issues.

What happens to my interest rate after receiving a denial letter?

When a rate lock extension is denied, the original interest rate is no longer protected. The loan will typically revert to "prevailing market rates," which means your interest rate will be reset based on the current market pricing at the time of the new lock or the original worst-case pricing, depending on the lender's policy.

Can I appeal a Rate Lock Extension Denial?

Yes, borrowers can appeal a denial by providing evidence that the closing delay was caused by circumstances beyond their control, such as a lender error or a delay in third-party services like appraisals or inspections. You should submit a written rebuttal to your loan officer or the lender's lock desk for reconsideration.

Are there fees associated with a rate lock extension even if it is denied?

Generally, you are not charged an extension fee if the request is denied. However, if the lock expires and you choose to re-lock at current market rates, you may be subject to "re-lock fees" or higher pricing if market conditions have worsened since your initial application.

Comments