A Verification of Cash to Close Letter is a crucial document confirming that a homebuyer possesses the necessary funds to complete a real estate transaction. This proof ensures financial transparency and builds trust between lenders and sellers. Understanding how to draft this confirmation helps streamline the mortgage approval process. Below are some ready to use template options to get you started.

Image cover: Mastering the Cash to Close Verification Letter: Samples and Templates

Letter Samples List

- Standard Bank Verification Of Cash To Close Letter

- Family Gift Funds Verification Of Cash To Close Letter

- Earnest Money Deposit Verification Of Cash To Close Letter

- Retirement Liquidation Verification Of Cash To Close Letter

- Proceeds From Sale Verification Of Cash To Close Letter

- Employer Relocation Verification Of Cash To Close Letter

- Certified Public Accountant Verification Of Cash To Close Letter

- Investment Portfolio Verification Of Cash To Close Letter

- Trust Fund Disbursement Verification Of Cash To Close Letter

- Business Account Funds Verification Of Cash To Close Letter

- Spousal Joint Account Verification Of Cash To Close Letter

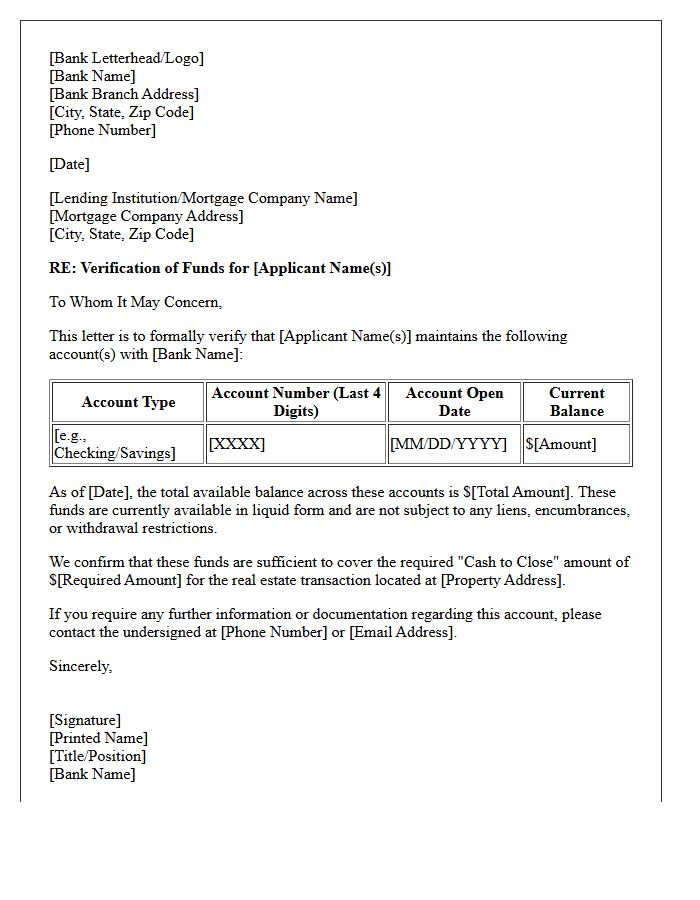

Standard Bank Verification Of Cash To Close Letter

A Standard Bank Verification of Cash to Close Letter is a critical document used in real estate transactions to confirm that a homebuyer possesses sufficient liquid funds to cover their down payment and closing costs. This official statement provides financial transparency to sellers and title companies, ensuring the buyer is capable of finalizing the purchase. Lenders issue this letter after verifying the account balance and source of wealth, making it a vital component for reaching a successful mortgage closing without unexpected delays or funding issues.

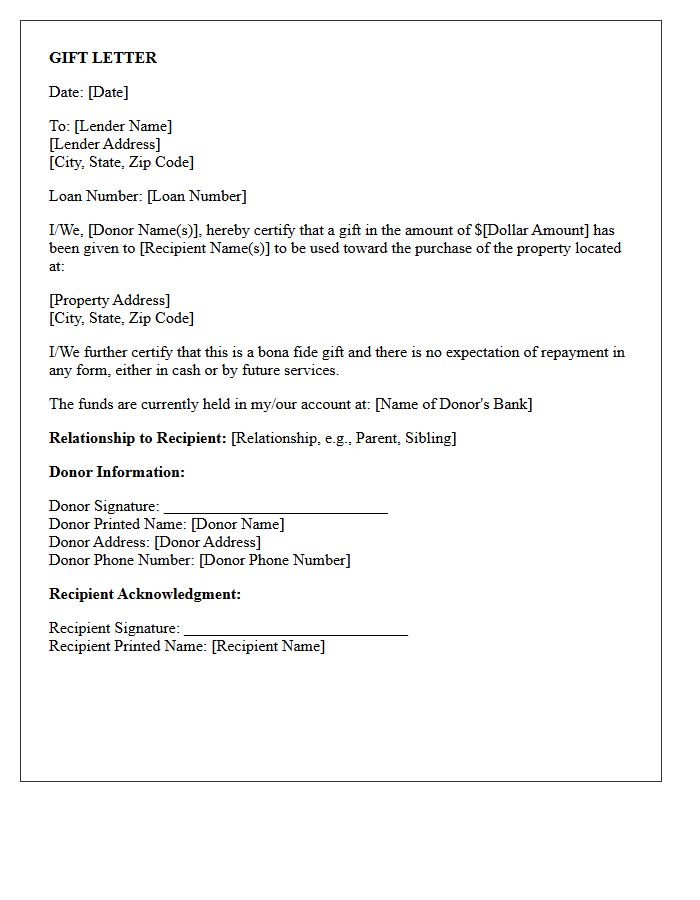

Family Gift Funds Verification Of Cash To Close Letter

A Family Gift Funds Verification Letter is a formal document confirming that money provided for a mortgage down payment is a bona fide gift, not a loan. Lenders require this to ensure the borrower has no additional repayment obligations. The letter must clearly state the donor's relationship, the specific dollar amount, and that no repayment is expected. Providing a clear paper trail through bank statements is essential to verify the legal transfer of equity, ensuring the cash to close meets strict regulatory and underwriting standards for final loan approval.

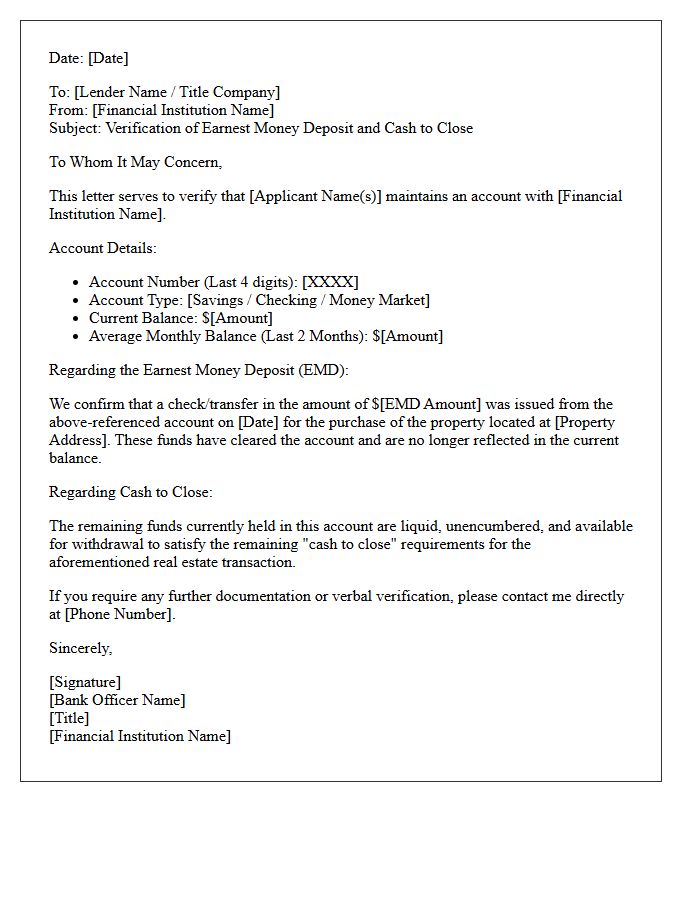

Earnest Money Deposit Verification Of Cash To Close Letter

An Earnest Money Deposit (EMD) proves a buyer's commitment to a real estate transaction. Lenders require a Verification of Cash to Close letter to confirm that the necessary funds for the down payment and closing costs are available and documented. This letter validates that the deposit has cleared the buyer's account and originated from an eligible source. Ensuring these funds are properly verified is a critical step in securing final mortgage approval and preventing delays during the underwriting process.

Retirement Liquidation Verification Of Cash To Close Letter

A Retirement Liquidation Verification letter is a critical document used in mortgage underwriting to prove a borrower has sufficient liquid assets for the cash to close. This letter confirms that funds held in 401(k) or IRA accounts are accessible and that the specific withdrawal amount has been initiated or received. Lenders require this verification to ensure the down payment and closing costs are sourced from verified retirement funds, maintaining compliance with federal lending standards and ensuring financial stability before the final loan approval.

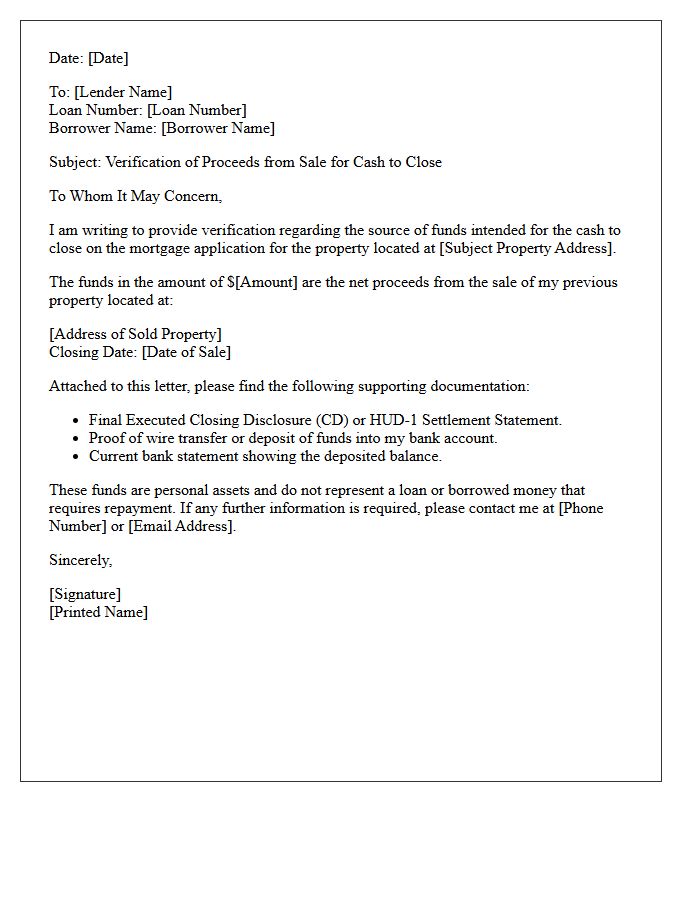

Proceeds From Sale Verification Of Cash To Close Letter

A Proceeds From Sale Verification is a critical document used to prove that the cash to close for a new home purchase originates from the equity of a previous property sale. Lenders require a signed Closing Disclosure or a Settlement Statement to verify these funds are available and legally sourced. This verification ensures the borrower meets the liquidity requirements for the mortgage. Without this paperwork, lenders cannot clear the loan for closing, as it confirms the verified funds are sufficient to cover the final down payment and transaction costs.

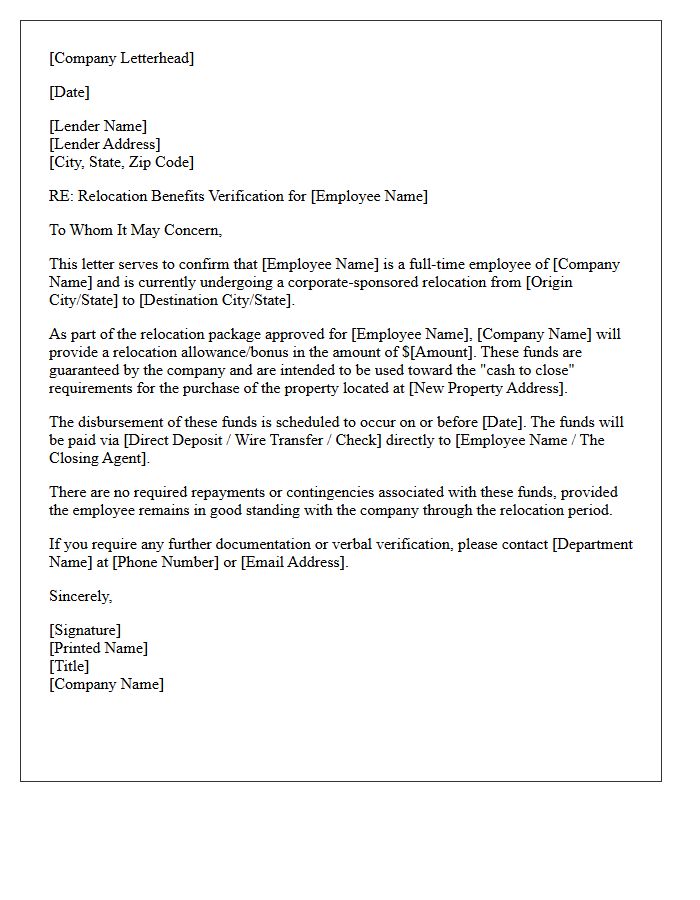

Employer Relocation Verification Of Cash To Close Letter

An Employer Relocation Verification Of Cash To Close Letter is a critical document used in mortgage underwriting to prove that a company is funding a transferee's closing costs or down payment. It verifies the exact benefit amount the employee will receive, ensuring the lender can document the source of funds without requiring traditional bank statements. This letter must clearly state the disbursement date and any specific conditions attached to the relocation package to satisfy lender compliance and debt-to-income requirements during the home buying process.

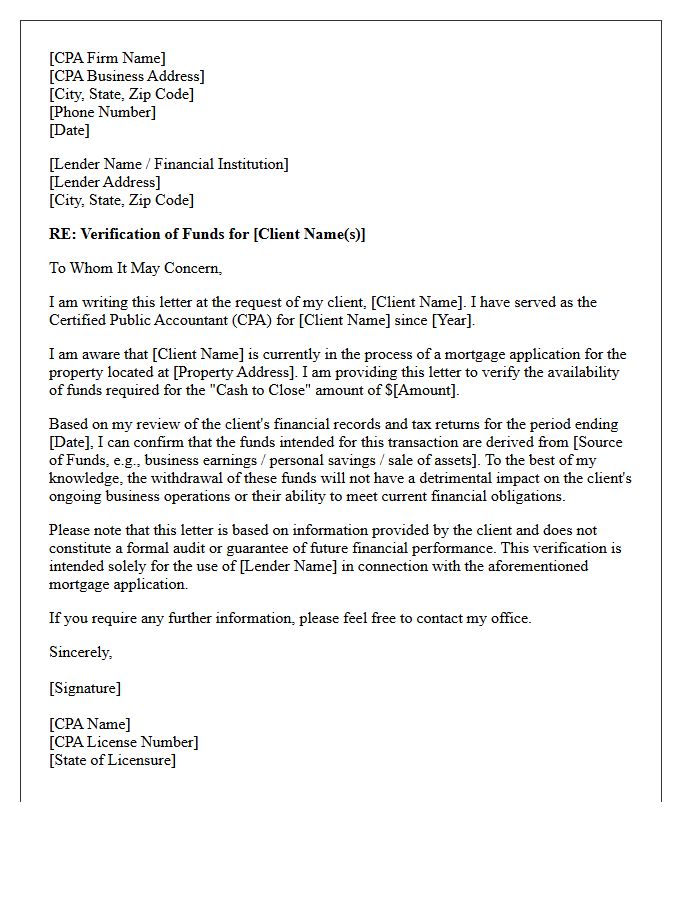

Certified Public Accountant Verification Of Cash To Close Letter

A Certified Public Accountant Verification of Cash to Close Letter serves as formal attestation regarding a homebuyer's available liquid assets. Lenders require this document to confirm that the funds designated for a mortgage down payment and closing costs are accessible and from legitimate sources. It is crucial to note that many CPAs are hesitant to sign these due to professional liability and strict AICPA guidelines regarding third-party verification. Borrowers should coordinate early with their financial professional to ensure the letter meets underwriting standards without violating accounting practice regulations.

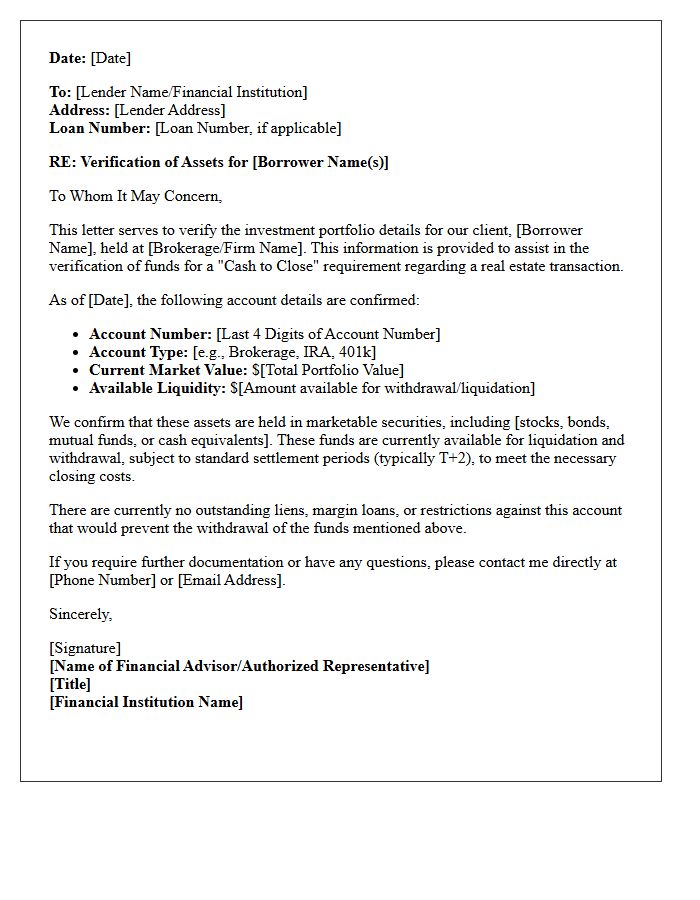

Investment Portfolio Verification Of Cash To Close Letter

An Investment Portfolio Verification Of Cash To Close Letter is a formal document proving a borrower possesses the liquid assets required to finalize a real estate transaction. Lenders use this to confirm that accessible funds, such as stocks or mutual funds, can cover the down payment and closing costs. This verification ensures financial stability and reduces lending risk. It is essential to ensure the valuation is current, as market fluctuations may affect the total liquidity available at the time of settlement.

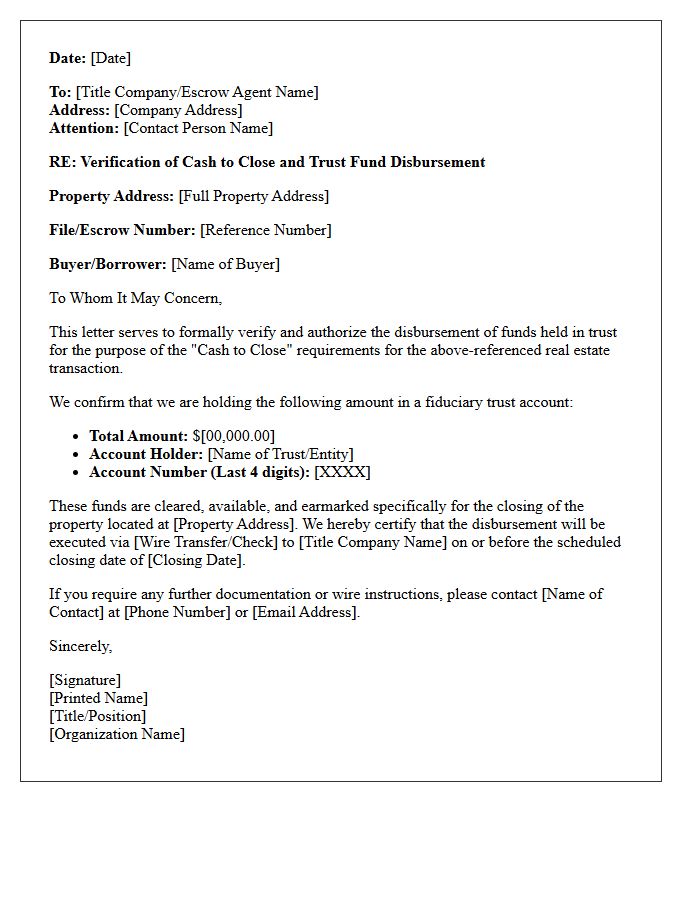

Trust Fund Disbursement Verification Of Cash To Close Letter

A Trust Fund Disbursement Verification of Cash to Close Letter is a critical document used in real estate to confirm that the buyer's required funds are secured and ready for transfer. This letter verifies that the specific amount needed to finalize the real estate transaction is held in a verified trust account. It prevents closing delays by providing lenders and title companies with formal proof of liquidity and availability. Ensuring the accuracy of this verification is essential for meeting contractual obligations and ensuring a seamless, legally compliant transfer of ownership.

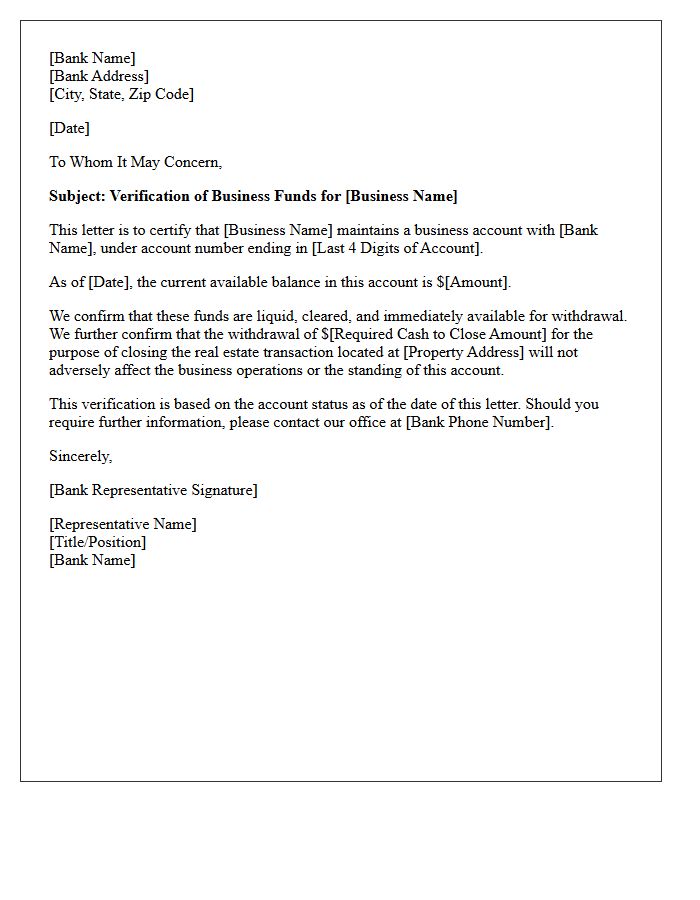

Business Account Funds Verification Of Cash To Close Letter

A Business Account Funds Verification letter confirms that a company possesses sufficient liquid assets for real estate transactions. Lenders require this document to ensure the Cash to Close is available and sourced from legitimate business operations. It typically validates the account balance, history, and the signer's authority to use corporate funds. Crucially, the letter must demonstrate that withdrawing these funds will not negatively impact the business's operational stability, ensuring the company remains solvent after the property acquisition is finalized.

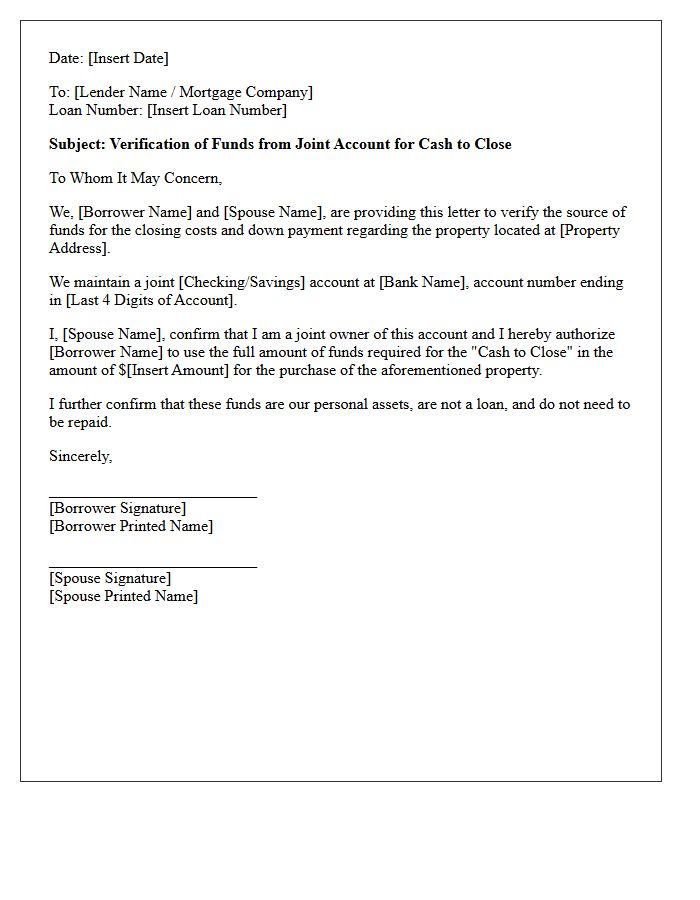

Spousal Joint Account Verification Of Cash To Close Letter

A spousal joint account verification of cash to close letter proves that mortgage funds are accessible and legitimate. When using a shared account, lenders require a signed statement from the non-borrowing spouse confirming the applicant has full permission to use the total balance for the home purchase. This document ensures transparency regarding the source of equity and prevents potential legal disputes over ownership. Providing this letter alongside recent bank statements streamlines the underwriting process by verifying that the necessary capital is seasoned and ready for the final real estate transaction.

What is a Verification of Cash to Close Letter?

A Verification of Cash to Close Letter is an official document issued by a financial institution confirming that a homebuyer has sufficient liquid funds available in their account to cover the down payment and closing costs required for a real estate transaction.

Who provides the Verification of Cash to Close Letter?

The letter is typically provided by the bank, credit union, or investment firm where the homebuyer's funds are held. It is usually requested by the mortgage lender or the title company during the final stages of the loan approval process.

What information is included in a Cash to Close verification document?

The document generally includes the account holder's name, the current balance of the account, the date the funds were verified, and a statement from the bank official confirming that the funds are seasoned and available for withdrawal.

Why do mortgage lenders require a Verification of Cash to Close Letter?

Lenders require this letter to mitigate risk by ensuring the borrower has the legal and financial capacity to finalize the purchase. It prevents last-minute financing collapses by verifying that the necessary cash is not dependent on unverified sources or pending loans.

Is a standard bank statement the same as a Verification of Cash to Close Letter?

No. While a bank statement shows historical transactions, a Verification of Cash to Close Letter is a formal, real-time attestation from a bank representative specifically intended for the mortgage underwriter to satisfy final funding conditions.

Comments