A Verification of Closing Costs Payment Letter serves as formal proof that a homebuyer has sufficient funds to cover final settlement fees. This essential document provides lenders and title companies with necessary financial transparency to ensure a smooth real estate transaction. It confirms your readiness to finalize the mortgage process. Below are some ready to use templates.

Image cover: Official Proof of Closing Costs Payment: Templates and Verified Letter Samples

Letter Samples List

- Verification Of Closing Costs Payment Letter

- Proof Of Funds Verification Letter

- Gift Funds Source Verification Letter

- Earnest Money Deposit Confirmation Letter

- Cash To Close Verification Letter

- Down Payment Source Verification Letter

- Final Closing Disclosure Approval Letter

- Escrow Account Funding Verification Letter

- Wire Transfer Confirmation Letter

- Mortgage Payoff Verification Letter

- Payment Of Closing Fees Confirmation Letter

- Third Party Closing Costs Verification Letter

- Lender Closing Instructions Letter

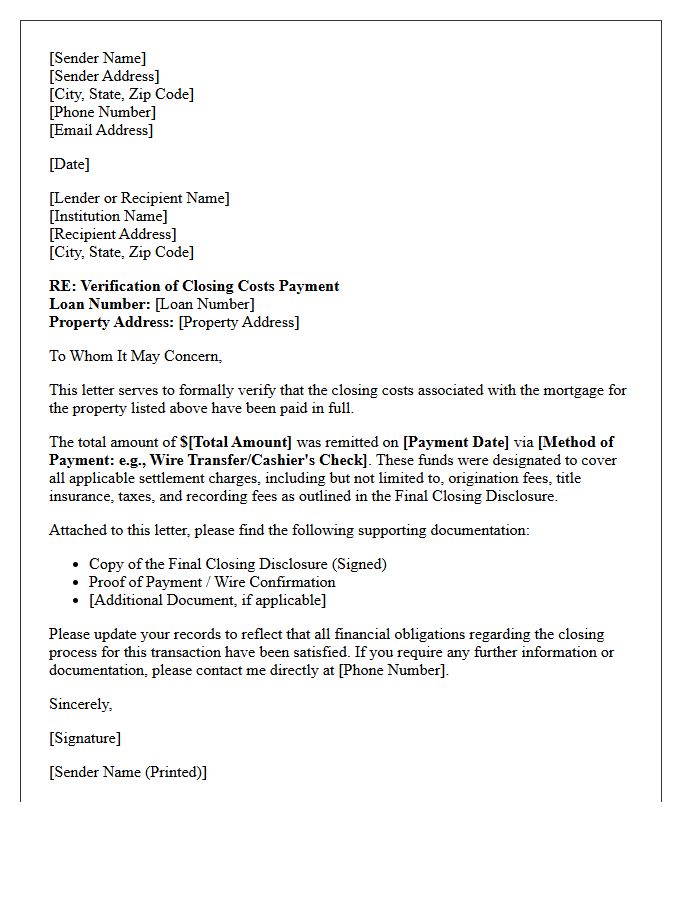

Verification Of Closing Costs Payment Letter

A Verification of Closing Costs Payment Letter is a formal document confirming that a homebuyer possesses the liquid assets necessary to cover final transaction fees. Lenders require this proof to ensure the borrower can afford down payments and administrative costs without incurring new debt. Typically issued by a financial institution, it validates current account balances and source of funds. Providing this letter is a critical step in securing mortgage approval, as it mitigates financial risk and ensures a transparent, successful property transfer during the final settlement process.

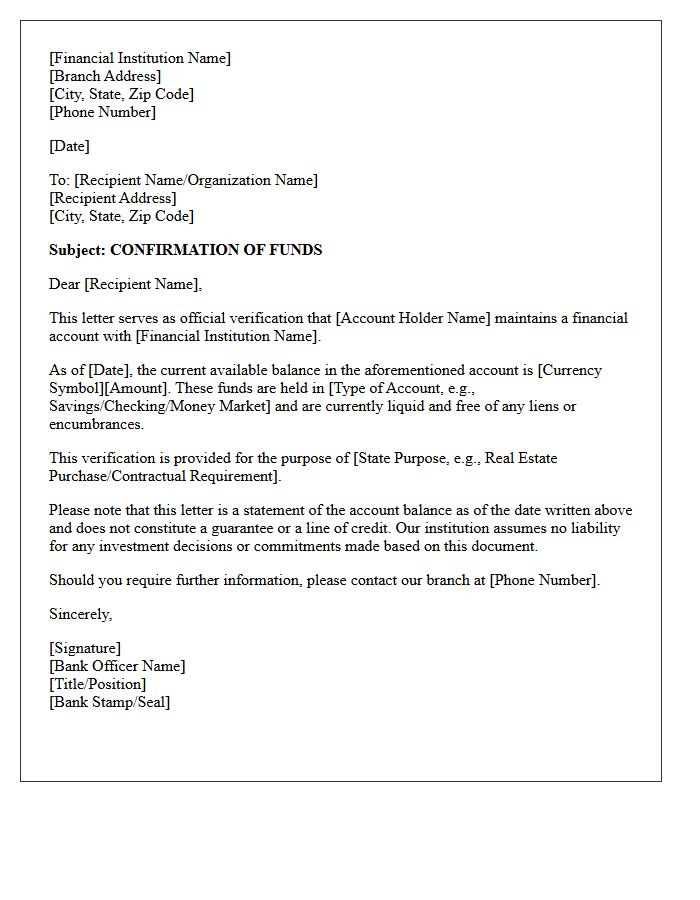

Proof Of Funds Verification Letter

A Proof of Funds (POF) verification letter is a critical document issued by a financial institution confirming a buyer has sufficient liquid assets to complete a transaction. It ensures the seller that the capital is readily available and legitimate. Common in real estate and high-value trade, this letter typically includes the account holder's name, the specific balance, and a banker's signature. Providing a POF builds credibility and strengthens your negotiating position by proving you possess the financial capacity to finalize the deal without delays.

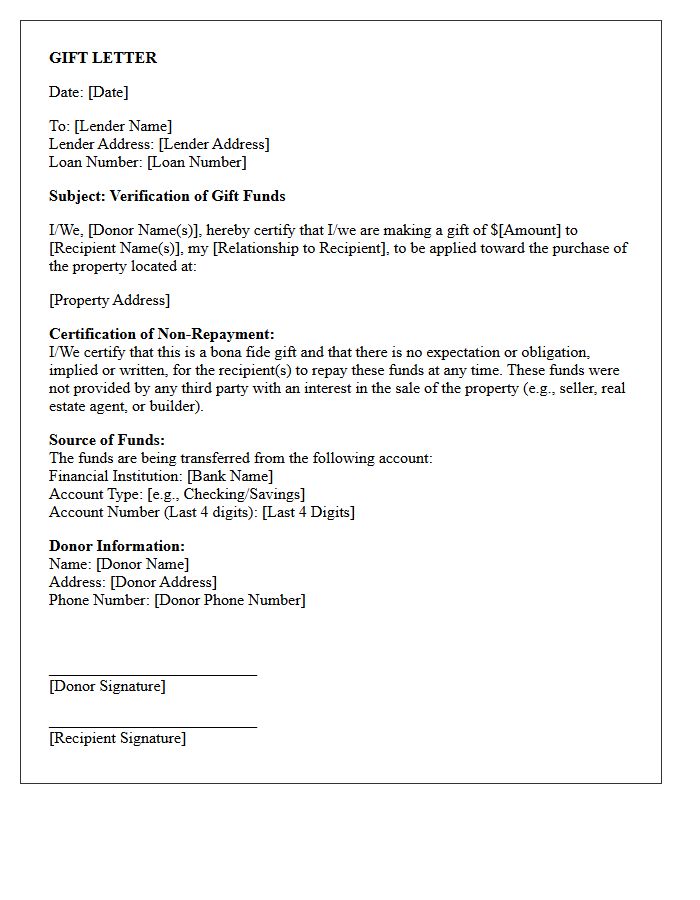

Gift Funds Source Verification Letter

A Gift Funds Source Verification Letter is a legal document used during mortgage underwriting to confirm that down payment assistance is a genuine gift rather than a loan. Lenders require this to ensure the donor has the financial capacity to provide the funds without expecting repayment. The letter must clearly state the relationship between parties, the exact amount, and include a certified statement that no debt is created. Verifying the source of funds is essential for compliance with anti-money laundering regulations and establishing the borrower's true debt-to-income ratio.

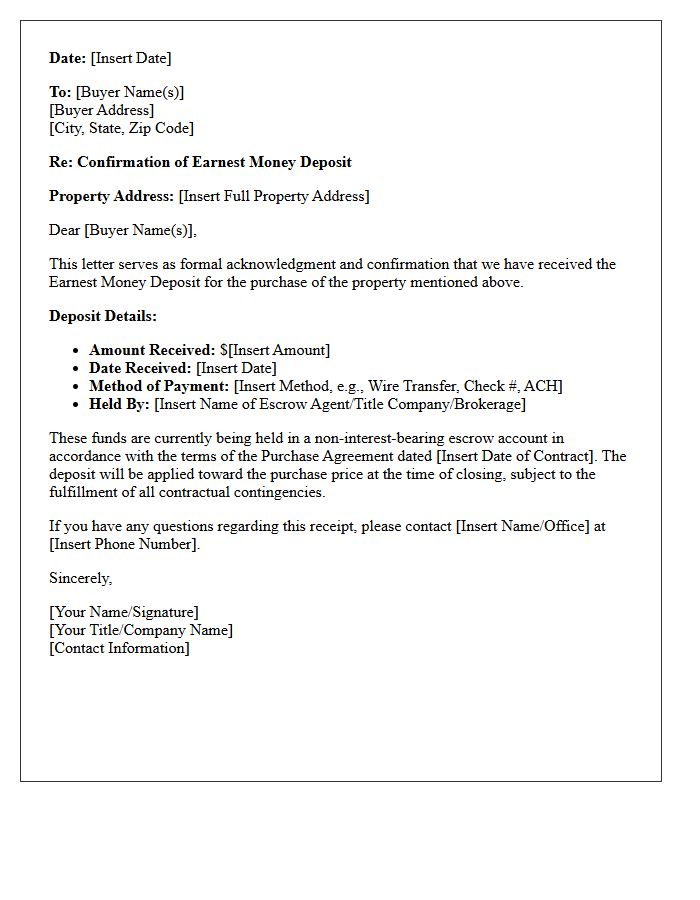

Earnest Money Deposit Confirmation Letter

An Earnest Money Deposit Confirmation Letter serves as official proof that a buyer has submitted funds to secure a real estate contract. This document, typically issued by an escrow agent or attorney, verifies the receipt of funds and ensures the buyer is acting in good faith. It protects both parties by documenting the deposit amount, date, and holding entity. Having this verification is a critical milestone in the mortgage approval process, as lenders require it to confirm the source and availability of the down payment.

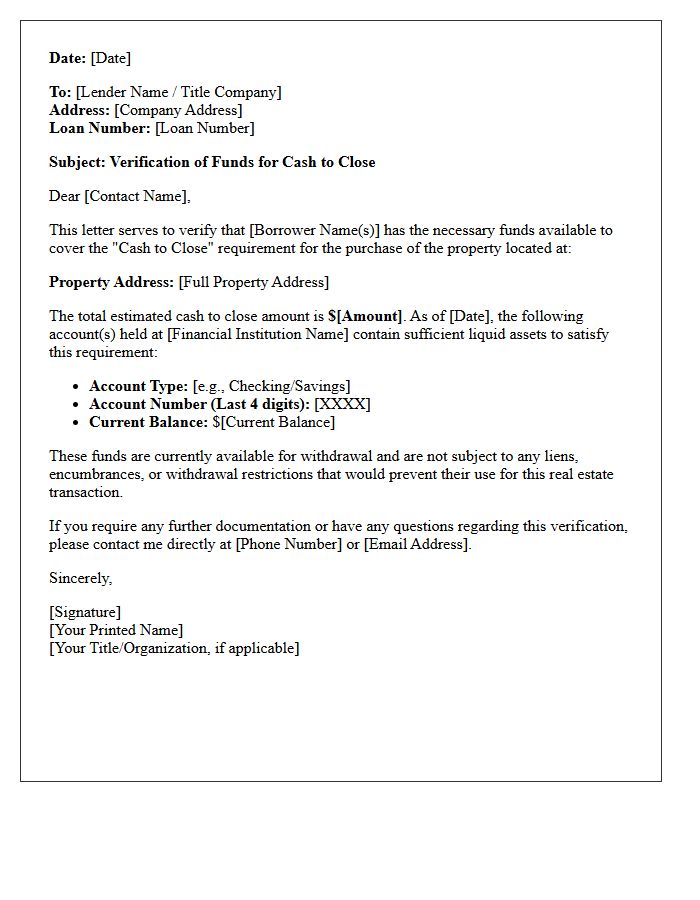

Cash To Close Verification Letter

A Cash to Close Verification Letter is a vital document confirming a homebuyer possesses the liquid assets required to finalize a real estate transaction. It validates that funds for the down payment and closing costs are readily available in a verified bank account. Lenders and title companies use this to prevent financing delays and ensure financial transparency. Providing this proof of funds early streamlines the mortgage approval process, demonstrating the buyer's serious intent and financial stability before the final signing stage of the home purchase.

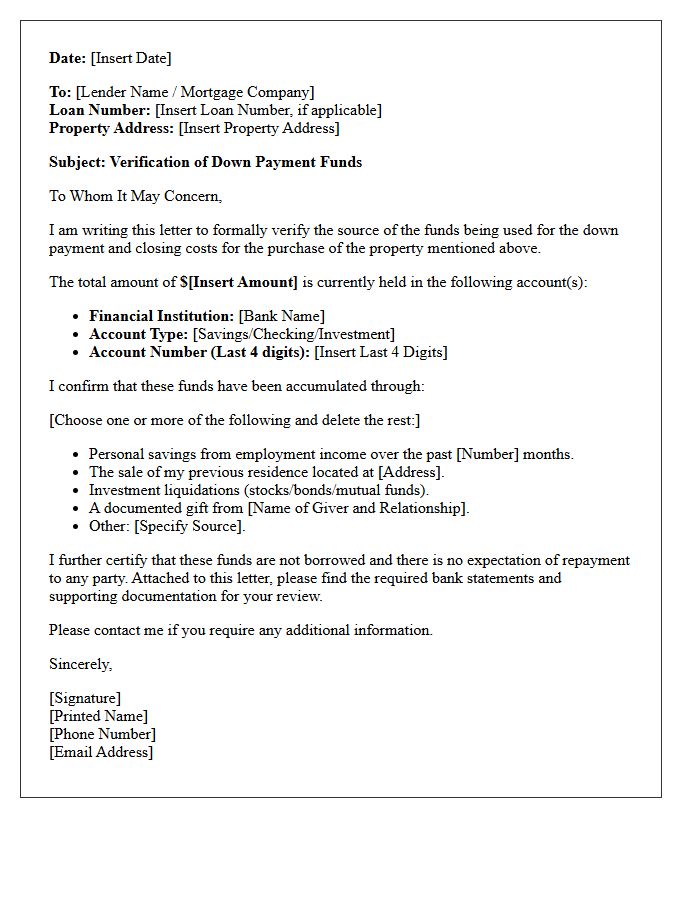

Down Payment Source Verification Letter

A Down Payment Source Verification Letter is a formal document proving the origin of your funds to mortgage lenders. This letter ensures compliance with anti-money laundering laws and confirms that the money is not a new undisclosed loan. Lenders require this to verify your financial stability and the legitimacy of your assets. Common documentation includes bank statements, gift letters, or investment liquidation records. Providing a clear, documented history of your down payment prevents delays and is essential for securing mortgage approval during the home-buying process.

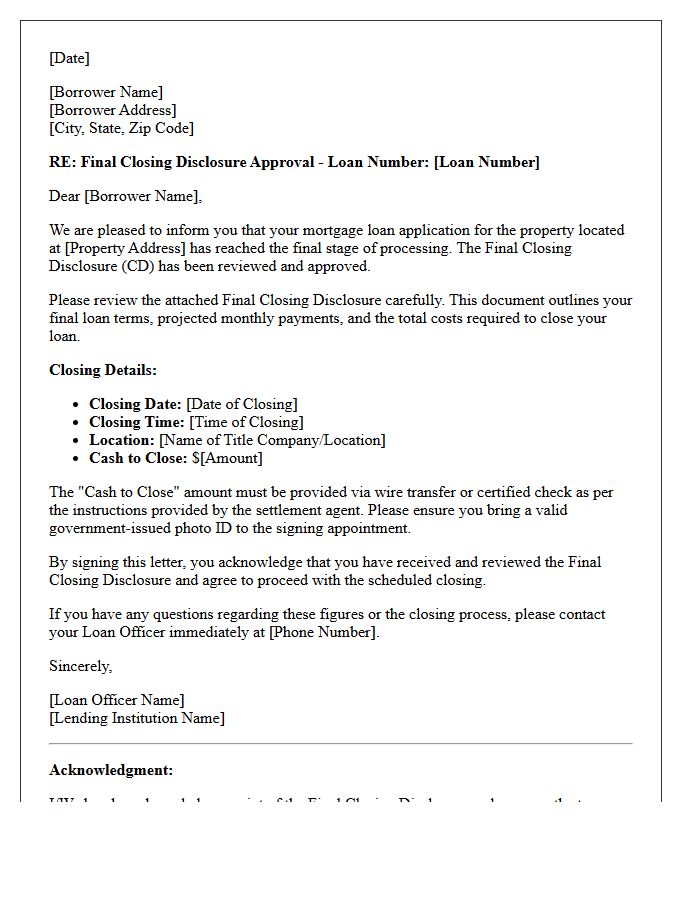

Final Closing Disclosure Approval Letter

The Final Closing Disclosure Approval Letter is a critical document issued by your lender once your mortgage reaches the "clear to close" stage. It provides a detailed breakdown of your loan's final terms, including interest rates, monthly payments, and total closing costs. Borrowers must review and sign this disclosure at least three business days before settlement to comply with federal regulations. This cooling-off period ensures you have sufficient time to compare the final figures against your initial Loan Estimate and confirm that all financial obligations are accurate before signing the deed.

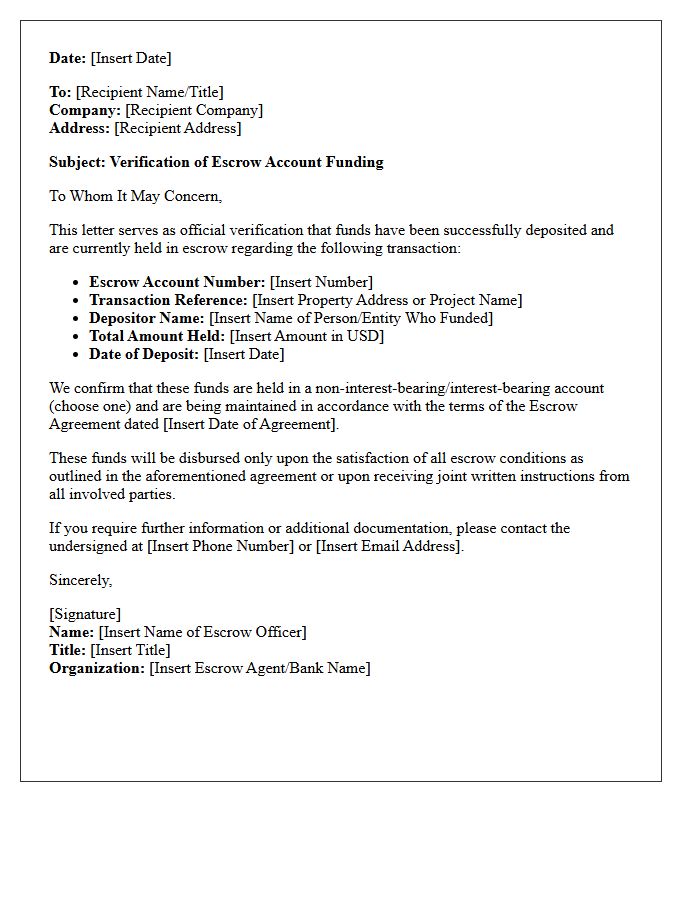

Escrow Account Funding Verification Letter

An Escrow Account Funding Verification Letter is a formal document issued by a financial institution confirming that specific liquid assets are secured for a transaction. It provides legal assurance to sellers or contractors that the necessary capital is already deposited and held by a neutral third party. This letter minimizes financial risk by verifying proof of funds and ensuring that payment is guaranteed once contractual obligations are met. It is an essential component for closing high-value real estate deals or complex business acquisitions where financial transparency is required to establish trust.

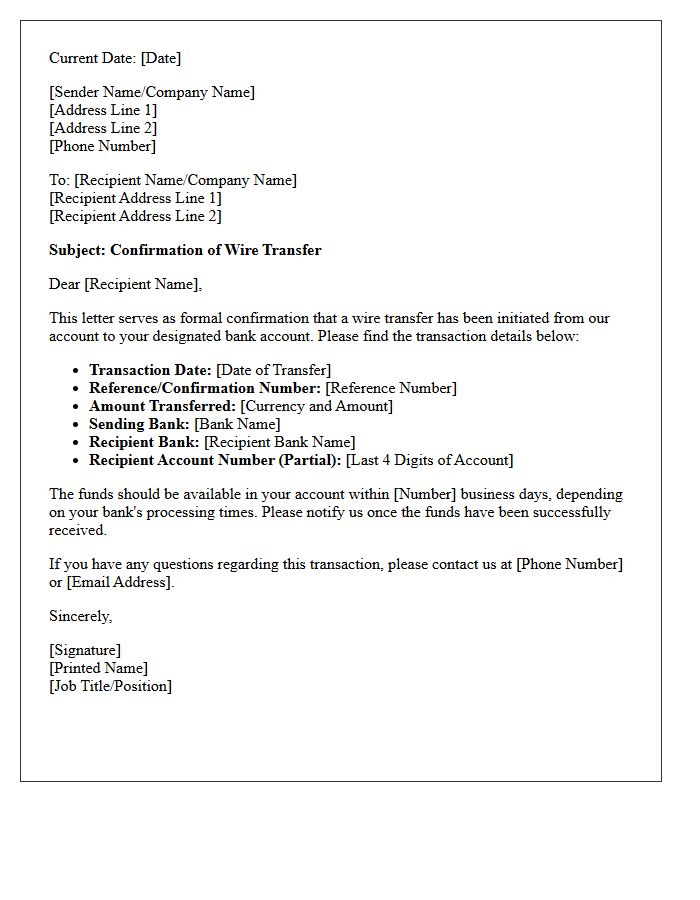

Wire Transfer Confirmation Letter

A Wire Transfer Confirmation Letter serves as official proof that a financial transaction was successfully executed. This document verifies critical details, including the IMAD/OMAD sequence numbers, transaction date, and the total amount sent. It acts as a vital receipt for tracking funds between institutions and resolving potential payment disputes. For businesses and individuals, maintaining this record ensures accountability and provides legal evidence that the sender has fulfilled their payment obligation through the banking system. Always verify the Federal Reference Number to track the real-time status of your transfer.

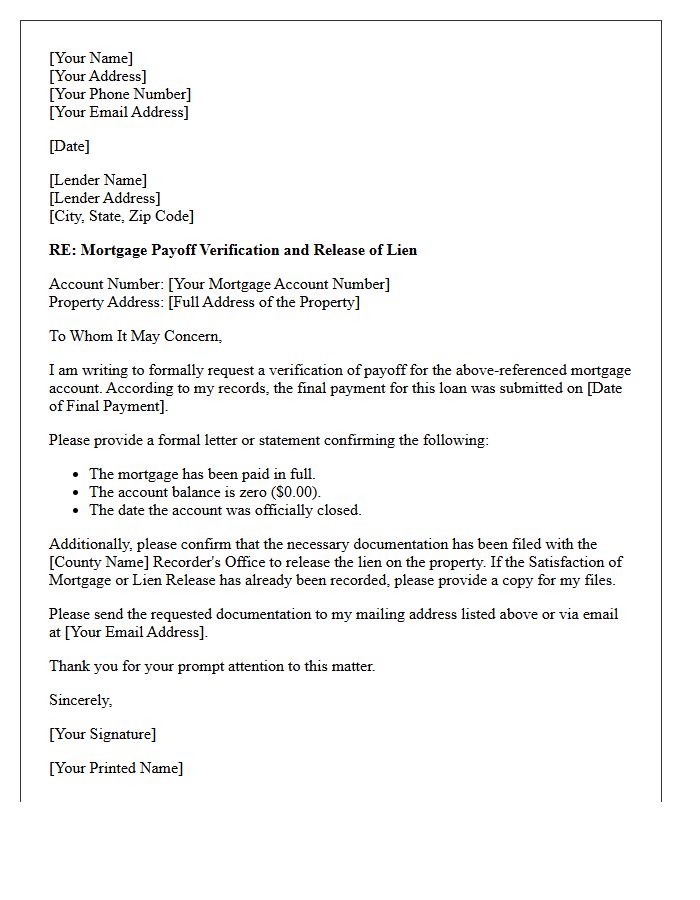

Mortgage Payoff Verification Letter

A Mortgage Payoff Verification Letter is an official document from your lender stating the exact amount required to fully satisfy your loan. Unlike a monthly statement, it includes the principal balance plus accrued interest and administrative fees calculated to a specific date. This letter is essential during a home sale or refinancing to ensure the lien is properly released. Always verify the good-through date to avoid underpayment penalties, as daily interest charges will change the total amount due after that window expires.

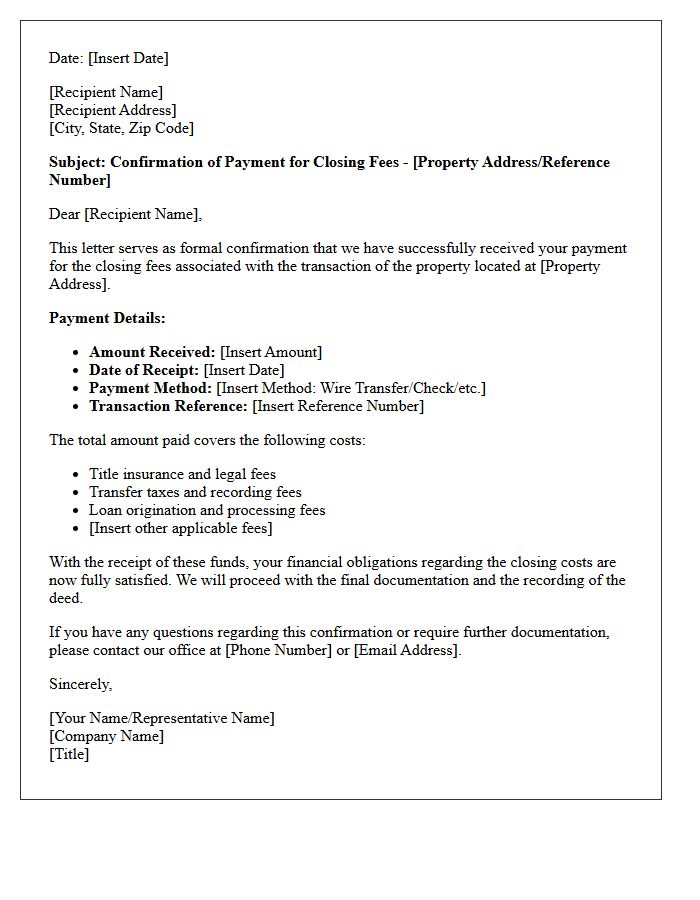

Payment Of Closing Fees Confirmation Letter

A Payment of Closing Fees Confirmation Letter is a legal document verifying that all real estate transaction costs have been settled. It serves as official proof of payment for items like attorney fees, taxes, and commissions. This letter is essential for ensuring a clear transfer of title and protecting both parties from future financial disputes. Homebuyers should retain this receipt as permanent evidence that their closing obligations were met in full, facilitating a smooth finalization of the property sale.

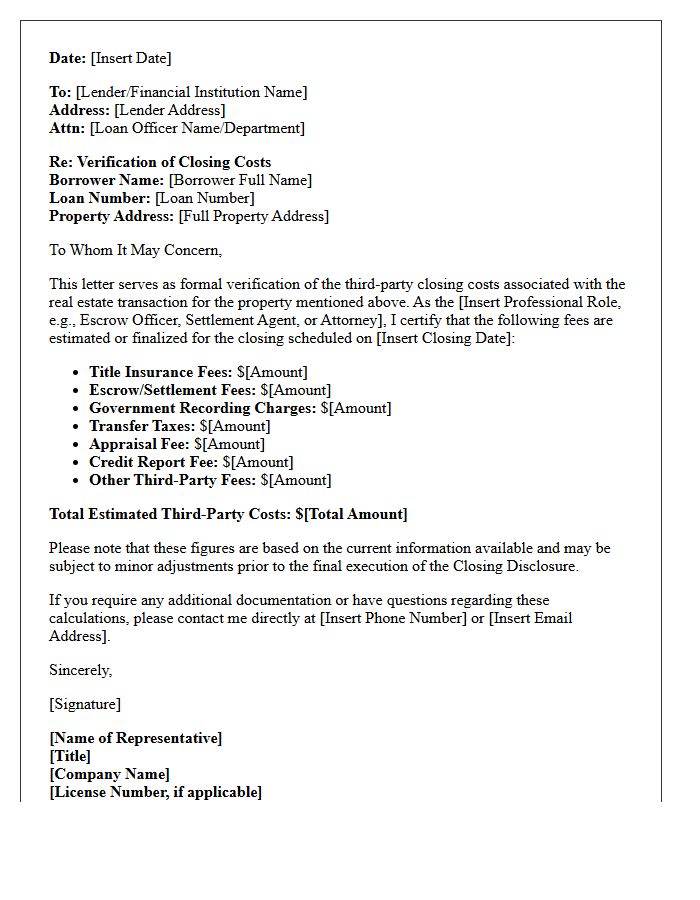

Third Party Closing Costs Verification Letter

A Third Party Closing Costs Verification Letter is a formal document confirming that an external entity will cover specific settlement charges. This letter ensures the lender that guaranteed funds are available to satisfy financial obligations at closing. It typically outlines the exact dollar amount and identifies the responsible party, such as a non-profit agency or government program. Providing this verification is crucial for loan approval, as it validates the borrower's ability to meet required costs without incurring additional undisclosed debt.

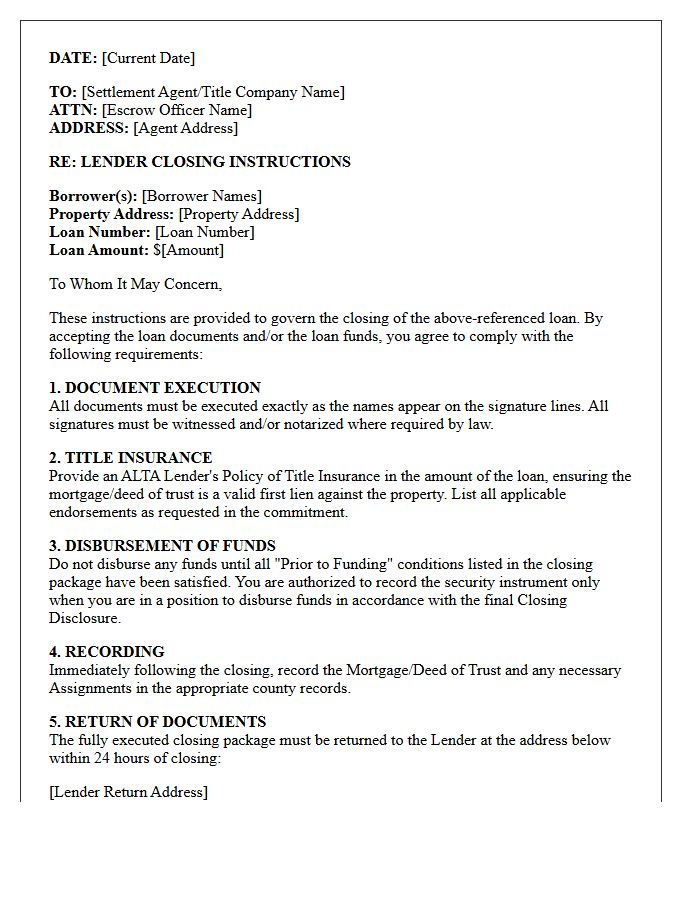

Lender Closing Instructions Letter

A Lender Closing Instructions Letter is a mandatory legal document sent to the settlement agent detailing exactly how to execute the mortgage. It outlines specific conditions for funding authorization, required signatures, and the disbursement of loan proceeds. Following these mandates is critical to ensure the enforceability of the security instrument and compliance with federal regulations. Any deviation from these instructions can delay the home purchase or prevent the loan from closing, making it the essential roadmap for a successful real estate settlement process.

What is a Verification of Closing Costs Payment Letter?

A Verification of Closing Costs Payment Letter is an official document or bank statement provided by a homebuyer to prove they have the liquid funds available to cover all one-time fees required to finalize a real estate transaction.

Who provides the proof of funds for closing costs?

The homebuyer typically provides this verification by obtaining a formal letter from their financial institution or by submitting recent certified bank statements that show a balance exceeding the estimated "cash to close" amount.

Why do lenders require a closing cost verification letter?

Lenders require this documentation to ensure the borrower can afford the down payment and settlement fees without incurring additional debt, which confirms the borrower's financial stability before the loan is funded.

Does a Verification of Closing Costs Letter include the down payment?

Yes, the verification usually covers the total "cash to close" requirement, which includes the down payment, loan origination fees, title insurance, appraisal fees, and any prepaid taxes or homeowner's insurance premiums.

When should I submit my verification of funds for closing?

This verification is typically required during the initial mortgage underwriting process and is often updated or re-verified 24 to 72 hours before the scheduled closing date to ensure the funds are still available.

Comments