A Notice of Acceleration is a formal legal demand issued by a lender when a borrower defaults on their mortgage or loan agreement. This document declares the entire remaining balance due immediately, effectively ending the installment payment plan. Understanding this critical step in the foreclosure process is essential for protecting your rights. To assist you, below are some ready to use templates.

Image cover: Notice of Acceleration: Official Demand for Full Loan Repayment Templates

Letter Samples List

- Notice Of Acceleration Of Commercial Loan Balance Letter

- Residential Mortgage Default And Acceleration Letter

- Auto Loan Balance Acceleration Demand Letter

- Pre-Foreclosure Loan Balance Acceleration Letter

- Unsecured Personal Loan Acceleration Notice Letter

- Small Business Loan Default Acceleration Letter

- Revolving Credit Facility Acceleration Letter

- Construction Loan Balance Acceleration Letter

- Guarantor Notice Of Loan Balance Acceleration Letter

- Post-Cure Period Loan Balance Acceleration Letter

- Commercial Real Estate Loan Acceleration Letter

- Business Line Of Credit Balance Acceleration Letter

- Promissory Note Breach And Acceleration Letter

Notice Of Acceleration Of Commercial Loan Balance Letter

A Notice of Acceleration is a critical legal document informing a borrower that the entire unpaid commercial loan balance is due immediately. This typically occurs after a material default, such as missing payments or breaching covenants. Once the lender invokes the acceleration clause, you lose the right to pay in monthly installments. It is the final step before the lender initiates foreclosure or legal action to seize collateral. If you receive this letter, you must act quickly to negotiate a workout or risk losing your business assets.

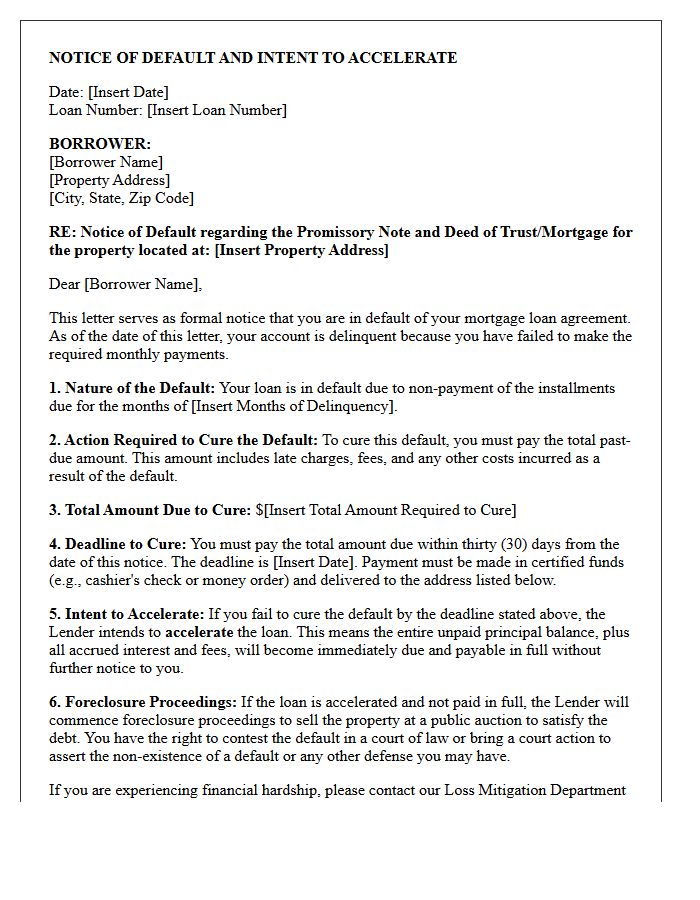

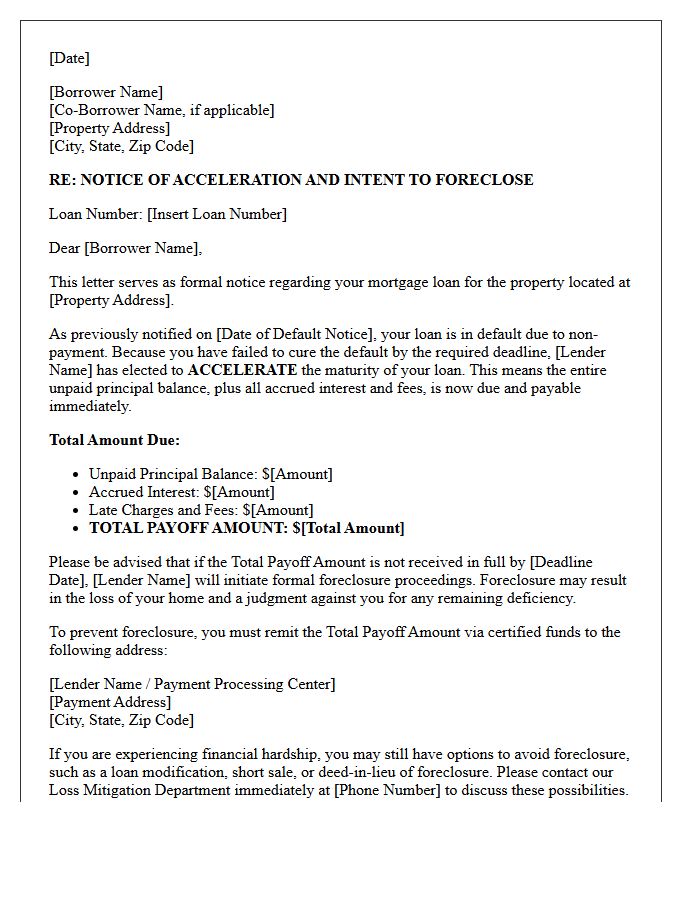

Residential Mortgage Default And Acceleration Letter

A residential mortgage default occurs when a borrower misses payments, violating the loan agreement. To begin the legal foreclosure process, lenders must send a formal Acceleration Letter. This critical notice informs the borrower of the breach of contract and provides a specific window, typically thirty days, to cure the default. Failure to pay the total outstanding amount requested will cause the lender to accelerate the debt, making the entire loan balance due immediately. Timely action after receiving this letter is essential to prevent the loss of the property through foreclosure.

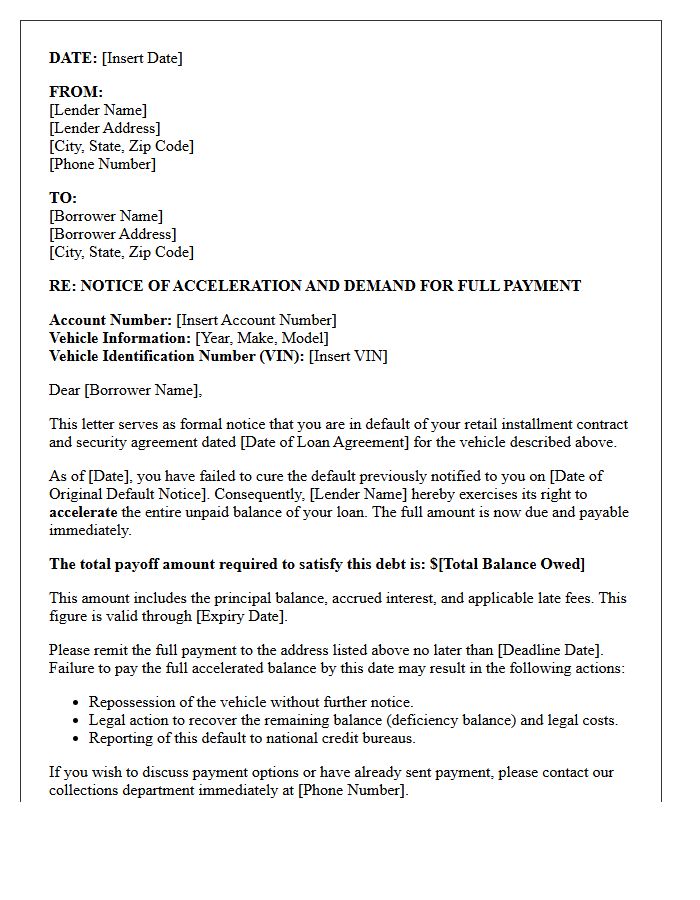

Auto Loan Balance Acceleration Demand Letter

An Auto Loan Balance Acceleration Demand Letter is a formal legal notice from a lender requiring immediate payment of the entire remaining loan balance. This typically occurs after a borrower defaults on payments or violates contract terms. Receiving this letter means the acceleration clause has been triggered, ending the installment plan and often serving as the final warning before vehicle repossession. It is critical to contact the creditor immediately to discuss reinstatement options, refinancing, or a lump-sum settlement to avoid the loss of the asset and severe credit damage.

Pre-Foreclosure Loan Balance Acceleration Letter

A Pre-Foreclosure Loan Balance Acceleration Letter is a formal notice from a lender demanding immediate payment of the entire remaining mortgage balance. This legal step occurs after multiple missed payments, signaling that the bank is terminating the installment plan due to default. Receiving this letter is critical because it is the final warning before the formal foreclosure process begins. To avoid losing the property, homeowners must quickly explore loss mitigation options, such as loan modification or reinstatement, to stop the acceleration of the debt and prevent a forced sale.

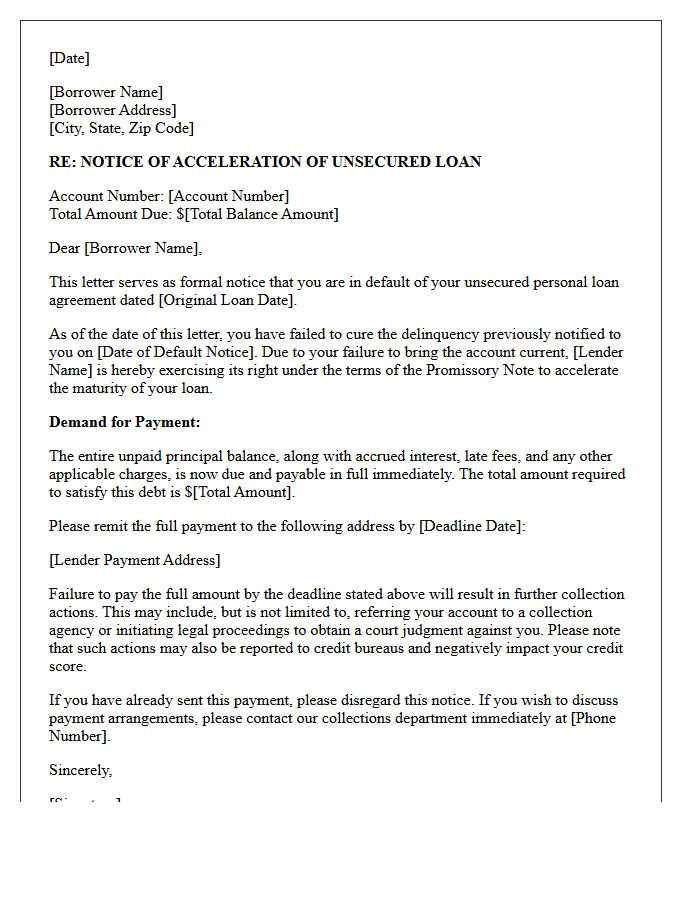

Unsecured Personal Loan Acceleration Notice Letter

An Unsecured Personal Loan Acceleration Notice Letter is a critical legal warning issued when a borrower defaults on payments. It signifies that the lender has triggered an acceleration clause, demanding immediate full repayment of the remaining balance rather than monthly installments. Receiving this notice indicates that the grace period has ended and the entire debt is due. To avoid severe credit damage or legal action, borrowers should contact their creditor immediately to negotiate a settlement or structured repayment plan before the account is transferred to collections.

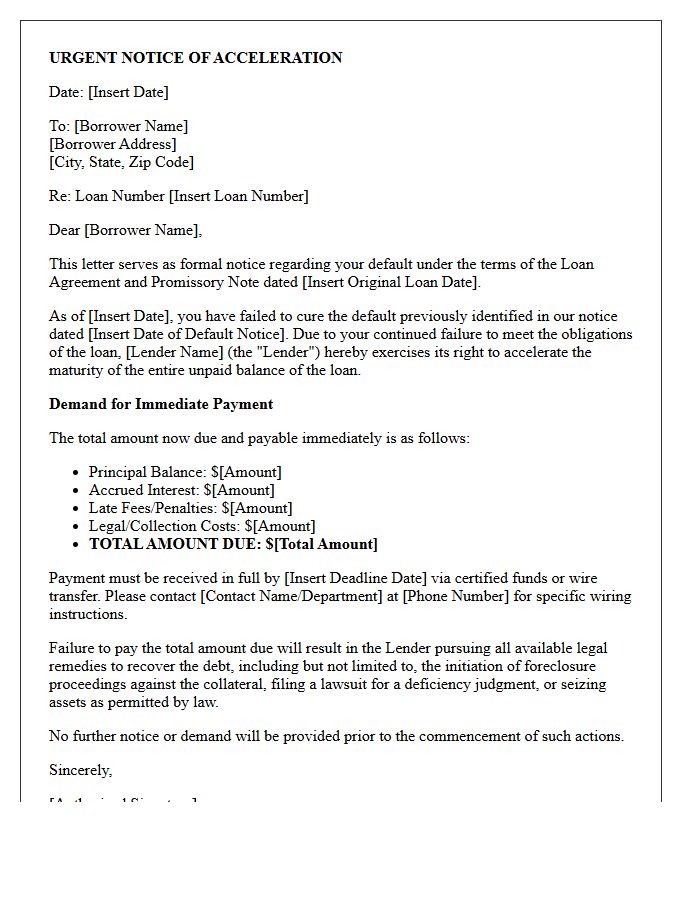

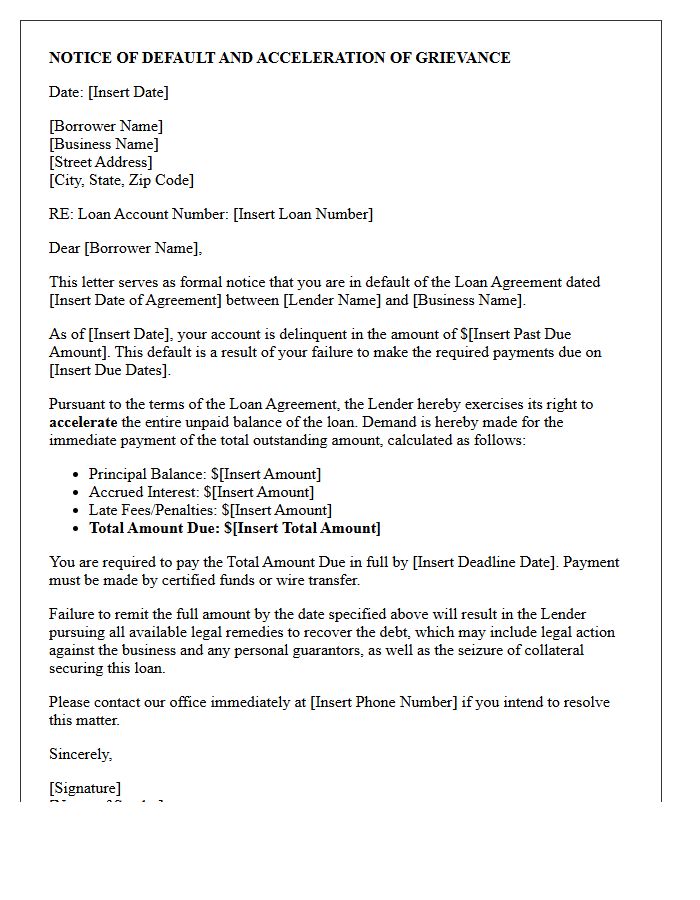

Small Business Loan Default Acceleration Letter

A Small Business Loan Default Acceleration Letter is a formal legal notice issued by a lender when a borrower breaches their contract. This document signifies that the grace period has ended and the entire loan balance is now due immediately, rather than in monthly installments. Receiving this acceleration notice is a critical warning; failure to settle the full amount or negotiate a workout plan typically leads to asset seizure, foreclosure, or legal action against personal guarantees. Prompt communication with the lender is essential to prevent permanent financial loss or business closure.

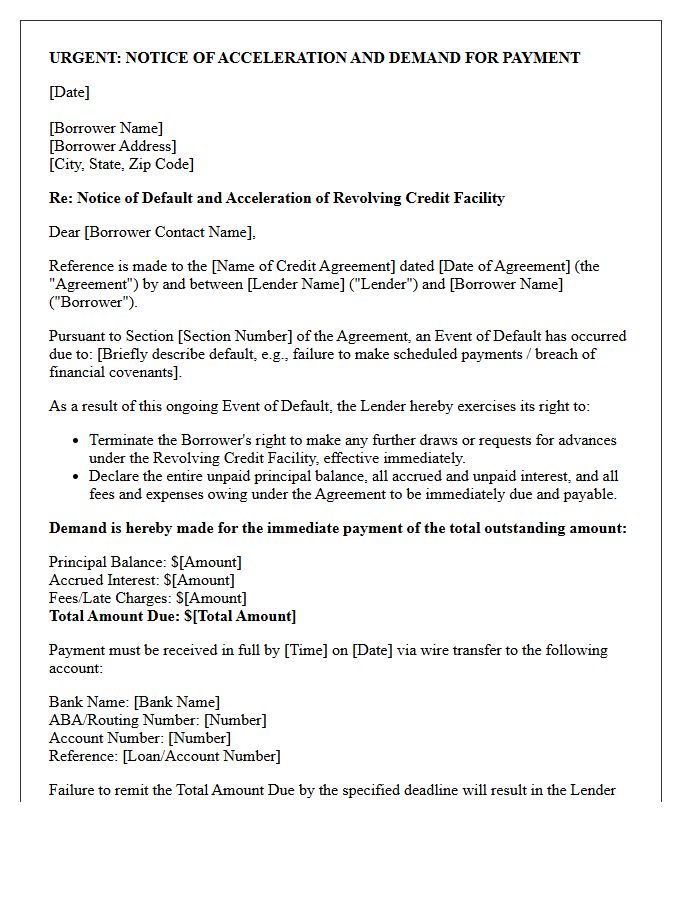

Revolving Credit Facility Acceleration Letter

A Revolving Credit Facility Acceleration Letter is a formal legal notice issued by a lender demanding immediate repayment of the entire outstanding balance. This action typically occurs after a borrower commits a Event of Default, such as missing payments or breaching financial covenants. Once accelerated, the borrower loses the ability to draw further funds, and the full debt becomes due instantly. It is a critical warning signal that often precedes foreclosure or legal litigation, requiring urgent communication between the debtor and financial institutions to negotiate a potential waiver or restructuring plan.

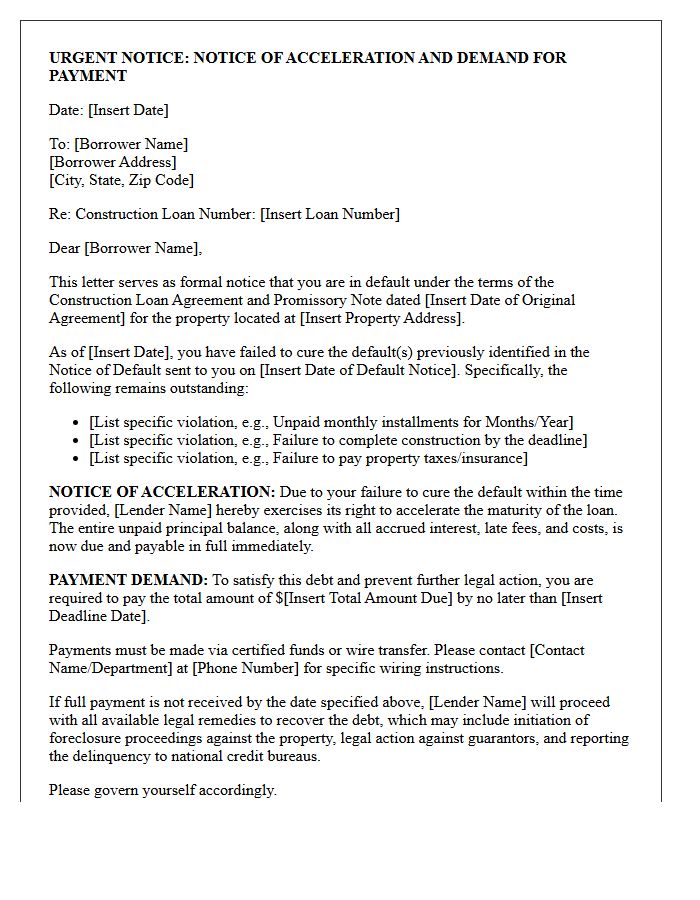

Construction Loan Balance Acceleration Letter

A Construction Loan Balance Acceleration Letter is a formal legal notice issued by a lender when a borrower defaults on their loan agreement. This critical document demands the immediate repayment of the entire outstanding principal and interest. It typically occurs due to missed payments, breach of contract, or failure to meet project milestones. Receiving this letter indicates that the lender has revoked the installment plan and may initiate foreclosure proceedings. Borrowers must act quickly to rectify defaults or negotiate terms to prevent the total loss of the property and investment.

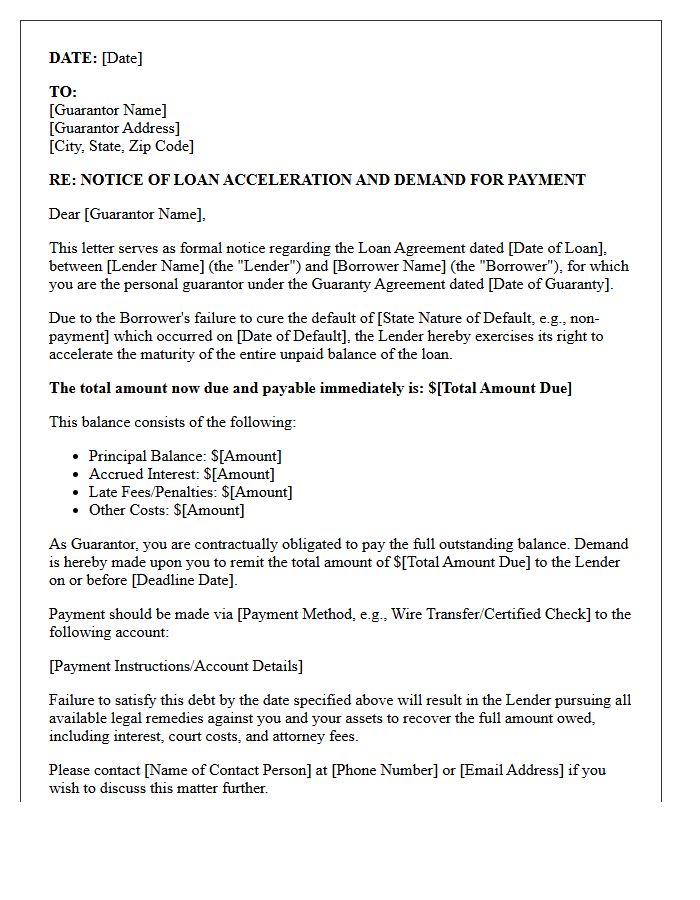

Guarantor Notice Of Loan Balance Acceleration Letter

A Guarantor Notice of Loan Balance Acceleration is a critical legal document informing a cosigner that the full debt is now due immediately. This occurs after a borrower defaults, triggering an acceleration clause that cancels the installment plan. As a guarantor, you are legally responsible for the entire outstanding balance, including accrued interest and late fees. Receiving this letter serves as a final warning before the lender initiates legal action or collection proceedings against your personal assets to satisfy the obligation.

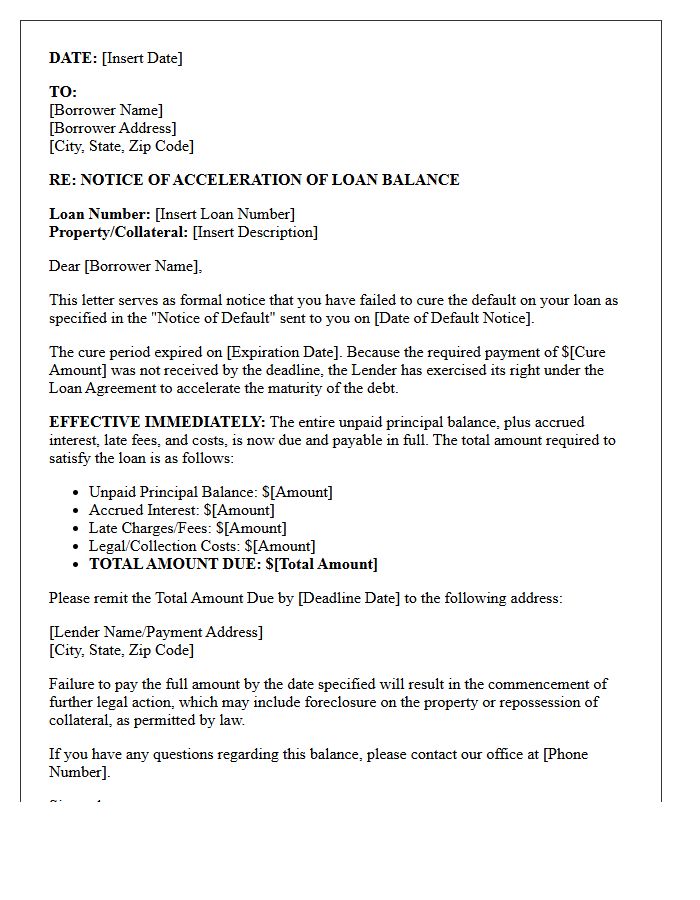

Post-Cure Period Loan Balance Acceleration Letter

A Post-Cure Period Loan Balance Acceleration Letter is a formal legal notice sent by a lender when a borrower fails to resolve a default within the allotted timeframe. This document signifies that the full loan balance is now due immediately, effectively terminating the installment payment plan. It serves as a final warning before the lender initiates formal foreclosure or debt collection lawsuits. Receiving this letter indicates that the grace period has expired, and the creditor is exercising their right to demand total repayment of the outstanding debt plus interest.

Commercial Real Estate Loan Acceleration Letter

A Commercial Real Estate Loan Acceleration Letter is a formal legal notice issued by a lender when a borrower defaults on their mortgage contract. This document signifies that the full outstanding balance of the loan is now due immediately, rather than following the original payment schedule. Receiving this letter is a critical warning that the lender intends to initiate foreclosure proceedings unless the default is cured promptly. It effectively terminates the borrower's right to pay in installments, making it essential to seek legal counsel or restructuring options instantly to protect the asset.

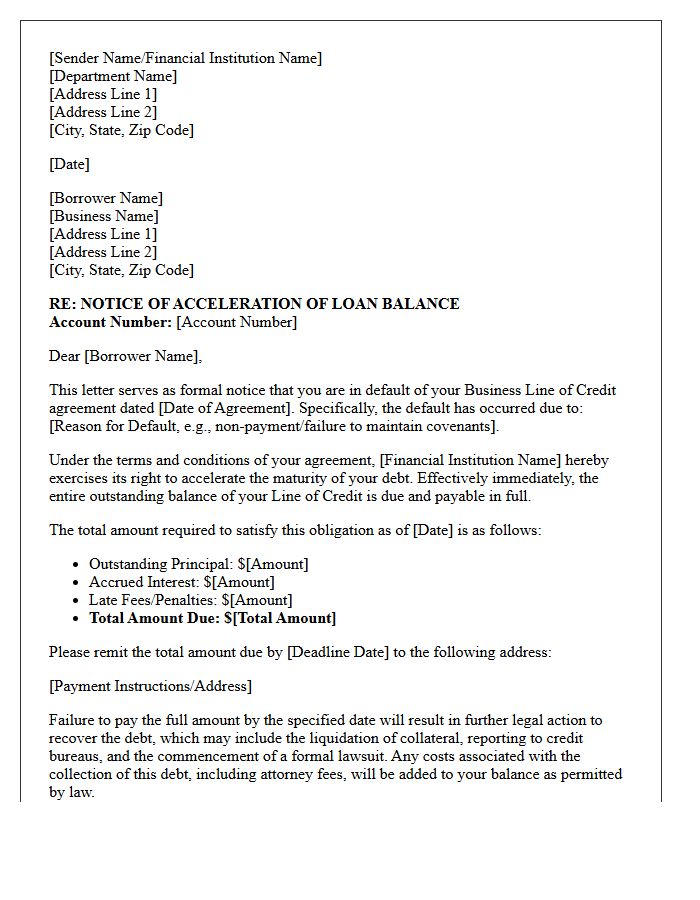

Business Line Of Credit Balance Acceleration Letter

A Business Line Of Credit Balance Acceleration Letter is a formal legal notice issued by a lender demanding immediate repayment of the entire outstanding debt. This usually occurs after a default, such as missed payments or a breach of loan covenants. Receiving this document means the typical monthly installment plan is cancelled, and the full balance is due now. To protect your company, you must act quickly to negotiate a settlement or restructuring plan to avoid further legal action, asset seizure, or damage to your corporate credit score.

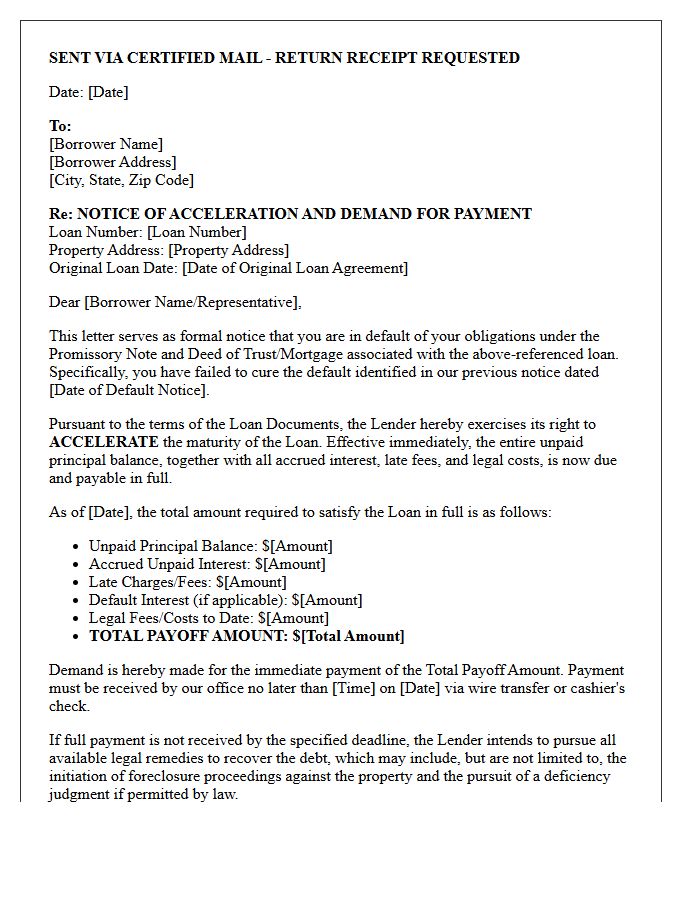

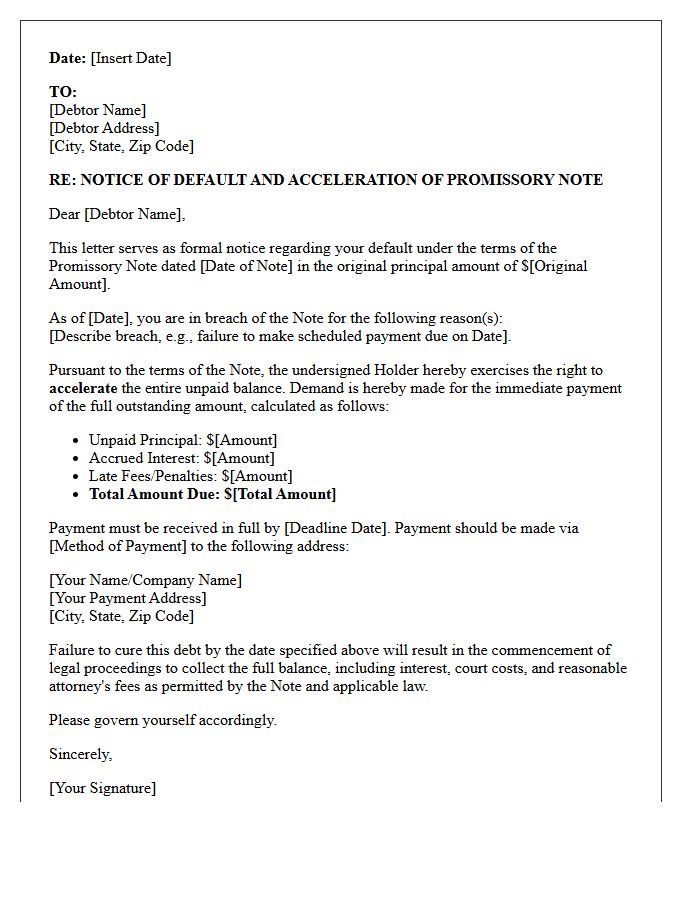

Promissory Note Breach And Acceleration Letter

A Promissory Note Breach And Acceleration Letter is a formal notice sent to a borrower who has defaulted on their repayment terms. This legal document identifies the specific default, such as missed payments, and demands immediate rectification. Critically, it invokes the acceleration clause, which declares the entire remaining loan balance due instantly rather than following the original installment schedule. Providing this notice is often a mandatory procedural step before a lender can initiate foreclosure or legal debt collection actions to recover the outstanding principal and interest owed under the agreement.

What is a Notice of Acceleration of Loan Balance?

A Notice of Acceleration is a formal correspondence from a lender informing a borrower that the entire remaining balance of a loan is due immediately. This occurs after a breach of contract, typically due to consecutive missed payments, which triggers the acceleration clause in the promissory note.

What happens after I receive an acceleration notice?

Once the loan is accelerated, you lose the right to pay the debt in monthly installments. You are required to pay the full principal balance, accrued interest, and any legal fees by a specific deadline. Failure to pay often leads to the commencement of foreclosure proceedings or legal action to seize collateral.

Can I stop a loan acceleration once it has started?

Yes, you can often stop acceleration through "reinstatement," which involves paying all past-due amounts, late fees, and lender costs before a specific cutoff date. Alternatively, you may negotiate a loan modification, a repayment plan, or seek a short sale to satisfy the debt and avoid further legal consequences.

Does a Notice of Acceleration affect my credit score?

Yes, a Notice of Acceleration significantly damages your credit score. It indicates a serious default and is usually preceded by reports of 90 to 120-day delinquencies. If the acceleration leads to foreclosure or a judgment, the negative impact on your credit report can last for seven years.

What is the difference between a Notice of Default and a Notice of Acceleration?

A Notice of Default is the initial warning that you are behind on payments and provides a "cure period" to catch up. A Notice of Acceleration is the subsequent step taken if the default is not cured, officially demanding the total loan balance and terminating the installment agreement.

Comments