Protect your home from unlawful proceedings with a Servicemembers Civil Relief Act Foreclosure Inquiry Letter. This essential document helps active-duty military personnel verify their legal protections and stop unauthorized foreclosures. Understanding your rights under the SCRA is critical for financial security during deployment. To help you take immediate action, below are some ready to use templates.

Image cover: SCRA Foreclosure Protection: Inquiry Letter Templates and Military Compliance Guide

Letter Samples List

- Servicemembers Civil Relief Act Foreclosure Inquiry Letter

- Active Duty Status Verification Foreclosure Letter

- Servicemembers Civil Relief Act Mortgage Inquiry Letter

- Pre-Foreclosure SCRA Compliance Inquiry Letter

- Military Service Foreclosure Hold Request Letter

- SCRA Protection Eligibility Verification Letter

- Bank Foreclosure SCRA Status Confirmation Letter

- Notice Of Deployment Foreclosure Suspension Letter

- Mortgage Servicing SCRA Inquiry Letter

- Servicemembers Civil Relief Act Default Inquiry Letter

- Military Order Submission For Foreclosure Review Letter

- SCRA Benefit Retroactive Foreclosure Inquiry Letter

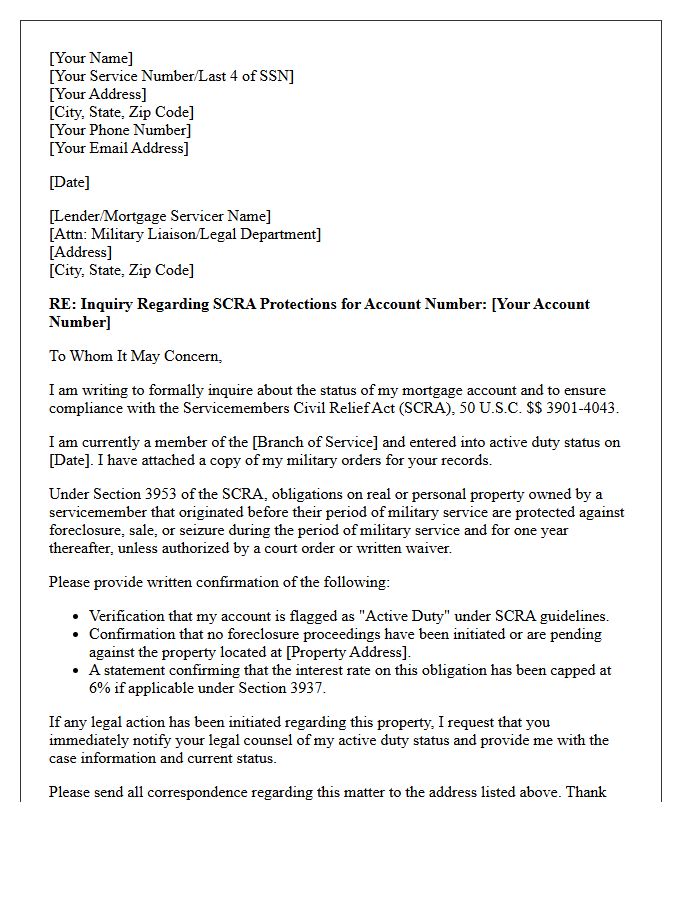

Servicemembers Civil Relief Act Foreclosure Inquiry Letter

A Servicemembers Civil Relief Act Foreclosure Inquiry Letter is a formal document used to verify a homeowner's military status before initiating legal action. Under the SCRA, active-duty service members receive federal protections against non-judicial foreclosures without a court order. Lenders send this inquiry to ensure compliance with legal safeguards, preventing the illegal seizure of property while a member is serving. Understanding this letter is essential for maintaining mortgage compliance and protecting the housing rights of those in the armed forces during their period of active service.

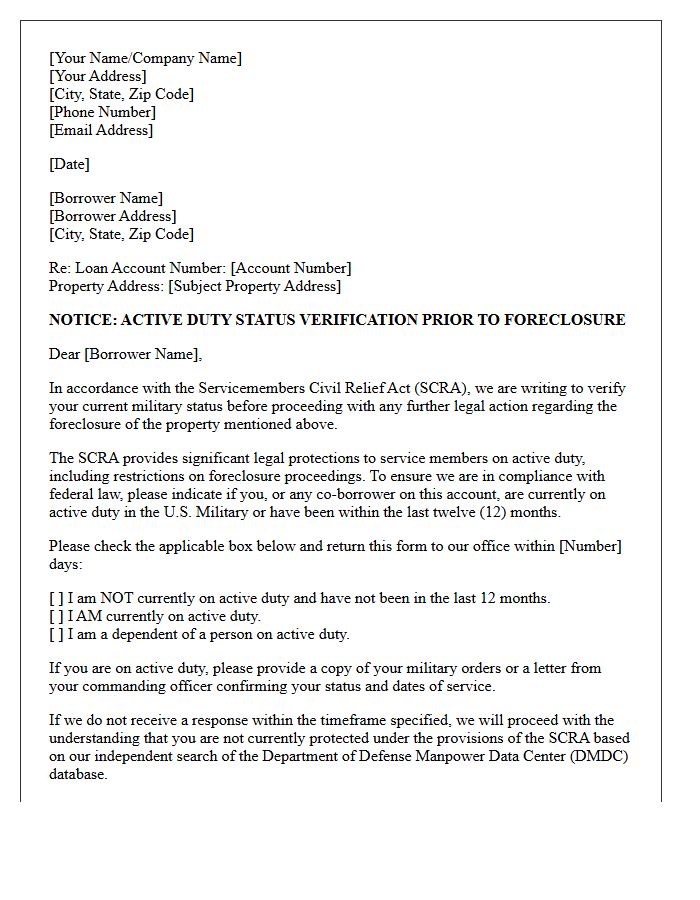

Active Duty Status Verification Foreclosure Letter

An Active Duty Status Verification Foreclosure Letter is a critical legal document used to confirm a borrower's military standing under the Servicemembers Civil Relief Act (SCRA). Lenders must verify active duty status before initiating foreclosure to prevent illegal seizures against qualifying service members. This verification protects personnel from judicial proceedings while they are deployed or on active duty. Failure to accurately verify status can result in severe legal penalties for financial institutions and the immediate voiding of foreclosure actions to ensure federal compliance and military protection.

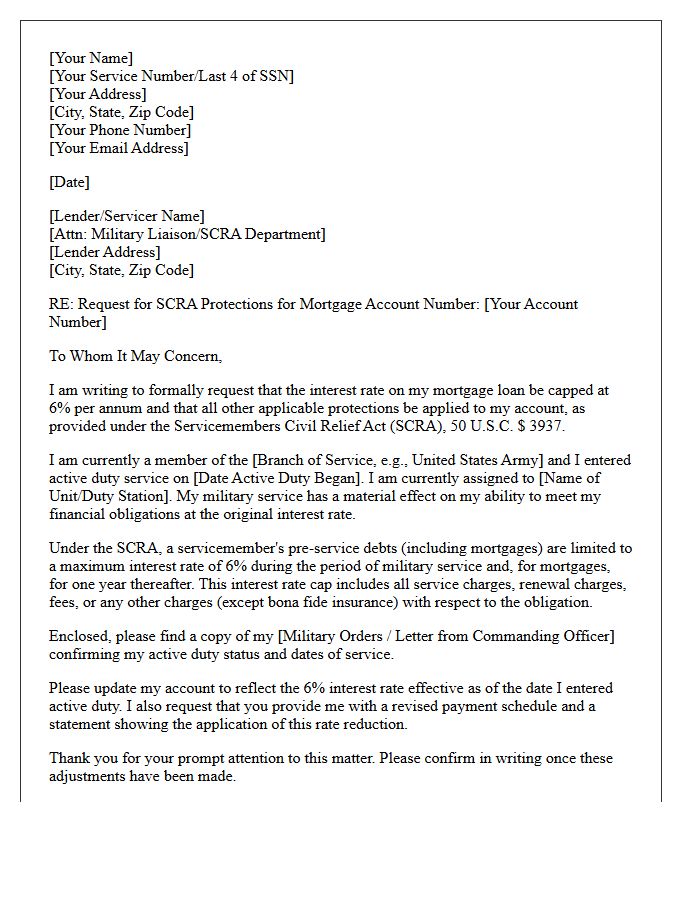

Servicemembers Civil Relief Act Mortgage Inquiry Letter

A Servicemembers Civil Relief Act Mortgage Inquiry Letter is a formal request used to invoke federal legal protections for active-duty military personnel. This document informs lenders of your service status to secure a reduced interest rate, capped at 6%, and provides safeguards against foreclosure without a court order. To qualify, mortgage obligations must have been established prior to entering active duty. Sending this letter with a copy of your military orders ensures compliance with SCRA mandates, protecting your financial stability and home ownership during periods of service.

Pre-Foreclosure SCRA Compliance Inquiry Letter

A Pre-Foreclosure SCRA Compliance Inquiry Letter is a mandatory verification step used by lenders to determine a borrower's military status. Under the Servicemembers Civil Relief Act, active-duty service members receive legal protections against foreclosure without a court order. Sending this inquiry ensures regulatory due diligence and prevents costly legal violations. Lenders must confirm eligibility through the Department of Defense database before proceeding with late-stage collections. Failure to document this compliance can void foreclosure proceedings and result in severe federal penalties or litigation.

Military Service Foreclosure Hold Request Letter

A Military Service Foreclosure Hold Request Letter is a formal document used to invoke protections under the Servicemembers Civil Relief Act (SCRA). This letter notifies lenders of active duty status to prevent unauthorized foreclosure proceedings without a court order. It is essential to include your official military orders to substantiate the request. Providing this notification ensures your home remains secure during deployment or permanent change of station. Timely delivery to your mortgage servicer is critical for establishing legal stay protections and safeguarding your financial rights while serving your country.

SCRA Protection Eligibility Verification Letter

An SCRA Protection Eligibility Verification Letter is a formal document confirming an individual's active-duty military status. It serves as official proof to lenders and creditors that a service member qualifies for legal benefits under the Servicemembers Civil Relief Act. This verification is essential for lowering interest rates to 6%, preventing foreclosures, and stopping repossessions during military service. Obtaining this letter, typically through the DMDC database, ensures that financial rights are legally protected while the individual is deployed or on active duty.

Bank Foreclosure SCRA Status Confirmation Letter

A Bank Foreclosure SCRA Status Confirmation Letter is a legal document used to verify if a homeowner is protected under the Servicemembers Civil Relief Act. This compliance verification ensures that active-duty military members are not subject to foreclosure without a court order. Lenders must conduct a Manpower Data Center search to confirm active service status before proceeding. Failing to secure this documentation can lead to severe legal penalties for the bank, as the SCRA provides essential legal protections and interest rate caps to those serving in the armed forces.

Notice Of Deployment Foreclosure Suspension Letter

A Notice Of Deployment Foreclosure Suspension Letter is a critical legal document that protects active-duty servicemembers from losing their homes. Under the Servicemembers Civil Relief Act (SCRA), lenders are prohibited from initiating foreclosure proceedings while a member is deployed. This letter serves as formal notification to your mortgage servicer, triggering immediate federal protections and freezing any current legal actions. It ensures financial security for families during military service by pausing foreclosure sales and related litigation until the deployment ends and a grace period follows.

Mortgage Servicing SCRA Inquiry Letter

A Mortgage Servicing SCRA Inquiry Letter is a formal request sent to lenders to determine if a borrower is eligible for protections under the Servicemembers Civil Relief Act. This federal law provides critical financial safeguards, such as interest rate caps at 6% and foreclosure protection, for active-duty military members. Borrowers should submit this letter along with their military orders to ensure their servicer applies these legal benefits correctly. Verifying SCRA status helps prevent unlawful home seizure and ensures fair financial treatment during active service periods.

Servicemembers Civil Relief Act Default Inquiry Letter

A Servicemembers Civil Relief Act Default Inquiry Letter is a mandatory legal verification used by plaintiffs before obtaining a default judgment. Under the SCRA, creditors must file an affidavit confirming whether a defendant is currently on active duty. This protects military members from legal prejudice while serving. If service status is uncertain, the court may require a bond or appoint an attorney to represent the servicemember. Failing to conduct this due diligence can result in penalties or the court vacating the judgment, ensuring essential procedural protections for those in uniform.

Military Order Submission For Foreclosure Review Letter

A Military Order Submission For Foreclosure Review Letter is a critical document for service members seeking protections under the Servicemembers Civil Relief Act (SCRA). This letter formally notifies lenders of active duty status to halt or review foreclosure proceedings initiated against a primary residence. To qualify, you must provide your official military orders to verify eligibility periods. Prompt submission ensures legal safeguards against non-judicial foreclosures, potentially preventing the loss of your home while serving. Always keep copies of all correspondence to maintain a clear legal record of your request.

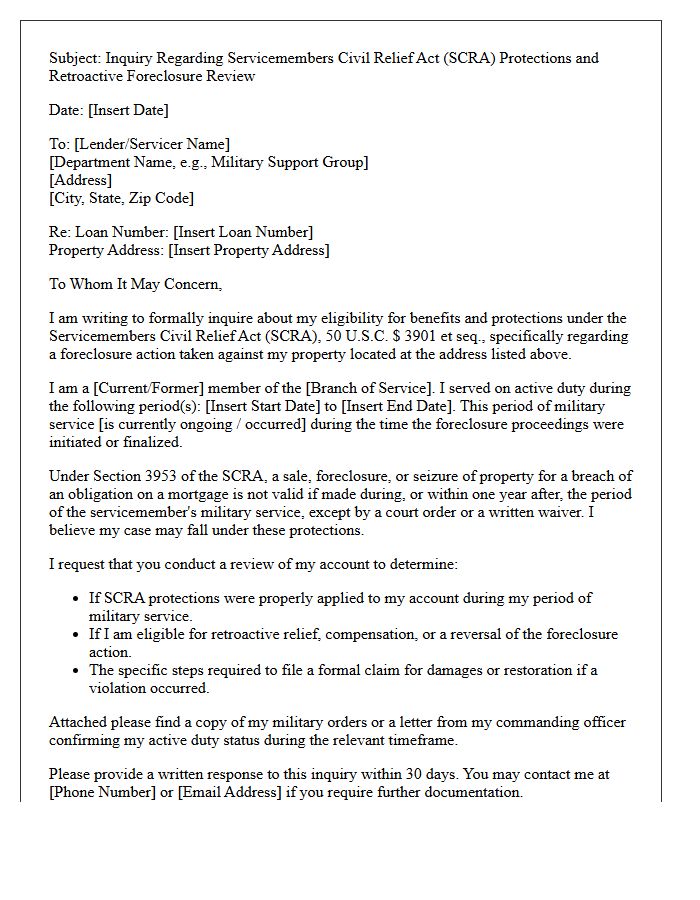

SCRA Benefit Retroactive Foreclosure Inquiry Letter

The SCRA Benefit Retroactive Foreclosure Inquiry Letter is a legal tool used by service members to challenge past foreclosures. Under the Servicemembers Civil Relief Act, lenders are prohibited from foreclosing on active-duty personnel without a court order. This letter serves as a formal request to investigate potential violations occurring during or shortly after military service. If a foreclosure happened illegally, this inquiry initiates the process for financial compensation or credit repair. Ensuring your military orders are documented is essential for validating claims and securing retroactive protections and legal remedies.

What is a Servicemembers Civil Relief Act (SCRA) Foreclosure Inquiry Letter?

An SCRA Foreclosure Inquiry Letter is a formal request sent to a mortgage servicer to determine if a homeowner is eligible for foreclosure protections under the Servicemembers Civil Relief Act due to active-duty military service.

Who is eligible for foreclosure protection under the SCRA?

Protection is generally available to active-duty service members, Reservists, and National Guard members on federal active orders, provided the mortgage was originated prior to the start of their period of military service.

Does the SCRA prevent a lender from foreclosing on a service member?

Under the SCRA, a lender cannot legally foreclose on a protected service member's property without a court order during their period of military service and for an additional one year following the conclusion of that service.

What information should be included in an SCRA Foreclosure Inquiry Letter?

The letter should include the service member's full name, social security number, date of birth, property address, and a copy of their active-duty military orders to verify their service dates and eligibility status.

What are the consequences if a lender violates SCRA foreclosure protections?

Foreclosures conducted in violation of the SCRA are generally considered invalid. Lenders who knowingly violate these protections may face federal penalties, fines, and civil lawsuits for damages filed by the affected service member.

Comments