Receiving a loan rejection due to identity verification failure can be frustrating for both lenders and applicants. This occurs when submitted documentation fails to confirm a borrower's legal identity, triggering security protocols. Understanding the specific reasons for these discrepancies is essential for maintaining regulatory compliance and data integrity. To assist your communication process, below are some ready to use template.

Image cover: Identity Verification Issues: Loan Application Decision Notice and Response Templates

Letter Samples List

- Unverified Identity Loan Application Denial Letter

- Customer Identification Program Compliance Rejection Letter

- Inconclusive Identity Authentication Loan Refusal Letter

- Discrepant Identification Documents Loan Denial Letter

- Unsuccessful Know Your Customer Verification Loan Decline Letter

- Unable To Verify Identity Loan Rejection Letter

- Identity Authentication Failure Credit Denial Letter

- Patriot Act Identity Verification Loan Rejection Letter

- Insufficient Proof Of Identity Loan Decline Letter

- Third-Party Identity Verification Failure Rejection Letter

- Unmatched Government Identification Loan Refusal Letter

- Fraud Prevention Identity Verification Decline Letter

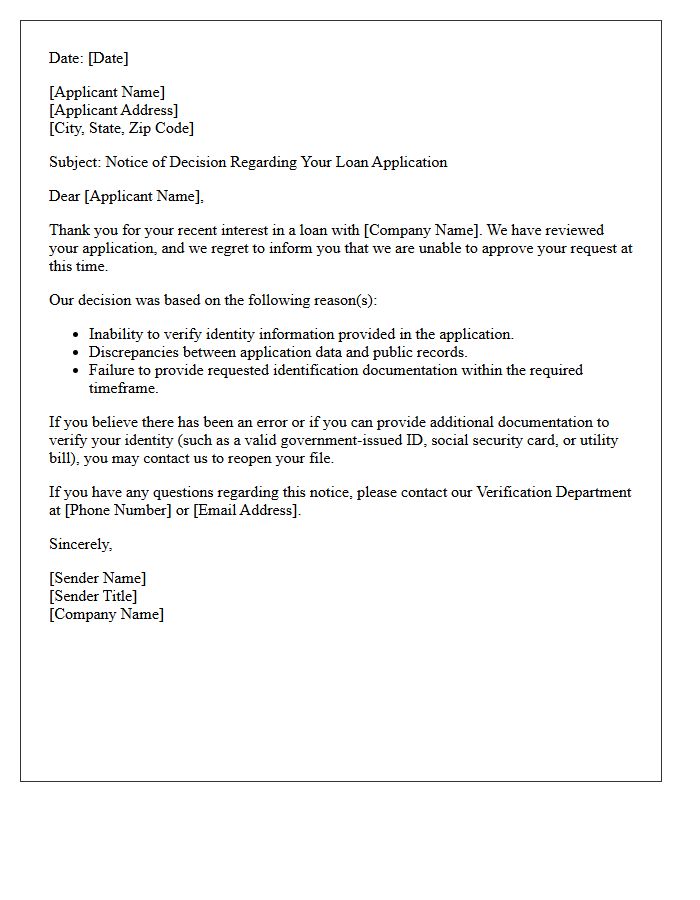

Unverified Identity Loan Application Denial Letter

An Unverified Identity Loan Application Denial Letter is issued when a lender cannot confirm a borrower's legal persona through provided documentation. This notice is often a security measure to prevent identity theft and fraud. Under the Equal Credit Opportunity Act, lenders must provide specific reasons for rejection. To resolve this, applicants should review their credit reports for errors and provide validated identification, such as a government ID or utility bill, to prove residency and legal authenticity during future financial requests.

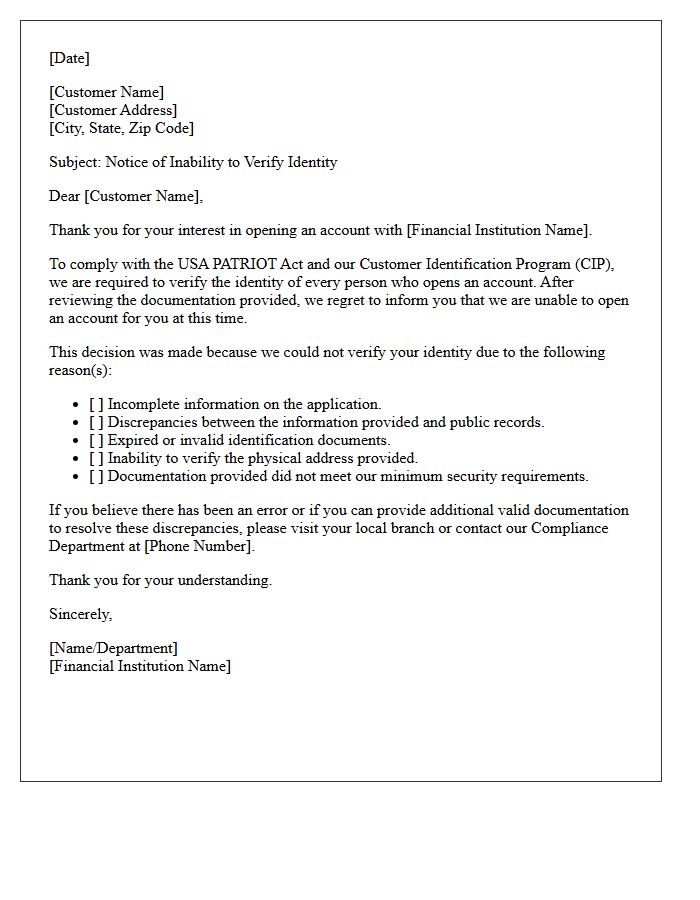

Customer Identification Program Compliance Rejection Letter

A Customer Identification Program (CIP) rejection letter notifies an applicant that a financial institution could not verify their identity under USA PATRIOT Act compliance standards. This formal notice typically outlines missing documentation or inconsistencies in personal data, such as tax identification numbers or residential addresses. Receiving this letter means the account opening process is halted until the discrepancies are resolved. To maintain regulatory compliance, applicants must promptly provide valid, government-issued identification to satisfy federal Know Your Customer (KYC) requirements and mitigate potential identity theft risks.

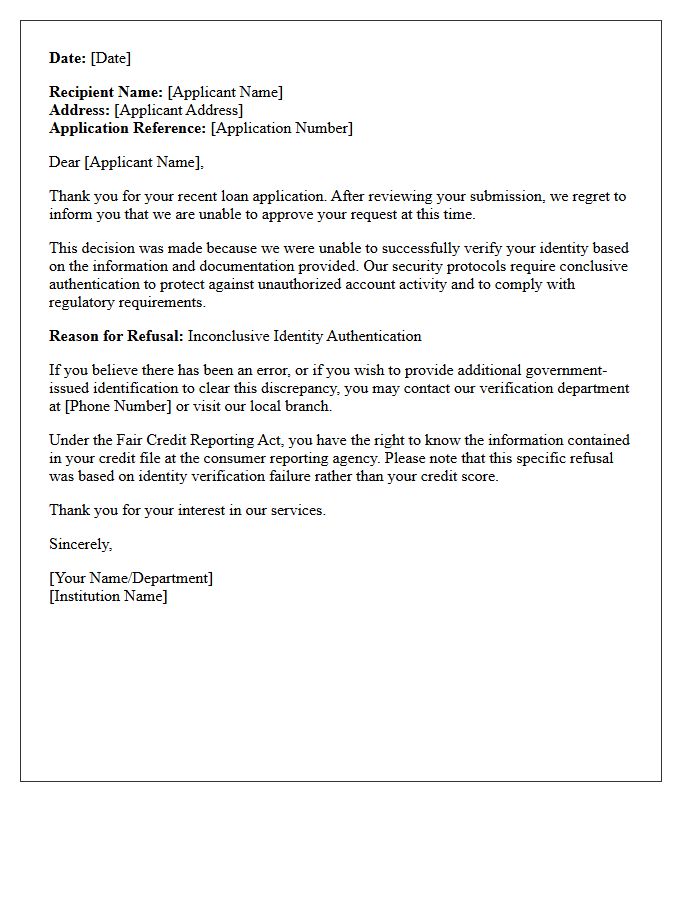

Inconclusive Identity Authentication Loan Refusal Letter

An Inconclusive Identity Authentication letter is a formal notice stating that a lender could not verify your personal details. This refusal occurs when information provided on an application fails to match consumer reporting agency records. It does not necessarily reflect poor creditworthiness, but rather a security measure to prevent fraud. To resolve this, you must typically provide supplemental documentation, such as a government-issued ID or utility bill, to confirm your legal identity. Promptly addressing these discrepancies is essential to successfully reapply for credit and protect against potential identity theft.

Discrepant Identification Documents Loan Denial Letter

A Discrepant Identification Documents Loan Denial Letter is a formal notification issued when a lender cannot verify your identity. This occurs if information on your loan application does not match your government-issued ID or credit reports. Under the Fair Credit Reporting Act, lenders must provide this adverse action notice to prevent fraud and comply with "Know Your Customer" laws. Receiving this letter indicates that identity verification failed, requiring you to provide updated, consistent documentation or correct errors in your credit file to proceed with future financing requests.

Unsuccessful Know Your Customer Verification Loan Decline Letter

An Unsuccessful Know Your Customer (KYC) Verification letter informs applicants that their loan request was denied due to identity validation failures. Lenders are legally required to confirm your identity to prevent financial fraud and money laundering. Common triggers include mismatched personal details, expired identification documents, or unverifiable addresses. Receiving this decline does not necessarily reflect your creditworthiness; however, it indicates that the provided documentation failed to meet regulatory compliance standards. It is essential to review the specific reasons cited to correct errors before reapplying for credit or financing.

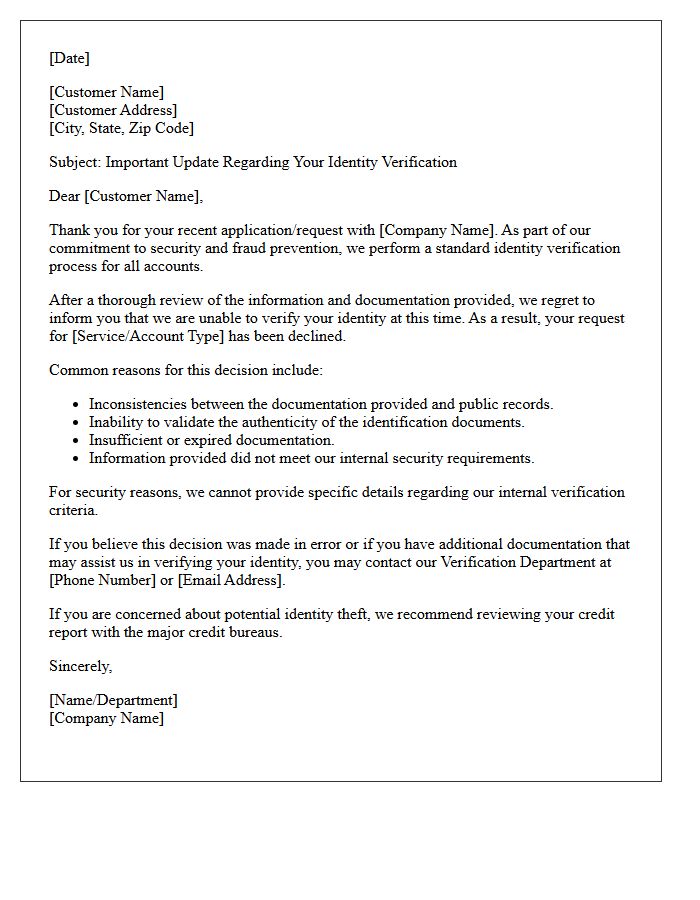

Unable To Verify Identity Loan Rejection Letter

Receiving an Unable To Verify Identity Loan Rejection Letter typically indicates a mismatch between your application data and credit bureau records. Lenders use Identity Verification protocols to prevent fraud and comply with "Know Your Customer" (KYC) regulations. Common causes include typos, recent address changes, or frozen credit reports preventing access. To resolve this, contact the lender immediately to provide valid government ID or proof of residency. Rectifying these clerical errors is essential to secure future financing and ensure your credit profile remains accurate and accessible for legitimate inquiries.

Identity Authentication Failure Credit Denial Letter

An Identity Authentication Failure Credit Denial Letter occurs when a lender cannot verify your identity through automated systems. Receiving this notice does not necessarily mean your credit score is low; rather, it indicates a discrepancy in your personal data or security freeze issues. To resolve this, you must provide supplemental documentation, such as a government-issued ID or utility bill, to prove your residency. Carefully reviewing the letter's specific verification instructions is essential to prevent potential fraud and successfully reactivate your loan application or credit request.

Patriot Act Identity Verification Loan Rejection Letter

Receiving a Patriot Act identity verification loan rejection indicates the lender could not confirm your identity as required by federal anti-money laundering laws. Under Section 326, banks must verify your legal name, date of birth, and address. Common causes for denial include mismatched credit bureau data, expired identification, or recent moves. This rejection is often a compliance failure rather than a reflection of your creditworthiness. To resolve this, contact the lender to provide supplemental documentation, such as a valid government ID or utility bill, to prove your identity and resubmit your application.

Insufficient Proof Of Identity Loan Decline Letter

Receiving an Insufficient Proof of Identity loan decline letter means the lender could not verify your persona according to Know Your Customer (KYC) regulations. This rejection often occurs due to expired documents, blurry uploads, or mismatched addresses between your application and credit profile. To resolve this, ensure you provide valid, government-issued photo identification and recent utility bills. Contacting the lender promptly to clarify specific discrepancies can help you successfully reapply and secure approval by confirming your legal identity and preventing potential fraud flags.

Third-Party Identity Verification Failure Rejection Letter

A Third-Party Identity Verification Failure Rejection Letter informs applicants that their identity could not be confirmed through external data providers. This official notice is often triggered by mismatched personal details, frozen credit reports, or insufficient public records. Under the Fair Credit Reporting Act (FCRA), the document must include the name of the agency used and instructions on how to dispute inaccuracies. Receiving this letter does not necessarily imply fraud; it typically indicates a data discrepancy that requires manual documentation to resolve your application status.

Unmatched Government Identification Loan Refusal Letter

Receiving an Unmatched Government Identification Loan Refusal Letter indicates a critical discrepancy between your application data and official records. Lenders use automated verification systems to confirm identities via databases like the Social Security Administration or DMV. If your name, date of birth, or ID number does not match exactly, the loan is automatically denied to prevent fraud. To resolve this, contact the bureau mentioned in the letter to correct administrative errors or update expired documents. Ensuring your legal information is consistent and accurate is essential for securing future financial approval.

Fraud Prevention Identity Verification Decline Letter

Receiving a Fraud Prevention Identity Verification Decline Letter means a financial institution could not confirm your identity during an application. This safeguard protects against identity theft and unauthorized account access. The letter typically outlines specific documentation discrepancies or issues with credit bureau records. To resolve this, you must contact the institution to provide valid government ID or proof of residency. Promptly addressing these concerns is crucial for financial security and ensures your legitimate credit applications are approved while keeping your personal information safe from malicious actors.

Why was my loan application rejected due to identity verification failure?

Your loan application was declined because the information provided did not match official records or could not be authenticated through our automated verification systems. This is a standard security measure to prevent identity theft and fraudulent applications.

What are the common reasons for identity verification issues in loan applications?

Common reasons include discrepancies in your Social Security Number, expired government-issued identification, inconsistencies between your current address and credit bureau records, or typos in your legal name provided during the application process.

How can I resolve an identity verification error to reapply for a loan?

To resolve the error, ensure your credit report information is up to date, obtain a valid government photo ID, and request a copy of the adverse action notice to identify the specific reporting agency that provided the conflicting data.

Does a loan rejection based on identity verification affect my credit score?

The rejection itself does not impact your credit score; however, the "hard inquiry" performed during the application process may cause a temporary, minor decrease in your score regardless of the final decision.

What documents should I provide to prove my identity after a rejection?

Most lenders require a combination of a valid driver's license or passport, a Social Security card, and recent utility bills or bank statements to verify your residential address and legal identity manually.

Comments