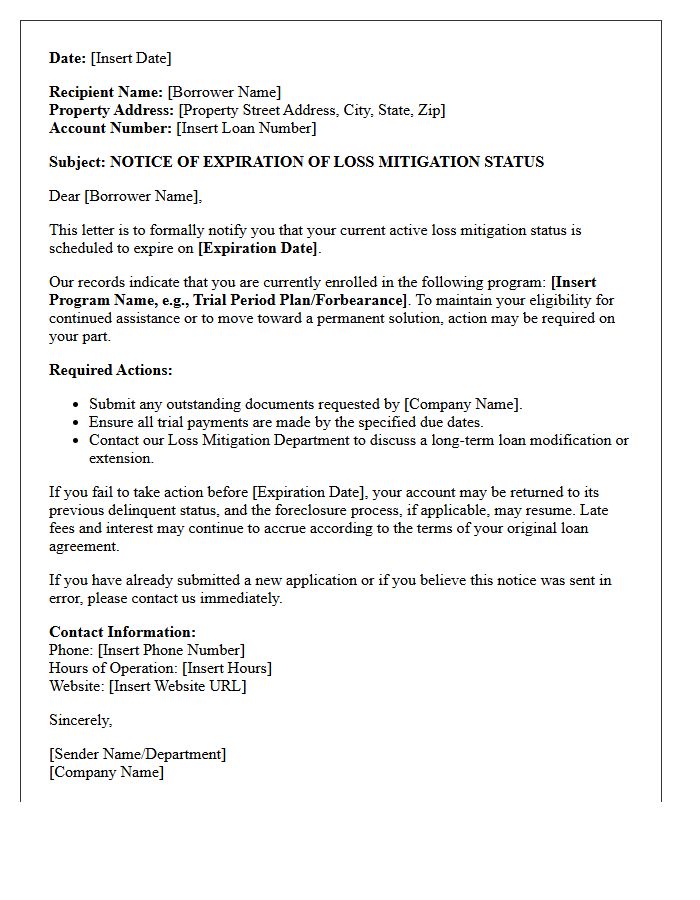

A Notice of Loss Mitigation Program Expiration informs borrowers that their temporary mortgage relief or repayment plan is ending. It is crucial to understand your options to avoid foreclosure and maintain homeownership stability. Acting quickly allows you to explore loan modifications or alternative arrangements before the deadline. To help you communicate effectively with your lender, below are some ready to use template.

Image cover: Final Loss Mitigation Expiration Notices: Templates and Best Practices

Letter Samples List

- Standard Notice of Loss Mitigation Program Expiration Letter

- Final Warning of Loss Mitigation Expiration Letter

- Mortgage Modification Program Expiration Notice Letter

- Trial Payment Plan Expiration Warning Letter

- Mortgage Forbearance Period Expiration Letter

- Loss Mitigation Repayment Plan Expiration Letter

- Loss Mitigation Application Deadline Expiration Letter

- Mortgage Loan Deferral Program Expiration Letter

- Short Sale Agreement Expiration Notice Letter

- Deed in Lieu Program Expiration Letter

- Temporary Mortgage Relief Expiration Letter

- Foreclosure Alternative Program Expiration Letter

- Active Loss Mitigation Status Expiration Letter

Standard Notice of Loss Mitigation Program Expiration Letter

A Standard Notice of Loss Mitigation Program Expiration Letter is a critical formal document sent by mortgage servicers to homeowners. It officially signals the end of temporary relief, such as a forbearance plan or trial modification. Homeowners must understand that this notice triggers the repayment obligation phase. To avoid potential foreclosure, it is essential to contact your lender immediately upon receipt to discuss permanent loan workout options. Ignoring this notification can lead to the loss of your primary residence, making timely communication with your servicer the most important step for long-term housing stability.

Final Warning of Loss Mitigation Expiration Letter

A Final Warning of Loss Mitigation Expiration Letter is a critical legal notice informing homeowners that their window to avoid foreclosure is closing. This document specifies the deadline for submitting or completing a workout plan to save the property. Ignoring this notice typically results in the lender initiating or resuming legal action to reclaim the home. Homeowners must take immediate action by contacting their mortgage servicer to provide missing documentation or accept offered terms before loss mitigation options permanently expire and the home is sold.

Mortgage Modification Program Expiration Notice Letter

A Mortgage Modification Program Expiration Notice Letter is a critical alert from your lender stating that your temporary loan restructuring period is ending. This document details when your monthly payments will revert to a higher rate or original terms. It is essential to review the effective date immediately to avoid financial delinquency. Homeowners should contact their servicer to discuss long-term refinancing options or new repayment plans. Ignoring this notice can lead to unexpected payment shocks and potential foreclosure risks if the new costs are unaffordable.

Trial Payment Plan Expiration Warning Letter

A Trial Payment Plan Expiration Warning Letter is a critical formal notice sent to homeowners nearing the end of their temporary mortgage modification period. It alerts the borrower that the trial phase is concluding and outlines the necessary steps to transition into a permanent loan modification. Ignoring this document can lead to immediate foreclosure proceedings. Recipients must promptly submit any final documentation or outstanding payments required by the lender to secure long-term affordability and maintain legal protection for their home ownership status.

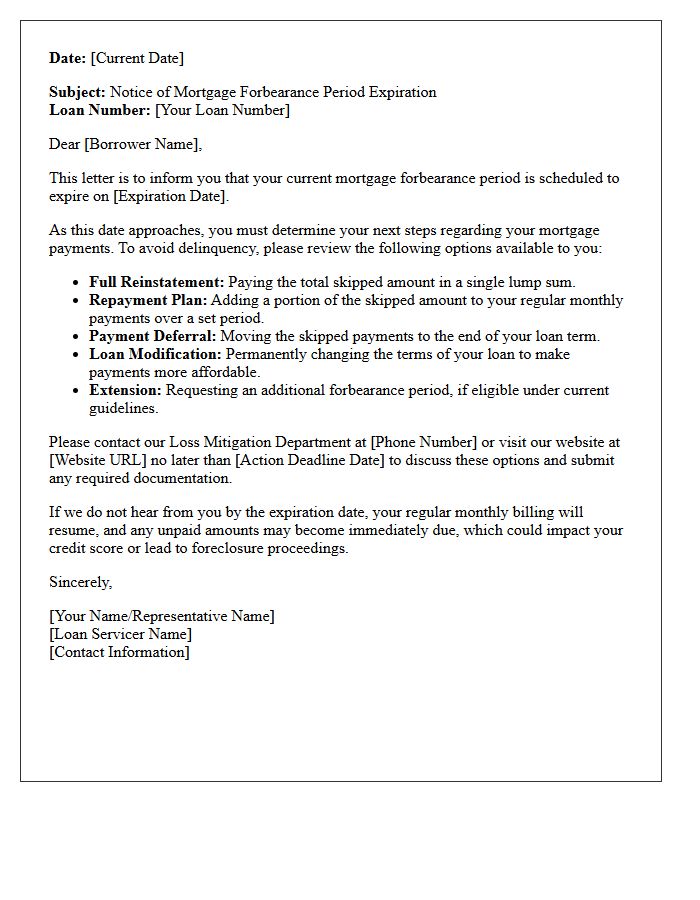

Mortgage Forbearance Period Expiration Letter

A mortgage forbearance period expiration letter is a critical notice from your servicer indicating your temporary payment relief is ending. This document outlines your repayment options to avoid delinquency. It is essential to contact your lender immediately to discuss a loan modification, repayment plan, or deferral. Ignoring this letter may lead to foreclosure proceedings. Carefully review the listed deadlines and required actions to ensure you maintain homeownership. Proactive communication is the most effective way to transition back to regular payments or secure a permanent solution for your financial situation.

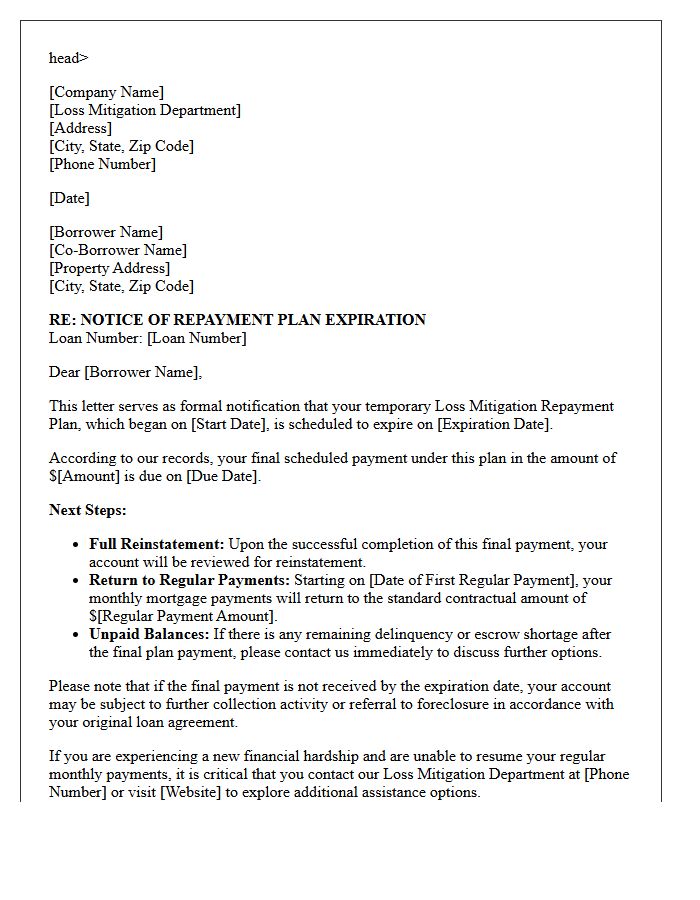

Loss Mitigation Repayment Plan Expiration Letter

A Loss Mitigation Repayment Plan Expiration Letter notifies borrowers that their temporary payment arrangement is ending. This formal notice confirms the final date of the repayment schedule and outlines the remaining balance due. It is critical to review this document to ensure all past-due amounts have been resolved. If the total delinquency is not cured by the expiration date, homeowners must contact their servicer immediately to discuss further foreclosure prevention options or permanent loan modifications to maintain housing stability and avoid default.

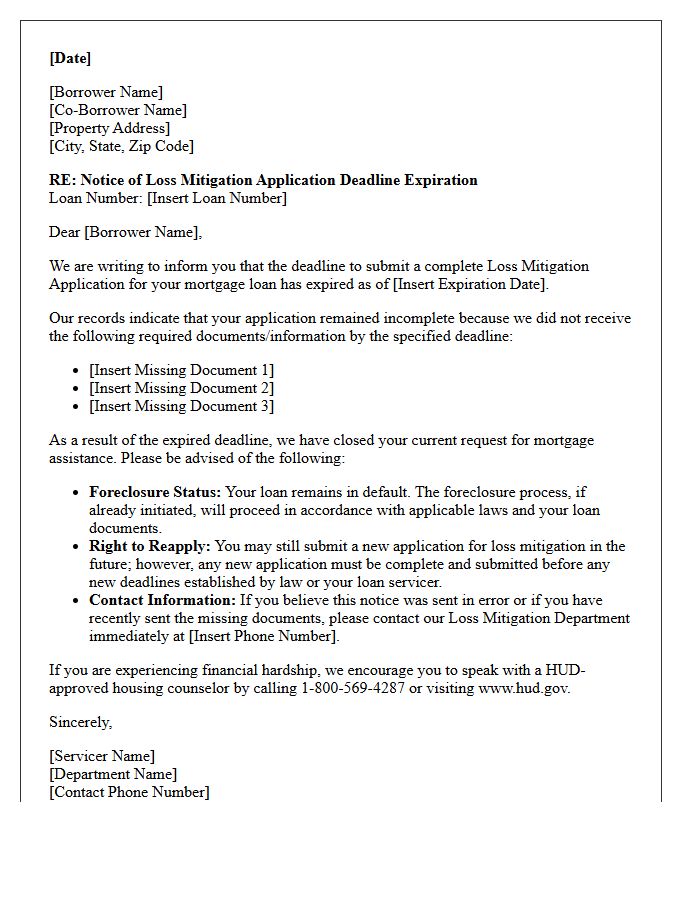

Loss Mitigation Application Deadline Expiration Letter

A Loss Mitigation Application Deadline Expiration Letter is a formal notice from your mortgage servicer indicating that the cutoff date for submitting a complete assistance package has passed. This document signifies that the lender is no longer required to evaluate you for foreclosure alternatives, such as loan modifications or short sales. Receiving this letter often means the foreclosure process will resume or accelerate. Homeowners should immediately contact their servicer to confirm if any reinstatement options remain or if a new application can be initiated to save the property.

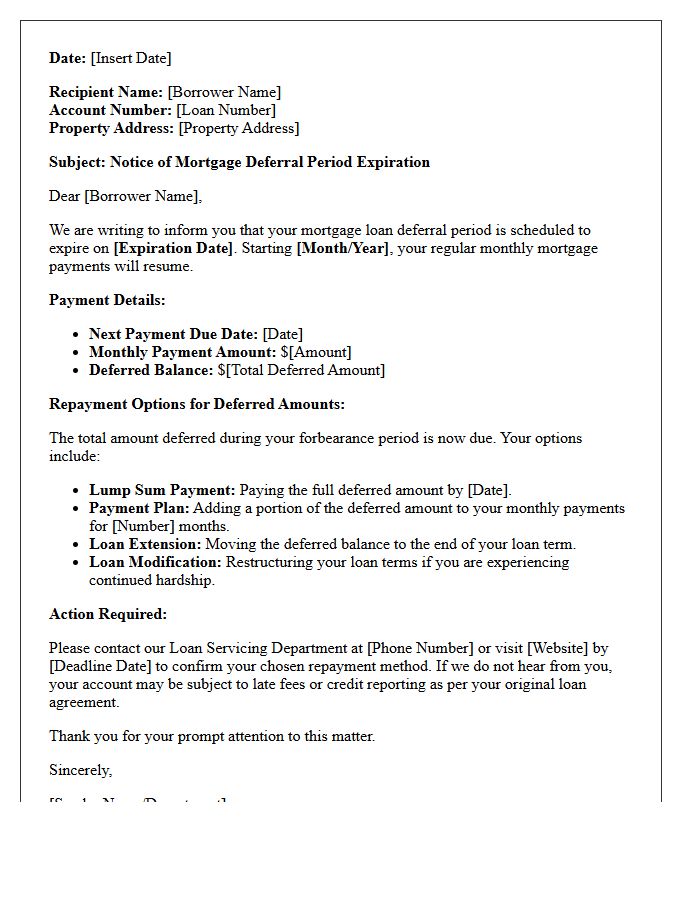

Mortgage Loan Deferral Program Expiration Letter

A Mortgage Loan Deferral Program Expiration Letter is a formal notice indicating that your temporary payment pause is ending. It is crucial to understand that deferred payments are not forgiven; they must be repaid. This document outlines your repayment options, such as a lump sum, loan modification, or repayment plan. Reviewing this letter immediately is vital to avoid foreclosure. You should contact your loan servicer promptly to discuss a sustainable transition back to regular billing and ensure your long-term financial stability before the deadline passes.

Short Sale Agreement Expiration Notice Letter

A Short Sale Agreement Expiration Notice Letter informs stakeholders that the pre-approved timeframe to sell a property for less than the mortgage balance is ending. This document serves as a critical deadline warning for homeowners and agents to finalize negotiations or request an extension. Failure to act before the expiration may lead to the cancellation of the short sale approval, potentially triggering foreclosure proceedings. It is essential to communicate promptly with the lender to maintain the short sale status and avoid losing the opportunity for a deficiency waiver.

Deed in Lieu Program Expiration Letter

A Deed in Lieu Program Expiration Letter is a formal notice from a mortgage servicer informing homeowners that their opportunity to voluntarily transfer property ownership to avoid foreclosure is ending. This deadline signifies the final chance to resolve debt without a public sale. Borrowers must act quickly to submit required documentation before the offer expires. Receiving this letter means you must either complete the voluntary conveyance process immediately or face standard legal proceedings. Understanding these timelines is crucial for protecting your financial future and exploring remaining loss mitigation options.

Temporary Mortgage Relief Expiration Letter

A Temporary Mortgage Relief Expiration Letter is a critical notice from your servicer indicating that your forbearance period is ending. Receiving this means you must promptly choose a repayment option to avoid delinquency. Common solutions include payment deferral, loan modification, or a repayment plan. It is vital to contact your lender immediately upon receipt to discuss your financial situation. Ignoring this document could lead to foreclosure proceedings. Always review the specific deadlines and terms listed to ensure your home remains protected as regular monthly obligations resume.

Foreclosure Alternative Program Expiration Letter

Receiving a Foreclosure Alternative Program Expiration Letter signifies that your deadline to participate in loss mitigation options is ending. This formal notice confirms that temporary relief measures, such as loan modifications or short sales, will no longer be available after the specified date. Once this window closes, the lender may proceed with foreclosure proceedings to reclaim the property. It is critical to contact your mortgage servicer immediately to submit required documentation or negotiate a repayment plan before legal action begins and you lose eligibility for assistance programs.

Active Loss Mitigation Status Expiration Letter

An Active Loss Mitigation Status Expiration Letter is a critical formal notice from your mortgage servicer. It signifies that your temporary foreclosure prevention options, such as forbearance or a trial modification plan, are nearing their end date. This document outlines the specific deadline to transition into a permanent repayment solution or resume standard monthly payments. Failure to act upon receiving this letter may result in the loss of home protection benefits and the resumption of legal foreclosure proceedings against your property.

What is a Notice of Loss Mitigation Program Expiration?

A Notice of Loss Mitigation Program Expiration is a formal communication from your mortgage servicer stating that the temporary foreclosure prevention options or trial payment plans previously offered to you are ending or have expired.

What should I do if I receive a Loss Mitigation Expiration notice?

You should immediately contact your mortgage servicer to discuss long-term options, such as a loan modification, short sale, or deed-in-lieu of foreclosure, to avoid the commencement of legal foreclosure proceedings.

Can I apply for a new loss mitigation program after one expires?

Yes, you can typically submit a new Loss Mitigation Application; however, approval depends on your current financial situation, the reason for the previous expiration, and the specific guidelines provided by the investor of your loan.

How long do I have to act once a loss mitigation offer expires?

Once a program expires, the mortgage servicer may resume the foreclosure process immediately. It is critical to respond within 15 to 30 days to seek alternative solutions before the account is referred to a foreclosure attorney.

Does an expired loss mitigation plan mean I will lose my home?

Not necessarily. While an expiration ends that specific protection plan, homeowners can still explore other exit strategies or repayment plans. Consulting with a HUD-approved housing counselor can provide additional paths to retain ownership.

Comments