A Foreclosure Redemption Payoff Letter is a formal document issued by a lender detailing the exact amount required to satisfy a debt and reclaim property ownership. It outlines the principal balance, interest, and legal fees necessary to halt the foreclosure process. Understanding this statement is vital for homeowners seeking to clear their titles. To simplify your request, below are some ready to use template.

Image cover: Sample Foreclosure Redemption Payoff Letters and Templates for Homeowners

Letter Samples List

- Standard Foreclosure Redemption Payoff Letter

- Pre-Foreclosure Reinstatement Quote Letter

- Borrower Request for Foreclosure Redemption Letter

- Lender Approved Redemption Payoff Statement Letter

- Post-Foreclosure Statutory Redemption Right Letter

- Final Demand and Foreclosure Notice Letter

- Third-Party Purchaser Redemption Payoff Letter

- Mortgage Default and Acceleration Warning Letter

- Equitable Right of Redemption Acknowledgment Letter

- Certificate of Redemption Issuance Letter

- Short Sale Alternative Payoff Approval Letter

- Deed in Lieu of Foreclosure Settlement Letter

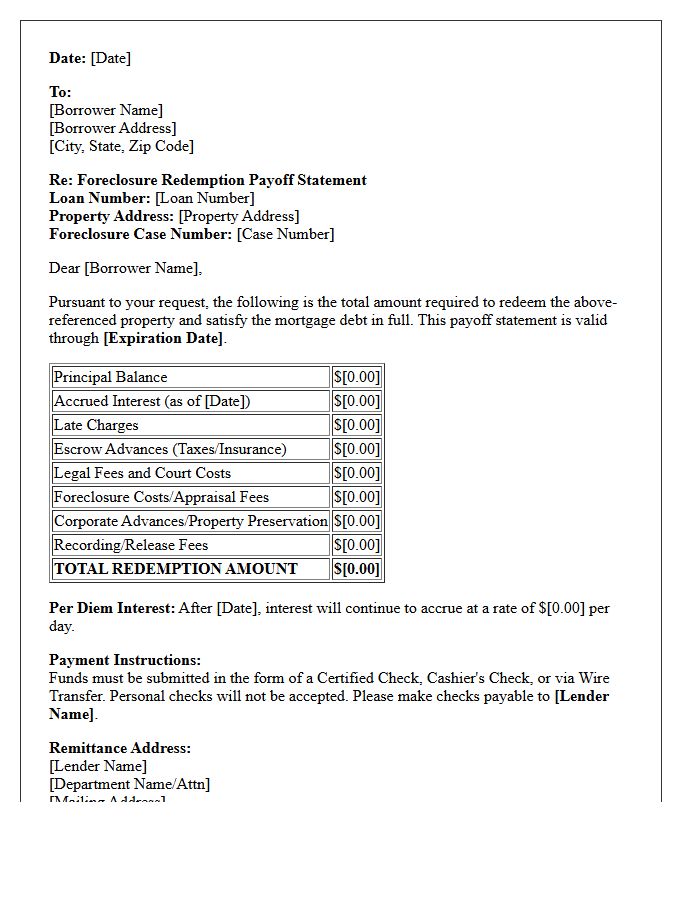

Standard Foreclosure Redemption Payoff Letter

A Standard Foreclosure Redemption Payoff Letter is a legal document specifying the total debt amount required to stop a foreclosure and reclaim property ownership. It outlines the principal balance, accrued interest, late fees, and legal costs. Homeowners must request this statement to understand their redemption rights before the sale date. Timely payment of the exact figure listed ensures the reinstatement of the title and satisfies the mortgage obligation. Accuracy is vital, as even minor shortfalls can result in the loss of the property during the final proceedings.

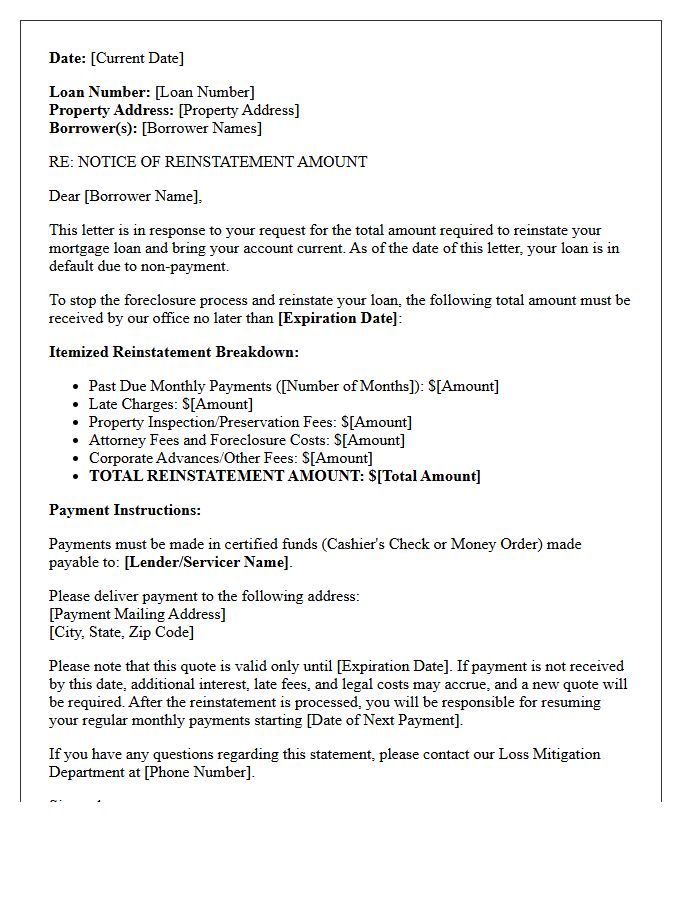

Pre-Foreclosure Reinstatement Quote Letter

A Pre-Foreclosure Reinstatement Quote Letter is a legal document issued by a mortgage lender detailing the specific amount required to bring a delinquent loan current. This letter is crucial for homeowners seeking to stop the foreclosure process by paying off all past-due balances, including late fees, interest, and legal costs. It provides a formal breakdown of the total debt and sets a firm deadline for payment. Obtaining an accurate reinstatement quote is the most direct way to resolve a default and restore the original terms of a mortgage agreement.

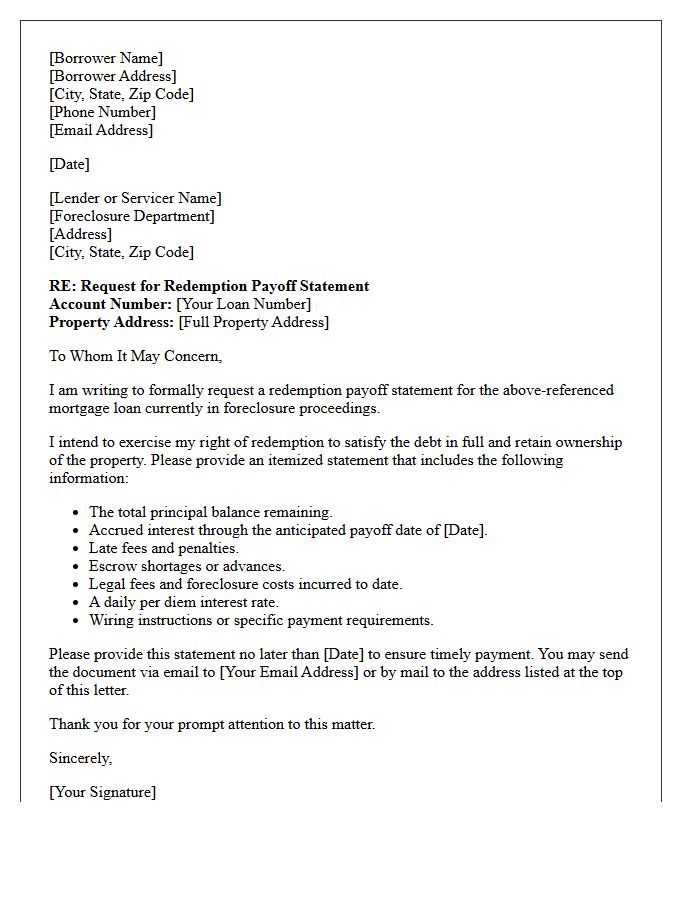

Borrower Request for Foreclosure Redemption Letter

A borrower request for a foreclosure redemption letter is a formal demand to a lender for the exact payoff amount required to reclaim a property. This document provides a detailed breakdown of the remaining principal, interest, and legal fees. Obtaining this letter is critical because it establishes the legal redemption price needed to stop the foreclosure process. Borrowers must act quickly within the state-defined redemption period to ensure they meet specific deadlines and secure their ownership rights before the final sale is finalized.

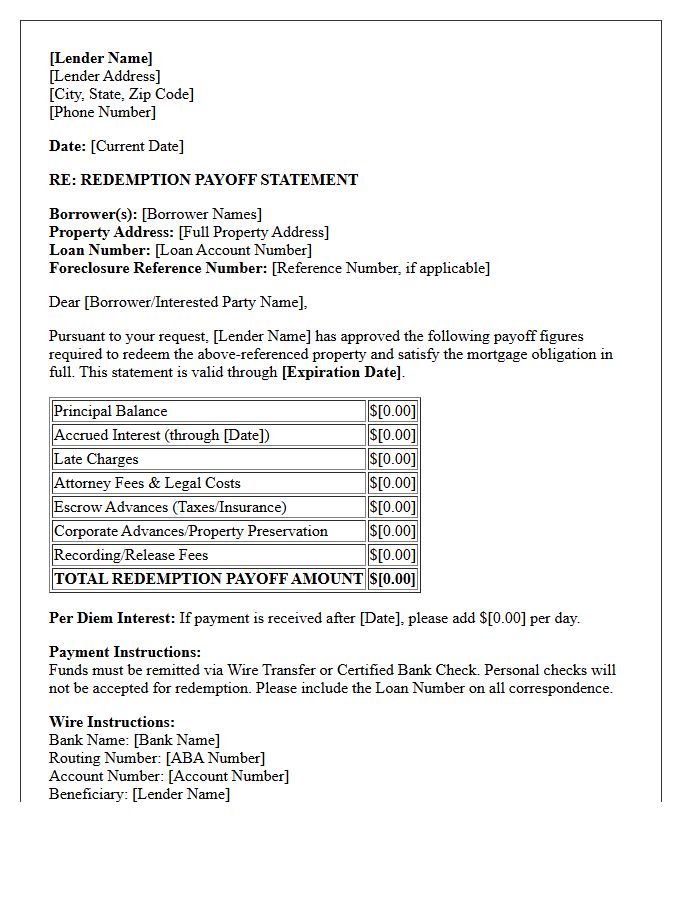

Lender Approved Redemption Payoff Statement Letter

A Lender Approved Redemption Payoff Statement Letter is a formal document detailing the exact amount required to satisfy a mortgage debt and release a property lien. It provides a precise payoff balance, including principal, interest, and legal fees, valid through a specific date. This letter is crucial during foreclosure or property sales to ensure the redemption process is legally binding. Homeowners must request this statement to confirm the final figure needed to regain full ownership and clear the title of any financial encumbrance before the deadline.

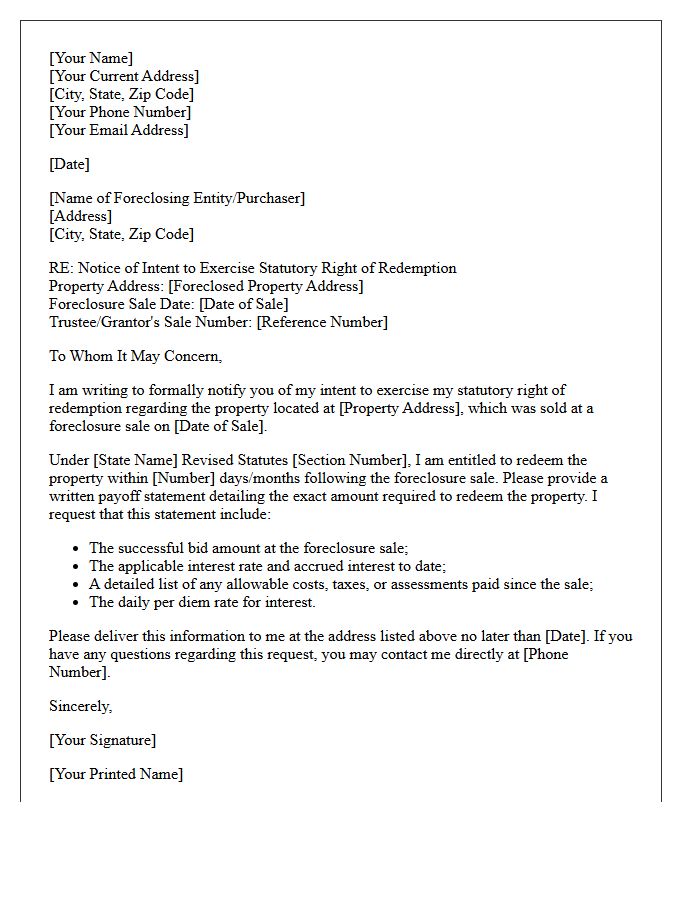

Post-Foreclosure Statutory Redemption Right Letter

A Post-Foreclosure Statutory Redemption Right Letter notifies former owners of their legal right to reclaim property after a foreclosure sale. This document specifies the redemption period and the exact amount required to repurchase the home, including the bid price, interest, and legal fees. Understanding this notice is critical because missing the statutory deadline permanently terminates all ownership interests. Laws vary by state, making it essential to act quickly to exercise these reacquired rights or negotiate a settlement before the redemption window expires.

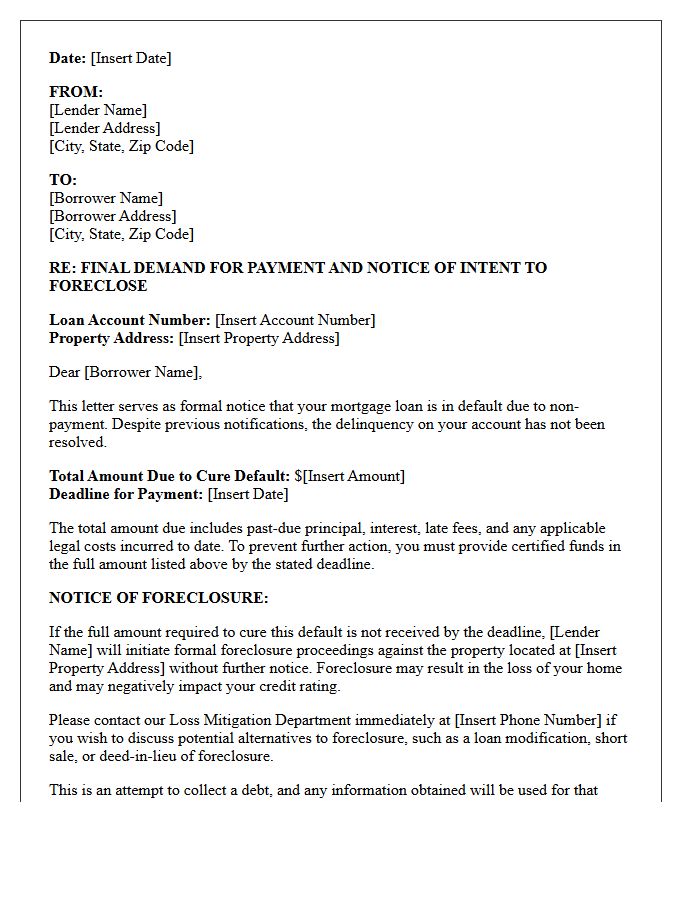

Final Demand and Foreclosure Notice Letter

A Final Demand and Foreclosure Notice Letter is a critical legal notification indicating that a borrower has defaulted on mortgage payments. This formal document serves as the last opportunity to cure the default before the lender initiates legal action to seize the property. It specifies the total overdue amount, including late fees and interest, and provides a strict deadline for payment. Ignoring this notice leads to foreclosure proceedings, resulting in the loss of homeownership and severe damage to your credit score. Immediate communication with your lender or legal counsel is essential.

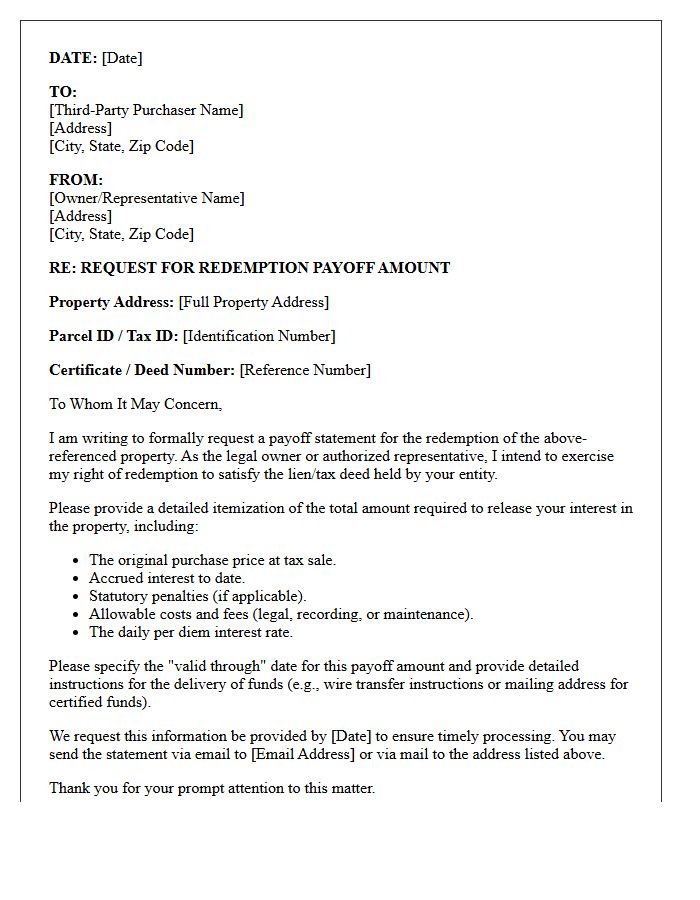

Third-Party Purchaser Redemption Payoff Letter

A Third-Party Purchaser Redemption Payoff Letter is a critical legal document used in tax lien foreclosures. It outlines the exact total balance required to satisfy a debt, including the original lien amount, accrued interest, and statutory fees. Property owners must request this official statement to facilitate a valid redemption and prevent the permanent loss of title. Accuracy is essential, as even minor discrepancies can delay the clearance of encumbrances. This letter ensures transparency between the investor and the homeowner during the final stages of the redemption process.

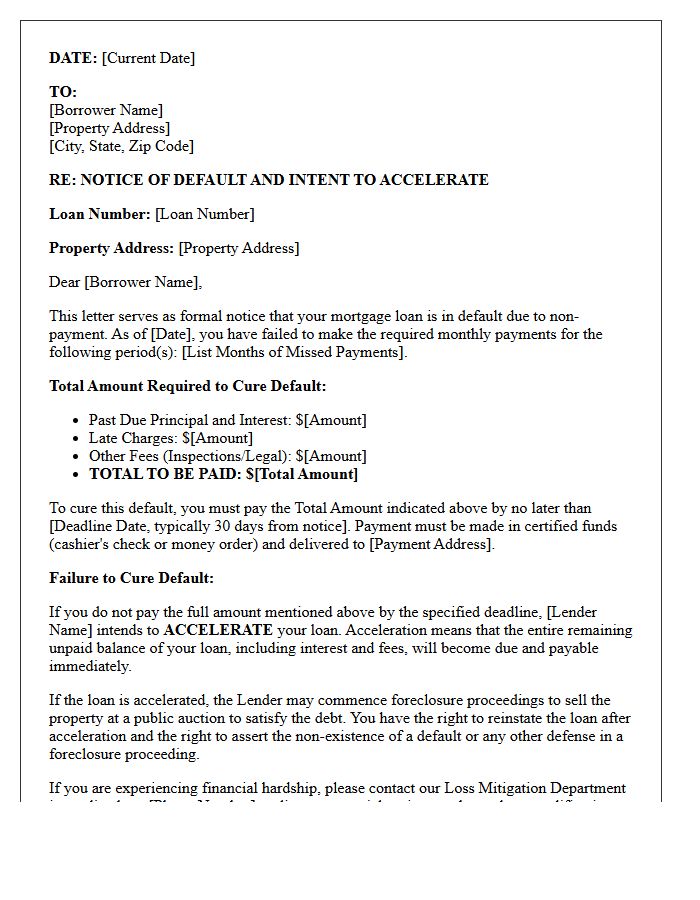

Mortgage Default and Acceleration Warning Letter

A mortgage default occurs when a borrower fails to make payments as agreed. Upon default, the lender issues an acceleration warning letter, a formal notice stating the intent to demand the full remaining balance immediately. This demand for payment serves as a final opportunity to cure the delinquency. If the homeowner does not pay the specified amount by the deadline, the lender can legally initiate foreclosure proceedings to recover the debt. Receiving this letter is a critical signal to seek legal counsel or contact the loan servicer to discuss loss mitigation options.

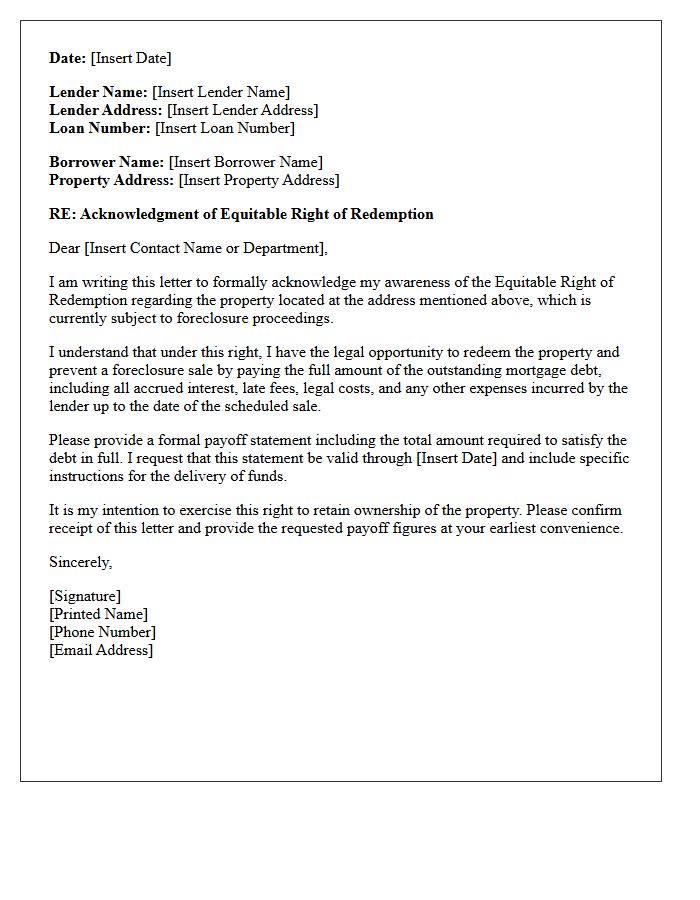

Equitable Right of Redemption Acknowledgment Letter

An Equitable Right of Redemption Acknowledgment Letter is a formal document confirming a borrower's legal right to reclaim foreclosed property by paying the total debt before the auction. This equitable right exists in all states until the foreclosure sale is finalized. The letter ensures all parties acknowledge the homeowner's opportunity to satisfy the mortgage obligation and stop legal proceedings. Understanding this timeline is crucial for preventing permanent loss of title and ensuring procedural fairness during the financial recovery process.

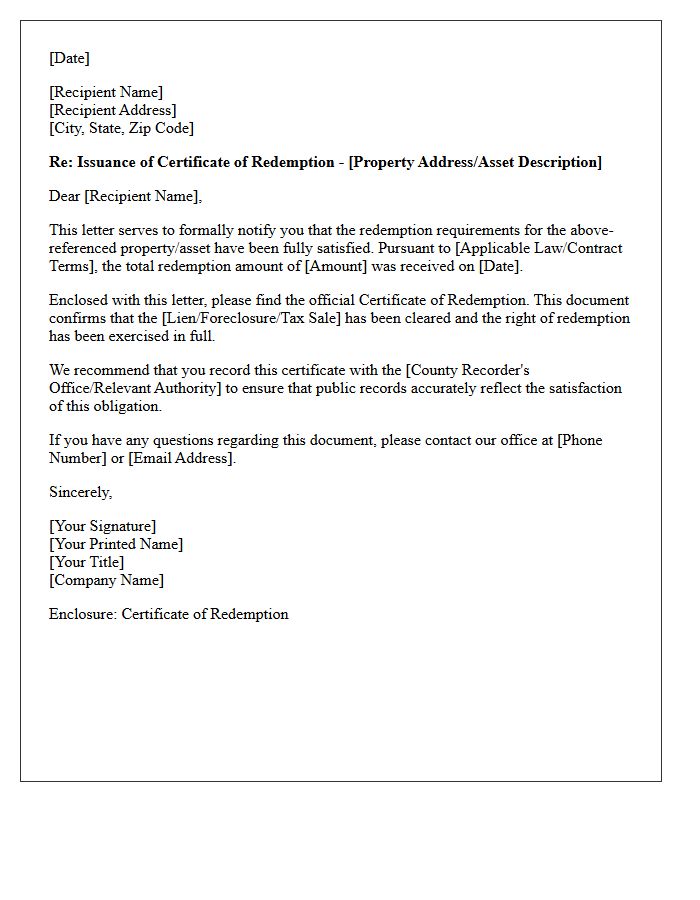

Certificate of Redemption Issuance Letter

A Certificate of Redemption Issuance Letter is a formal document confirming that a property owner has successfully paid all outstanding tax debts and penalties. This letter serves as legal proof that the right of redemption has been exercised, effectively canceling a tax sale or foreclosure process. It verifies that the lien is satisfied and the owner's legal title is cleared of the specific tax liability. Retaining this letter is essential for updating public records and ensuring the property remains in the owner's possession without further legal encumbrance.

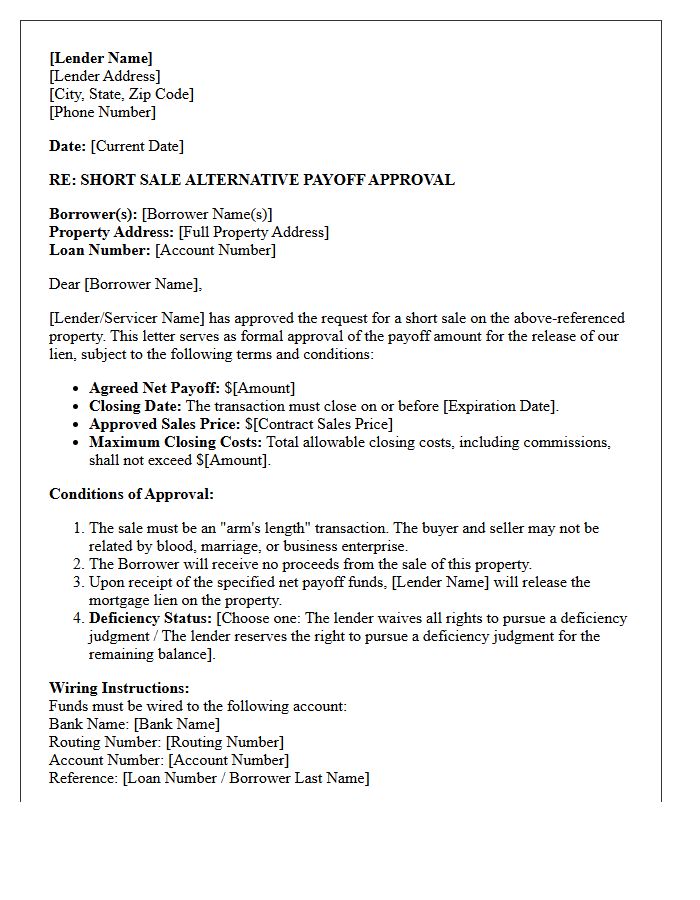

Short Sale Alternative Payoff Approval Letter

A Short Sale Alternative Payoff Approval Letter is a formal document from a mortgage lender agreeing to accept less than the total balance owed to settle a debt. This letter is crucial because it outlines specific closing deadlines, approved net proceeds, and whether the lender waives their right to a deficiency judgment. Receiving this written authorization is the final step in preventing foreclosure, ensuring the lien release occurs upon the successful sale of the property to a third-party buyer at the discounted payoff amount.

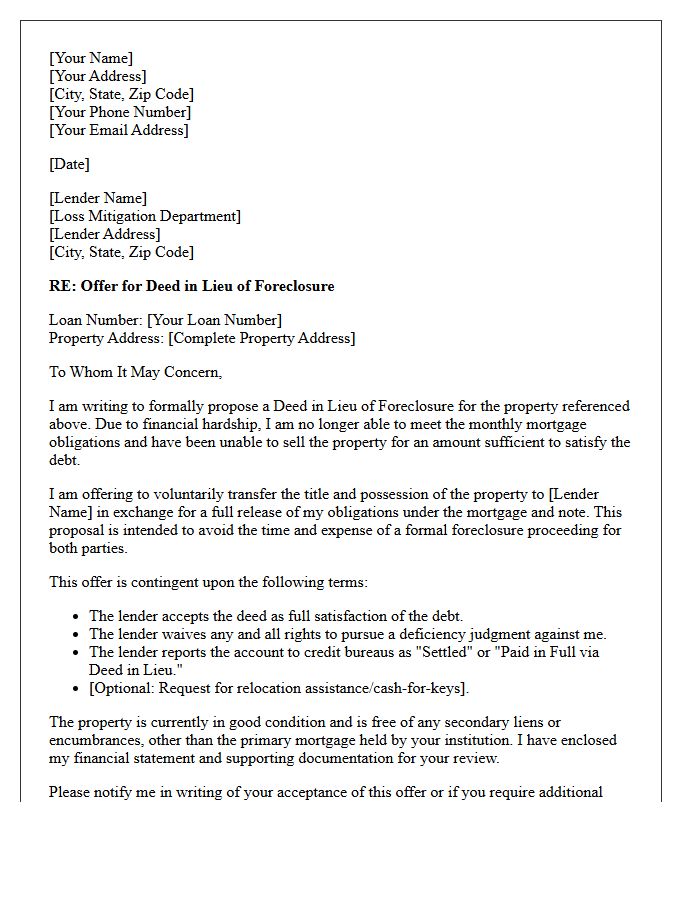

Deed in Lieu of Foreclosure Settlement Letter

A Deed in Lieu of Foreclosure Settlement Letter is a formal legal agreement where a borrower voluntarily transfers property ownership to the lender to satisfy a defaulted loan. This document is crucial because it outlines the release of liability, ensuring the lender waives the right to pursue a deficiency judgment. It serves as a strategic alternative to foreclosure, potentially mitigating credit score damage. Before signing, verify that the letter explicitly states the debt is considered paid in full to avoid future financial claims or unexpected legal obligations during the settlement process.

What is a Foreclosure Redemption Payoff Letter?

A foreclosure redemption payoff letter is an official document issued by a mortgage lender or servicer that provides the exact total amount required to pay off a loan in full and stop the foreclosure process. It includes the outstanding principal balance, accrued interest, legal fees, and administrative costs calculated through a specific expiration date.

How do I request a payoff letter to stop a foreclosure?

To request a payoff letter, you must contact your mortgage servicer's loss mitigation or payoff department in writing. Under the Real Estate Settlement Procedures Act (RESPA), servicers are generally required to provide a payoff statement within seven business days of receiving a written request from the borrower or an authorized representative.

What costs are included in a foreclosure redemption statement?

A redemption statement typically includes the unpaid principal balance, delinquent interest, late charges, escrow deficiencies for taxes and insurance, attorney fees, property inspection costs, and recording fees associated with the foreclosure proceedings.

What is the difference between a reinstatement amount and a redemption payoff?

A reinstatement amount is the total needed to bring the loan current by paying only the past-due payments and fees, whereas a redemption payoff is the total amount required to satisfy the entire mortgage debt and release the lien on the property.

Can a lender refuse to provide a payoff letter during foreclosure?

No, federal law requires mortgage servicers to provide accurate payoff statements to borrowers. If a lender refuses to provide the letter or includes unauthorized fees, the borrower may have grounds for a legal dispute or a complaint with the Consumer Financial Protection Bureau (CFPB).

Comments