A Business Line of Credit Approval Letter is an official document from a lender confirming your company's access to flexible funding. It outlines essential terms, including the maximum credit limit, interest rates, and repayment conditions. Securing this letter validates your business's creditworthiness and financial stability. To help you draft or review one professionally, below are some ready to use template.

Image cover: Standard Approval Letter Templates for a Business Line of Credit

Letter Samples List

- Standard Business Line of Credit Approval Letter

- Commercial Line of Credit Final Approval Letter

- Small Business Line of Credit Terms Approval Letter

- Revolving Business Line of Credit Approval Letter

- Corporate Line of Credit Facility Approval Letter

- Unsecured Business Line of Credit Approval Letter

- Secured Business Line of Credit Approval Letter

- Business Line of Credit Renewal Approval Letter

- Business Line of Credit Limit Increase Approval Letter

- Conditional Business Line of Credit Approval Letter

- Short-Term Business Line of Credit Approval Letter

- Enterprise Line of Credit Origination Approval Letter

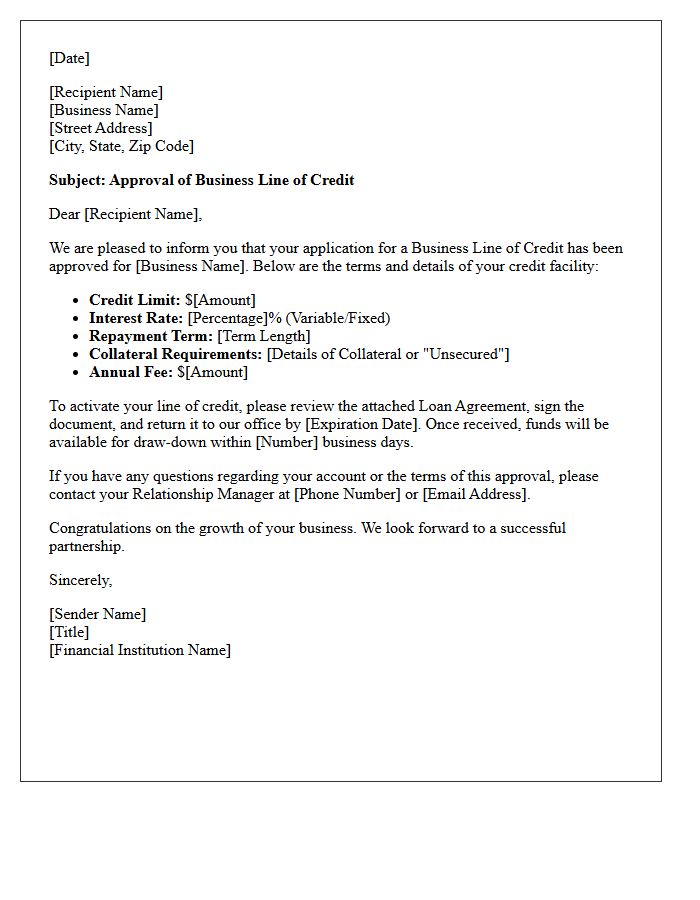

Standard Business Line of Credit Approval Letter

A Standard Business Line of Credit Approval Letter serves as a formal commitment from a lender, outlining the specific terms of your flexible financing. It identifies your maximum credit limit, the applicable interest rates, and necessary collateral requirements. This document is essential for understanding your borrowing capacity and repayment obligations. Before signing, businesses must review the expiration date and any closing conditions to ensure the funds remain accessible for operational needs. Receiving this letter signifies a successful credit assessment and the final step before activating your revolving capital.

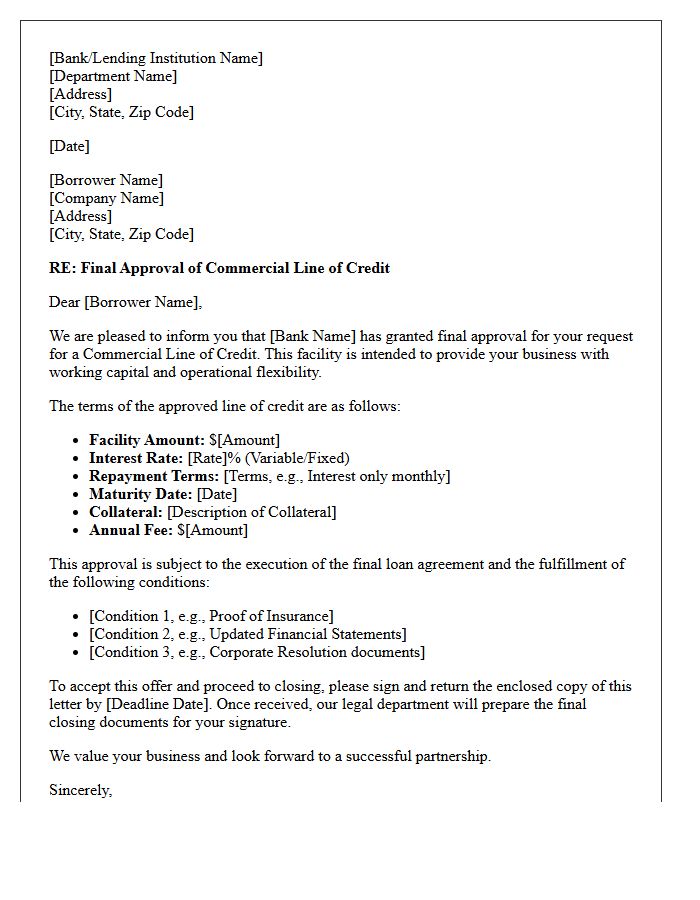

Commercial Line of Credit Final Approval Letter

A Commercial Line of Credit Final Approval Letter is a formal document confirming that a lender has granted guaranteed access to funds. This binding commitment outlines critical terms, including the maximum credit limit, variable interest rates, and specific repayment structures. Receipt of this letter signifies that all underwriting conditions and financial audits are complete. It serves as the final step before loan closing, allowing businesses to draw capital for operational needs, inventory, or expansion with confidence in their liquid credit availability.

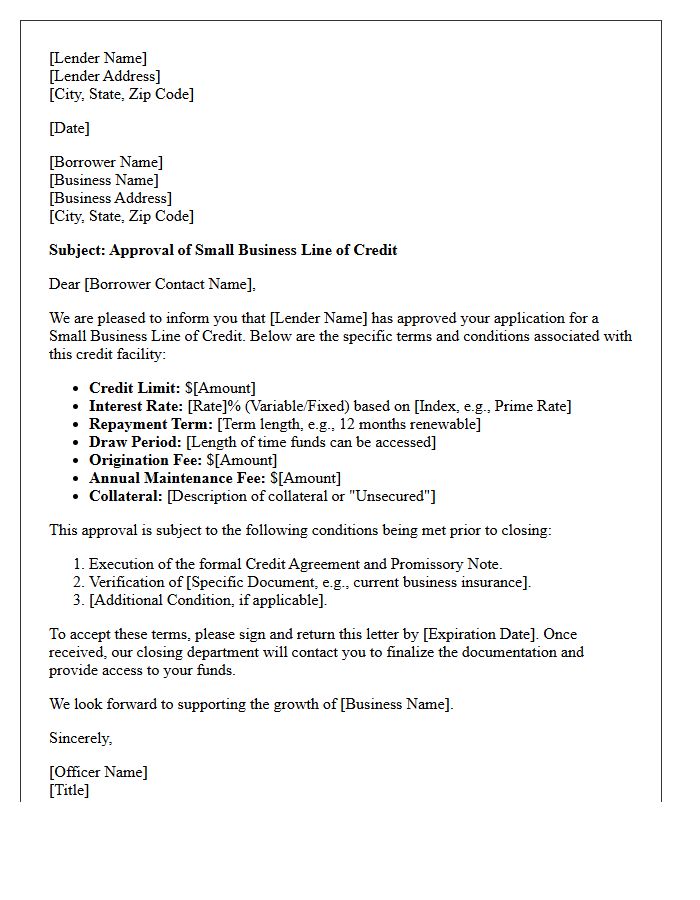

Small Business Line of Credit Terms Approval Letter

A Small Business Line of Credit Approval Letter outlines the specific terms and conditions of your financing. It typically details your maximum borrowing limit, variable interest rates, and repayment schedules. Reviewing this document is crucial to understanding any collateral requirements, annual fees, or draw periods associated with the facility. This letter serves as a formal commitment from the lender but remains subject to final verification. Always ensure the drawdown flexibility aligns with your operational cash flow needs before signing to secure your revolving capital.

Revolving Business Line of Credit Approval Letter

A Revolving Business Line of Credit Approval Letter is a formal document confirming that a lender has authorized your business to access flexible funding. This letter specifies your credit limit, applicable interest rates, and repayment terms. Unlike a traditional loan, this approval allows you to withdraw funds, repay them, and borrow again as needed. It serves as essential proof of liquidity, enabling business owners to manage cash flow gaps or seize immediate growth opportunities with confidence. Always review the contingencies and expiration date mentioned in the letter to ensure funds remain available.

Corporate Line of Credit Facility Approval Letter

A corporate line of credit facility approval letter is a formal document from a lender confirming that a business is authorized to access flexible financing up to a specified limit. This letter details critical terms and conditions, including the maximum borrowing capacity, applicable interest rates, and repayment schedules. It serves as proof of liquidity, allowing companies to manage operational cash flow or fund growth. Before drawdown, borrowers must satisfy all covenants mentioned to maintain the facility's availability and ensure ongoing compliance with the financial institution's requirements.

Unsecured Business Line of Credit Approval Letter

An Unsecured Business Line of Credit Approval Letter is a formal commitment from a lender outlining your pre-approved credit limit without requiring collateral. This document specifies essential terms, including the variable interest rate, repayment schedule, and draw periods. Receiving this letter confirms your business's creditworthiness based on cash flow and financial history. It serves as a vital tool for managing working capital and operational flexibility, allowing you to access funds as needed to cover immediate expenses or strategic growth opportunities without risking specific physical assets.

Secured Business Line of Credit Approval Letter

A Secured Business Line of Credit Approval Letter is a formal document confirming that a lender has authorized flexible funding backed by collateral, such as inventory or accounts receivable. This letter specifies your maximum borrowing limit, interest rates, and draw periods. Receiving this document signifies that your business has passed rigorous underwriting and risk assessment. It serves as proof of available capital, enabling you to manage cash flow gaps or invest in growth opportunities immediately. Always review the terms and conditions before signing to ensure the repayment structure aligns with your revenue cycle.

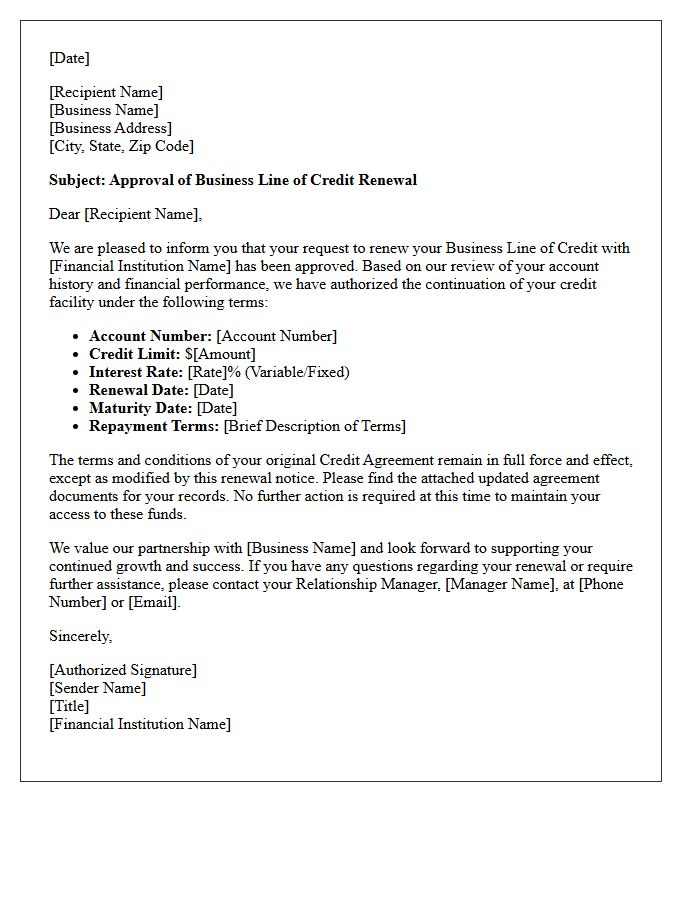

Business Line of Credit Renewal Approval Letter

A Business Line of Credit Renewal Approval Letter confirms your lender has extended your access to revolving funds. It outlines the updated credit limit, applicable interest rates, and the new maturity date. Key terms may change based on your recent financial performance or credit score. Reviewing the fee structure and any new covenants is essential before signing. This document serves as legal proof of continued liquidity, ensuring your business maintains the working capital necessary for daily operations and strategic growth opportunities.

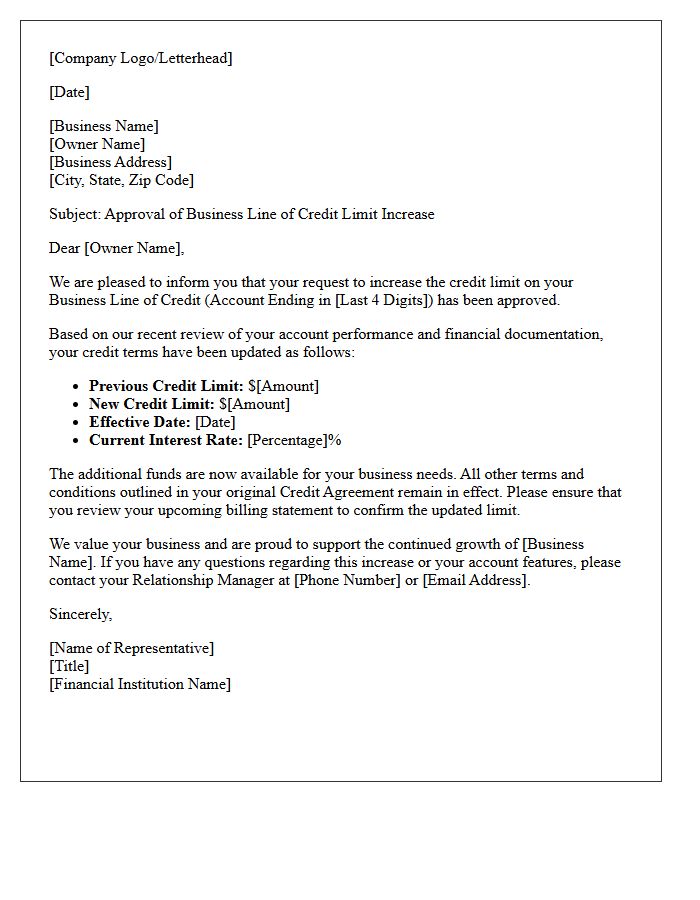

Business Line of Credit Limit Increase Approval Letter

A Business Line of Credit Limit Increase Approval Letter is a formal document confirming that a lender has authorized a higher borrowing capacity for your company. This notice specifies your new credit limit, updated interest rates, and any revised repayment terms. Receiving this approval enhances your working capital and provides greater financial flexibility for operational growth. It is essential to review the letter carefully to understand any additional collateral requirements or fees associated with the expanded credit facility before utilizing the increased funds.

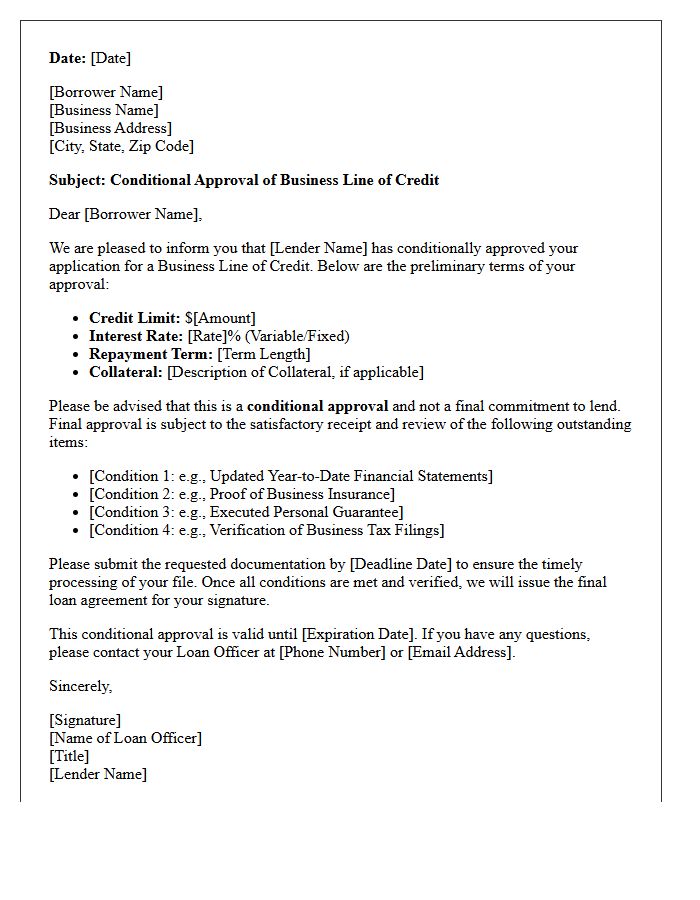

Conditional Business Line of Credit Approval Letter

A Conditional Business Line of Credit Approval Letter serves as a formal commitment from a lender, indicating that your business is eligible for financing subject to specific underwriting requirements. It outlines the preliminary credit limit and interest rates but is not a final guarantee. To secure funding, you must satisfy outstanding conditions, such as providing updated tax returns, verifying collateral value, or maintaining a stable credit score. Understanding these contingencies is essential for business owners to ensure they meet all milestones before the final loan disbursement occurs.

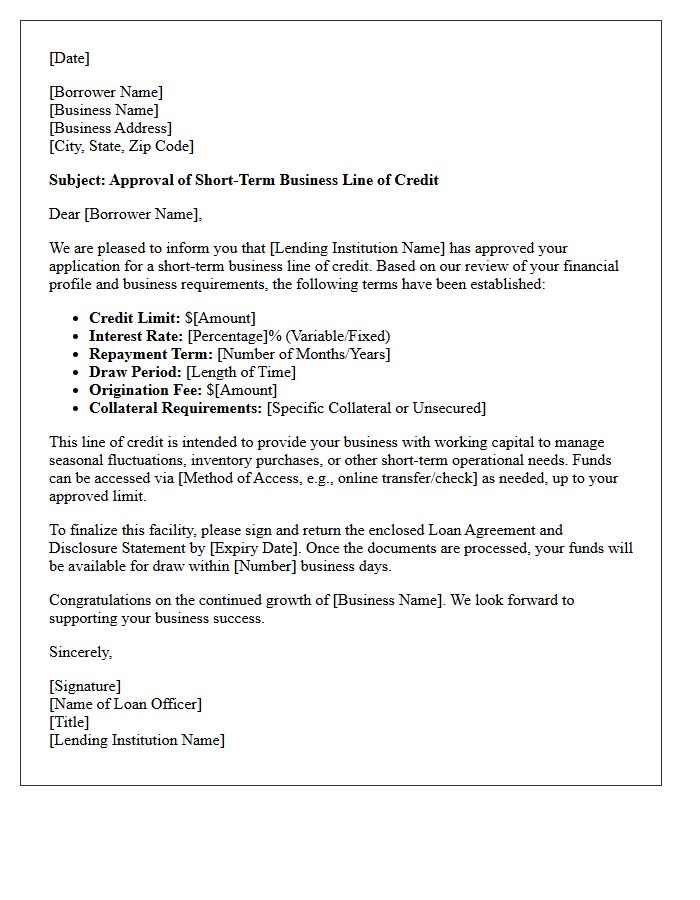

Short-Term Business Line of Credit Approval Letter

A short-term business line of credit approval letter is a formal document confirming that a lender has authorized your access to flexible funding. It outlines the maximum credit limit, interest rates, and specific repayment terms. Crucially, it signifies that your business has met the underwriting criteria regarding cash flow and creditworthiness. This letter serves as proof of available capital, allowing you to manage seasonal gaps or unexpected expenses. Reviewing the draw period and fee structure within this document is essential before accessing funds to ensure optimal financial management.

Enterprise Line of Credit Origination Approval Letter

An Enterprise Line of Credit Origination Approval Letter is a formal document confirming that a financial institution has authorized a borrowing limit for a business. This letter outlines the maximum credit capacity, applicable interest rates, and specific covenants the borrower must maintain. It serves as an official commitment, detailing the repayment terms and collateral requirements necessary to activate the funds. For corporations, this letter is a critical milestone in securing flexible working capital and ensuring long-term liquidity for operational growth or strategic investments.

What is a business line of credit approval letter?

A business line of credit approval letter is an official document issued by a lender notifying a business owner that their application for a revolving line of credit has been approved, detailing the maximum credit limit and borrowing terms.

What information is typically included in a business line of credit approval letter?

The letter generally includes the approved credit limit, the applicable interest rate (fixed or variable), repayment terms, draw period duration, any required collateral, and a list of closing conditions or outstanding documents needed to activate the line.

Does an approval letter mean the funds are immediately available?

Not necessarily. An approval letter signifies that the credit has been granted, but funds typically become available only after the business owner signs the final loan agreement and meets any final underwriting stipulations mentioned in the letter.

What is the difference between a pre-approval and a final business line of credit approval letter?

A pre-approval letter is a preliminary estimate based on basic data and credit scores, whereas a final approval letter is a binding commitment issued after the lender has completed a full review of the business's financial statements, tax returns, and bank records.

How long is a business line of credit approval letter valid?

Most approval letters are valid for a specific window, typically ranging from 30 to 60 days. If the business fails to execute the agreement within this timeframe, the lender may require updated financial documentation to re-verify the business's creditworthiness.

Comments