A Home Equity Line of Credit Approval Letter is a formal document from a lender confirming you have been cleared to access your home's equity. This letter outlines your borrowing limit, interest rates, and specific terms of the credit line. It serves as vital proof of financing for major projects or debt consolidation. To help you get started, below are some ready to use template.

Image cover: Official HELOC Approval Letter Templates and Professional Samples

Letter Samples List

- Standard Home Equity Line of Credit Approval Letter

- Conditional Home Equity Line of Credit Approval Letter

- Final Home Equity Line of Credit Approval Letter

- Variable-Rate Home Equity Line of Credit Approval Letter

- Fixed-Rate Option Home Equity Line of Credit Approval Letter

- Introductory Rate Home Equity Line of Credit Approval Letter

- High-Limit Home Equity Line of Credit Approval Letter

- Joint Applicant Home Equity Line of Credit Approval Letter

- Primary Residence Home Equity Line of Credit Approval Letter

- Investment Property Home Equity Line of Credit Approval Letter

- Expedited Home Equity Line of Credit Approval Letter

- Automated Decision Home Equity Line of Credit Approval Letter

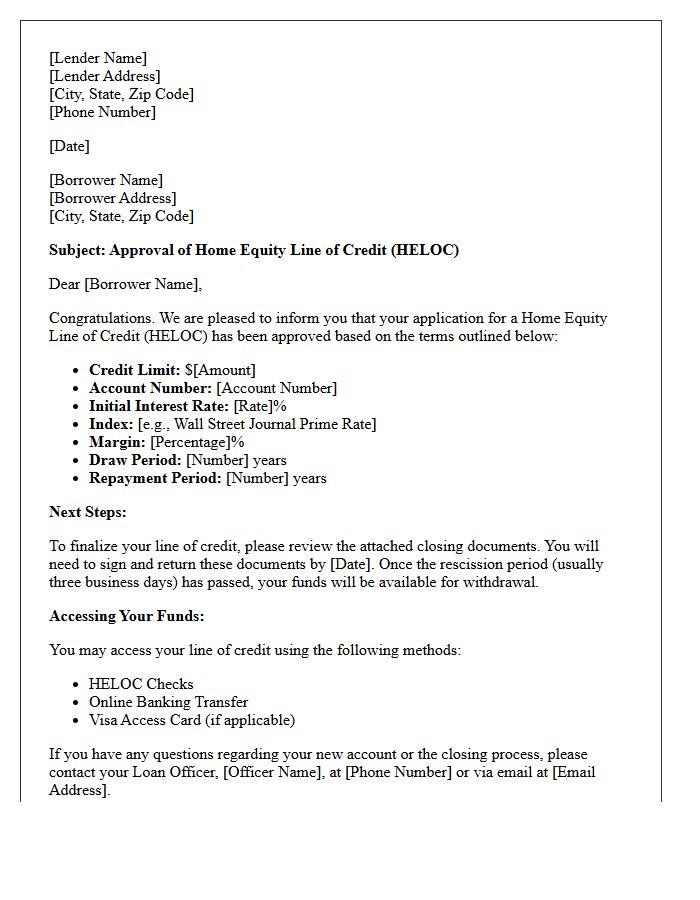

Standard Home Equity Line of Credit Approval Letter

A standard Home Equity Line of Credit (HELOC) Approval Letter confirms that a lender has verified your financial profile and committed to a specific credit limit. This document outlines essential terms, including the variable interest rate, draw period duration, and repayment conditions. It serves as official proof of your borrowing power, allowing you to access funds against your home's equity. Homeowners should carefully review the expiration date and any outstanding conditions required before the line of credit becomes active for property improvements or debt consolidation.

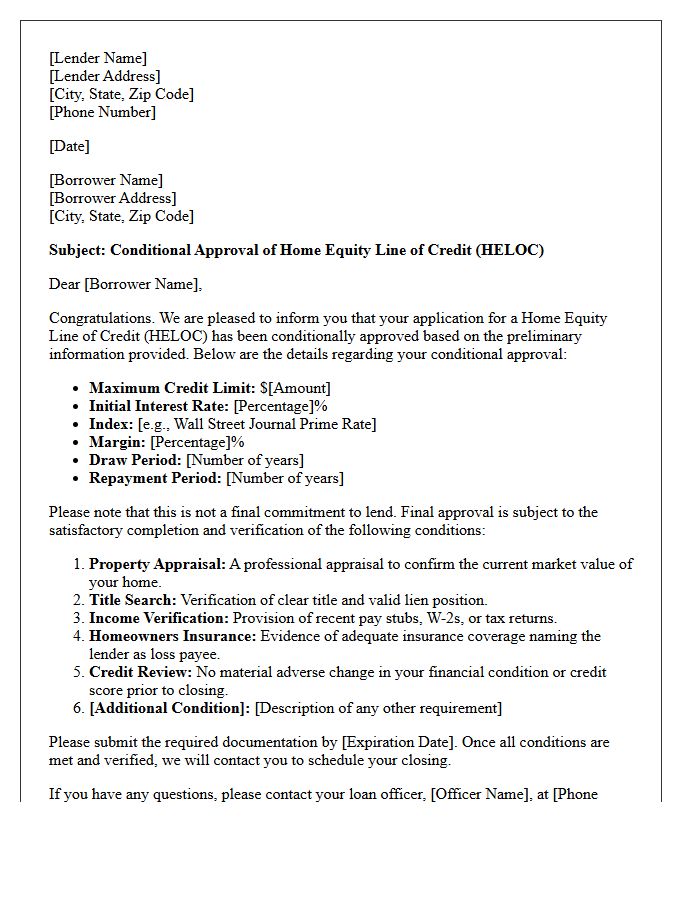

Conditional Home Equity Line of Credit Approval Letter

A Conditional Home Equity Line of Credit Approval Letter is a formal document issued by a lender indicating that your HELOC application is tentatively approved. It outlines specific conditions you must satisfy before final funding, such as property appraisals, income verification, or debt payoffs. This letter is not a final guarantee but signifies you meet initial credit and equity criteria. Reviewing these requirements promptly is essential to move toward the final approval stage and access your home's equity for flexible borrowing needs.

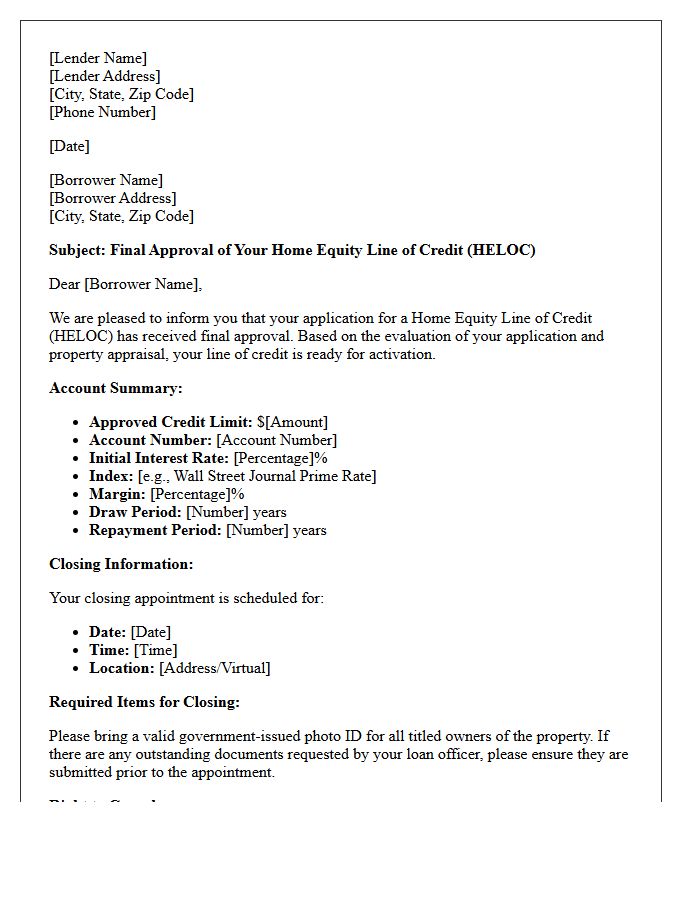

Final Home Equity Line of Credit Approval Letter

A Final Home Equity Line of Credit Approval Letter is the official document confirming your lender has cleared all contingencies. This commitment letter outlines your specific credit limit, variable interest rate, and the draw period duration. It signifies that underwriting is complete and you are ready for the closing process. Before signing, verify that the terms match your initial offer. Once executed, this letter grants you the legal right to access your home's equity as a revolving credit source for home improvements or debt consolidation.

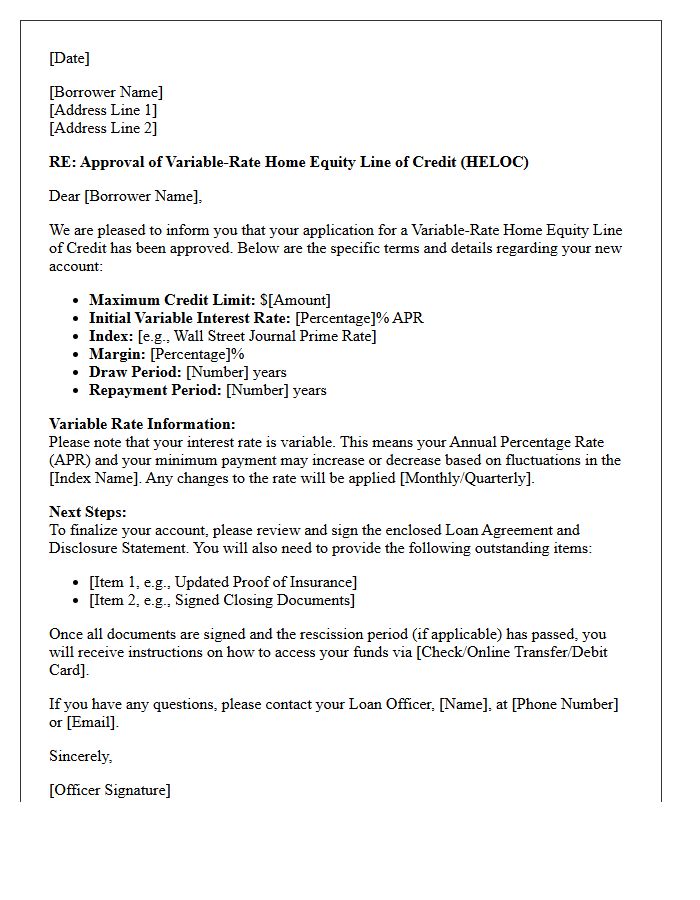

Variable-Rate Home Equity Line of Credit Approval Letter

A variable-rate HELOC approval letter confirms your credit limit based on home equity. It is crucial to understand that your interest rate is benchmarked to the prime rate, meaning monthly payments will fluctuate as market conditions change. The document outlines the draw period, repayment terms, and specific contingencies required for final funding. Reviewing the margin added to the index is essential, as this determines your long-term borrowing costs. This letter serves as formal proof of secondary financing, allowing you to access flexible funds for renovations or debt consolidation.

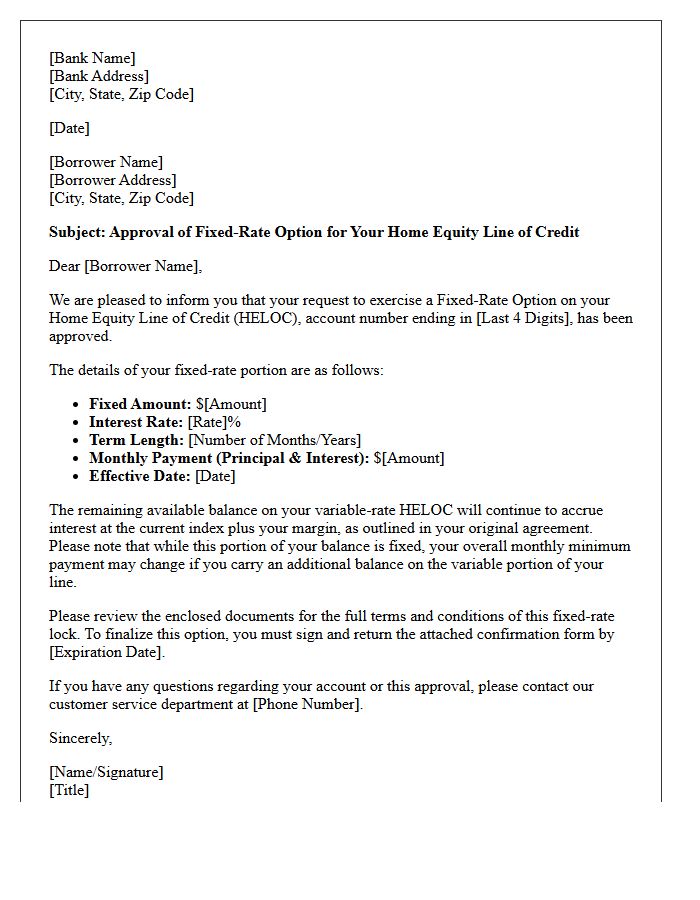

Fixed-Rate Option Home Equity Line of Credit Approval Letter

A Fixed-Rate Option Home Equity Line of Credit Approval Letter confirms your lender's commitment to your credit line while highlighting the Fixed-Rate Option. This feature allows you to convert variable-rate balances into stable, predictable monthly payments at a set interest rate. The letter details your maximum borrowing limit, specific repayment terms, and the lock-in requirements for converting debt. Reviewing this document is essential to understanding your repayment stability and protecting yourself against future market fluctuations while maintaining flexible access to your home's equity during the draw period.

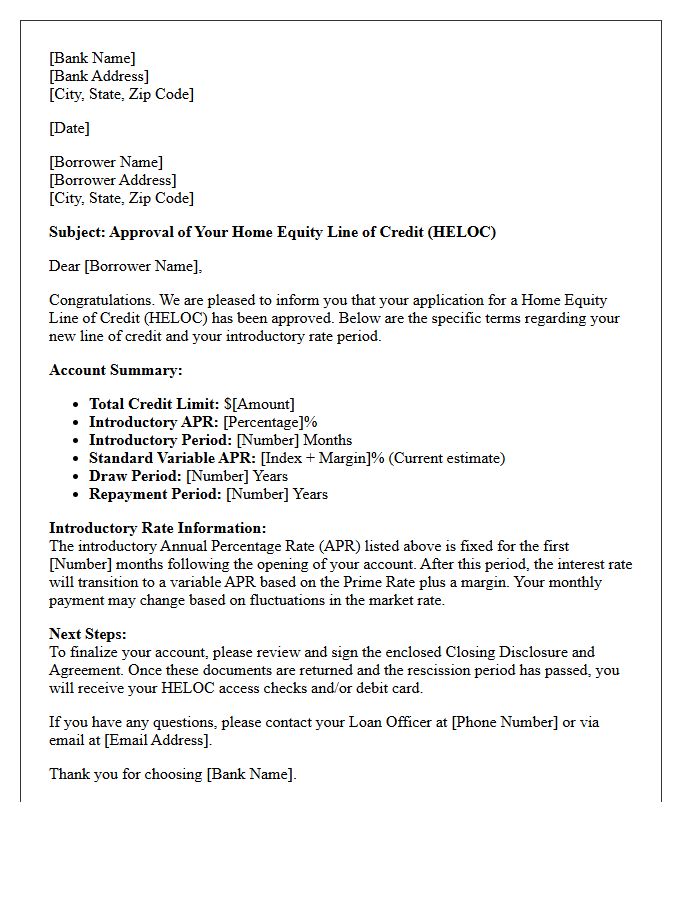

Introductory Rate Home Equity Line of Credit Approval Letter

An introductory rate HELOC approval letter confirms your preliminary qualification for a flexible credit line secured by home equity. This document outlines your initial borrowing limit and a temporary, low interest rate designed to reduce early repayment costs. It is crucial to verify the draw period duration and the variable rate adjustment terms that apply once the teaser period expires. Reviewing these conditions ensures you understand the transition to standard market rates and your long-term monthly payment obligations before finalizing the loan agreement.

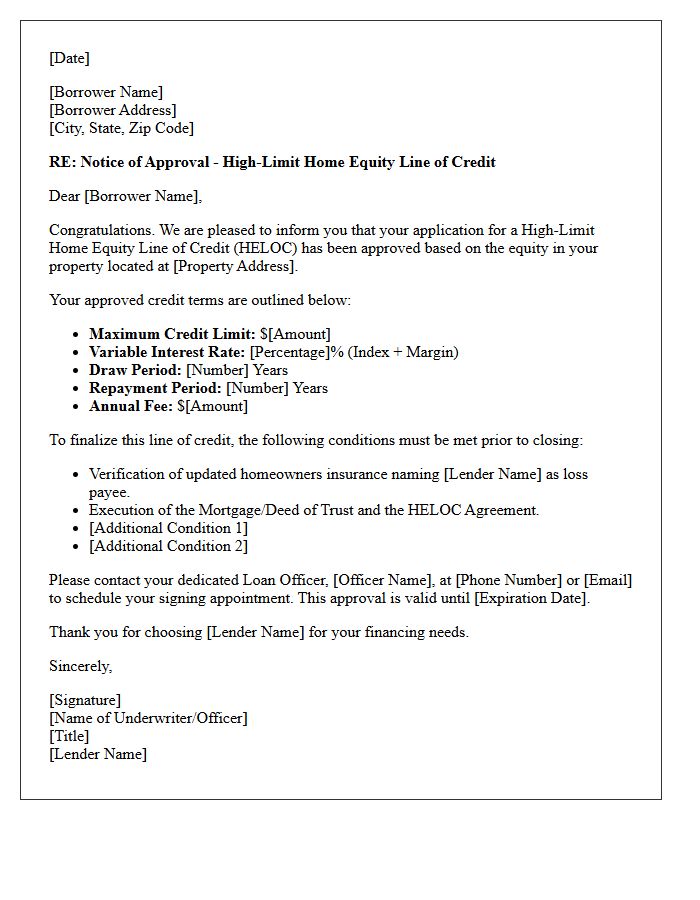

High-Limit Home Equity Line of Credit Approval Letter

A High-Limit Home Equity Line of Credit (HELOC) Approval Letter serves as official verification that a lender has authorized a substantial borrowing limit based on your property's value. This document specifies your maximum credit limit, the applicable interest rate, and the draw period duration. It is a critical financial tool for homeowners planning significant renovations or debt consolidation. Securing this letter confirms your borrowing power and provides the necessary documentation to move forward with large-scale projects or investments using your home's accumulated equity as collateral.

Joint Applicant Home Equity Line of Credit Approval Letter

A Joint Applicant HELOC Approval Letter confirms that two or more individuals are collectively approved for a credit line based on their combined income and creditworthiness. It is legally binding and specifies the maximum borrowing limit, interest rates, and draw period terms. Both parties share equal responsibility for repayment, meaning each applicant is liable for the total debt regardless of who spent the funds. Reviewing this document ensures all co-borrowers understand the lien placed on their property and the specific financial obligations required to maintain the account.

Primary Residence Home Equity Line of Credit Approval Letter

A primary residence home equity line of credit approval letter is a formal document confirming a lender's commitment to provide a revolving credit line secured by your home's equity. This letter outlines the maximum credit limit, variable interest rate, and specific draw period terms. It serves as proof of available financing, allowing homeowners to fund renovations or consolidate debt. Approval is strictly based on your combined loan-to-value ratio, credit score, and verified income, ensuring the borrower can manage the additional debt against their most valuable asset.

Investment Property Home Equity Line of Credit Approval Letter

An Investment Property HELOC Approval Letter is a formal document from a lender confirming you meet the specific criteria to access secondary financing. Unlike primary residences, investment properties often require higher credit scores and a lower combined loan-to-value ratio. This letter outlines your approved credit limit, the variable interest rate, and specific draw period terms. Obtaining this document is a critical step for real estate investors looking to leverage existing equity to fund renovations, cover down payments on new acquisitions, or maintain liquid capital for property-related expenses.

Expedited Home Equity Line of Credit Approval Letter

An Expedited Home Equity Line of Credit Approval Letter serves as a formal confirmation that a lender has fast-tracked your application based on preliminary financial data. This document highlights your pre-approved credit limit and estimated interest rate, providing the leverage needed for time-sensitive projects or real estate transactions. While it speeds up the initial process, final funding remains contingent upon a successful property appraisal and comprehensive title search. Obtaining this letter early helps homeowners secure immediate liquidity and demonstrates financial readiness to potential contractors or sellers.

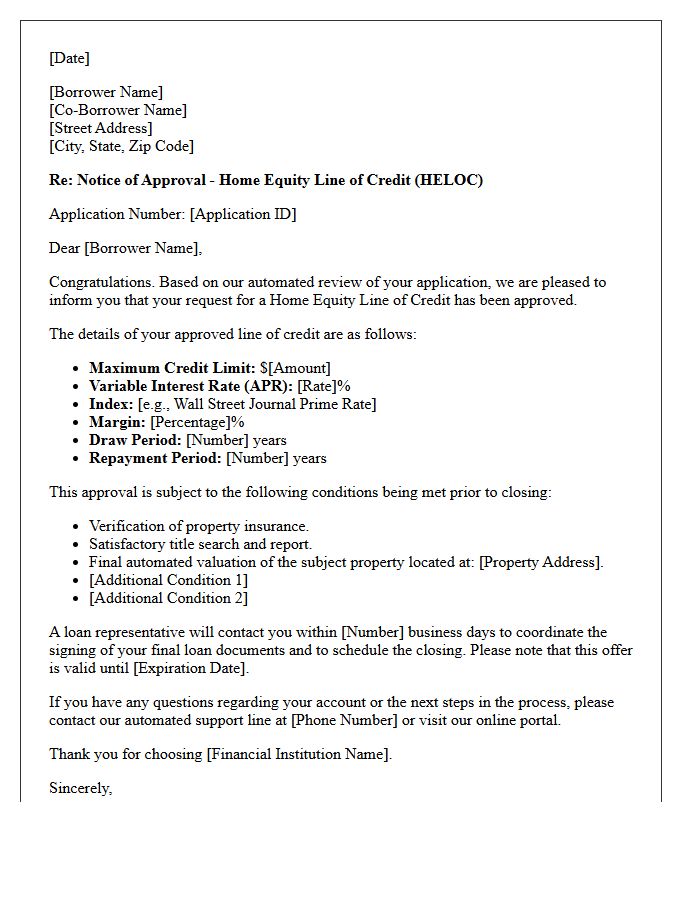

Automated Decision Home Equity Line of Credit Approval Letter

An Automated Decision Home Equity Line of Credit Approval Letter provides an immediate, algorithm-based preliminary verification of your borrowing eligibility. This document confirms that your credit profile and estimated property value meet specific lending criteria for a HELOC. While it accelerates the process, the approval remains conditional, pending final manual reviews of income documentation, property appraisals, and title searches. It serves as a vital indicator of your borrowing power, allowing homeowners to understand their potential credit limit and interest rates quickly before proceeding with formal underwriting steps.

What is a HELOC approval letter?

A HELOC approval letter is an official document from a lender confirming that a homeowner has been cleared for a Home Equity Line of Credit based on their creditworthiness, income, and available home equity.

How long does it take to receive a HELOC approval letter?

The timeline typically ranges from two to six weeks, as the process requires a full underwriting review, including a home appraisal, title search, and verification of the borrower's financial documentation.

What information is included in a Home Equity Line of Credit approval letter?

The letter details the maximum credit limit, the variable interest rate (margin plus index), the draw period duration, the repayment terms, and any specific conditions that must be met before closing.

Does a HELOC pre-approval letter guarantee funding?

No, a pre-approval letter is a preliminary estimate based on unverified data. Final funding is only guaranteed after a formal approval letter is issued following a successful appraisal and comprehensive underwriting check.

What can cause a lender to rescind a HELOC approval letter?

A lender may revoke approval if there is a significant drop in the borrower's credit score, a change in employment status, an increase in debt-to-income ratio, or if the home appraisal comes in lower than the required loan-to-value ratio.

Comments