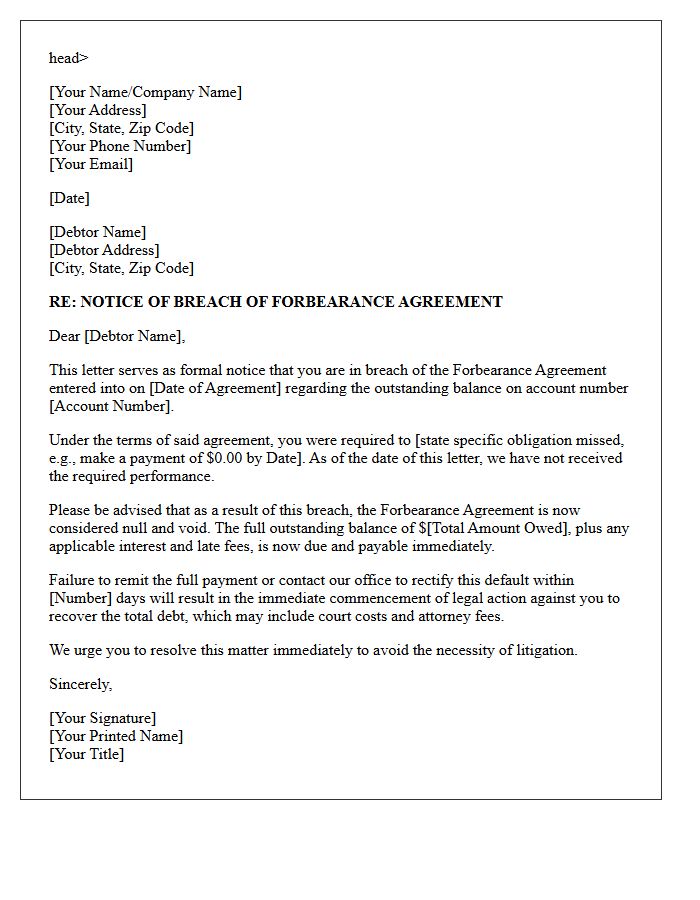

A Breach of Forbearance Agreement Notice is a formal legal document issued when a borrower fails to meet the specific repayment terms previously negotiated to delay foreclosure or legal action. It officially terminates the temporary relief period, allowing the lender to resume collection efforts. Understanding your rights and obligations is essential during this process. Below are some ready to use templates.

Image cover: Notice of Breach of Forbearance Agreement: Templates and Key Filing Samples

Letter Samples List

- Initial Notification of Forbearance Breach Letter

- Missed Forbearance Payment Warning Letter

- Notice of Default on Forbearance Terms Letter

- Demand to Cure Forbearance Agreement Breach Letter

- Urgent Forbearance Plan Delinquency Letter

- Intent to Terminate Forbearance Agreement Letter

- Cancellation of Forbearance Arrangement Letter

- Reinstatement of Original Debt Terms Letter

- Notice of Acceleration Following Forbearance Breach Letter

- Final Demand After Forbearance Default Letter

- Revocation of Forbearance Payment Plan Letter

- Pre-Legal Action Forbearance Breach Letter

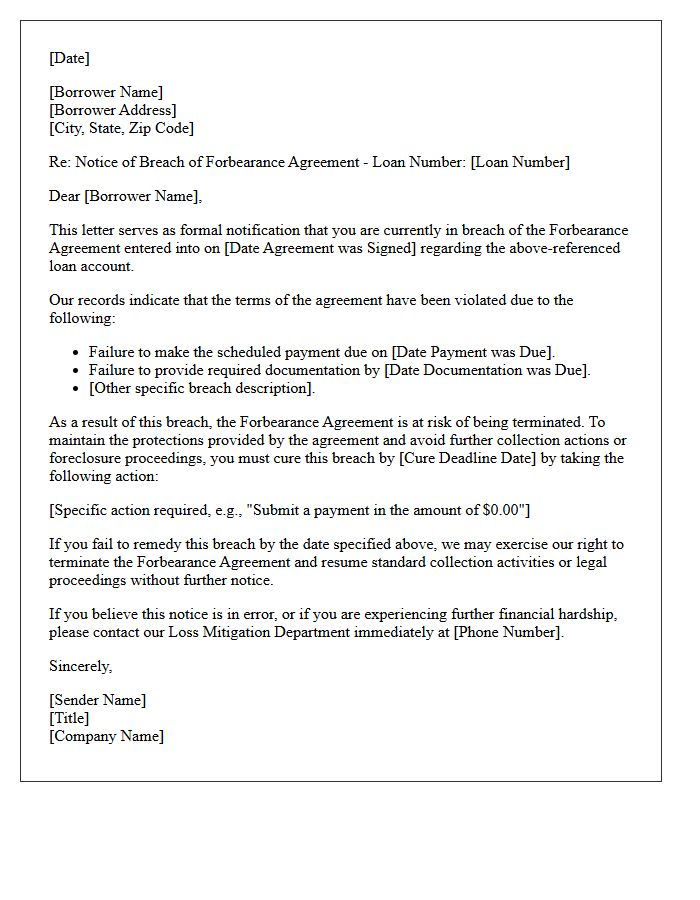

Initial Notification of Forbearance Breach Letter

An Initial Notification of Forbearance Breach Letter is a formal legal notice sent by a lender when a borrower fails to meet the specific terms of a repayment agreement. This critical document identifies the exact nature of the default and warns that the temporary protection from foreclosure has been revoked. Receiving this letter means the grace period has ended, and the lender may now initiate or resume legal action to recover the debt. Borrowers must act immediately to negotiate a loan modification or cure the delinquency to save their property.

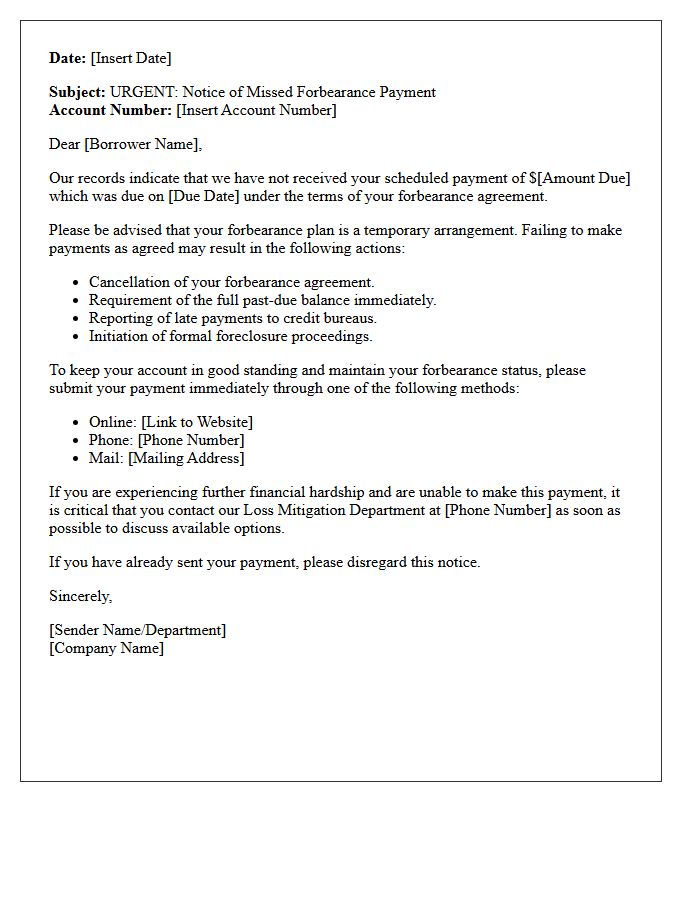

Missed Forbearance Payment Warning Letter

A Missed Forbearance Payment Warning Letter is a critical formal notice sent by lenders when a borrower fails to meet the specific terms of their repayment agreement. This document signals that your account is no longer in good standing, potentially triggering foreclosure proceedings. It is essential to contact your loan servicer immediately upon receipt to discuss reinstatement options or loan modifications. Ignoring this warning can lead to severe credit damage and the loss of your property. Timely communication is the most effective way to resolve delinquency and protect your home investment.

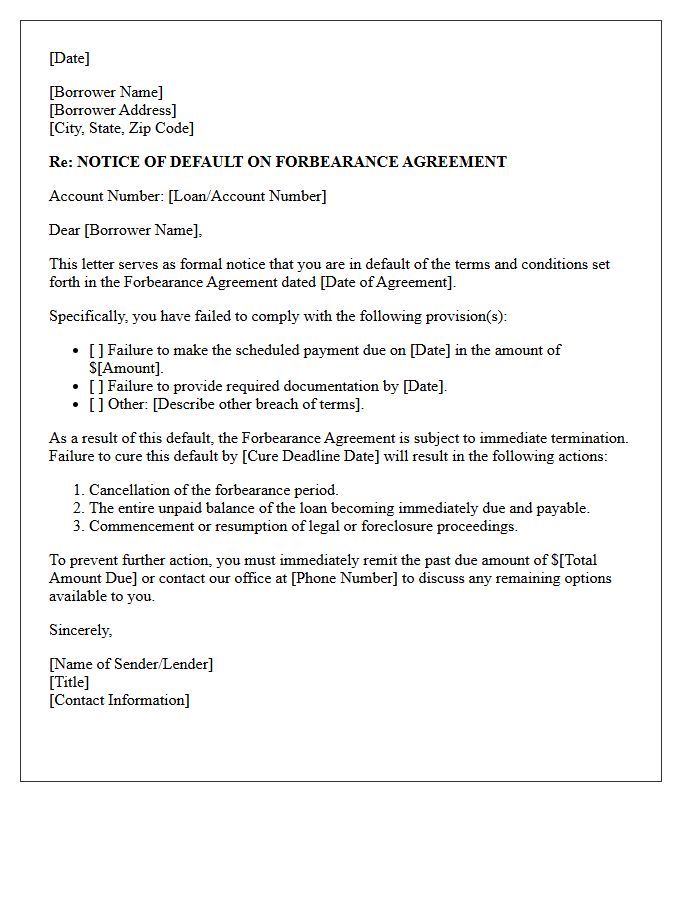

Notice of Default on Forbearance Terms Letter

A Notice of Default on Forbearance Terms Letter is a critical legal warning issued when a borrower fails to meet the specific repayment obligations outlined in a temporary relief agreement. Receiving this document signifies that the lender may soon initiate foreclosure proceedings. It serves as formal notification that the protective grace period has ended due to a breach of contract. Homeowners must act immediately by contacting their loan servicer to explore alternative loss mitigation options or legal remedies to prevent losing their property title and permanent credit damage.

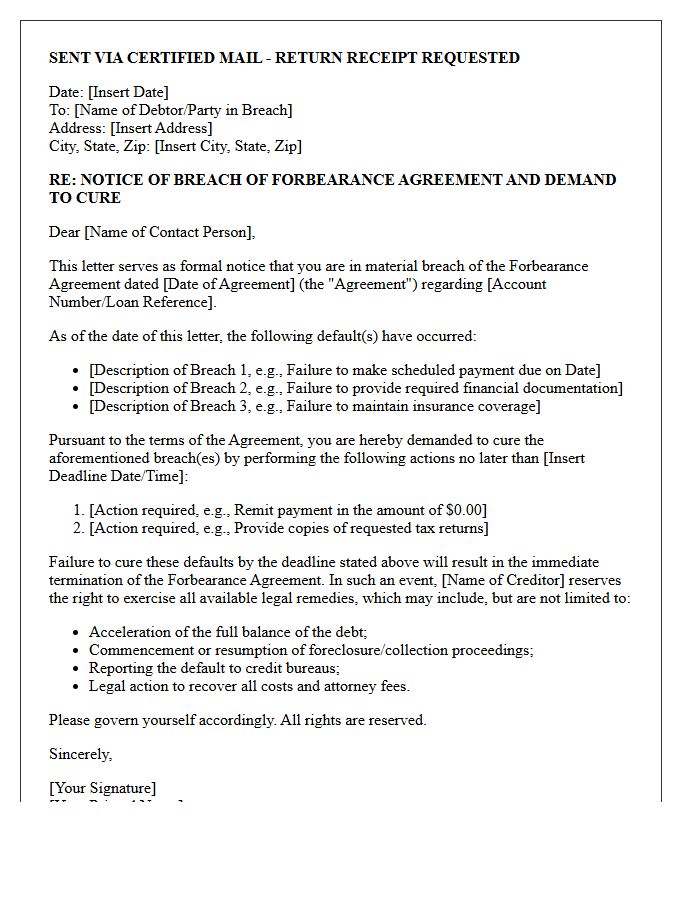

Demand to Cure Forbearance Agreement Breach Letter

A Demand to Cure letter is a formal notice sent when a borrower violates terms within a forbearance agreement. This legal document identifies the specific default and provides a deadline to rectify the breach before the lender resumes foreclosure actions. It is crucial to respond immediately, as failing to restate compliance can result in the loss of temporary payment relief and the acceleration of the entire loan balance. Timely action is the only way to protect your property and preserve the existing workout arrangement with your mortgage servicer.

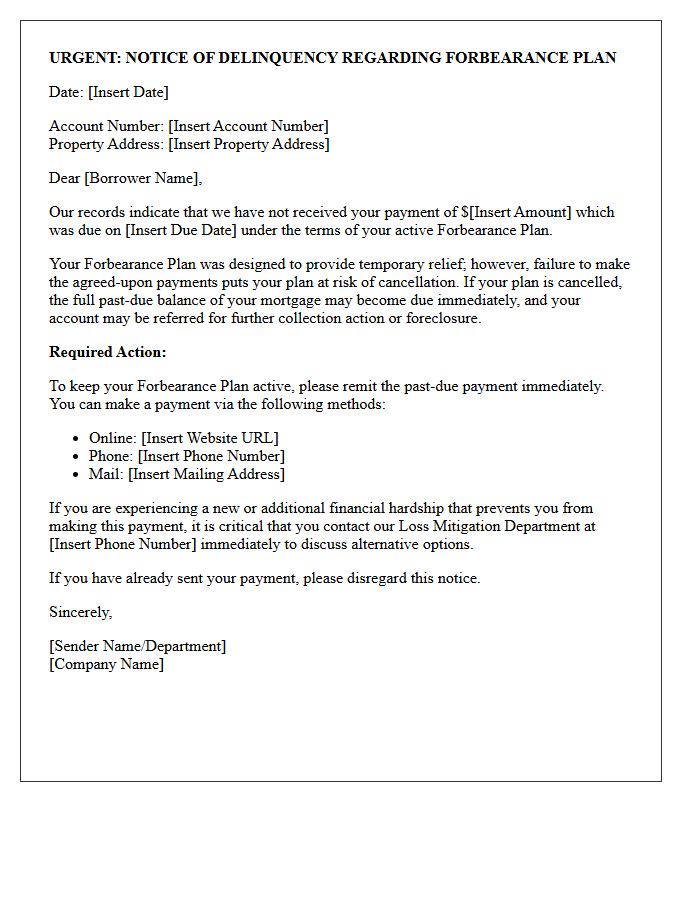

Urgent Forbearance Plan Delinquency Letter

An Urgent Forbearance Plan Delinquency Letter is a critical notice sent when a homeowner misses payments required by their mortgage relief agreement. This document serves as a final warning that your repayment status is at risk, potentially leading to the cancellation of the plan. Receiving this letter means you must take immediate action to address the past-due balance. Contacting your loan servicer promptly is essential to discuss loss mitigation options, prevent formal foreclosure proceedings, and protect your long-term housing stability during financial hardship.

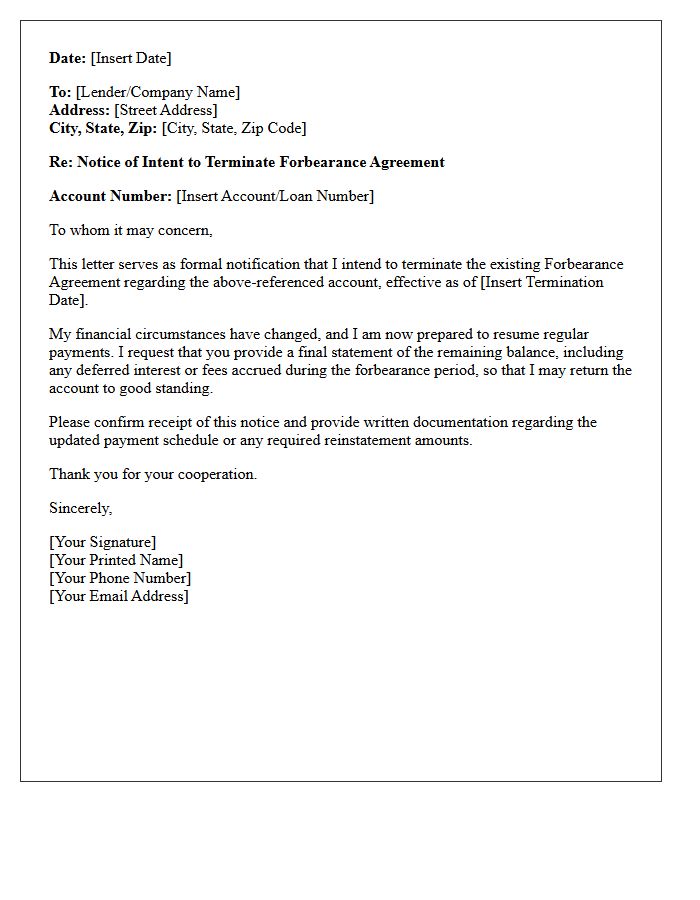

Intent to Terminate Forbearance Agreement Letter

An Intent to Terminate Forbearance Agreement Letter is a formal notice sent by a lender to a borrower when terms are breached. It signifies the end of temporary payment relief, often due to missed payments or the expiration of the agreed period. This document is critical because it marks the transition toward foreclosure or legal recovery actions. Borrowers must act immediately upon receipt to negotiate a loan modification or repayment plan to protect their property rights and credit standing. Understanding this default notice is essential for maintaining financial security.

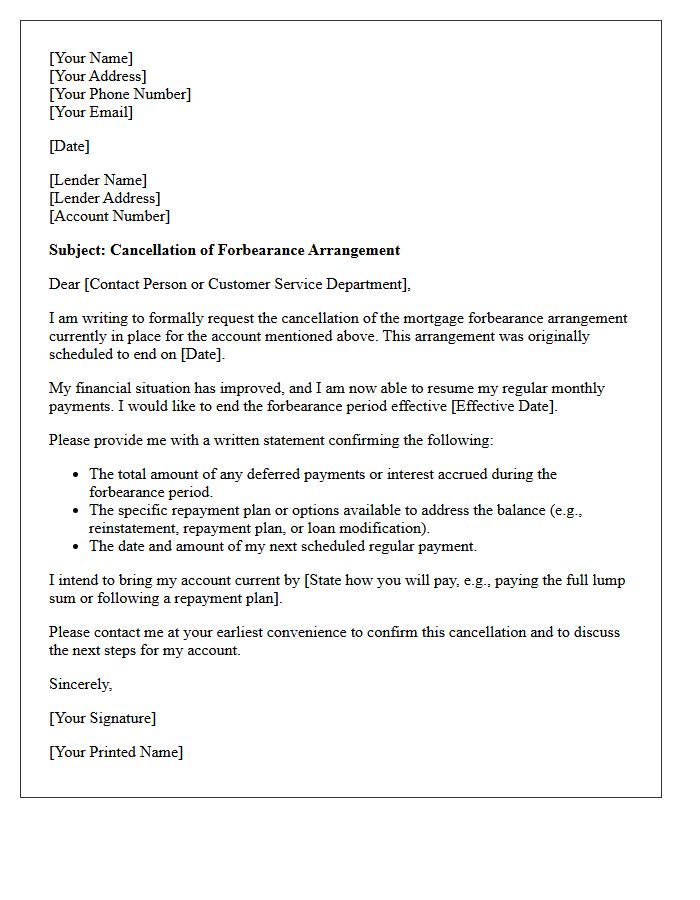

Cancellation of Forbearance Arrangement Letter

A Cancellation of Forbearance Arrangement Letter is a formal notice stating that the temporary pause or reduction of loan payments has ended. It is crucial to understand that regular payment obligations will resume immediately. Borrowers should carefully review the repayment terms outlined in the letter to avoid default. If you cannot afford the full installments, contact your lender to discuss loss mitigation options or a loan modification. Promptly acknowledging this letter ensures you remain in good standing and protects your credit score from negative reporting due to missed payments.

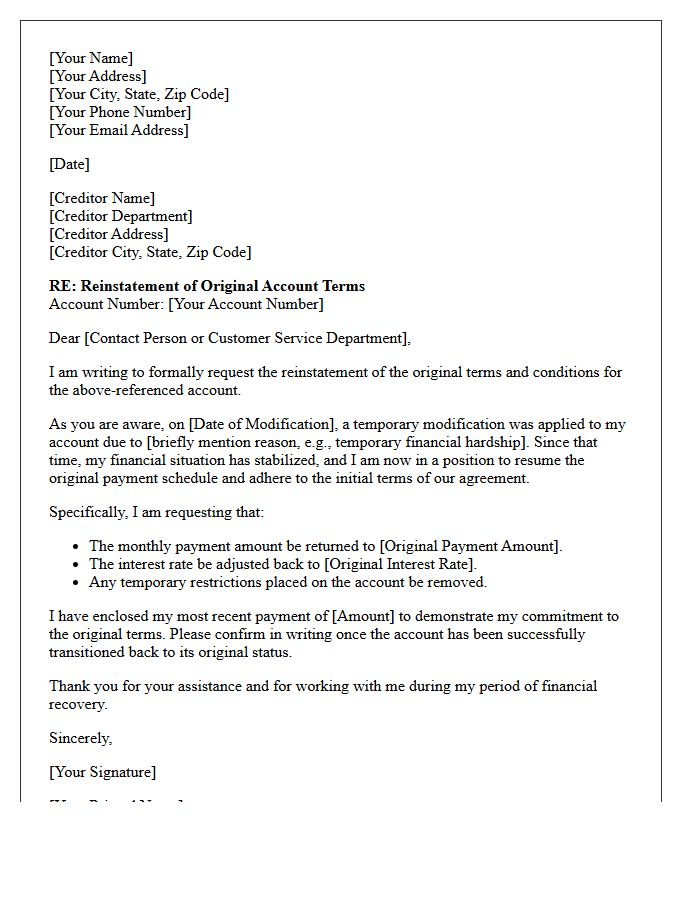

Reinstatement of Original Debt Terms Letter

A Reinstatement of Original Debt Terms Letter is a critical formal notice confirming that a borrower has successfully rectified a default. By paying the total arrears and associated fees, the debtor restores the contractual agreement to its initial state. This legal document effectively cancels any acceleration of the balance, allowing for regular monthly payments to resume. It serves as essential proof that the loan is no longer in jeopardy of foreclosure or legal action, ensuring your financial standing is protected under the original terms of the promissory note.

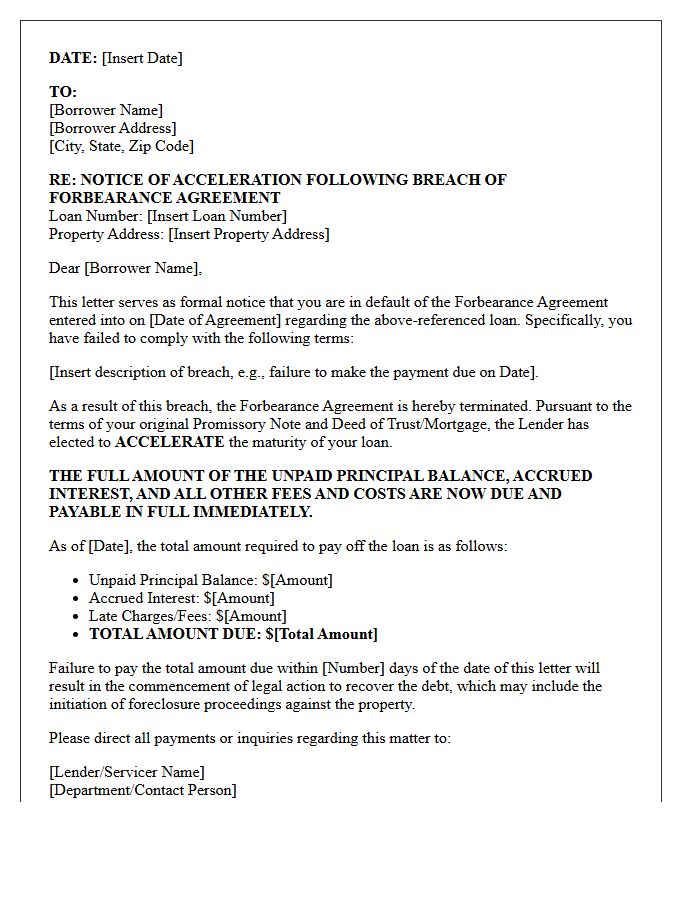

Notice of Acceleration Following Forbearance Breach Letter

A Notice of Acceleration Following Forbearance Breach is a critical legal document informing a borrower that their repayment agreement has been violated. By failing to meet the specific terms of a forbearance plan, the lender invokes the acceleration clause, demanding the entire remaining mortgage balance be paid immediately. This formal notice typically serves as the final step before the foreclosure process begins. Borrowers must act quickly to cure the default or seek legal counsel to prevent the permanent loss of their property through a forced judicial or non-judicial sale.

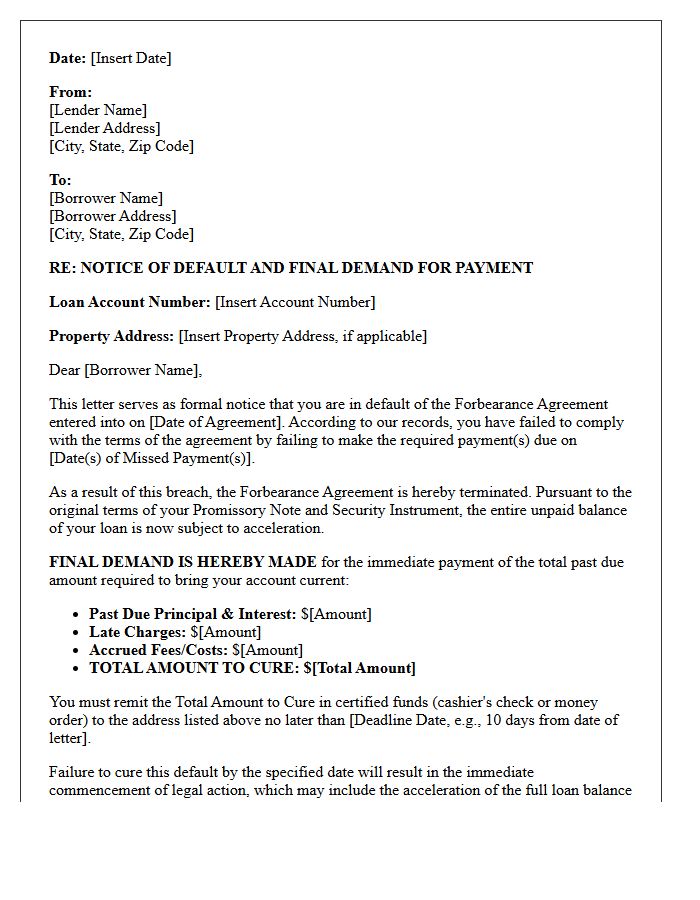

Final Demand After Forbearance Default Letter

A Final Demand After Forbearance Default Letter is a critical legal notice issued when a borrower fails to meet the terms of a repayment plan. This document signifies the termination of temporary relief and serves as a formal warning before the lender initiates foreclosure proceedings. It outlines the total outstanding balance, including late fees and interest, that must be paid immediately to cure the default. Receiving this letter indicates that the grace period has ended, making it essential for homeowners to seek legal advice or contact their servicer to explore final loss mitigation options.

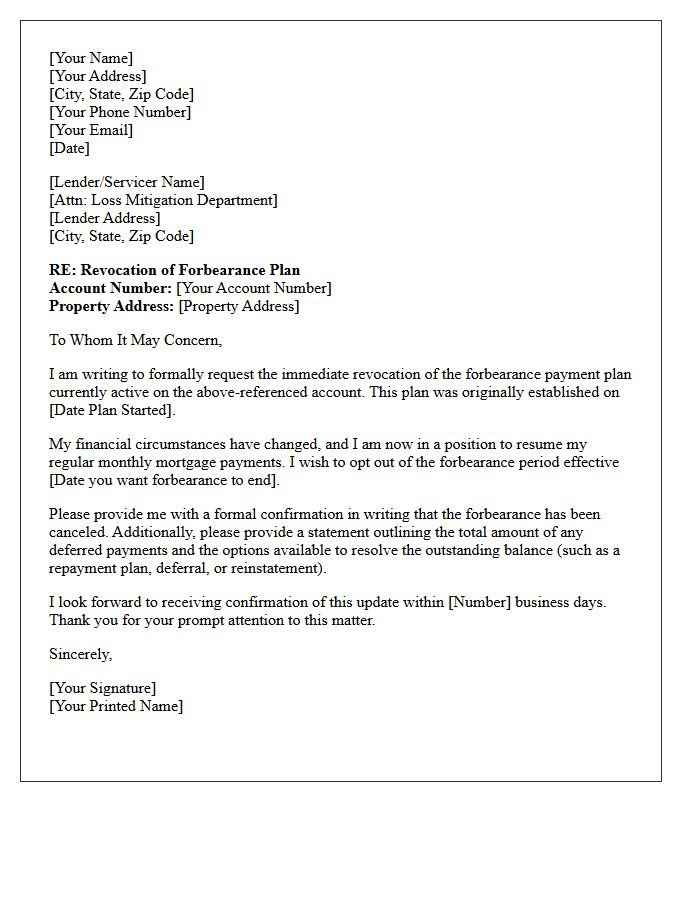

Revocation of Forbearance Payment Plan Letter

A Revocation of Forbearance Payment Plan Letter is a formal notice used to cancel an existing agreement between a borrower and a lender. It officially terminates the temporary suspension or reduction of mortgage payments, often triggered when a homeowner decides to resume regular installments or transition into a permanent loan modification. Understanding this document is crucial because it outlines your new repayment obligations and prevents foreclosure proceedings. Always verify the effective date to ensure your financial records remain accurate and to avoid unintentional payment defaults during the transition period.

Pre-Legal Action Forbearance Breach Letter

A Pre-Legal Action Forbearance Breach Letter is a formal notice sent to a borrower who has failed to meet the terms of a repayment agreement. This critical document serves as a final warning, detailing the specific violations and the outstanding balance due. It notifies the debtor that legal proceedings or foreclosure will commence unless the default is cured within a set timeframe. Receiving this letter indicates that the lender is transitioning from informal negotiations to enforcement actions to recover the debt, making immediate professional legal or financial advice essential.

What is a Breach of Forbearance Agreement Notice?

A Breach of Forbearance Agreement Notice is a formal legal document issued by a lender to a borrower stating that the borrower has failed to comply with the specific terms, payment schedules, or conditions outlined in a previously signed forbearance agreement.

What are the common causes for receiving a Notice of Breach of Forbearance?

Common causes include missing a scheduled partial payment, failing to pay the remaining balance by the expiration date, violating property maintenance requirements, or failing to provide required financial documentation as stipulated in the agreement.

What happens after a Breach of Forbearance Agreement Notice is issued?

Once a breach notice is issued, the lender typically terminates the forbearance period and resumes the original foreclosure or collection process. The borrower loses the protections of the agreement, and the full outstanding debt may become immediately due via acceleration.

Can you cure a breach of a forbearance agreement?

Whether a breach can be cured depends on the specific "right to cure" clause within the agreement. Some contracts allow a short grace period to remedy the default, while many others state that any single violation results in an automatic and irreversible default of the arrangement.

What should I do if I receive a Breach of Forbearance Agreement Notice?

You should immediately review the notice for accuracy, identify the specific default cited, and contact your lender to discuss potential loss mitigation options or a loan modification. Consulting with a legal professional is recommended to protect your rights and explore remaining ways to prevent foreclosure.

Comments