A Comfort Letter serves as a vital assurance document in real estate development financing, bridging the gap between lenders and developers. It outlines a parent company's commitment to support a subsidiary's financial obligations, enhancing project credibility and mitigating risk for investors. This guide explores its legal significance and strategic role in securing funding. Below are some ready to use template.

Image cover: Securing Real Estate Financing: Professional Comfort Letter Templates and Strategic Samples

Letter Samples List

- Parent Company Financial Support Comfort Letter

- Sponsor Cost Overrun Assurance Comfort Letter

- Syndicated Lending Bank Comfort Letter

- Certified Auditor Financial Projection Comfort Letter

- General Contractor Project Completion Comfort Letter

- Takeout Lender Permanent Financing Comfort Letter

- Equity Investor Capital Call Comfort Letter

- Anchor Tenant Pre-Lease Commitment Comfort Letter

- Municipal Zoning And Planning Comfort Letter

- Environmental Agency Site Clearance Comfort Letter

- Government Infrastructure Support Comfort Letter

- Mezzanine Lender Subordination Comfort Letter

- Debt Service Reserve Assurance Comfort Letter

- Insurance Provider Risk Coverage Comfort Letter

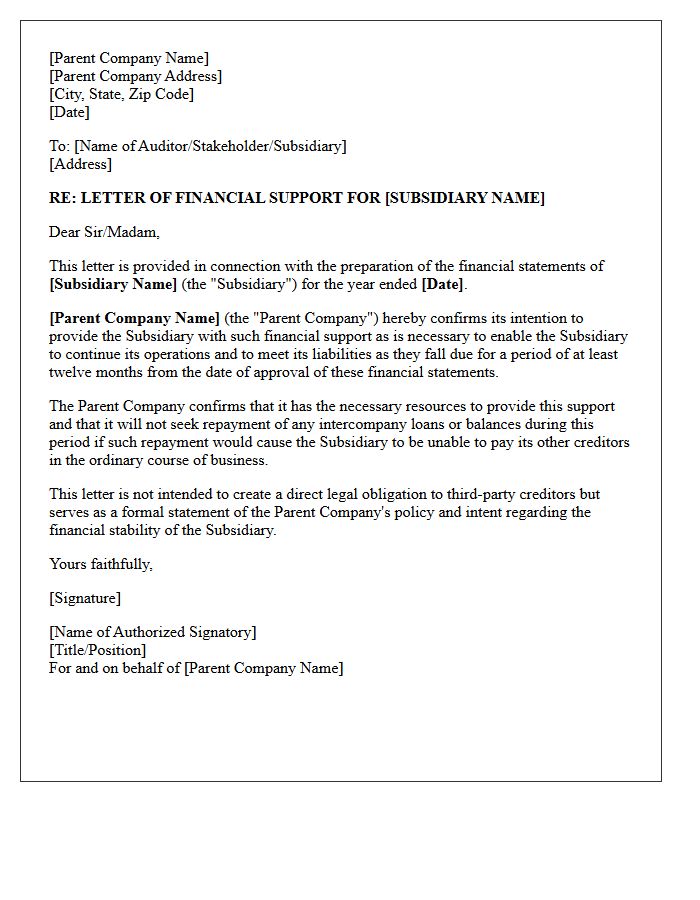

Parent Company Financial Support Comfort Letter

A parent company financial support comfort letter is a document issued to a subsidiary's auditors or lenders to confirm financial backing. Although often legally non-binding, it serves as a critical assurance that the parent intends to maintain the subsidiary's solvency and liquidity. These letters are essential for "going concern" assessments, helping subsidiaries meet audit requirements when their independent finances are weak. However, parties must carefully distinguish between a moral statement of intent and a formal guarantee to understand the actual level of enforceable liability involved.

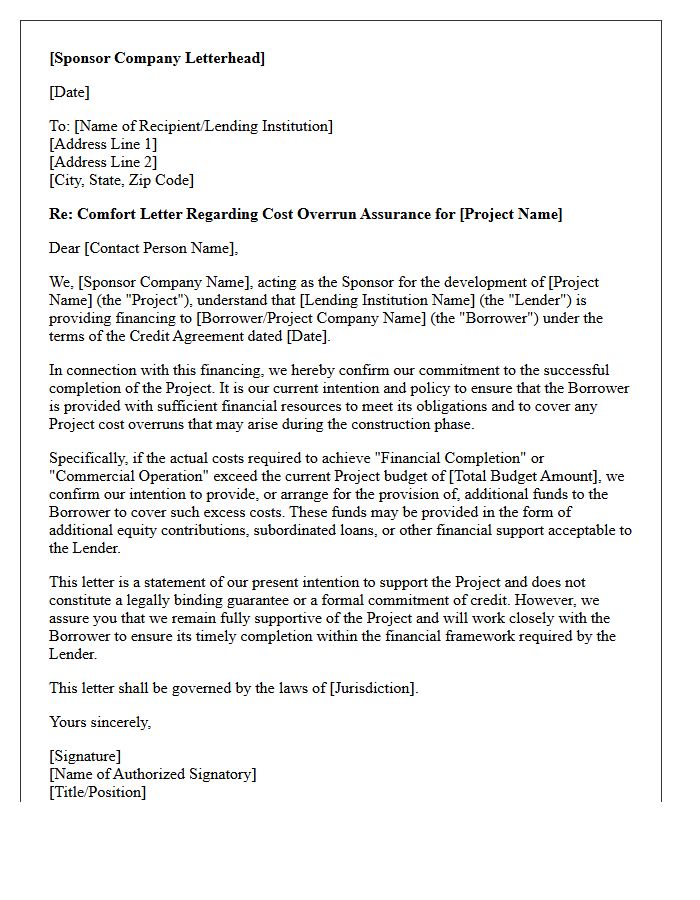

Sponsor Cost Overrun Assurance Comfort Letter

A Sponsor Cost Overrun Assurance Comfort Letter is a financial guarantee issued by a project sponsor to lenders. It provides credit enhancement by formally committing the sponsor to cover any unexpected expenses exceeding the initial budget. This document ensures project completion by mitigating funding risks during the construction phase. Although often considered a moral rather than a strictly legal obligation in some jurisdictions, it serves as a critical security instrument to maintain liquidity and protect senior debt holders from unforeseen capital shortfalls in large-scale infrastructure or energy projects.

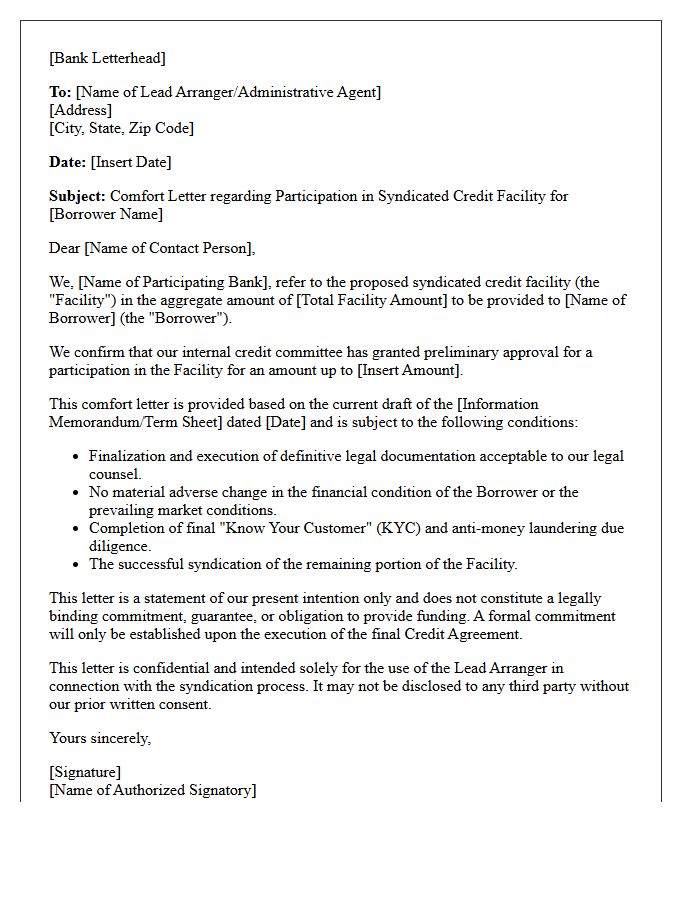

Syndicated Lending Bank Comfort Letter

A Syndicated Lending Bank Comfort Letter is a formal document issued by a parent company or third party to reassure lenders about a borrower's financial obligations. While it expresses support and intent to maintain creditworthiness, it is generally considered a non-binding moral commitment rather than a legal guarantee. In large-scale syndications, these letters provide vital psychological security and clarify the relationship between entities, helping to mitigate perceived risk during the underwriting process without appearing as a formal liability on the issuer's balance sheet.

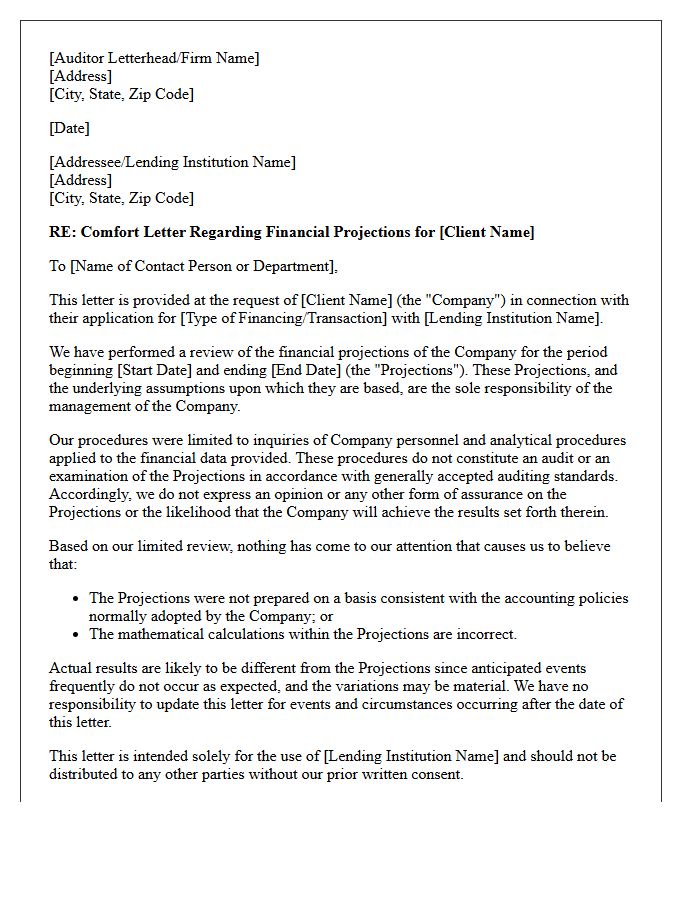

Certified Auditor Financial Projection Comfort Letter

A Certified Auditor Financial Projection Comfort Letter provides limited assurance to lenders or underwriters regarding the consistency and mathematical accuracy of a company's forward-looking statements. It confirms that prospective financial data is prepared using the same accounting policies as historical audits. This document is essential during due diligence or debt offerings to mitigate financial risk and validate that projections are based on reasonable assumptions. While not a guarantee of future results, it increases transparency and investor confidence by verifying the rigorous methodology used to develop future financial outlooks.

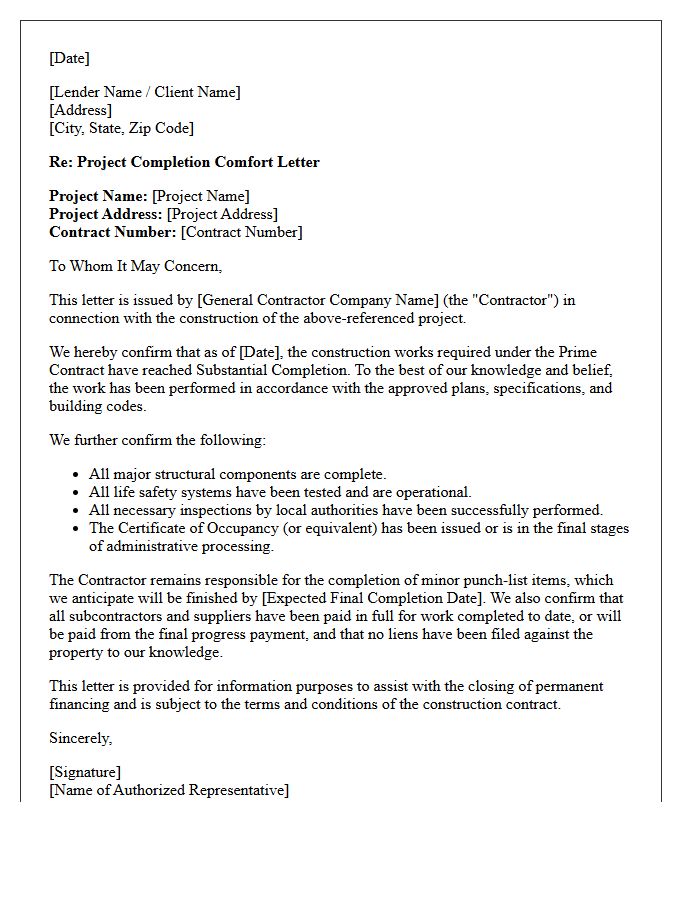

General Contractor Project Completion Comfort Letter

A General Contractor Project Completion Comfort Letter is a formal document confirming that a construction project has reached substantial completion according to the contract terms. It provides financial stakeholders and owners with legal assurance that the work is finished, inspections are passed, and the property is ready for its intended use. This letter is essential for releasing final payments, triggering warranty periods, and securing permanent financing. By certifying that all contractual obligations are met, it mitigates risk and ensures a smooth transition from construction to operational occupancy.

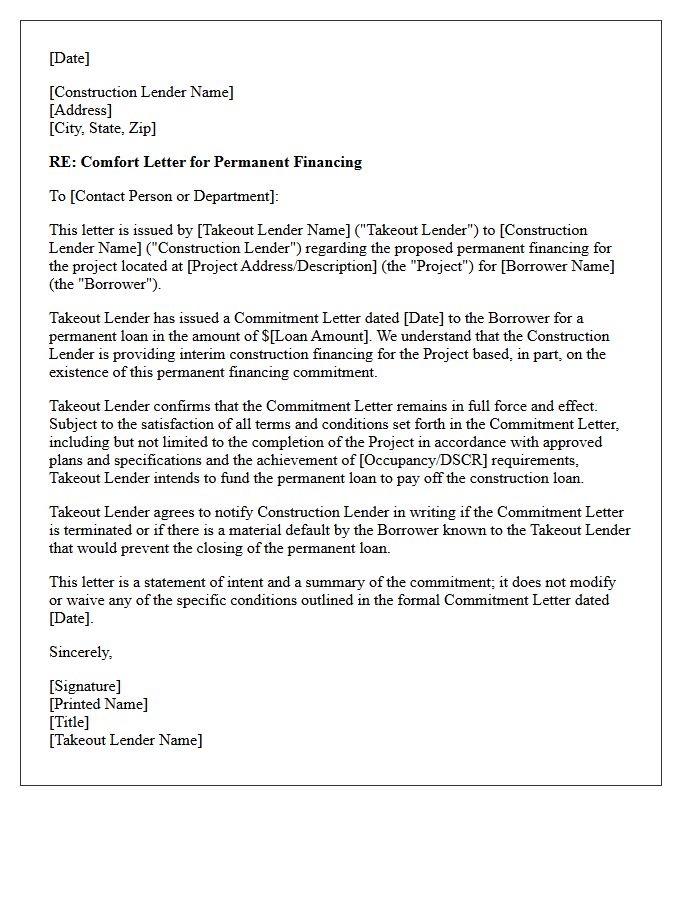

Takeout Lender Permanent Financing Comfort Letter

A Takeout Lender Permanent Financing Comfort Letter is a critical document provided by a long-term financier to a construction lender. It outlines the commitment to provide permanent financing once project milestones are met. This letter mitigates risk by ensuring a clear exit strategy for the short-term loan. Developers must understand that while it offers assurance, it is often conditional upon specific underwriting criteria, lease-up targets, and final inspections. It bridges the gap between construction completion and long-term stability, securing the financial transition of the asset.

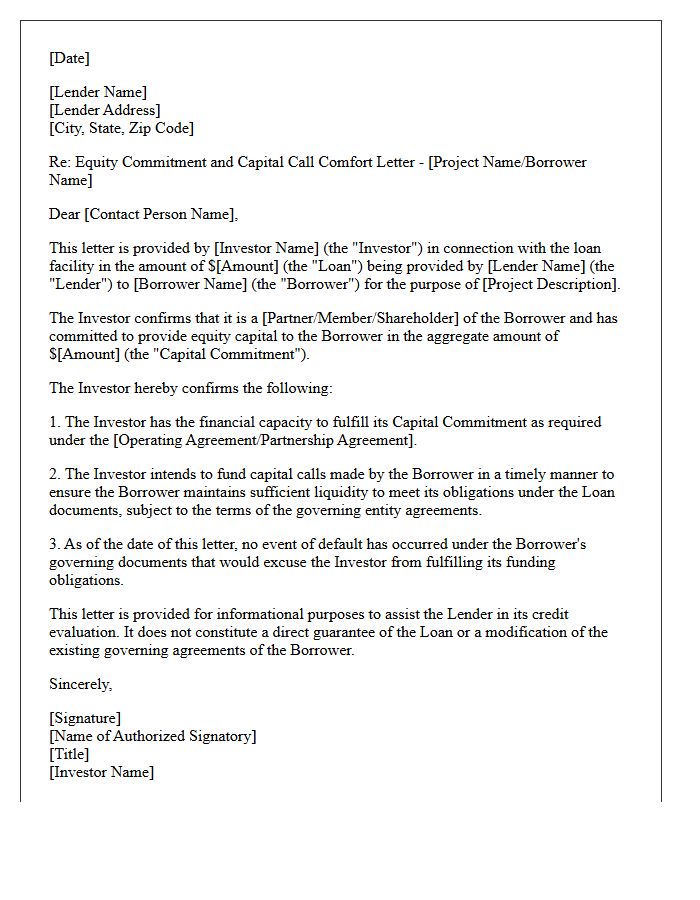

Equity Investor Capital Call Comfort Letter

An Equity Investor Capital Call Comfort Letter provides a lender with assurance that a sponsor is committed to funding a project. This document confirms that the investor has the financial capacity and intent to meet future capital calls if needed. While typically not a direct guarantee of payment, it reduces risk by verifying equity availability and strengthening the credit profile of the borrower. It serves as a vital bridge of trust between lenders and shareholders, ensuring that sufficient liquidity remains accessible throughout the lifecycle of a transaction or investment vehicle.

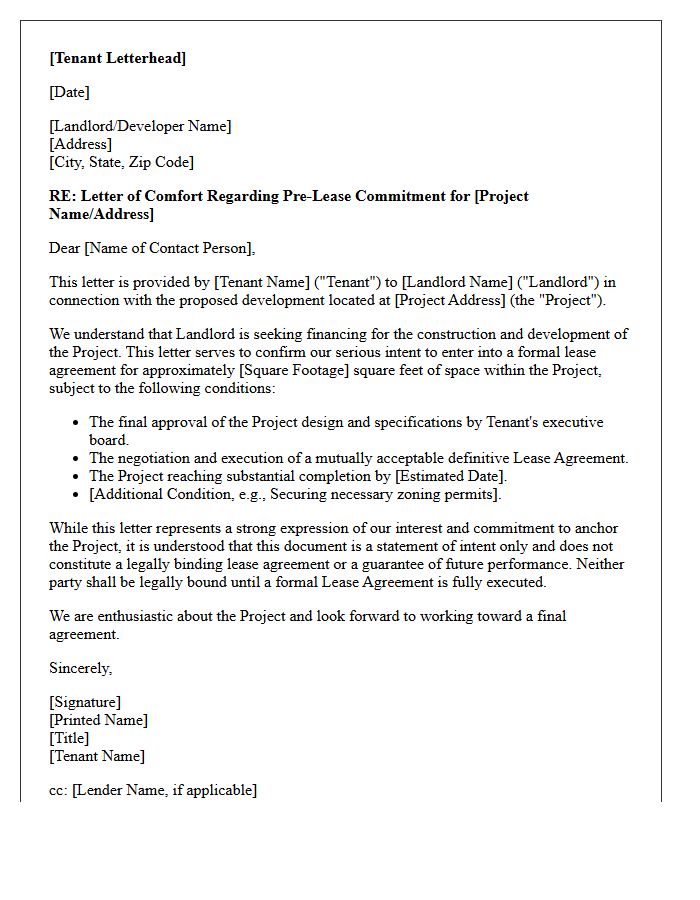

Anchor Tenant Pre-Lease Commitment Comfort Letter

An Anchor Tenant Pre-Lease Commitment Comfort Letter provides critical assurance to lenders and developers during the early stages of project financing. This document confirms a primary tenant's intent to occupy space, establishing financial viability and reducing risk for stakeholders. While typically non-binding, it serves as a vital signal of market demand and creditworthiness. Securing this commitment is an essential milestone in unlocking construction capital, ensuring that the development has the necessary rental security to proceed with large-scale commercial or retail investments.

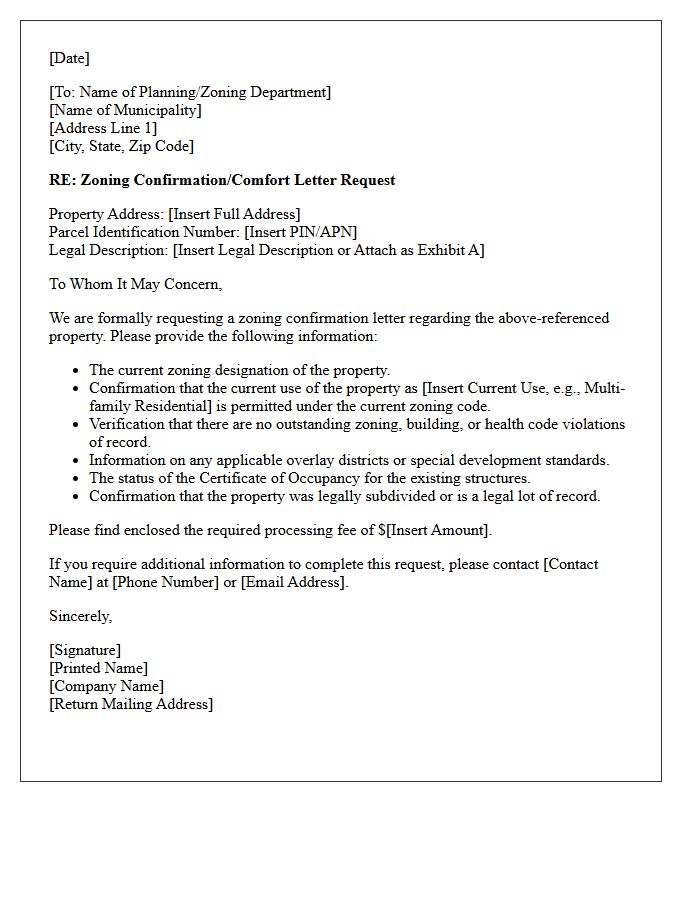

Municipal Zoning And Planning Comfort Letter

A Municipal Zoning and Planning Comfort Letter is a formal document issued by local authorities to confirm a property's compliance with land-use regulations. It verifies the current zoning designation, identifies any outstanding work orders, and confirms if existing structures follow legal requirements. Lenders and buyers typically request this letter during due diligence to mitigate risks related to non-conforming uses or building violations. While not a definitive guarantee against all legal issues, it provides essential administrative assurance that the property aligns with municipal bylaws and development standards.

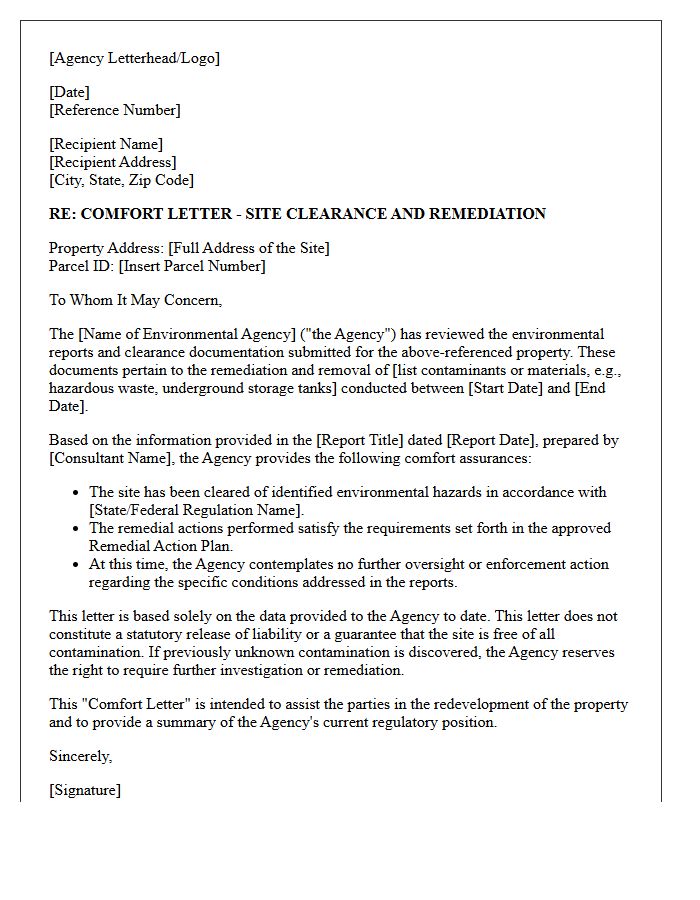

Environmental Agency Site Clearance Comfort Letter

An Environmental Agency Site Clearance Comfort Letter provides regulatory assurance that a previously contaminated site has been sufficiently remediated for its intended use. This document is vital for risk management during property transactions, helping developers and lenders confirm that the authority is satisfied with the cleanup efforts. While it does not offer absolute legal immunity, it significantly reduces the likelihood of future enforcement action. Obtaining this letter is a key step in due diligence, ensuring the land is safe for redevelopment and increasing overall project marketability.

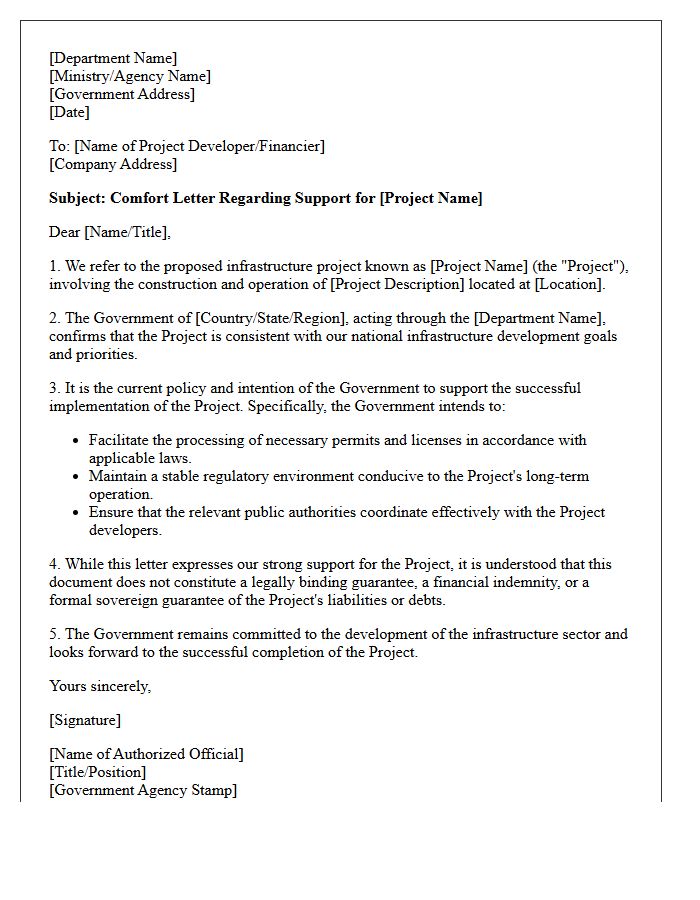

Government Infrastructure Support Comfort Letter

A Government Infrastructure Support Comfort Letter is a non-binding policy statement issued to lenders or investors. It demonstrates the state's intent to support a specific infrastructure project without creating a formal legal guarantee. These letters mitigate perceived political risk by confirming the government is aware of the venture and intends to maintain a stable regulatory environment. While they lack the force of a sovereign guarantee, they are crucial for enhancing creditworthiness and securing financing in complex public-private partnerships.

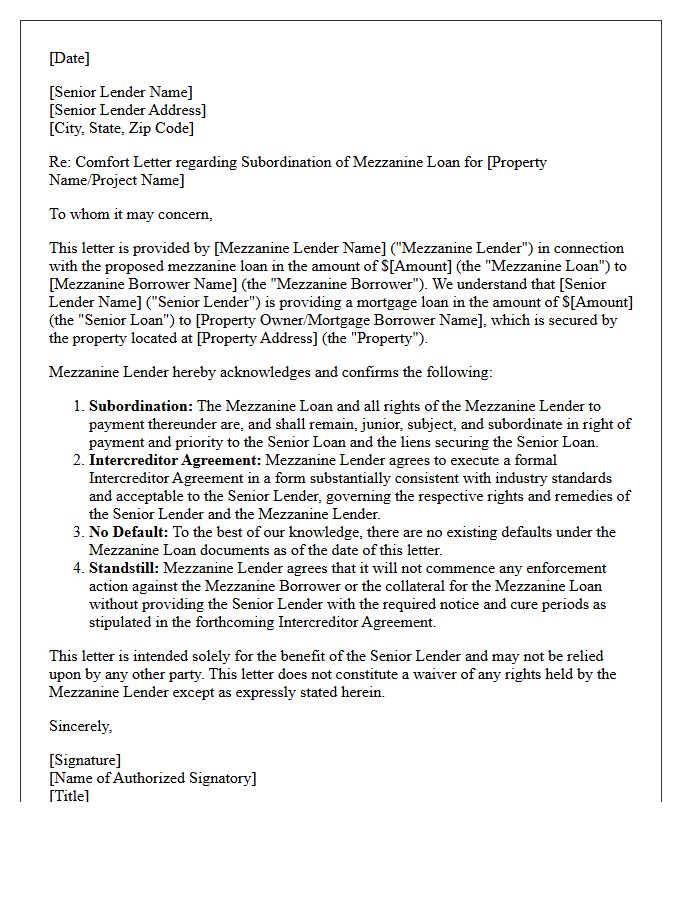

Mezzanine Lender Subordination Comfort Letter

A Mezzanine Lender Subordination Comfort Letter is a crucial legal document where a senior lender acknowledges the mezzanine loan and outlines the priority of debt. It provides structural assurance by defining how junior debt is repaid relative to the senior claim. This letter typically addresses intercreditor dynamics, ensuring the senior lender will not disrupt the mezzanine lender's right to receive payments unless a default occurs. It serves as essential risk mitigation, offering clarity on foreclosure rights and payment waterfalls to protect the mezzanine investor's position within the capital stack.

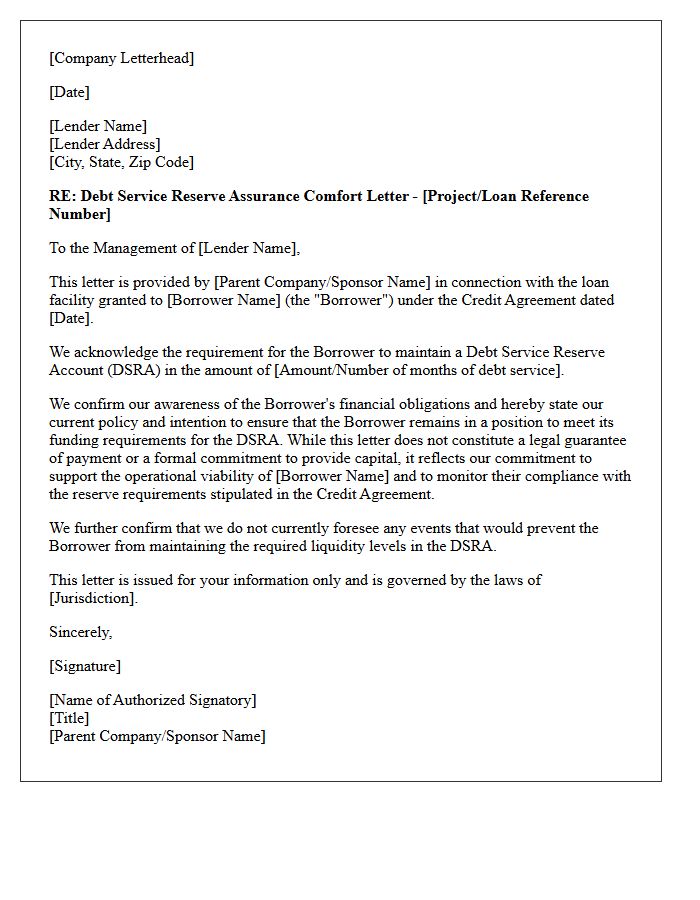

Debt Service Reserve Assurance Comfort Letter

A Debt Service Reserve Assurance Comfort Letter is a formal document issued by a parent company or third party to provide financial reassurance to lenders. It acts as a non-binding commitment to ensure a borrower maintains sufficient liquidity in their reserve accounts. While not a legal guarantee of repayment, it strengthens the borrower's credit profile by demonstrating secondary support to cover interest and principal obligations. This instrument is vital in project finance for mitigating default risk and building trust between stakeholders when formal guarantees are unavailable or restricted.

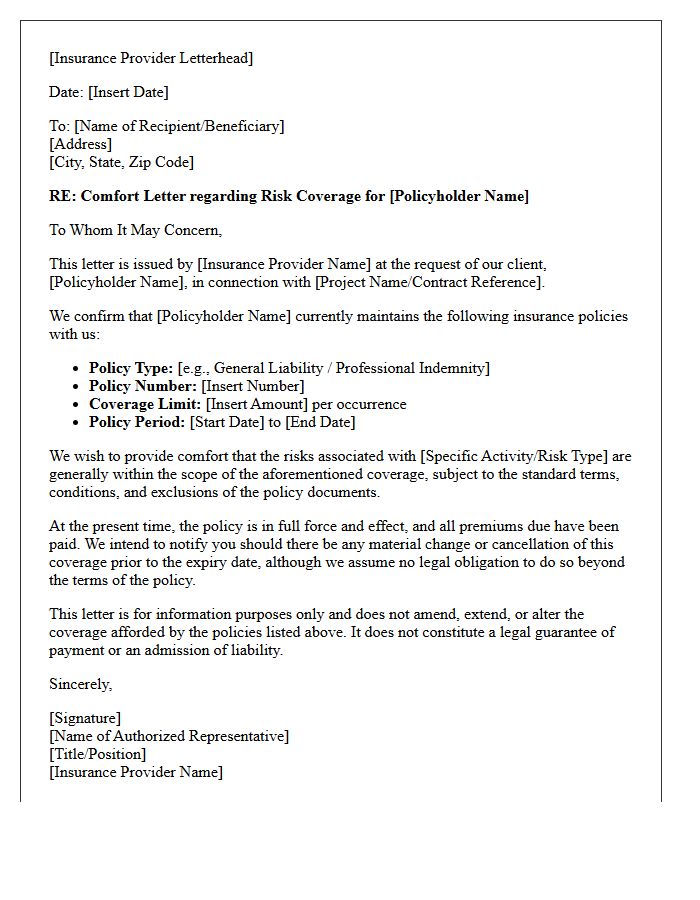

Insurance Provider Risk Coverage Comfort Letter

An Insurance Provider Risk Coverage Comfort Letter is a formal document issued by an insurer to confirm the existence of specific underwriting support. It serves as a non-binding assurance to third parties that a policyholder maintains adequate financial protection for potential liabilities. These letters are crucial in commercial contracts to verify that risks are sufficiently mitigated before project commencement. While not a substitute for a legal policy, it provides a level of professional confidence regarding the insurer's commitment to provide coverage under agreed terms, facilitating smoother business transactions and regulatory compliance.

What is a Comfort Letter in real estate development financing?

A Comfort Letter is a document issued by a parent company or a stakeholder to a lender, providing assurance that a subsidiary or borrower has the financial backing and management support necessary to fulfill its obligations under a development loan. While often not a legally binding guarantee, it serves as a moral and professional commitment to maintain the borrower's solvency during the project lifecycle.

Is a Comfort Letter legally binding for real estate lenders?

The legal enforceability of a Comfort Letter depends on its specific phrasing; most are drafted as statements of intent rather than absolute guarantees. However, courts may interpret certain clauses as binding if they contain definitive language regarding financial support, making it essential for both developers and lenders to have legal counsel review the document's wording.

How does a Comfort Letter differ from a Corporate Guarantee?

Unlike a Corporate Guarantee, which creates an unconditional legal obligation for the guarantor to repay a debt if the borrower defaults, a Comfort Letter typically only confirms a "policy of support." It is often used when a parent company is restricted by internal bylaws or regulatory limits from providing a formal guarantee but still needs to secure financing for a project.

Why do lenders require Comfort Letters for special purpose entities (SPEs)?

Real estate developments are often structured as Special Purpose Entities (SPEs) with limited assets. Lenders require a Comfort Letter from the parent organization to mitigate risk, ensuring that the SPE remains adequately capitalized and that the parent company will not abandon the project if unforeseen costs or market fluctuations occur.

What are the key components of a Comfort Letter for construction financing?

A standard Comfort Letter includes an acknowledgment of the loan terms, a statement of awareness regarding the subsidiary's obligations, a commitment to maintain ownership or control of the borrower, and an assurance that the parent company intends to ensure the borrower remains in a position to meet its financial commitments.

Comments