A Residential Mortgage Commitment Letter is a formal document issued by a lender confirming your home loan approval under specific terms. It outlines the interest rate, loan amount, and final conditions required before closing. Securing this letter is a critical milestone in the home-buying process, signaling financial readiness to sellers. To help you draft or review one, below are some ready to use template.

Image cover: Essential Guide to Residential Mortgage Commitment Letter Samples and Templates

Letter Samples List

- Standard Residential Mortgage Commitment Letter

- Conditional Residential Mortgage Commitment Letter

- Firm Residential Mortgage Commitment Letter

- Final Residential Mortgage Commitment Letter

- Revised Residential Mortgage Commitment Letter

- Amended Residential Mortgage Commitment Letter

- Extended Residential Mortgage Commitment Letter

- Expired Residential Mortgage Commitment Letter

- Withdrawn Residential Mortgage Commitment Letter

- Rate Lock Residential Mortgage Commitment Letter

- Conventional Residential Mortgage Commitment Letter

- Jumbo Residential Mortgage Commitment Letter

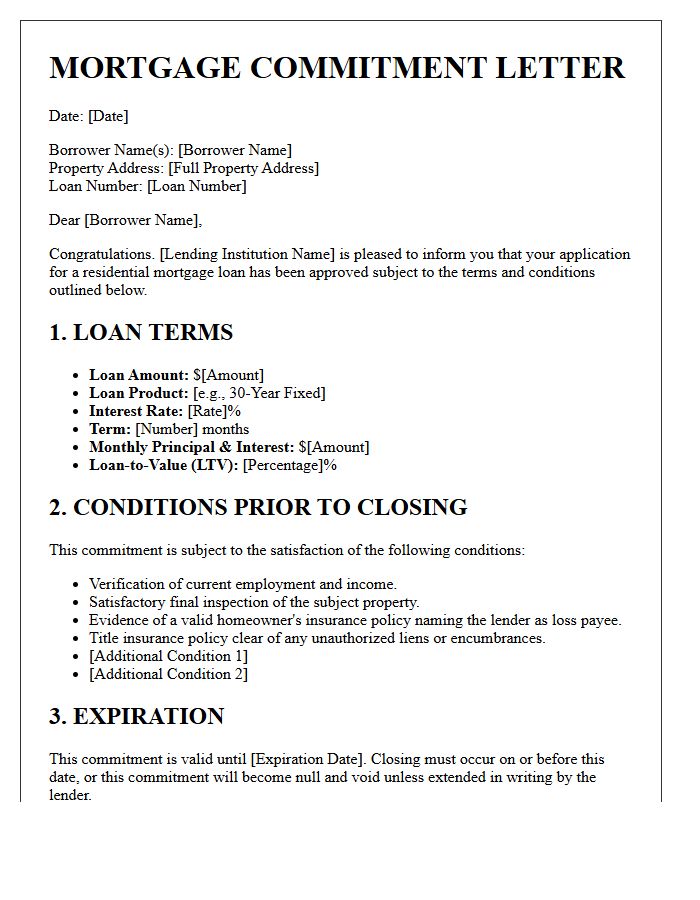

Standard Residential Mortgage Commitment Letter

A standard residential mortgage commitment letter is a legally binding document issued by a lender, confirming your loan approval subject to specific underwriting conditions. This document outlines critical financial details, including the total loan amount, interest rate, and required down payment. It signifies that the lender has verified your financial profile and is committed to funding the home purchase. Borrowers must carefully review the expiration date and any outstanding contingencies, such as property appraisals or proof of insurance, to ensure a successful closing process within the specified timeframe.

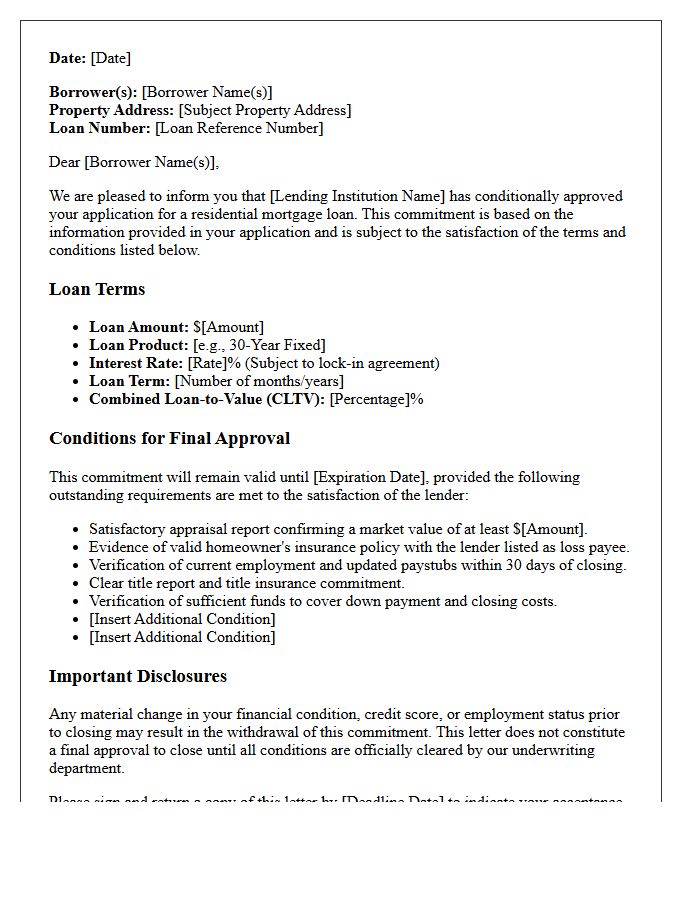

Conditional Residential Mortgage Commitment Letter

A Conditional Residential Mortgage Commitment Letter is a formal document from a lender indicating approval for a loan, provided specific underwriting requirements are met. It outlines critical details like the interest rate, loan amount, and expiration date. To finalize the financing, borrowers must satisfy outstanding conditions, such as property appraisals, proof of insurance, or updated financial verification. Receiving this letter is a significant milestone in the home-buying process, signaling that the bank is prepared to fund the mortgage once all contingencies are cleared.

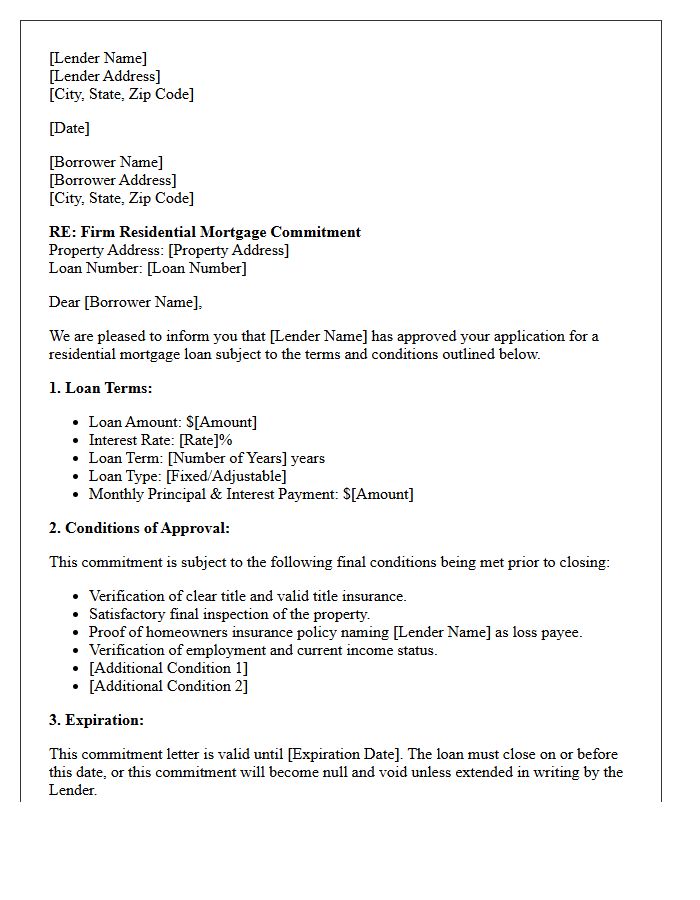

Firm Residential Mortgage Commitment Letter

A firm residential mortgage commitment letter is a legally binding agreement issued by a lender after completing a full underwriting process. Unlike a pre-approval, this document guarantees that your loan is approved for a specific property, provided you satisfy any minor outstanding conditions before closing. It outlines critical details including the final interest rate, loan amount, and expiration date. Receiving this letter is the final milestone in the financing process, signaling to sellers that your funding is guaranteed and you are ready to complete the home purchase.

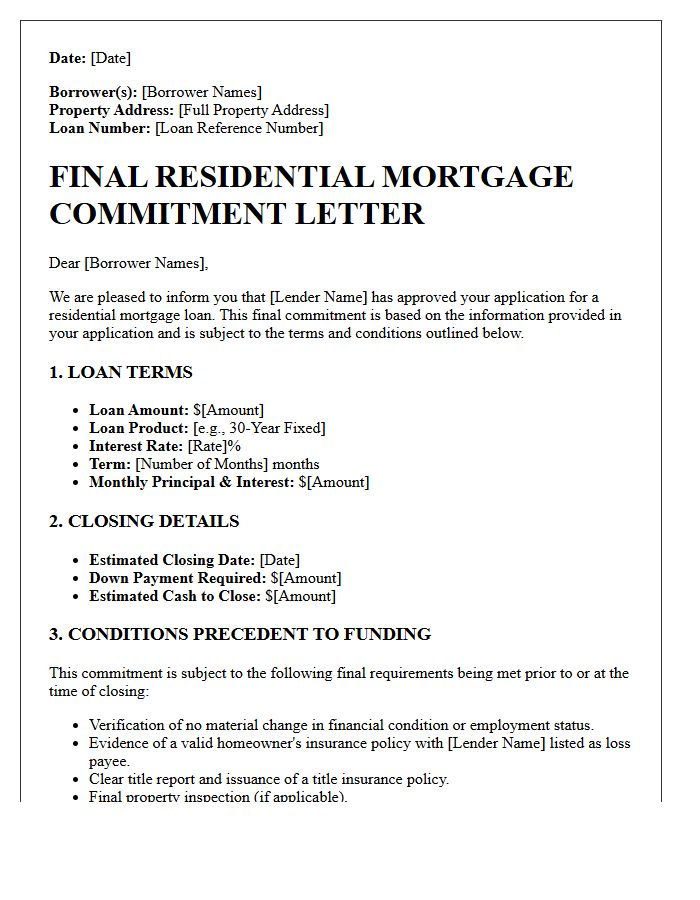

Final Residential Mortgage Commitment Letter

A final residential mortgage commitment letter is a binding agreement issued by a lender after successful underwriting. It confirms that your loan is officially approved, subject to specific closing conditions. Unlike a pre-approval, this document signifies that the lender has verified your financial data, appraisal, and title. Borrowers must review the interest rate, loan terms, and expiration date carefully. Once you sign and return this letter, you move toward the final closing disclosure and funding stage, marking the final hurdle in the home-buying process.

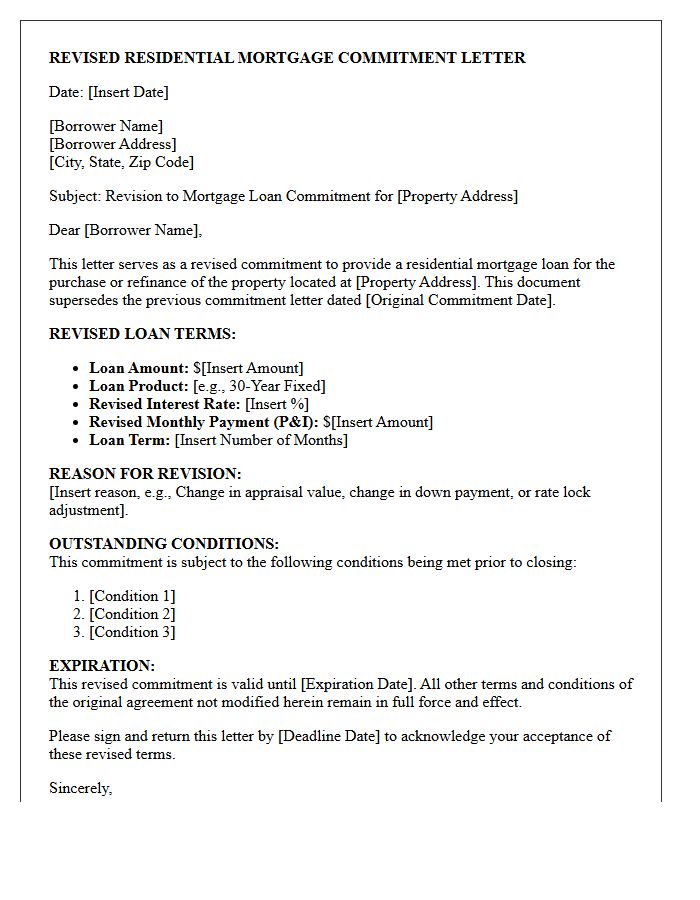

Revised Residential Mortgage Commitment Letter

A Revised Residential Mortgage Commitment Letter is a formal document issued by a lender when loan terms change after the initial approval. It reflects updates to the interest rate, loan amount, or closing conditions due to appraisal results or financial shifts. Borrowers must review this document carefully, as it replaces previous agreements and contains binding requirements that must be met before funding. Timely acknowledgment is essential to ensure the mortgage closing stays on schedule and complies with all updated underwriting criteria.

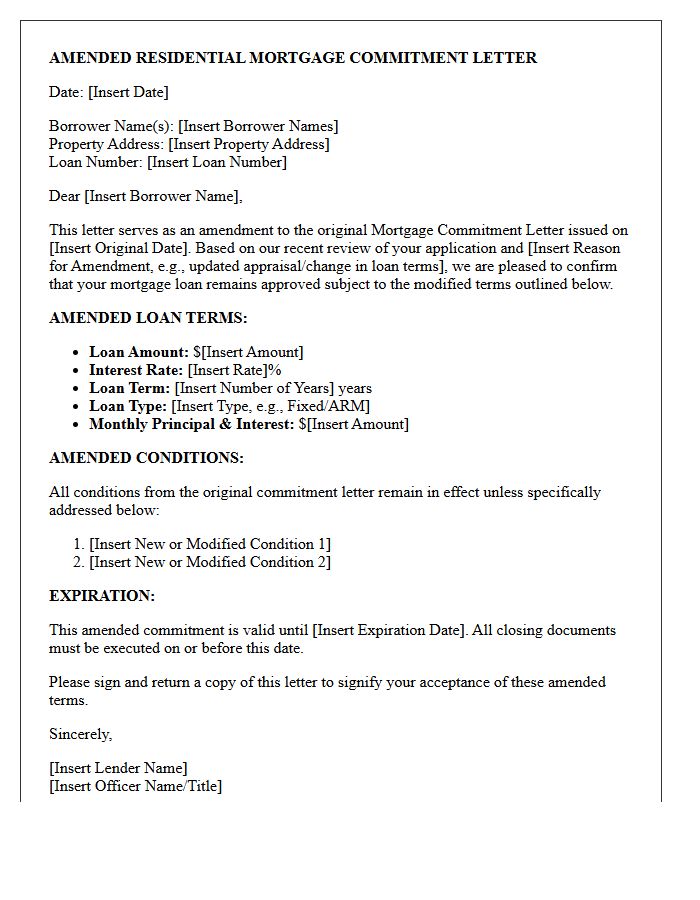

Amended Residential Mortgage Commitment Letter

An Amended Residential Mortgage Commitment Letter is a formal document issued by a lender that modifies the terms of an original loan approval. This update typically occurs due to changes in interest rates, loan amounts, or updated property appraisals. It is crucial for borrowers to review these revisions carefully, as they represent the final binding agreement before closing. Ensuring all contingencies are met within the new timeframe is essential to secure funding and avoid delays in the home-buying process.

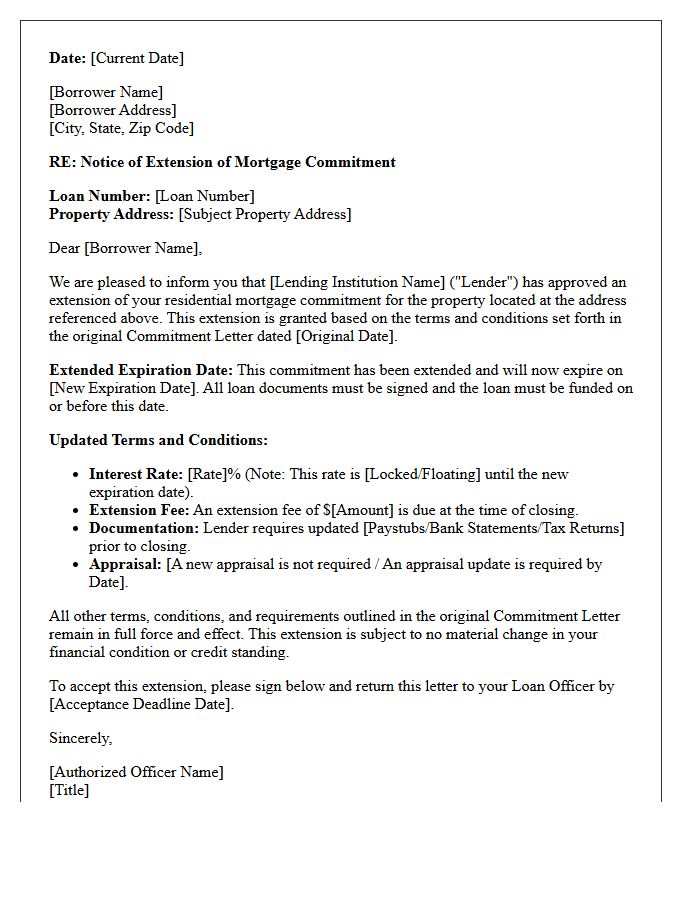

Extended Residential Mortgage Commitment Letter

An Extended Residential Mortgage Commitment Letter is a formal agreement from a lender to provide financing for a period typically exceeding the standard 90 days. This document is essential for new construction projects where the completion date is far in the future. It guarantees specific interest rate locks or loan terms, protecting buyers from market volatility during the build. Borrowers must ensure all contingencies are met and verify if additional fees apply to maintain the commitment through the extended duration.

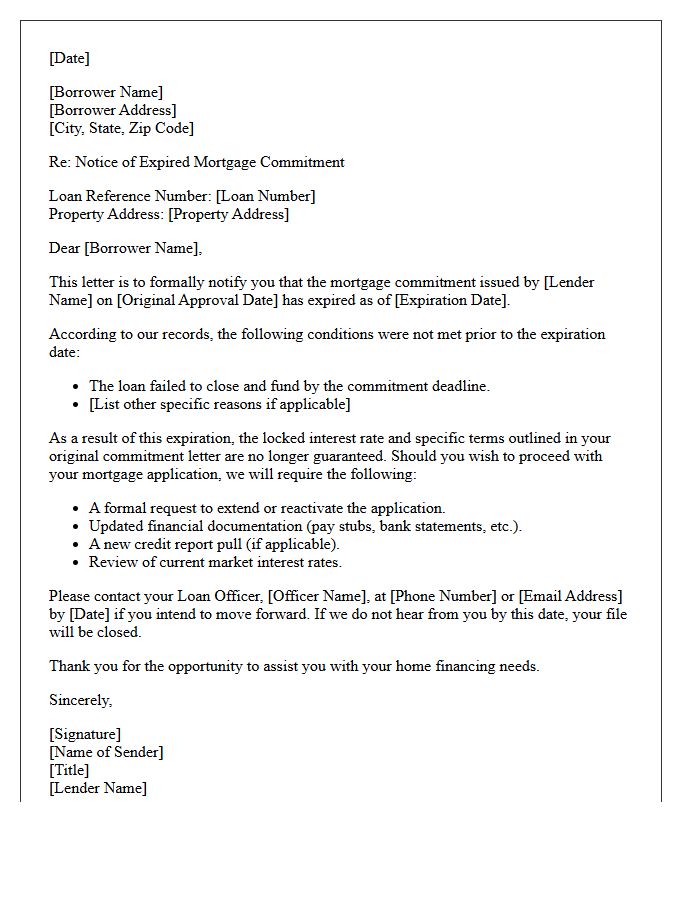

Expired Residential Mortgage Commitment Letter

An expired residential mortgage commitment letter means the lender's formal offer to fund your loan has voided due to passing the expiration date. This typically occurs because of closing delays or incomplete documentation. Once expired, the interest rate and terms are no longer guaranteed, potentially requiring a re-approval process or a rate lock extension. It is critical to monitor this deadline closely to avoid higher costs or losing the financing necessary to finalize your home purchase.

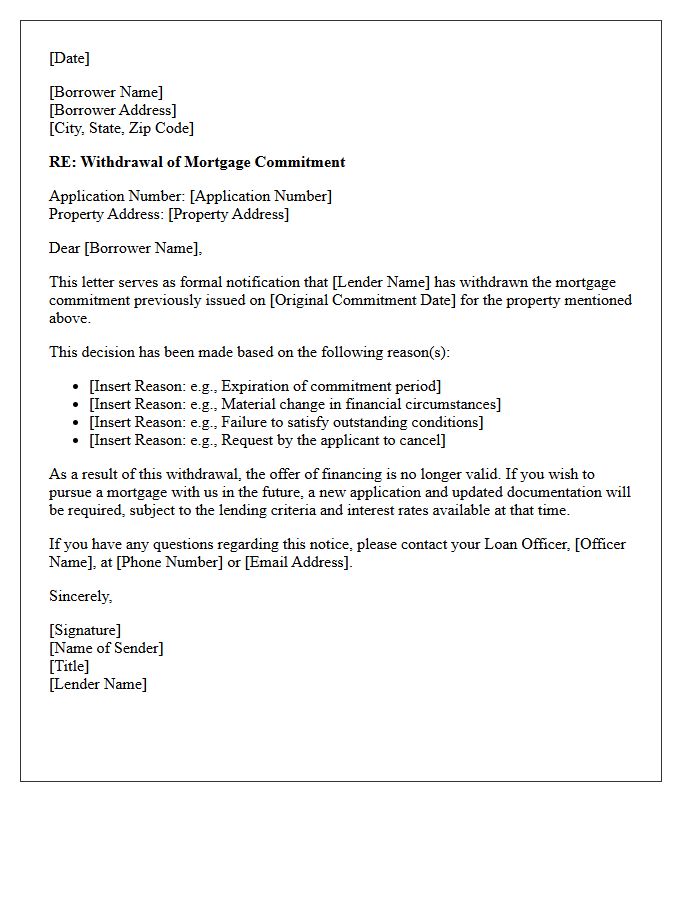

Withdrawn Residential Mortgage Commitment Letter

A Withdrawn Residential Mortgage Commitment Letter occurs when a lender cancels a formal loan offer before closing. This typically happens due to negative changes in the borrower's credit score, loss of employment, or issues discovered during the final property appraisal. It is crucial to maintain financial stability and avoid new debts after receiving a commitment. Understanding the expiration date and specific conditions within the letter is vital, as any breach of terms allows the financial institution to legally rescind their promise to fund your home purchase.

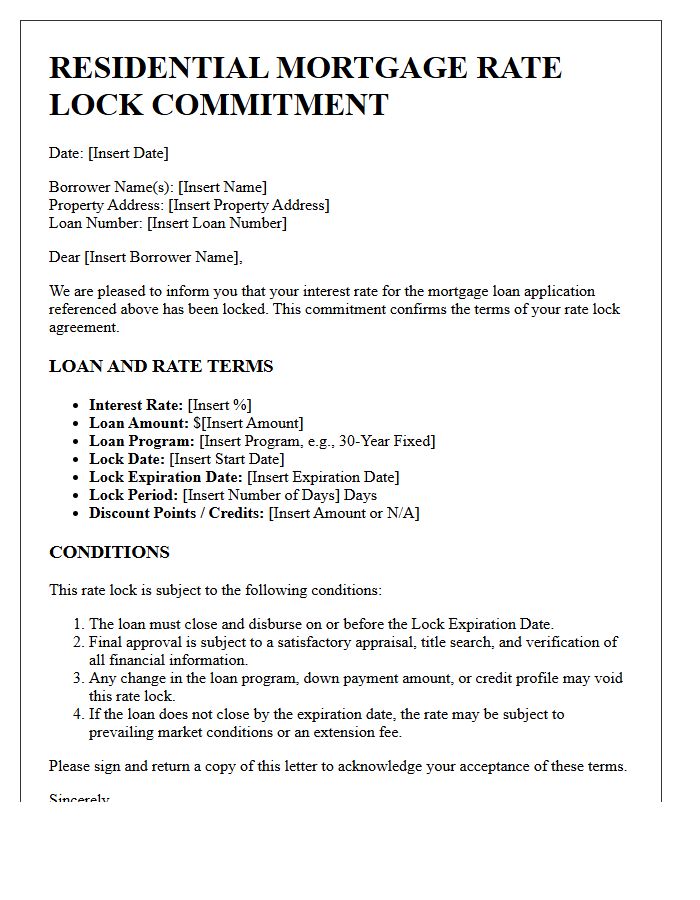

Rate Lock Residential Mortgage Commitment Letter

A residential mortgage commitment letter with a rate lock is a formal agreement from a lender guaranteeing a specific interest rate for a set period. This protection shields borrowers from market fluctuations while their loan is processed. It is essential to monitor the expiration date, as failing to close before the lock expires could result in higher monthly payments or additional extension fees. Always review the lock-in agreement terms to understand any conditions or potential adjustments required to maintain your secured financing rate during the homebuying journey.

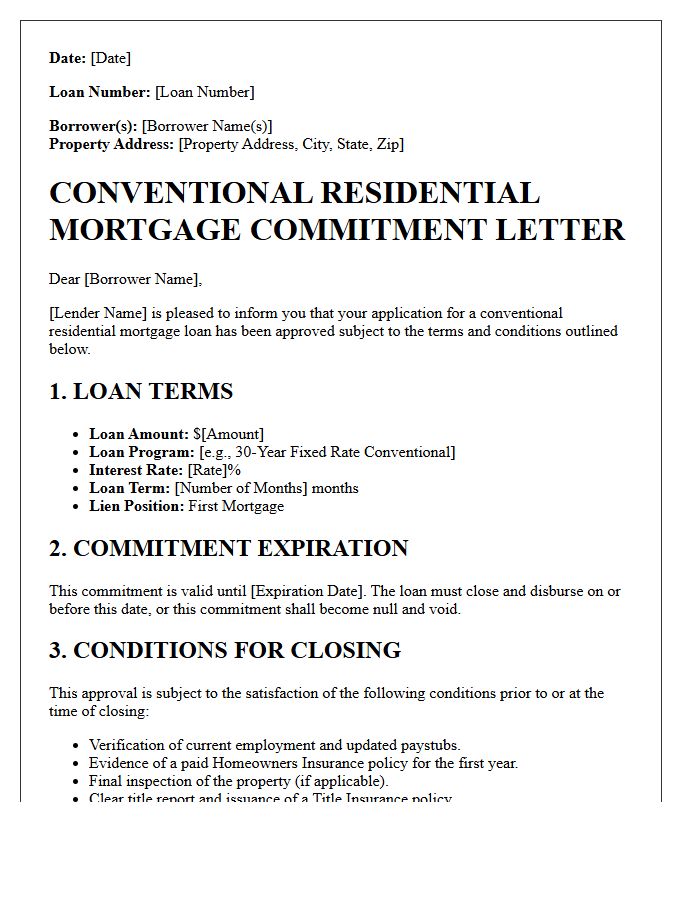

Conventional Residential Mortgage Commitment Letter

A conventional residential mortgage commitment letter is a legally binding agreement issued by a lender after full underwriting approval. Unlike a pre-approval, it guarantees financing under specific terms and interest rates, provided all conditions precedent are met before closing. This document confirms the borrower's creditworthiness and the property's value. It is the final milestone for buyers, signaling to sellers that the loan is secure. Key details include the loan-to-value ratio, expiration date, and any outstanding requirements, such as final inspections or updated financial statements, necessary to fund the mortgage.

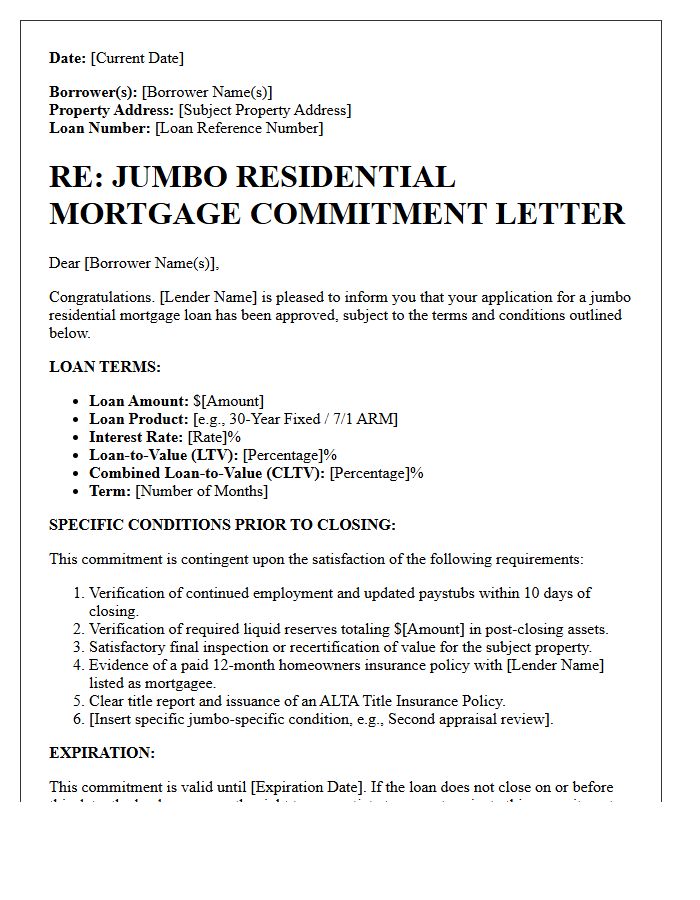

Jumbo Residential Mortgage Commitment Letter

A Jumbo Residential Mortgage Commitment Letter is a formal document issued by a lender confirming approval for a loan exceeding conforming limits. Unlike pre-approvals, this binding agreement outlines specific financial terms, interest rates, and expiration dates. To ensure final funding, borrowers must satisfy all underwriting conditions, such as updated appraisals or asset verification. Receiving this letter is a critical milestone, signaling that the lender is legally committed to financing your high-value property purchase, provided no significant changes occur in your credit profile before the scheduled closing date.

What is a residential mortgage commitment letter?

A residential mortgage commitment letter is a formal document issued by a lender stating they have approved a borrower for a home loan under specific terms and conditions. It serves as a binding agreement that the lender will provide the funds, provided all stated requirements are met before the closing date.

What is the difference between a pre-approval and a mortgage commitment letter?

A pre-approval is a preliminary assessment based on unverified or basic data, whereas a mortgage commitment letter is issued after a full underwriting review of the borrower's financial documents and the property's appraisal. The commitment letter is a much stronger guarantee of financing than a pre-approval.

What common conditions are found in a mortgage commitment letter?

Common conditions often include a satisfactory property appraisal, proof of homeowners insurance, verification of employment, no significant changes to the borrower's credit score, and documentation of the source of the down payment. All "prior-to-closing" conditions must be cleared for the loan to fund.

Can a lender withdraw a mortgage commitment letter?

Yes, a lender can withdraw a commitment letter if the borrower's financial situation changes significantly, such as job loss or taking on new debt. It can also be revoked if the property fails inspection, the appraisal comes in too low, or if any fraudulent information is discovered during the final verification process.

How long is a mortgage commitment letter valid?

A mortgage commitment letter typically has an expiration date ranging from 30 to 90 days. This period is designed to align with the lock-in period of the interest rate and the expected closing date of the real estate transaction. If the loan does not close by this date, the borrower may need to re-apply or request an extension.

Comments