A Notice of Servicing Transfer informs borrowers that a new company will manage their debt. When loans are in default, this transition requires clear communication regarding payment history and loss mitigation options. Understanding your rights during this move is essential for effective debt resolution. To assist your outreach efforts, below are some ready to use template.

Image cover: Official Notice: Transfer of Servicing for Loans in Default and Required Templates

Letter Samples List

- Notice of Servicing Transfer for Defaulted Mortgage Letter

- RESPA Compliant Servicing Transfer Letter for Delinquent Account

- Introductory Default Servicer Transfer Letter

- Loss Mitigation Transition and Servicing Transfer Letter

- Post-Default Mortgage Servicing Reassignment Letter

- Pre-Foreclosure Servicing Transfer Notification Letter

- New Servicer Introduction Letter for Defaulted Loan

- Notice of Assignment and Servicing Transfer Letter

- Delinquent Mortgage Servicing Transfer Acknowledgment Letter

- Transfer of Servicing Rights Letter for Non-Performing Loan

- Successor Servicer Notice Letter for Defaulted Mortgage

- Goodbye Letter for Defaulted Mortgage Servicing Transfer

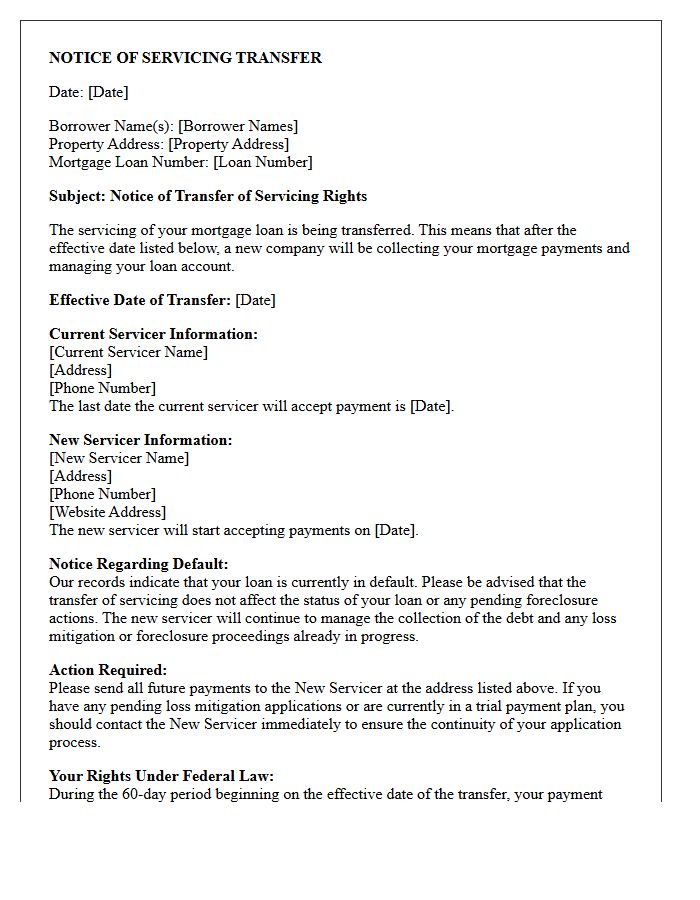

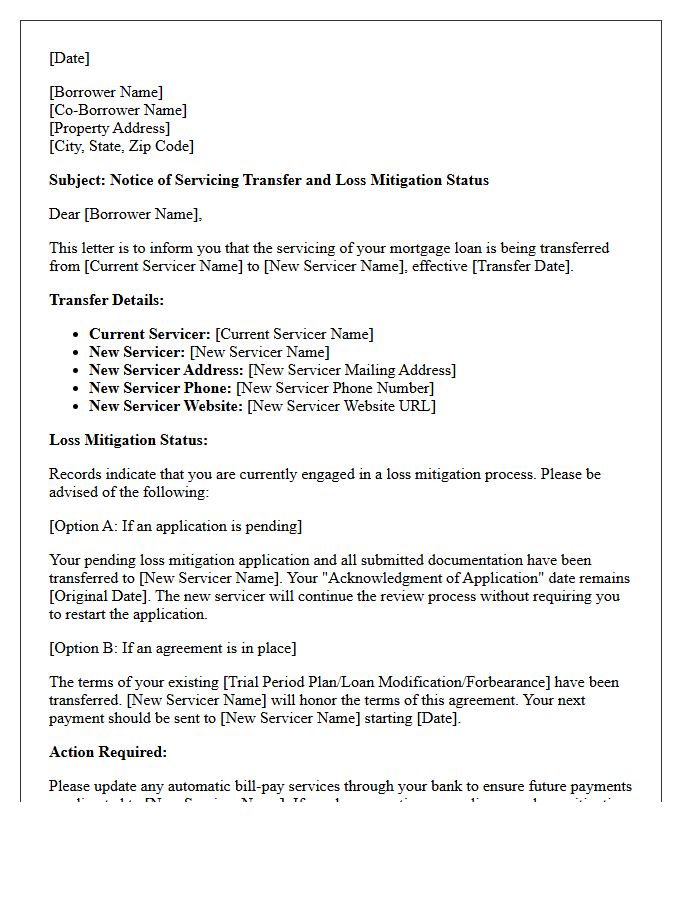

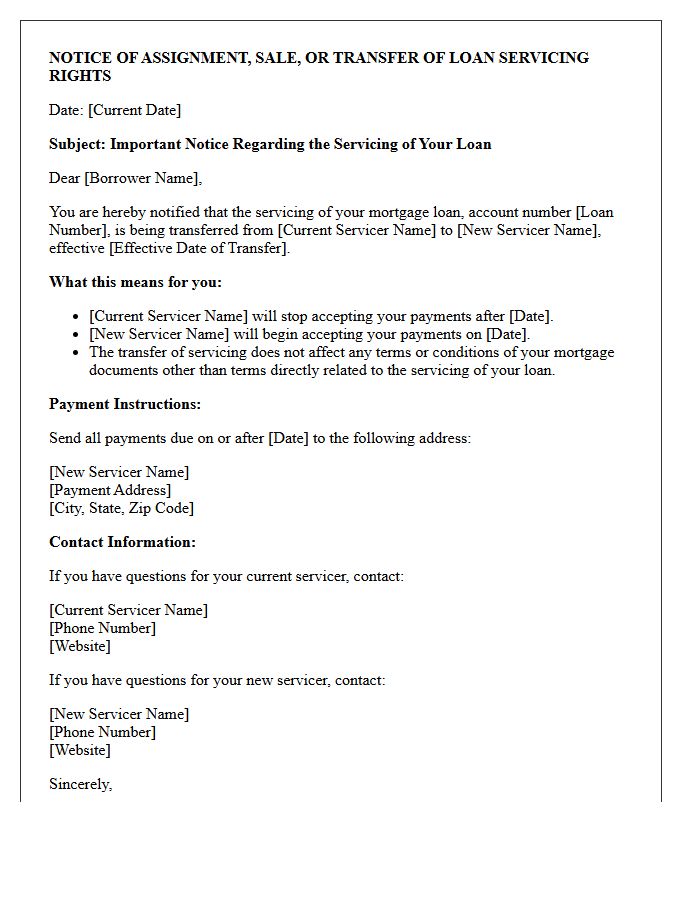

Notice of Servicing Transfer for Defaulted Mortgage Letter

A Notice of Servicing Transfer informs you that a new company will now manage your loan payments and loss mitigation. If your mortgage is in default, this letter is critical because it identifies the new loan servicer responsible for evaluating your foreclosure alternatives. By law, you get a 60-day grace period where payments sent to the old servicer cannot be deemed late. You must contact the new entity immediately to resume loan modification talks or repayment plans to protect your home from legal action.

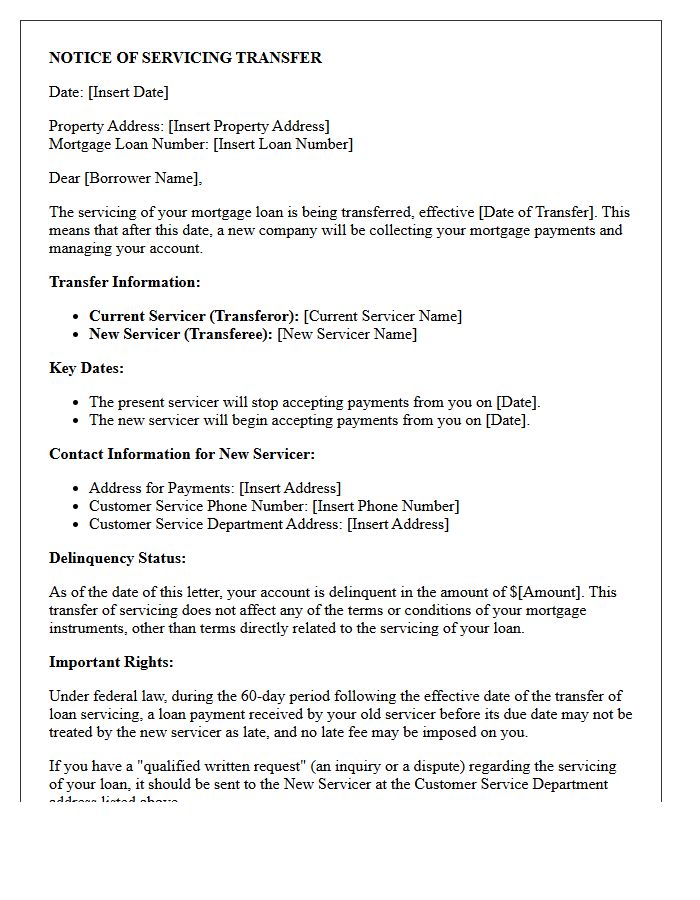

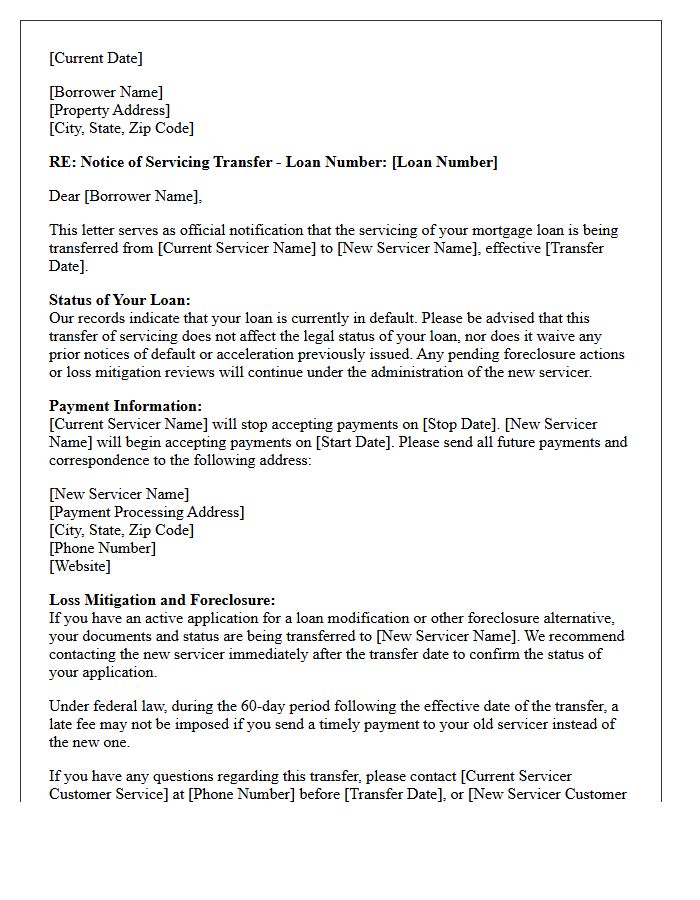

RESPA Compliant Servicing Transfer Letter for Delinquent Account

When sending a RESPA compliant servicing transfer letter for a delinquent account, you must provide a Notice of Transfer to the borrower at least 15 days before the effective date. The letter must detail the new servicer's contact information, the transfer date, and the date the current servicer will stop accepting payments. Crucially, during the 60-day grace period following the transfer, a late fee cannot be charged if the payment was sent to the previous servicer on time, ensuring consumer protection during the transition.

Introductory Default Servicer Transfer Letter

An Introductory Default Servicer Transfer Letter is a critical formal notice sent to borrowers when the management of a delinquent mortgage changes hands. This document confirms the transfer of servicing rights from the current company to a new entity. It outlines essential details, including the new payment address, contact information, and the effective date of the transition. Reviewing this letter ensures you avoid payment misdirection and maintain communication during loss mitigation. Understanding your legal protections under the Real Estate Settlement Procedures Act (RESPA) is vital during this transition period.

Loss Mitigation Transition and Servicing Transfer Letter

A Loss Mitigation Transition occurs when your mortgage servicer changes while you are seeking payment relief. The most critical document is the Servicing Transfer Letter, often called a "Goodbye Letter." Federal law requires the new servicer to honor existing trial period plans or completed modification agreements. Carefully monitor your mail to ensure the new company receives your documents promptly, as continuity of contact is essential to prevent foreclosure during the transition period. Always verify the effective date of transfer to avoid payment delays or processing errors.

Post-Default Mortgage Servicing Reassignment Letter

A Post-Default Mortgage Servicing Reassignment Letter is a formal notification sent to borrowers when a delinquent loan is transferred to a specialized servicer. This document outlines the transfer of rights to collect payments and manage the foreclosure process. It is critical to verify the new entity's contact details to avoid scams and ensure payment accuracy. Understanding this transition is essential for homeowners seeking loss mitigation options or loan modifications to prevent final foreclosure, as the new servicer becomes the primary point of contact for all debt resolution activities.

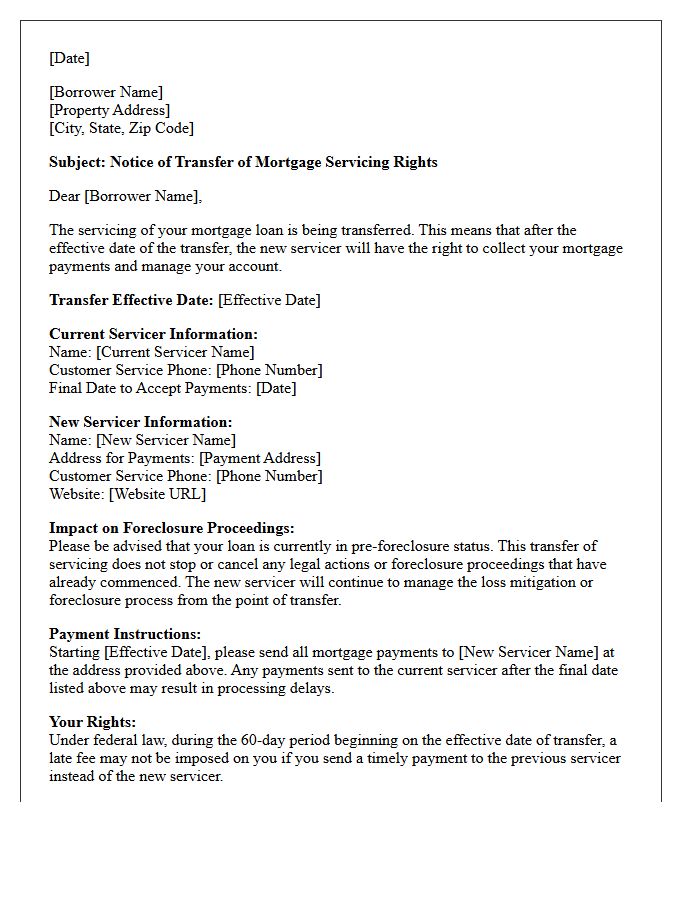

Pre-Foreclosure Servicing Transfer Notification Letter

A Pre-Foreclosure Servicing Transfer Notification Letter is a formal legal notice sent when the management of your mortgage changes hands during delinquency. This document informs you that a new loan servicer will now handle your payments and loss mitigation requests. It is critical to verify the effective transfer date and the new mailing address to ensure your repayment negotiations continue without interruption. Always confirm the letter's authenticity to avoid scams and ensure your legal rights are protected during the transition process.

New Servicer Introduction Letter for Defaulted Loan

A New Servicer Introduction Letter is a critical legal notice informing you that the management of your defaulted loan has changed. It identifies your new point of contact for payment processing and debt resolution. This document officially initiates the transfer of ownership or servicing rights, outlining where to send future payments. It is essential to verify the details to avoid identity theft or scams. Reviewing this letter immediately helps you understand available loss mitigation options and prevents further delinquency during the transition period.

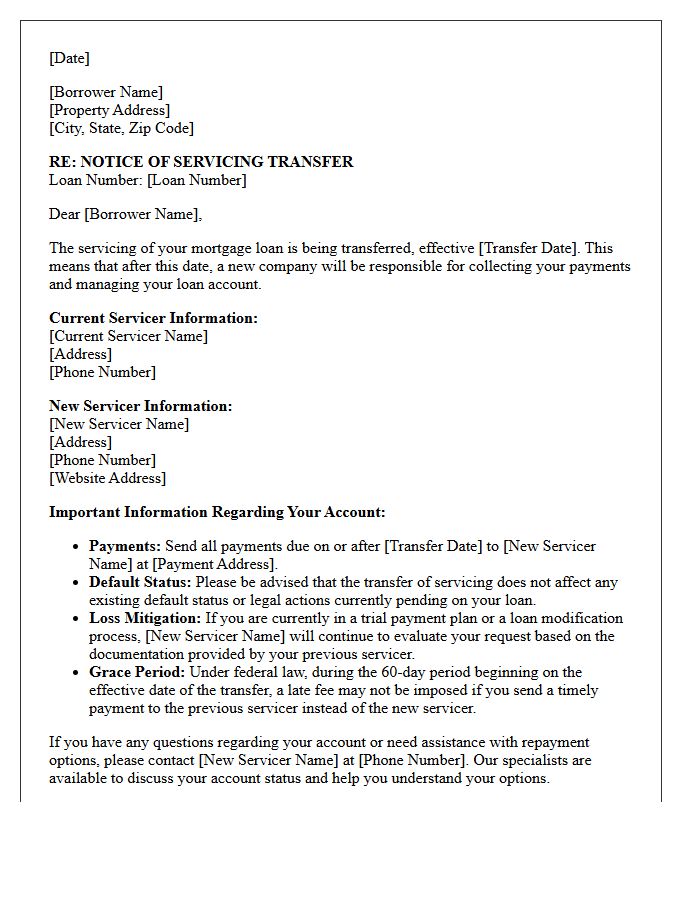

Notice of Assignment and Servicing Transfer Letter

When your mortgage is sold, you will receive a Notice of Assignment and a Servicing Transfer Letter. These legal documents inform you that a new company now manages your loan payments and escrow account. It is crucial to verify the effective transfer date and the new mailing address to avoid missed payments. By law, you have a 60-day grace period where late fees cannot be charged if you accidentally pay the old servicer. Always confirm the new servicer's legitimacy through your original lender to prevent potential payment fraud.

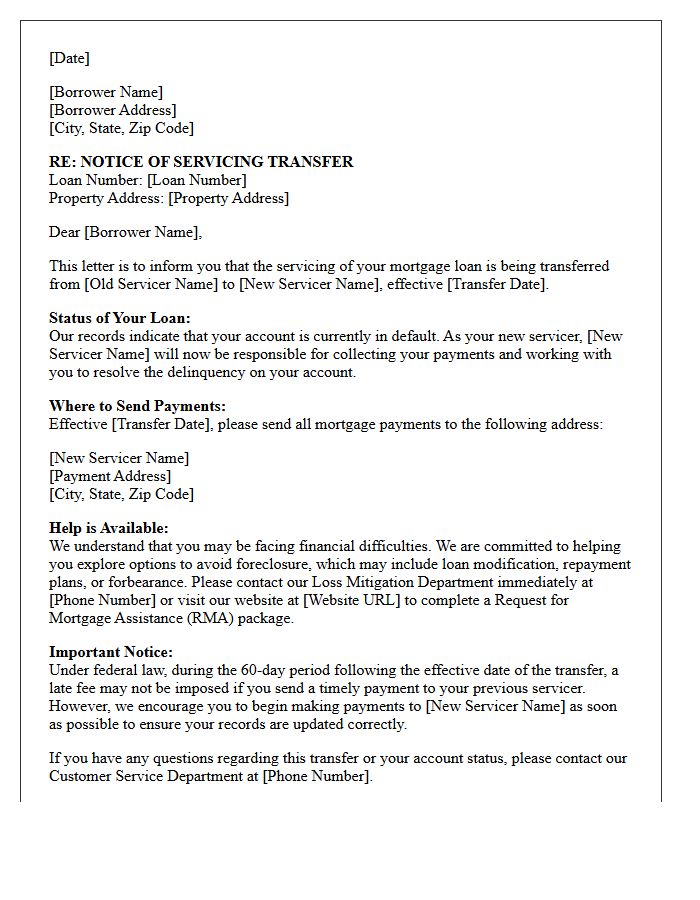

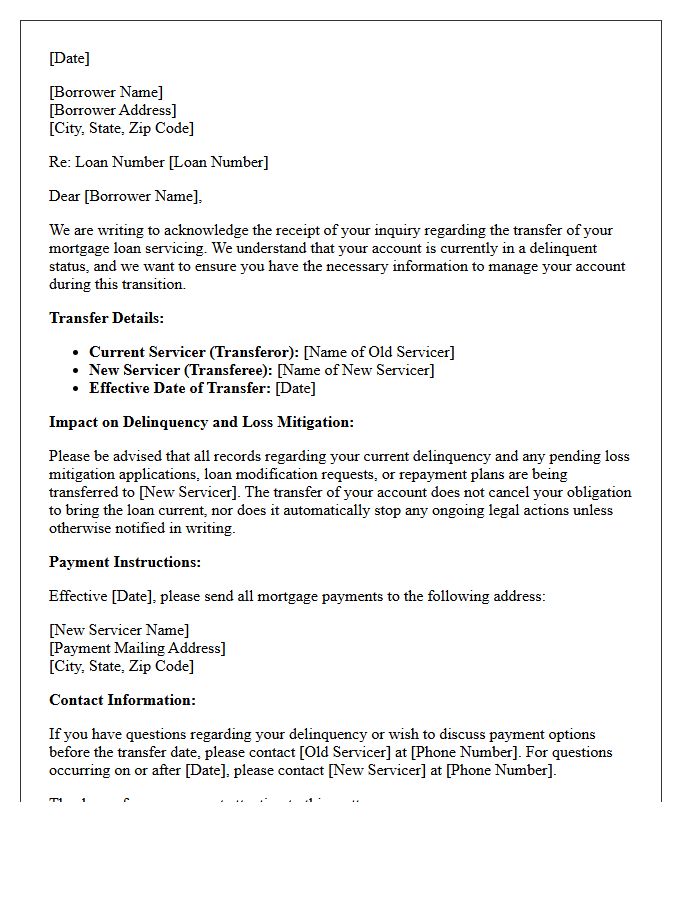

Delinquent Mortgage Servicing Transfer Acknowledgment Letter

A Delinquent Mortgage Servicing Transfer Acknowledgment Letter is a critical legal notice sent when your past-due loan is moved to a new servicer. It confirms that the new company is now responsible for collecting payments and managing your loss mitigation applications. To protect your rights, you must verify the effective transfer date and ensure all previous repayment plans or loan modification terms are honored. Acting quickly upon receipt helps prevent foreclosure and ensures your credit reporting remains accurate during the transition between mortgage lenders.

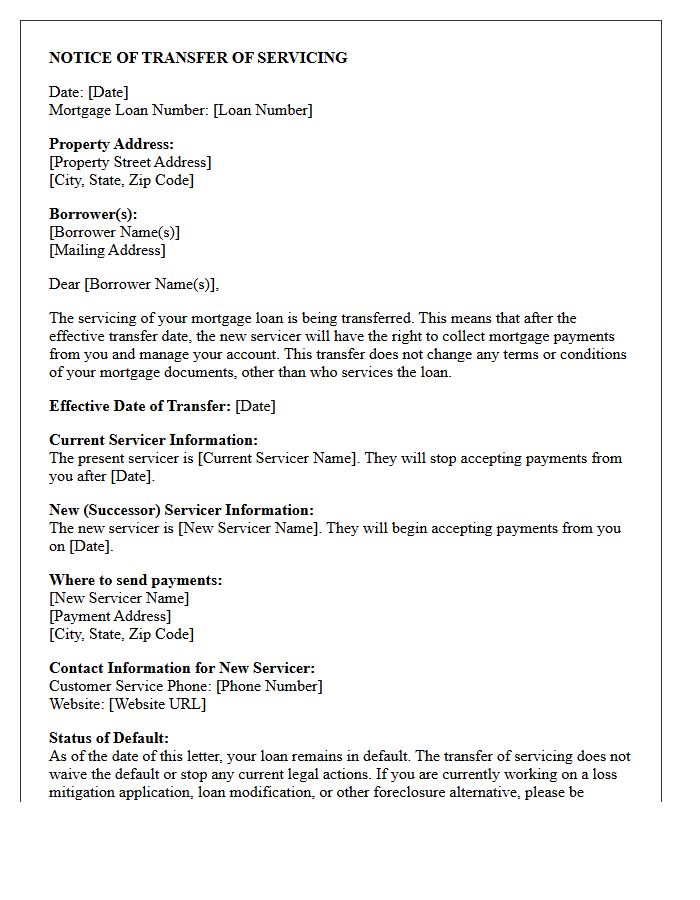

Transfer of Servicing Rights Letter for Non-Performing Loan

A Transfer of Servicing Rights Letter is a critical legal notice informing borrowers that a new company will manage their Non-Performing Loan. This document confirms the effective date of the transition and provides updated contact information for payment processing. For distressed debts, it is essential to verify the Notice of Transfer to prevent fraud and ensure loss mitigation applications remain active. Borrowers must acknowledge the new servicer to resume debt resolution efforts or restructuring negotiations, as the previous servicer no longer holds authority over the account's administration or foreclosure proceedings.

Successor Servicer Notice Letter for Defaulted Mortgage

A Successor Servicer Notice Letter is a critical legal document issued when a defaulted mortgage is transferred between financial institutions. It informs the homeowner that a new entity now manages their debt and loss mitigation options. This notice is essential for maintaining your legal rights under the Real Estate Settlement Procedures Act (RESPA). You must verify the new servicer's identity to avoid scams and ensure foreclosure prevention applications are correctly transitioned. Timely communication with the successor is vital to negotiating loan modifications or repayment plans to save your property from auction.

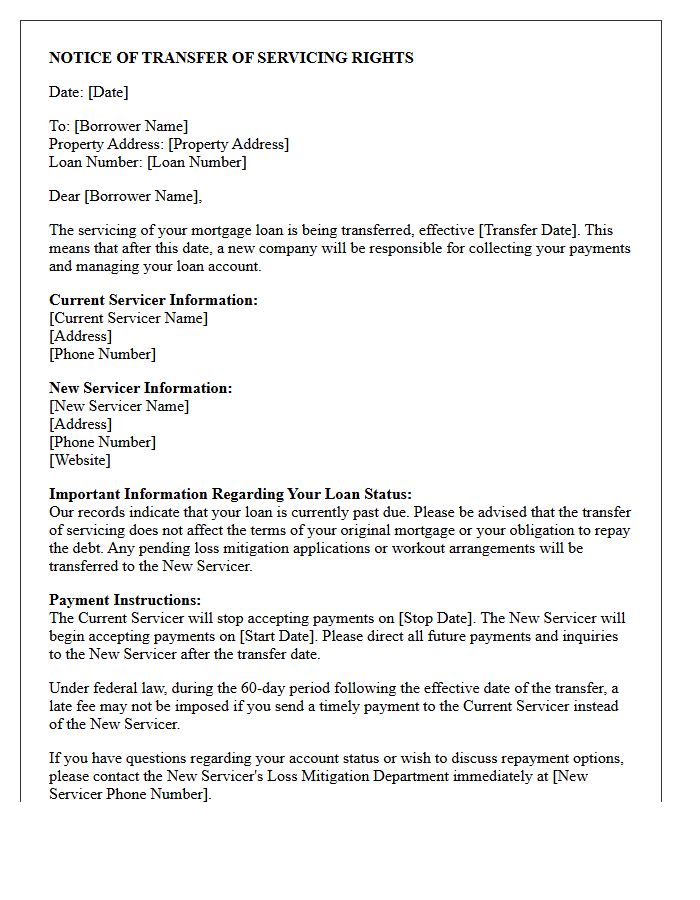

Goodbye Letter for Defaulted Mortgage Servicing Transfer

When receiving a Goodbye Letter, it signifies that your mortgage servicer is transferring management of your account to a new entity. For a defaulted mortgage, this notice is critical as it identifies the new contact for loan modifications or loss mitigation. Ensure you verify the effective transfer date and the new payment address to avoid further delinquency. Under federal law, you have a 60-day grace period where late fees cannot be charged if payments are mistakenly sent to the previous servicer during the transition.

What is a Notice of Servicing Transfer for a loan in default?

A Notice of Servicing Transfer is a formal communication informing a borrower that the responsibility for managing their mortgage loan, including collecting payments and managing loss mitigation, is moving from the current servicer to a new company.

Does a servicing transfer change the terms of my defaulted loan or loss mitigation plan?

No, a transfer of servicing does not change the legal terms of your original promissory note or mortgage. If you have an active trial payment plan or a permanent loan modification agreement, the new servicer is generally required to honor those existing terms.

Who should I contact about my pending foreclosure or loss mitigation application during a transfer?

During the transition period, you should contact the "new servicer" listed on your transfer notice. Both the old and new servicers are required to coordinate the transfer of all documentation, including active loss mitigation applications and foreclosure sale holds.

Can I be charged late fees immediately after my loan is transferred to a new servicer?

Under federal law (RESPA), there is a 60-day "safe harbor" period beginning on the effective date of the transfer. During these 60 days, a new servicer cannot charge late fees or report a payment as late if you sent the on-time payment to the old servicer by mistake.

Where do I send my mortgage payments if my loan is in default during a servicing transfer?

You must send payments to the old servicer until the "effective date" listed in your Goodbye Letter, and to the new servicer after that date. If your loan is in default, ensure you use the specific address provided for "Default or Loss Mitigation Payments" to avoid processing delays.

Comments